|

시장보고서

상품코드

2063965

핵심 HR 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Core HR Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

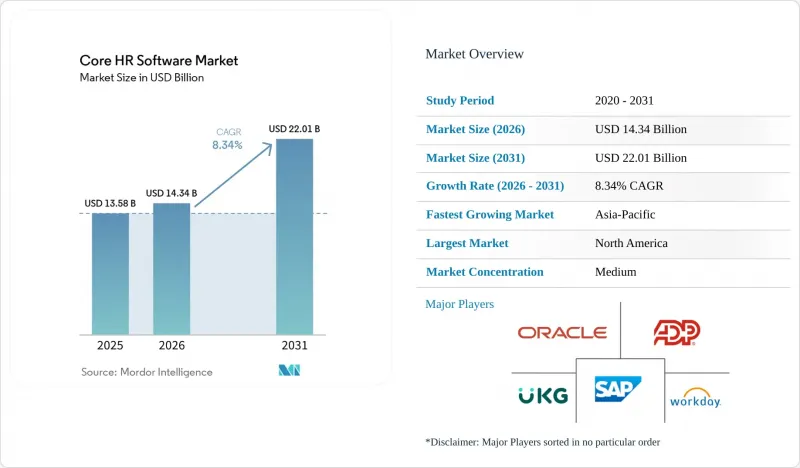

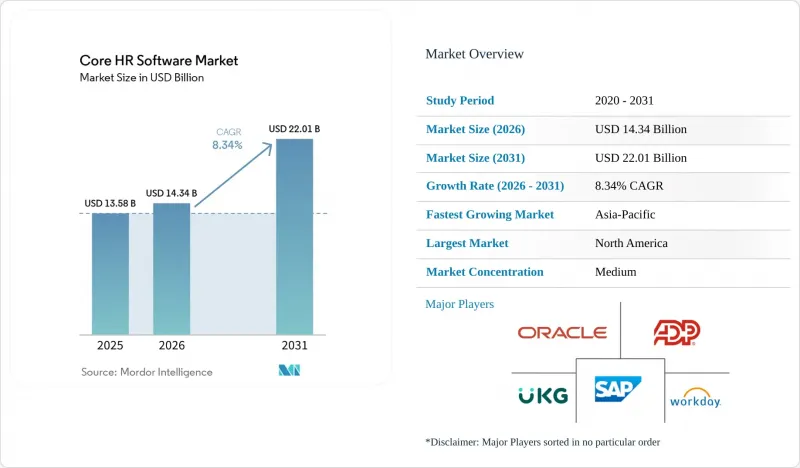

Mordor Intelligence에 의하면, 핵심 HR 소프트웨어 시장 규모는 2025년에 135억 8,000만 달러로 평가되었고, 2026년에는 147억 4,000만 달러에 이를 것으로 예상되고 있습니다.

또한, 2026-2031년 연평균 성장률(CAGR) 8.34%를 기록하며 성장할 것으로 예상되며, 2031년에는 220억 1,000만 달러에 달할 것으로 전망됩니다.

본 보고서는 컴포넌트별(소프트웨어 및 서비스), 전개 방식별(클라우드, 온프레미스, 하이브리드), 조직 규모별(중소기업 및 대기업), 업종별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 소매 및 전자상거래, 제조, 정부 및 공공 부문 등) 및 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 핵심 HR 소프트웨어 시장 동향 및 인사이트

HR 제품군의 클라우드 우선 도입

분기별 SaaS 릴리스를 통해 방화벽 내부에서는 재현할 수 없는 혁신이 제공됨에 따라, 기업들은 온프레미스 시스템의 폐지를 추진하고 있습니다. 벤더의 로드맵에 따르면, 클라우드 서비스 제공과 에이전트형 AI 간의 연동이 점점 더 확대됨에 따라, 고객은 최소한의 추가 비용으로 이직 예측 분석, 자동화된 규정 준수 점검, 대화형 셀프 서비스를 체험할 수 있게 되었습니다. 다국적 기업들은 또한 수십 개의 관할 구역에 걸쳐 있는 복잡한 세무 시스템을 처리하기 위해 하이퍼스케일러의 데이터센터에 의존하고 있습니다. 그러나 전환 전에 수십 년에 걸친 급여 내역을 추출하고 정리하는 작업은 여전히 많은 노력이 필요하기 때문에 관련 서비스에 대한 수요가 증가하고 있습니다.

AI를 활용한 인재 분석의 통합

대기업들은 2025년에 AI를 접목한 인재 관리 도구를 대규모로 시범 도입했으며, 인사 관리용 AI에 대한 기업 예산은 2026년에 중앙값 기준 160만 달러에 달했습니다. Workday의 ‘Talent Optimization’이나 SAP의 ‘SuccessFactors’에 포함된 에이전틱 워크플로우와 같은 최근 출시된 기능들은 단순한 설명형 대시보드의 범위를 넘어, 승진 추천, 후계자 리스크의 가시화, 성과 평가 문서 자동 생성을 실현하고 있습니다. 감사 추적을 요구하는 규제가 엄격한 업계에서는 도입이 빠르게 진행되고 있지만, 많은 중견 기업에서는 여전히 공식적인 거버넌스 방침이 마련되어 있지 않아 전면적인 도입에 걸림돌이 되고 있습니다.

데이터의 소재지와 주권에 관한 우려

유럽연합(EU)의 GDPR(EU 개인정보보호규정), 중국의 개인정보보호법, 인도의 디지털 개인데이터 보호법 등의 규정에 따라 특정 직원 정보는 국내에 보관해야 합니다. 그 때문에 벤더는 지역별 인스턴스를 유지할 수밖에 없으며, 그 결과 미국 이외 지역에서의 기능 표준화가 지연되고 인프라 비용이 증가하고 있습니다. 방위, 은행, 의료 분야의 구매자들은 현지 호스팅 증명을 요구하고 있으며, 데이터 소재지는 주요 평가 기준이 되고 있습니다.

부문별 분석

2025년, 소프트웨어 부문이 핵심 HR 소프트웨어 시장 점유율의 79.18%를 차지했습니다. 이는 급여 계산, 복리후생, 인력 분석 모듈에 대한 대규모 정기 구독 계약에 따른 것입니다. 현재, 성장의 기세는 서비스 분야로 옮겨가고 있습니다. 데이터 이전, 다국간 세무 설정, AI 거버넌스에는 전문적인 지식이 필요하기 때문입니다. 따라서 급여 계산 관리형 아웃소싱, Tier 1 헬프데스크 지원, 지속적인 최적화 계약을 통해 시스템 통합사업자 및 벤더의 전문 서비스 팀의 수익 기반이 확대되고 있습니다.

AI 에이전트가 저부가가치 업무를 자동화함으로써 컨설턴트는 기술 프레임워크 및 변화 관리에 관한 자문에 집중할 수 있게 되며, 이에 따른 핵심 HR 소프트웨어 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 8.87%로 확대될 것으로 전망됩니다. SAP의 SmartRecruiters 통합 기능은 기존의 채용 워크플로를 SuccessFactors에 자동으로 매핑하는 것으로, 이미 프로페셔널 서비스의 작업량을 약 30% 절감했으며, 자동화를 통해 청구 가능한 업무가 설정 단계에서 전략 수립 단계로 전환될 수 있음을 보여주고 있습니다.

2025년 지출 중 클라우드 도입이 72.46%를 차지했습니다. 이는 벤더 관리를 통한 보안, 신속한 기능 제공, 그리고 기존의 온프레미스 도입에 비해 낮은 초기 투자 비용에 대한 구매자의 강한 신뢰를 반영하고 있습니다. 조직들은 확장성, 자동 업데이트, 분산형 인력 지원 능력은 물론, 인프라 유지보수 및 시스템 업그레이드에 따른 사내 IT 팀의 부담을 줄일 수 있다는 점에서 클라우드 기반 핵심 HR 시스템을 점점 더 선호하고 있습니다. 그러나 하이브리드 모델은 기밀성이 높은 급여 데이터를 온프레미스에 보관하면서 새로운 인사 관리 모듈을 SaaS로 실행할 수 있기 때문에 2031년까지 연평균 성장률(CAGR)이 9.28%를 나타낼 것으로 예측되며, 도입 유형 중 가장 높은 성장률을 보이고 있습니다.

두 환경 간에 실시간 데이터 동기화를 유지하는 것은 기술적으로 어렵기 때문에 대부분의 경우 미들웨어를 통한 오케스트레이션이 필요합니다. UKG가 2026년 초에 Inova Payroll을 인수함에 따라, 에어갭 네트워크 내에서 작동 가능한 하이브리드 지원 엔진이 제공되게 되었으며, 이는 주권과 현대화 사이의 균형을 맞추어야 하는 규제 대상 기관을 위한 조치입니다. 성공의 핵심은 견고한 API 거버넌스, 지연 시간 관리, 그리고 공급업체와 고객 간의 보안 책임에 대한 명확한 분담입니다.

지역별 분석

북미는 2025년, 확립된 컨설팅 생태계, 대기업 구매자의 집중, 그리고 비교적 관대한 데이터 전송 규정의 혜택을 받아 전 세계 매출의 38.96%를 차지했습니다. 연방 정부의 HR 2.0 이니셔티브에 따라 2026 회계연도부터 농무부 등 기관에 하이브리드형 핵심 HCM이 도입될 예정(OPM.GOV)인 만큼, 공공 부문의 현대화는 여전히 주목할 만한 기회로 남아 있습니다. 그러나 포춘 1000대 기업의 대부분이 이미 클라우드 또는 하이브리드형 제품군을 운영하고 있으며, 예산을 스킬 마켓플레이스, 직원 경험 레이어, 분석 애드온으로 전환하고 있기 때문에 성장세가 둔화되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 10.11%를 나타낼 것으로 예측되며, 다른 어떤 지역보다 높은 성장률을 보일 것으로 전망됩니다. 인도, 중국, 동남아시아의 중견 기업들에서는 고용 계약의 정식화와 세무 규정 준수 강화를 위한 정부의 이니셔티브에 힘입어, 처음으로 급여 계산의 디지털화를 추진하는 움직임이 가장 활발합니다. Darwinbox는 2025년 3월, 인도 외 지역으로의 사업 확장을 위한 자금으로 1억 4,000만 달러를 조달했으며, 이는 투자자들이 해당 지역의 지속적인 성장 잠재력을 확신하고 있음을 시사합니다. 중국과 인도의 현지 데이터 보호법은 국내 또는 지역 내에서 호스팅되는 플랫폼을 우선시하고 있으며, 현지화된 인프라를 유지하는 공급업체에 경쟁 우위를 제공합니다.

유럽, 남미, 중동 및 아프리카에서는 전반적으로 안정적인 수요가 나타나고 있지만, 그 양상은 제각각입니다. GDPR(EU 개인정보보호규정)에 따른 데이터 보관 장소 요건으로 인해, 다국적 기업의 구매자들은 하이브리드형 또는 EU 전용 클라우드 인스턴스를 선택하도록 권장받고 있습니다. 브라질은 복잡한 전자 사회 노동 보고 제도 덕분에 남미 지역에서 이 제도의 도입을 주도하고 있습니다. 한편, 걸프협력회의(GCC) 회원국에서는 임금 보호 시스템(Wage Protection System)에 따라 급여 파일 제출이 의무화되어 있어, 해당 지역에 특화된 벤더의 부상을 뒷받침하고 있습니다. 아프리카 시장은 아직 발전 단계에 있지만, 모바일 이용률이 높아 온프레미스 방식의 도입 단계를 건너뛰고 클라우드 급여 계산에 대한 관심이 높아지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the core HR software market size reached USD 13.58 billion in 2025 and is expected to reach USD 14.74 billion in 2026, growing to USD 22.01 billion by 2031, at a CAGR of 8.34% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), Organization Size (SMEs, and Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Lifesciences, Retail and E-Commerce, Manufacturing, Government and Public Sector, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Core HR Software Market Trends and Insights

Cloud-First Adoption of HR Suites

Organizations continue to retire on-premises systems as quarterly SaaS releases deliver innovations that cannot be replicated behind the firewall. Vendor roadmaps increasingly couple cloud delivery with agentic AI, letting customers experiment with predictive attrition, automated compliance checks, and conversational self-service at minimal incremental cost. Multinational firms also lean on hyperscaler data centers to handle complex tax engines across dozens of jurisdictions. However, extracting and cleansing decades of payroll history before migration remains labor-intensive, reinforcing demand for implementation services.

AI-Driven Talent Analytics Integration

Large enterprises piloted AI-infused talent tools at scale in 2025, and corporate budgets for HR-focused AI climbed to a median of USD 1.6 million in 2026. Recent releases such as Workday's Talent Optimization and SAP's SuccessFactors agentic workflows move beyond descriptive dashboards, recommending promotions, surfacing succession risks, and drafting performance narratives automatically. Adoption is rapid in highly regulated sectors looking for audit trails, yet many mid-market firms still lack formal governance policies, slowing full deployment.

Data Residency and Sovereignty Concerns

Rules such as the GDPR in the European Union, the Personal Information Protection Law in China, and India's Digital Personal Data Protection Act mandate that certain employee attributes remain inside national borders. Vendors are therefore forced to maintain region-specific instances, which delays feature parity outside the United States and raises infrastructure costs. Buyers in defense, banking, and healthcare demand proof of local hosting, turning data residency into a primary evaluation criterion.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Remote and Hybrid Work Models

- Shift to Skills-Based Workforce Planning

- High Switching Costs From Legacy Suites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The software segment captured 79.18% of the core HR software market share in 2025, thanks to large recurring subscriptions for payroll, benefits, and workforce analytics modules. Growth momentum is now tilting toward services because data migration, multi-country tax configuration, and AI governance demand specialized expertise. Managed payroll outsourcing, tier-1 help-desk support, and continuous optimization contracts are therefore widening the revenue base for systems integrators and vendor professional services teams.

The core HR software market size attributed to services is forecast to climb at an 8.87% CAGR between 2026 and 2031 as AI agents automate low-value tasks, freeing consultants to advise on skills frameworks and change management. SAP's SmartRecruiters integration, which auto-maps legacy recruiting workflows into SuccessFactors, already trims professional services hours by about 30%, demonstrating how automation can shift billable effort from configuration to strategy.

Cloud installations represented 72.46% of spending in 2025, reflecting strong buyer confidence in vendor-managed security, rapid feature delivery, and lower upfront capital expenditure compared to traditional on-premises deployments. Organizations are increasingly favoring cloud-based core HR systems due to their scalability, automatic updates, and ability to support distributed workforces, while also reducing the burden on internal IT teams for infrastructure maintenance and system upgrades. Yet the hybrid model is on track for a 9.28% CAGR through 2031, the fastest within deployment types, because it allows sensitive payroll data to stay on-premises while newer talent modules run in SaaS.

Maintaining real-time data synchronization across two environments is technically demanding and often requires middleware orchestration. UKG's early-2026 acquisition of Inova Payroll provides a hybrid-ready engine capable of operating inside air-gapped networks, a move aimed at regulated agencies that must balance sovereignty with modernization. Success will hinge on robust API governance, latency management, and clear division of security responsibilities between vendor and customer.

Geography Analysis

North America retained 38.96% of global revenue in 2025, benefiting from established consulting ecosystems, a concentration of large enterprise buyers, and relatively permissive data-transfer rules. Public-sector modernization remains a notable opportunity as the federal HR 2.0 initiative rolls out a hybrid core HCM to agencies such as the Department of Agriculture beginning in fiscal 2026, OPM.GOV. Growth is easing, however, because most Fortune 1000 organizations already run cloud or hybrid suites and are redirecting budgets toward skills marketplaces, employee experience layers, and analytics add-ons.

Asia-Pacific is forecast to register a 10.11% CAGR through 2031, outstripping every other region. Demand is strongest among mid-market firms in India, China, and Southeast Asia that are digitizing payroll for the first time, encouraged by government efforts to formalize employment contracts and improve tax compliance. Darwinbox raised USD 140 million in March 2025 to fund expansion beyond India, signaling investor belief in a sustained regional growth runway. Local data-protection laws in China and India favor domestic or regionally hosted platforms, giving vendors that maintain localized infrastructure a competitive edge.

Europe, South America, the Middle East and Africa collectively offer steady but fragmented demand patterns. GDPR-driven residency rules nudge multinational buyers toward hybrid or EU-specific cloud instances. Brazil leads South America on adoption because of its intricate e-social labor reporting, while Gulf Cooperation Council states mandate Wage Protection System payroll files, spurring specialized regional vendors. African markets are still nascent but exhibit high mobile use and interest in cloud payroll that leapfrogs on-premises deployments.

- Workday Inc.

- Oracle Corporation

- SAP SE

- Automatic Data Processing Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paycom Software Inc.

- Cornerstone OnDemand Inc.

- BambooHR LLC

- Paylocity Holding Corporation

- Gusto Inc.

- Sage Group plc

- Rippling Inc.

- Zoho Corporation Pvt. Ltd.

- OrangeHRM Inc.

- SumTotal Systems LLC

- ClearCompany Inc.

- Ceipal Corp.

- Freshworks Inc.

- Darwinbox Digital Solutions Pvt. Ltd.

- Infor Inc.

- Paycor HCM Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first Adoption of HR Suites

- 4.2.2 Expansion of Remote and Hybrid Work Models

- 4.2.3 Increasing Regulatory Reporting Complexity

- 4.2.4 AI-Driven Talent Analytics Integration

- 4.2.5 Shift to Skills-Based Workforce Planning

- 4.2.6 Rising Mid-Market Demand in Emerging Economies

- 4.3 Market Restraints

- 4.3.1 Data Residency and Sovereignty Concerns

- 4.3.2 High Switching Costs From Legacy Suites

- 4.3.3 Shortage of HR Tech Implementation Talent

- 4.3.4 Persistent Cyber-security and Privacy Breaches

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Lifesciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 SAP SE

- 6.4.4 Automatic Data Processing Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 Paycom Software Inc.

- 6.4.8 Cornerstone OnDemand Inc.

- 6.4.9 BambooHR LLC

- 6.4.10 Paylocity Holding Corporation

- 6.4.11 Gusto Inc.

- 6.4.12 Sage Group plc

- 6.4.13 Rippling Inc.

- 6.4.14 Zoho Corporation Pvt. Ltd.

- 6.4.15 OrangeHRM Inc.

- 6.4.16 SumTotal Systems LLC

- 6.4.17 ClearCompany Inc.

- 6.4.18 Ceipal Corp.

- 6.4.19 Freshworks Inc.

- 6.4.20 Darwinbox Digital Solutions Pvt. Ltd.

- 6.4.21 Infor Inc.

- 6.4.22 Paycor HCM Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment