|

시장보고서

상품코드

2065445

프리보딩 및 온보딩 자동화 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Preboarding And Onboarding Automation Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

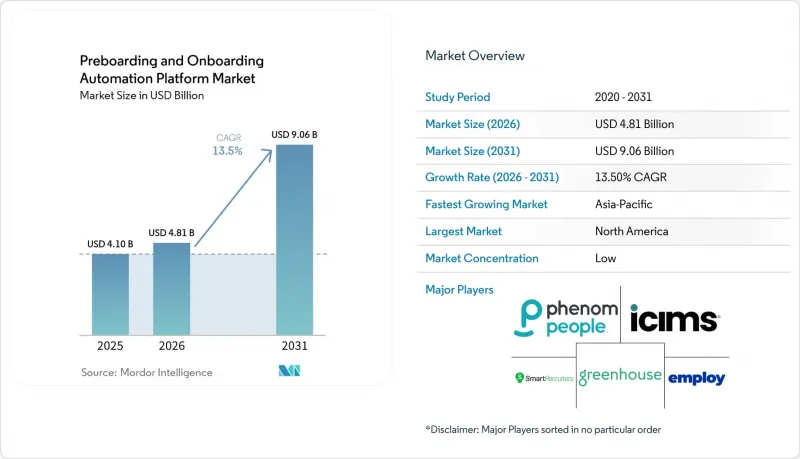

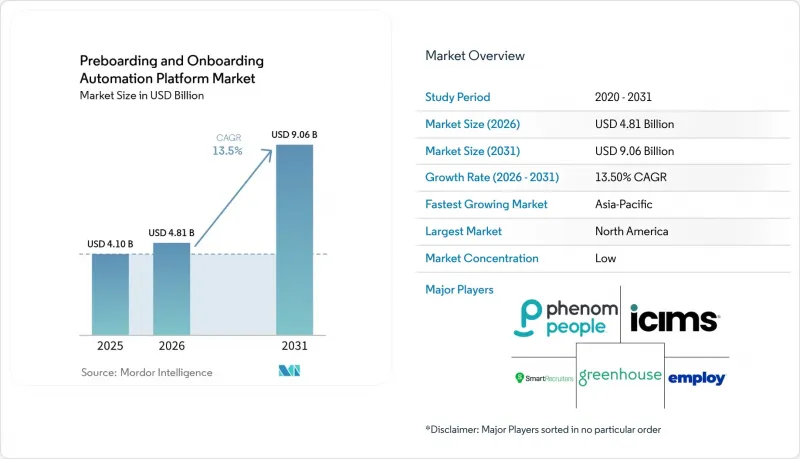

프리보딩 및 온보딩 자동화 플랫폼 시장 규모는 2025년 41억 달러로 평가되었고, 2026년 48억 1,000만 달러로 추정되고, 2031년까지 90억 6,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 13.50%를 나타낼 전망입니다.

본 보고서는 도입 모델별(클라우드 기반, 온프레미스형, 하이브리드형), 기업 규모별(대기업 등), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학 등), 기능별(채용부터 입사 전 준비 과정까지의 자동화, 서류 작성·검증 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 프리보딩 및 온보딩 자동화 플랫폼 시장 동향 및 인사이트

수동 인사 워크플로우에서 디지털 직원 여정으로의 전환

수동 조정에서 체계화된 디지털 워크플로로 전환하는 것은 프리보딩 및 온보딩 자동화 플랫폼 시장에서 여전히 가장 뚜렷한 성장 요인으로 작용하고 있습니다. 기존의 온보딩 절차는 이메일을 통한 후속 조치, 서로 연계되지 않은 체크리스트, 인사·IT·법무·시설 관리 각 부서의 개별적인 대응에 의존하고 있었기 때문에 채용 인원 증가에 따라 지연을 피할 수 없었습니다. 현재 고용주들은 내정 수락 직후부터 시작하여 서류 절차, 접근 권한 설정, 첫 출근 준비에 이르기까지 일관되게 이어지는 단일 워크플로우를 원하고 있습니다. 이러한 단계들이 통합됨에 따라, 인수 기업은 완료 현황의 격차나 초기 경험의 징후를 보다 명확하게 파악할 수 있게 되며, 온보딩은 단순한 행정 절차에 그치지 않고 인재 유지 관리 측면에서도 더욱 유용한 과정이 됩니다. 워크플로우 완료를 보다 신속한 업무 준비 태세와 측정 가능한 비용 절감으로 연결할 수 있는 벤더는 프리보딩 및 온보딩 자동화 플랫폼 시장에서 구매 기업들의 주목을 받고 있습니다.

하이브리드 및 분산형 근무 방식의 확대가 입사 전날의 자동화 수요를 높이고 있습니다.

하이브리드 근무 및 원격 근무의 확산으로 인해, 프리보딩 및 온보딩 자동화 플랫폼 시장에서 입사 첫날 이전에 완료해야 할 프리보딩 업무의 내용이 변화했습니다. 신입 사원, 관리자, 확인 담당자가 같은 장소에 있지 않은 경우가 많기 때문에 서류 수집, 장비 준비, 의사소통 및 준비 업무는 비동기적으로 수행되어야 합니다. 따라서 기존의 채용 모델에 비해, 고정된 사무실에서 이루어지는 온보딩 관련 일상 업무의 효과는 크게 떨어지고 있습니다. 2026년 말까지 노동 인구의 70% 이상이 한 달에 최소 5일은 원격 근무를할 것으로 예상되며, 이에 따라 지역을 고려한 온보딩 절차에 대한 수요는 계속해서 증가하고 있습니다. 고용주가 매번 워크플로를 재구축할 필요 없이 국가, 법인, 관리자별로 업무를 조정할 수 있는 벤더는 프리보딩 및 온보딩 자동화 플랫폼 시장에서 더욱 확고한 입지를 차지하고 있습니다.

분산된 레거시 HR 시스템이 종단간 워크플로우 조정을 저해하고 있습니다.

분산된 인사 환경은 프리보딩 및 온보딩 자동화 플랫폼 시장에서 여전히 가장 뿌리 깊은 운영상의 제약 요인으로 남아 있습니다. 많은 고용주는 채용, 인사, 급여, 복리후생, 교육, ID 관리 등의 업무를, 서로 다른 시기에 도입되어 단일 아키텍처로 기능하도록 설계되지 않은 여러 시스템에 걸쳐 운영하고 있습니다. 이러한 환경에서는 주요 병목 현상이 워크플로우 설계 자체가 아니라 시스템의 연결 지점에 있는 경우가 많습니다. SAP의 ‘2026년 통합 메시지’에서는 채용 및 온보딩 업무 간에 공유 데이터 흐름이 확립되기 전까지 막대한 수작업에 의한 재입력이 필요했던 점이 지적되었으며, 연동되지 않은 시스템들이 왜 가치 실현을 계속 지연시키고 있는지가 명확히 드러났습니다. 그 결과, 프리보딩 및 온보딩 자동화 플랫폼 시장의 구매자들에게는 도입 주기의 장기화, 서비스 요구 사항 증가, 그리고 가치 실현까지의 시간 지연이 발생하고 있습니다.

부문별 분석

2025년에는 클라우드 기반 솔루션의 도입이 매출의 68.41%를 차지했으며, 프리보딩 및 온보딩 자동화 플랫폼 시장의 주요 모델로 자리매김했습니다. 구매자가 클라우드 플랫폼을 선호한 이유는 새로운 온프레미스 인프라를 구축할 필요 없이 ATS, HRIS, 급여 계산 시스템 간에 보다 원활하게 연동할 수 있기 때문입니다. 온프레미스 방식의 도입은 유연성보다는 데이터 관리나 사내 호스팅이 여전히 중시되는 보다 제한적인 규제 환경에서 여전히 중요한 위치를 차지하고 있습니다. 하이브리드형 도입은 2031년까지 연평균 성장률(CAGR) 16.47%로 확대될 것으로 예측되며, 이 프리보딩 및 온보딩 자동화 플랫폼 시장에서 가장 빠르게 성장하는 모델로 자리매김하고 있습니다.

이러한 경향은 전 세계 많은 기업들이 이미 운영 중인 인사 관리 핵심 시스템 전체를 교체하지 않고도 온보딩 워크플로우를 현대화하고자 한다는 사실을 반영하고 있습니다. 하이브리드 구성을 통해 기업은 핵심 시스템인 ‘시스템 오브 레코드’를 유지하면서, 그 위에 클라우드 기반의 사용자 경험 및 규정 준수 계층을 추가할 수 있습니다. 2026년 3월 SAP가 SmartRecruiters 및 SuccessFactors와 함께 진행한 통합 작업은 채용과 온보딩을 연계함으로써, 이 전환 모델에서 수작업으로 인한 재입력 부담을 줄일 수 있음을 입증했습니다. 프리보딩 및 온보딩 자동화 플랫폼 업계에서 안정적인 시스템 오브 레코드 운영과 유연한 워크플로우 오케스트레이션을 모두 지원하는 벤더가 가장 확고한 입지를 차지하고 있습니다.

2025년에는 대기업이 매출의 62.37%를 차지했으며, 프리보딩 및 온보딩 자동화 플랫폼 시장에서 가장 큰 구매층이 되었습니다. 그 규모, 여러 사업체에 걸친 채용 수요, 그리고 높은 규정 준수 리스크로 인해, 엔드투엔드 워크플로우 자동화 도입의 의의를 설명하기가 더 쉬워졌습니다. 포춘 500에 선정된 한 제조업체의 사례에 따르면, 각 부서에 자동화를 도입한 결과 연간 40만 달러 이상의 비용 절감과 5배 이상의 ROI를 달성한 것으로 보고되었습니다. 중소기업은 2031년까지 연평균 성장률(CAGR) 17.83%를 나타낼 것으로 예측되며, 이는 도입이 대기업 이외의 분야로도 확대되고 있음을 보여줍니다.

SMB의 성장을 뒷받침하고 있는 것은 PEPM(사용자당 월간) 가격의 서비스, 노코드 워크플로우 빌더, 그리고 진입 장벽을 낮추는 규정 준수 라이브러리의 번들 제공입니다. 한편, 이러한 구매 기업들은 전담 HR 기술 팀이 부족한 경우가 많기 때문에 여전히 보다 신속한 도입과 충실한 공급업체 지원을 원하고 있습니다. Intuit이 GoCo를 통해 연계형 HR 자동화 분야에 진출한 사실 또한, 소규모 고용주들이 개별 도구를 따로따로 사용하는 대신 급여 계산, 인사, 온보딩을 통합한 솔루션을 원하고 있다는 관점을 뒷받침하고 있습니다. 따라서 프리보딩 및 온보딩 자동화 플랫폼 업계에서는 대기업과 중소기업이 ‘도입 첫날부터 가동’에 대해 요구하는 요건의 차이가 점차 좁혀지고 있지만, 도입 과정의 용이성 측면에서는 여전히 대기업이 유리한 상황이 지속되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 39.61%를 차지했으며, 채용 예정자 관리 및 신입 사원 온보딩 자동화 플랫폼을 위한 최대 지역 시장이 되었습니다. 이 지역은 성숙한 인사 관리 소프트웨어의 도입, 원격 및 하이브리드 채용의 높은 보급률, 그리고 고용주가 감사 대응이 가능한 업무 흐름으로 전환할 수 있도록 돕는 규정 준수 환경의 혜택을 누리고 있습니다. 현재 미국에서는 2026년 3월로 예정된 I-9 양식의 실질적 위반 기준에 관한 ICE(이민세관단속국)의 개정안이 큰 영향을 미치고 있습니다. 대체 절차 체크박스를 선택하지 않았거나, 원격 서류 심사 이용 시 E-Verify 요건을 충족하지 못한 경우 등 원격 검증 과정에서 발생하는 오류는 현재 양식 1장당 최대 2,861달러의 직접적인 과태료 위험을 초래할 수 있습니다. 이러한 변화로 인해, 프리보딩 및 온보딩 자동화 플랫폼 시장에서 원격 I-9 및 E-Verify 지원 워크플로우를 표준 기능으로 갖춘 제품에 대한 수요가 증가하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)의 처리 요건과 EU AI법으로 인해 발생하는 광범위한 거버넌스상의 부담이 큰 영향을 미치고 있습니다. 독일은 여전히 규제가 가장 엄격한 환경이며, 고용 데이터에 관한 규정이나 근로자 대표 위원회와의 협의가 AI를 활용한 온보딩 시스템의 도입 방식에 영향을 미칠 가능성이 있기 때문입니다. 제26조(7)항에 규정된 근로자에 대한 통지 의무는 2026년 8월 이후에도 계속 적용되며, 이에 따라 플랫폼은 근로자를 위한 절차에서 정보 공개 절차를 지원해야 합니다. 영국은 독자적인 취업 자격 확인 절차를 채택하고 있는 반면, 남미는 여전히 초기 단계에 머물러 있어, 국내 우선 도입이라기보다는 다국적 기업에 의한 진출이 주류를 이루고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 14.71%를 나타낼 것으로 예측되며, 프리보딩 및 온보딩 자동화 플랫폼 시장에서 가장 빠르게 성장하는 지역이 될 것입니다. 이러한 성장은 인도, 호주, 한국, 싱가포르의 인사 부문 디지털화에 힘입은 것입니다. 싱가포르의 ‘고용 허가증(Employment Pass)’ 절차나 필리핀의 여러 기관에 걸친 법정 등록 요건은 현지화된 워크플로 템플릿에 대한 명확한 수요를 창출하고 있습니다. 일본과 중국은 여전히 개척되지 않은 거대한 기회를 안고 있지만, 양국 모두 언어, 데이터 관리, 의사소통 방식에 있어 더욱 강력한 현지화가 요구되고 있습니다. 중동 및 아프리카에서는 사우디아라비아, 아랍에미리트(UAE), 남아프리카공화국, 나이지리아가 주도적인 역할을 하며 수요가 집중되고 있으며, 이들 국가에서는 다국적 기업의 자회사나 지역 기술 기업들이 ‘클라우드 퍼스트’ 온보딩 시스템을 도입하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the preboarding and onboarding automation platform market size is projected to expand from USD 4.10 billion in 2025 and USD 4.81 billion in 2026 to USD 9.06 billion by 2031, registering a CAGR of 13.50% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), Functionality (Recruitment-To-Preboarding Automation, Documentation and Verification, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Preboarding And Onboarding Automation Platform Market Trends and Insights

Shift from Manual HR Workflows to Digital Employee Journeys

The move from manual coordination to structured digital workflows remains the clearest growth driver in the preboarding and onboarding automation platform market. Older onboarding routines relied on email follow-ups, disconnected checklists, and separate actions from HR, IT, legal, and facilities, which made delays hard to avoid as hiring volumes rose. Employers now want one workflow that starts as soon as the offer is accepted and continues through documentation, access setup, and first-day readiness. As these steps are brought together, buyers gain clearer visibility into completion gaps and early experience signals, making onboarding more useful for retention management, not just administration. Vendors that can tie workflow completion to faster readiness and measurable cost savings are gaining stronger buyer attention in the preboarding and onboarding automation platform market.

Hybrid and Distributed Hiring Expands Pre-Day-One Automation Needs

Hybrid and remote work changed what preboarding must complete before day one in the preboarding and onboarding automation platform market. New hires, managers, and verification contacts are often not in the same place, so document collection, equipment coordination, communication, and readiness tasks need to run asynchronously. That makes fixed office-based onboarding routines much less effective than they were in earlier hiring models. More than 70% of the workforce is expected to work remotely at least 5 days per month by the end of 2026, which keeps demand high for geography-aware onboarding flows. Vendors that let employers adapt tasks by country, legal entity, and manager without rebuilding the workflow each time are in a stronger position in the market for preboarding and onboarding automation platforms.

Fragmented Legacy HR Stacks Slow End-To-End Workflow Orchestration

Fragmented HR environments remain the most persistent operational restraint in the preboarding and onboarding automation platform market. Many employers still run recruiting, HR, payroll, benefits, learning, and identity tasks across systems acquired at different times and not built to work as a single architecture. In that setting, the main bottleneck is often the system connection point and not the workflow design itself. SAP's 2026 integration messaging highlighted the significant manual re-entry that existed before shared data flow was established across hiring and onboarding tasks, underscoring why disconnected stacks continue to delay value realization. The result is longer implementation cycles, heavier service requirements, and slower time-to-value for buyers in the preboarding and onboarding automation platform market.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Automation Demand Across Labor, Privacy, and Hiring Rules

- Platform Consolidation Across ATS, HRIS, Payroll, and Experience Layers

- Budget Scrutiny And Longer HR Tech Payback Hurdles In SMBs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment accounted for 68.41% of revenue in 2025, making it the leading model in the preboarding and onboarding automation platform market. Buyers favored cloud platforms because they can connect more easily across ATS, HRIS, and payroll without requiring new on-premises infrastructure. On-premises deployment remained relevant in a narrower set of regulated environments where data control and internal hosting still carry more weight than flexibility. Hybrid deployment is projected to expand at a 16.47% CAGR through 2031, which makes it the fastest-growing model in this preboarding and onboarding automation platform market.

This pattern reflects the fact that many global employers want to modernize onboarding workflows without replacing the full HR backbone they already run. A hybrid setup lets them keep the core system of record in place while adding cloud-based experience and compliance layers on top. SAP's March 2026 integration work with SmartRecruiters and SuccessFactors demonstrated how a connected flow between recruiting and onboarding can reduce manual re-entry during this transition model. Within the preboarding and onboarding automation platform industry, vendors that support both stable system-of-record operations and flexible workflow orchestration are in the strongest position.

Large enterprises accounted for 62.37% of revenue in 2025, making them the largest buyer group in the preboarding and onboarding automation platform market. Their scale, multi-entity hiring needs, and greater compliance exposure make end-to-end workflow automation easier to justify. A Fortune 500 manufacturing case documented annual savings of more than USD 400,000 and more than 5x ROI after automation was applied across divisions. Small and medium-sized businesses are projected to grow at a 17.83% CAGR through 2031, which shows that adoption is broadening beyond the largest employers.

SMB growth is being helped by PEPM-priced offerings, no-code workflow builders, and bundled compliance libraries that reduce the entry barrier. At the same time, these buyers still expect faster activation and greater vendor support because they often lack dedicated HR technology teams. Intuit's move into connected HR automation through GoCo also supports the view that smaller employers want unified payroll, HR, and onboarding coverage rather than a collection of separate tools. The preboarding and onboarding automation platform industry is therefore seeing the gap narrow between what large enterprises and SMBs expect from day-zero readiness, even if the buying path remains easier for larger accounts.

Geography Analysis

North America accounted for 39.61% of global revenue in 2025, making it the largest regional market for preboarding and onboarding automation platforms. The region benefits from mature HR software adoption, a high level of remote and hybrid hiring, and a compliance environment that pushes employers toward audit-ready workflows. The United States is now being shaped by the March 2026 ICE revision to the substantive violation standards for Form I-9. Remote-verification errors, including failure to mark the alternative procedure checkbox and failure to meet E-Verify requirements while using remote document examination, can now trigger direct penalty exposure of up to USD 2,861 per form. That shift is increasing demand for remote I-9 and E-Verify-enabled workflows as standard product features in the preboarding and onboarding automation platform market.

Europe is shaped by GDPR handling requirements and the wider governance burden created by the EU AI Act. Germany remains the most regulation-heavy environment because employment data rules and works council consultation can affect how AI-enabled onboarding systems are deployed. Article 26(7) worker notification obligations remain relevant from August 2026, which adds disclosure steps that platforms must support in employee-facing flows. The UK follows its own right-to-work verification path, while South America remains earlier stage and is still led mainly by multinational rollouts rather than domestic-first deployments.

Asia-Pacific is projected to expand at a 14.71% CAGR through 2031, which makes it the fastest-growing region in the preboarding and onboarding automation platform market. Growth is being supported by HR digitization in India, Australia, South Korea, and Singapore. Singapore's Employment Pass process and the Philippines' multi-agency statutory enrollment needs create clear demand for localized workflow templates. Japan and China remain large untapped opportunities, but both require stronger localization around language, data control, and communication patterns. The Middle East and Africa add concentrated demand, driven by Saudi Arabia, the UAE, South Africa, and Nigeria, where multinational subsidiaries and regional technology employers are adopting cloud-first onboarding systems.

- Phenom People, Inc.

- iCIMS, Inc.

- Greenhouse Software, Inc.

- SmartRecruiters, Inc.

- Employ, Inc.

- Lever, Inc.

- ClearCompany, LLC

- Bamboo HR LLC

- GoCo.io, Inc.

- Namely, Inc.

- Talentech Group AS

- Tribepad Ltd

- EMP Trust Solutions, LLC

- Click Boarding, LLC

- Enboard.Me Pty Ltd.

- WorkBright

- NEO Global Pty Ltd.

- Affirm Software Group Pty Ltd.

- HROnboard Pty Ltd.

- Onboarded Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift From Manual HR Workflows to Digital Employee Journeys

- 4.2.2 Hybrid and Distributed Hiring Expands Pre-Day-One Automation Needs

- 4.2.3 Compliance Automation Demand Across Labor, Privacy, and Hiring Rules

- 4.2.4 Platform Consolidation Across ATS, HRIS, Payroll, and Experience Layers

- 4.2.5 HR-To-IT Identity Provisioning Becomes a Day-Zero Readiness Priority

- 4.2.6 Cross-Border Hiring Raises Need for Localized Preboarding and Right-To-Work Flows

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy HR Stacks Slow End-To-End Workflow Orchestration

- 4.3.2 Budget Scrutiny and Longer HR Tech Payback Hurdles in SMBs

- 4.3.3 EU AI Act and Worker-Notice Duties Raise Governance Burden for AI-Enabled Flows

- 4.3.4 Remote I-9 and Identity Verification Liability Keeps Regulated Employers Cautious

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-Sized Businesses

- 5.3 By End User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Information Technology and Telecom

- 5.3.4 Retail and E-commerce

- 5.3.5 Industrial Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-user Industries

- 5.4 By Functionality

- 5.4.1 Recruitment-to-Preboarding Automation

- 5.4.2 Documentation and Verification

- 5.4.3 Compliance and Identity Governance

- 5.4.4 IT Provisioning and Workspace Enablement

- 5.4.5 Learning and Productivity Enablement

- 5.4.6 Employee Experience and Journey Management

- 5.4.7 Workforce Analytics and Intelligence

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Netherlands

- 5.5.2.8 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Phenom People, Inc.

- 6.4.2 iCIMS, Inc.

- 6.4.3 Greenhouse Software, Inc.

- 6.4.4 SmartRecruiters, Inc.

- 6.4.5 Employ, Inc.

- 6.4.6 Lever, Inc.

- 6.4.7 ClearCompany, LLC

- 6.4.8 Bamboo HR LLC

- 6.4.9 GoCo.io, Inc.

- 6.4.10 Namely, Inc.

- 6.4.11 Talentech Group AS

- 6.4.12 Tribepad Ltd

- 6.4.13 EMP Trust Solutions, LLC

- 6.4.14 Click Boarding, LLC

- 6.4.15 Enboard.Me Pty Ltd.

- 6.4.16 WorkBright

- 6.4.17 NEO Global Pty Ltd.

- 6.4.18 Affirm Software Group Pty Ltd.

- 6.4.19 HROnboard Pty Ltd.

- 6.4.20 Onboarded Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment