|

시장보고서

상품코드

2065449

중국의 해상 화물 운송 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Sea Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

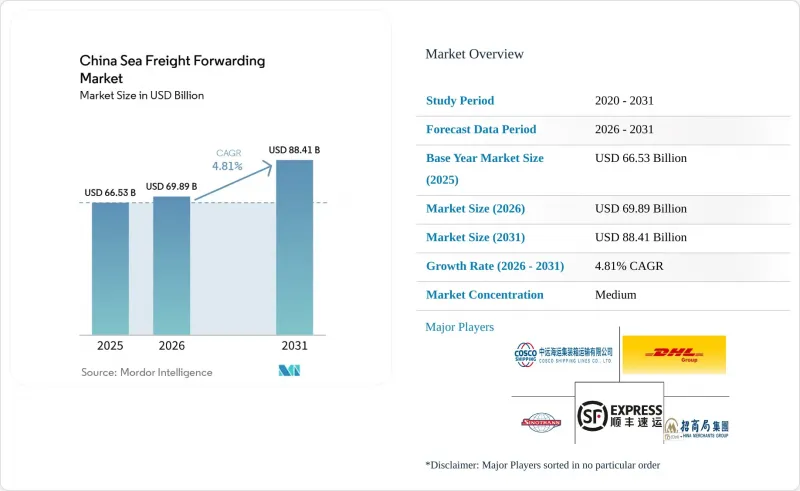

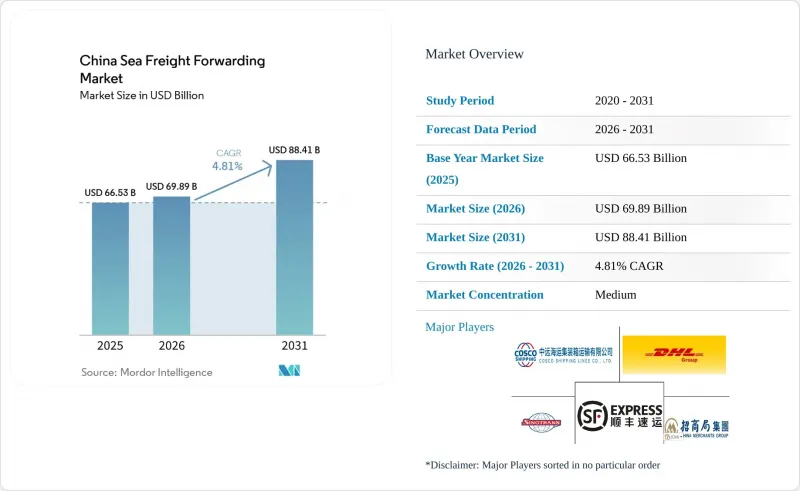

중국의 해상 화물 운송 시장 규모는 2025년 665억 3,000만 달러로 평가되었고, 2026년에는 698억 9,000만 달러로 추정되고, 2031년까지 884억 1,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 4.81%로 성장할 전망입니다.

이러한 확대 추세는 연안 지역을 중심으로 한 집하 체계에서 ‘신국제 육해 무역 회랑’을 통해 서부 각 성의 공장과 항구를 연결하는 내륙 복합 운송 노선으로의 전환을 반영하고 있습니다. 본 보고서는 서비스별(전체 컨테이너 적재(FCL), 소량 혼적(LCL)), 화물 유형별(건화물/일반 화물, 냉장 화물), 최종 사용자 산업별(일렉트로믹스 및 반도체, 제조·산업, 소매 및 전자상거래, 기타), 지역별(북부, 북동부, 동부, 중부, 남부, 남서부, 북서부)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 해상 화물 운송 시장 동향 및 인사이트

증가하는 크로스보더 전자상거래 수출량

2025년, 중국 세관 보고서에 따르면, 크로스보더 전자상거래 수출액은 2조 7,500억 위안(3,860억 달러)에 달했으며, 이는 2020년 대비 69.7% 증가한 수치입니다. 이러한 급증으로 인해 주문 규모가 축소됨에 따라, 각 포워더 업체들은 풀컨테이너 운송(FCL) 방식에서 TEU당 이익률이 높은 LCL 운송을 더 빈번하게 수행하는 방식으로 전환하고 있습니다. 이러한 물류 전략의 전환은 보다 신속하고 유연한 배송 옵션을 원하는 소비자 수요에 힘입어, 전자상거래 공급망이 점점 더 복잡해지고 있음을 반영하고 있습니다. 또한, LCL 운송 증가에 따라 각 운송 업체들은 컨테이너 이용률을 최적화하고 업무상의 비효율성을 줄이기 위한 혁신적인 솔루션 도입을 촉진하고 있습니다. 이러한 변화는 물류 업계의 양상을 완전히 바꾸어 놓고 있으며, 이해관계자들은 진화하는 시장 역학과 소비자의 기대에 적응해야 합니다.

지속가능성 추진의 일환으로, 알리바바 산하의 카이니아오(Cainiao)는 16만 9,000톤의 포장재를 줄였을 뿐만 아니라, 2025년 배송에서 신에너지 차량의 비중을 99%까지 끌어올렸습니다. 이러한 움직임은 라스트 마일의 지속가능성 목표가 업스트림 단계의 컨테이너 운영에도 영향을 미치고 있다는 보다 광범위한 추세를 여실히 보여주고 있습니다. 항저우와 선전에서는 보세창고가 사전 통관 서비스를 활용하여 업무 효율화를 도모하고 있습니다. 이러한 혁신을 통해 판매업체는 온라인 주문을 받은 당일에 컨테이너에 화물을 적재할 수 있게 되어, 리드타임을 2-3일 단축할 수 있습니다. 또한, API 연동을 통한 통관 신고를 활용하는 포워더는 소포 데이터를 실시간으로 확보할 수 있으므로, 체류 시간을 단축하고 컨테이너 전체 이용률을 높이는 데 기여합니다. 이러한 발전은 기술 통합, 업무 효율화, 그리고 지속가능성을 위한 노력을 통해 추진되는 크로스보더 전자상거래 물류의 지속적인 변화를 여실히 보여주고 있습니다.

동부·남부 허브의 항만 자동화 및 처리 능력 확대

2026년에는 상하이의 샤오양산 자동 터미널이 처리 능력을 1,160만 TEU 확대할 예정입니다. 한편, 2026년 2월에 가동을 시작한 광저우 난샤 4단계 단지는 24시간 이내에 45,200TEU라는 최대 처리량을 달성했습니다. 이러한 발전은 증가하는 무역량을 감당하고 업무 효율을 높이기 위해 중국이 항만 인프라 강화에 주력하고 있음을 보여줍니다. 이러한 터미널의 확장은 중국의 물류 네트워크를 강화하고, 세계 무역에서 경쟁력을 유지하는 데 있어 매우 중요한 역할을 할 것으로 기대됩니다. 또한, 이러한 발전은 업무 효율화와 비용 절감을 위해 도입이 확대되고 있는 항만 부문의 자동화라는 광범위한 추세와도 부합합니다.

같은 기간 동안 닝보·저우산항은 전년 동기 대비 19.8% 증가하여, 2026년 1월과 2월 두 달 동안 798만 7,000TEU를 처리했습니다. 이러한 성장은 조주문 수로의 준설 공사가 진행되어 조위와 관계없이 20만 톤급 선박이 항해할 수 있게 된 데 기인합니다. 자동화를 통해 1회 하역당 노동력을 최대 40%까지 줄일 수 있음이 입증되었으나, 막대한 설비 투자가 필요하기 때문에 부두 이용 할당량이 보장된 국유 항만이나 대형 포워더에게 유리하게 작용하고 있습니다. 반면, 비자동화 터미널에 의존하는 중소규모 포워더들은 트럭 대기 행렬이 길어지거나 드레이지 비용이 높아지는 등 운영상의 문제에 직면해 있습니다. 이러한 격차는 자동화 터미널과 비자동화 터미널 간의 효율성과 비용 대비 효과 측면에서 격차가 확대되고 있음을 여실히 보여주고 있으며, 끊임없이 변화하는 항만 업계에서 자동화의 전략적 중요성을 한층 더 부각시키고 있습니다.

운임 변동과 선박 공급 과잉

2026년 4월, 상하이 컨테이너 운임 지수(SCFI)는 1,875.26까지 하락했습니다. 이는 신조 선박의 취항으로 약 240만 TEU가 추가되었고, 이것이 전 세계 운송 능력의 8-10%를 차지했기 때문입니다. 이러한 운송 능력 증가는 상하이-로스앤젤레스 구간의 현물 운임에 하락 압력을 가해, 해당 운임은 1TEU당 2,239달러까지 떨어졌습니다. 시장공급 과잉은 업계 이해관계자들에게, 특히 운임 하락 속에서 수익성을 유지해야 한다는 점에서 큰 과제가 되고 있습니다. 또한, 해운사들이 과잉 운송 능력을 효과적으로 관리하는 데 어려움을 겪고 있어, 운임의 장기적인 지속가능성에 대한 우려도 커지고 있습니다.

2024년 계약에 묶여 있는 각 운송 업체들은 변화하는 시장 역학에 적응하기 위해 현재 압박 속에서 재협상을 진행하고 있습니다. 한편, 현물 운임에 의존하고 있는 운송 업체들은 운임의 변동성으로 인해 이익률을 정확하게 예측하기 어려워지고 있습니다. 게다가, 얼라이언스 주도로 인한 결항으로 화물이 정체되어, 재예약 및 보관료로 인한 비용 증가로 이어지고 있습니다. 이러한 혼란은 해운 업계가 수급 균형을 효과적으로 맞추기 위해 현재도 고군분투하고 있음을 여실히 보여주고 있습니다. 시장의 불확실성은 해운사와 운송업체 양측의 업무 계획을 더욱 복잡하게 만들고, 업계의 재정적 부담을 가중시키고 있습니다.

부문별 분석

2025년, 중국 해상 화물 운송 시장 규모의 67.33%를 FCL(전체 컨테이너 적재) 서비스가 차지했으나, LCL(혼재) 부문의 중국 해상 화물 운송 시장은 2031년까지 연평균 7.53%의 성장률을 보일 것으로 전망됩니다. 선전, 상하이, 닝보에서 보세 창고를 운영하는 LCL 통합 운송업체는 85-90%의 가동률을 달성하며, FCL 운임보다 15-20% 높은 이익률을 확보하고 있습니다. 디지털 플랫폼을 통해 화물 매칭이 자동화됨에 따라, 자체 혼적 시설을 갖추지 않은 포워더들은 소프트웨어 중개업체에 수익을 빼앗기고 있습니다. FCL은 전자기기 및 기계 운송에 있어 여전히 필수적이지만, 선박 공급 과잉으로 인한 운임 압박에 직면해 있습니다. 상하이-오사카 노선에서 일본통운 브랜드의 컨테이너는 FCL 사업자가 컨테이너 확보와 통합 통관 대행 서비스를 통해 부가가치를 제공하고 있음을 보여줍니다.

LCL 시장 점유율의 확대는 중국의 해상 포워딩 시장이 소량 수출에 어떻게 적응하고 있는지를 보여줍니다. Cainiao와 SF는 국내 특송과 해상 LCL을 통합하여, 주문부터 항구까지 소요되는 시간을 2-3일 단축하고 있습니다. API를 활용한 통관 절차를 이용하는 포워더는 혼합 화물의 통관을 보다 신속하게 처리할 수 있으며, 이러한 기능은 컨테이너를 가득 채우지 못하는 중소규모 판매업체와의 유대 관계를 강화하고 있습니다. FCL 사업자들은 상품화된 정기선 운임에 대응하기 위해 부가가치가 높은 창고 업무나 복합 운송 패키지로 사업을 전환하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the china sea freight forwarding market size is expected to increase from USD 66.53 billion in 2025 to USD 69.89 billion in 2026 and reach USD 88.41 billion by 2031, growing at a CAGR of 4.81% over 2026-2031.

The measured expansion reflects a shift from coast-centric consolidation to inland multimodal routing that links factories in western provinces to seaports through the New International Land-Sea Trade Corridor. This report is Segmented by Service (Full-Container-Load (FCL), Less-Than-Container-Load (LCL)), by Cargo Type (Dry/General, Reefer), by End User Industry (Electronics and Semiconductors, Manufacturing and Industrial, Retail and E-Commerce, and Others), and by Region (North, Northeast, East, Central, South, Southwest, Northwest). The Market Forecasts are Provided in Terms of Value (USD).

China Sea Freight Forwarding Market Trends and Insights

Rising Cross-Border E-Commerce Export Volumes

In 2025, China Customs reported cross-border e-commerce exports of RMB 2.75 trillion (USD 386 billion), a 69.7% increase from 2020. This surge has led to smaller order sizes, prompting forwarders to transition from full-container load workflows to more frequent LCL shipments, capitalizing on higher margins per TEU. The shift in logistics strategies reflects the growing complexity of e-commerce supply chains, driven by consumer demand for faster, more flexible delivery options. Additionally, the rise in LCL shipments has encouraged forwarders to adopt innovative solutions to optimize container utilization and reduce operational inefficiencies. These changes are reshaping the logistics landscape, requiring stakeholders to adapt to evolving market dynamics and consumer expectations.

In a nod to sustainability, Alibaba's Cainiao not only eliminated 169,000 tons of packaging but also achieved 99% coverage with new-energy vehicles for 2025 distributions. This move underscores a broader trend: last-mile sustainability goals are now influencing upstream container operations. In Hangzhou and Shenzhen, bonded warehouses are streamlining operations with pre-clearance services. This innovation enables sellers to load containers on the same day an online order is made, trimming lead times by 2-3 days. Furthermore, forwarders utilizing API-linked customs filing can capture parcel data in real-time, leading to reduced dwell times and enhanced overall container utilization. These advancements highlight the ongoing transformation of the cross-border e-commerce logistics landscape, driven by technological integration, operational efficiency, and sustainability initiatives.

Regional Port Automation and Capacity Expansion in East/South Hubs

In 2026, Shanghai's Xiaoyangshan automated terminal is set to boost its capacity by 11.6 million TEUs. Meanwhile, Guangzhou Nansha Phase IV, which commenced operations in February 2026, achieved a peak handling of 45,200 TEUs within a 24-hour span. These developments underscore China's commitment to enhancing its port infrastructure to accommodate growing trade volumes and improve operational efficiency. The expansion of these terminals is expected to play a pivotal role in strengthening China's logistics network and maintaining its competitive edge in global trade. Additionally, these advancements align with the broader trend of automation in the port sector, which is increasingly being adopted to streamline operations and reduce costs.

Over the same period, Ningbo-Zhoushan saw a 19.8% year-on-year increase, processing 7.987 million TEUs in January and February 2026. This growth followed the deepening of the Tiaozhoumen Channel, enabling 200,000-ton ships to transit at any tide, as highlighted by. Automation has proven to reduce labor per lift by up to 40%, but the high capital investment required favors state-owned ports and large forwarders with guaranteed berth windows. In contrast, smaller forwarders relying on non-automated terminals face operational challenges, including longer truck queues and higher drayage costs. These disparities highlight the growing divide in efficiency and cost-effectiveness between automated and non-automated terminals, further emphasizing the strategic importance of automation in the evolving port industry.

Freight-Rate Volatility and Vessel Overcapacity

The Shanghai Containerized Freight Index declined to 1,875.26 in April 2026, as the addition of newbuilds contributed approximately 2.4 million TEU, representing 8-10% of global capacity. This increase in capacity exerted downward pressure on Shanghai-Los Angeles spot rates, which fell to USD 2,239 per TEU. The oversupply in the market has created significant challenges for industry stakeholders, particularly in maintaining profitability amidst falling rates. The situation has also raised concerns about the long-term sustainability of freight rates, as carriers struggle to manage excess capacity effectively.

Forwarders bound by 2024 contracts are now renegotiating under pressure, seeking to adapt to the changing market dynamics. Meanwhile, those relying on spot rates face difficulties in accurately predicting margins due to the volatility. Additionally, alliance-driven blank sailings have left cargo stranded, leading to increased costs from rebooking and storage fees. These disruptions highlight the ongoing struggles within the shipping industry to balance supply and demand effectively. The market uncertainty has further complicated operational planning for both carriers and forwarders, adding to the industry's financial strain.

Other drivers and restraints analyzed in the detailed report include:

- Belt and Road Initiative Opening New Maritime Corridors

- Digital Freight Platforms and E-Documentation Adoption

- Geopolitical Trade Restrictions and Tariff Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-container-load services accounted for 67.33% of the China sea freight forwarding market size in 2025, yet the China sea freight forwarding market for LCL is projected to grow 7.53% annually to 2031. LCL consolidators operating bonded warehouses in Shenzhen, Shanghai, and Ningbo achieved 85-90% utilization, earning margins 15-20% above FCL rates. Digital platforms automate cargo matching, so forwarders without proprietary consolidation facilities cede revenue to software intermediaries. FCL remains essential for electronics and machinery but faces rate pressure from vessel overcapacity. Nippon Express-branded containers on the Shanghai-Osaka run show FCL players adding value with guaranteed equipment and integrated customs brokerage.

The LCL share rise indicates how the China sea freight forwarding market adapts to parcel-level exports. Cainiao and SF integrate domestic express with seaborne LCL, shrinking order-to-port times by 2-3 days. Forwarders leveraging API customs filing can clear mixed consignments faster, a feature that strengthens stickiness with small and midsize sellers that cannot fill a full box. FCL players pivot to value-added warehousing and multimodal bundles to counter commoditized liner rates.

List of Companies Covered in this Report:

- SINOTRANS Limited

- COSCO Shipping Logistics Co., Ltd.

- China Merchants Logistics Group Co., Ltd.

- DHL Group

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- CMA CGM Group (Including CEVA Logistics)

- Nippon Express Holdings

- NYK Line (Including Yusen Logistics Global Management Co., Ltd)

- A.P. Moller-Maersk

- SF Holdings (KEX-SF)

- SITC International Holdings Co., Ltd.

- Toll Group

- Rhenus Logistics

- AIT Worldwide Logistics, Inc.

- SEKO Logistics

- CIMC Logistics (CIMC Shilianda)

- Huamao International Freight Forwarding Co., Ltd.

- CTS International Logistics Corporation

- Basenton Logistics Co., Ltd.

- Shenzhen King-Hor Supply Chain Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cross-Border E-Commerce Export Volumes

- 4.2.2 Regional Port Automation and Capacity Expansion in East/South Hubs

- 4.2.3 Belt and Road Initiative Opening New Maritime Corridors

- 4.2.4 Digital Freight Platforms and E-Documentation Adoption

- 4.2.5 Carbon-Neutral Procurement Mandates from Chinese Tech Giants

- 4.2.6 Pinglu Canal Unlocking Sea Access for Inland Guangxi Industries

- 4.3 Market Restraints

- 4.3.1 Freight-Rate Volatility and Vessel Overcapacity

- 4.3.2 Geopolitical Trade Restrictions and Tariff Uncertainty

- 4.3.3 Reefer-Equipment Repositioning Imbalances During Harvest Peaks

- 4.3.4 Inland Depot Labor Shortages Causing Drayage Bottlenecks

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Freight-Rate and Surcharges Trend Analysis

- 4.9 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Service

- 5.1.1 Full-Container-Load (FCL)

- 5.1.2 Less-than-Container-Load (LCL)

- 5.2 By Cargo Type

- 5.2.1 Dry/General

- 5.2.2 Reefer

- 5.3 By End User Industry

- 5.3.1 Electronics and Semiconductors

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Food and Beverage

- 5.3.4 Pharmaceuticals and Healthcare

- 5.3.5 Retail and E-commerce

- 5.3.6 Others

- 5.4 By Region

- 5.4.1 North

- 5.4.2 Northeast

- 5.4.3 East

- 5.4.4 Central

- 5.4.5 South

- 5.4.6 Southwest

- 5.4.7 Northwest

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 SINOTRANS Limited

- 6.4.2 COSCO Shipping Logistics Co., Ltd.

- 6.4.3 China Merchants Logistics Group Co., Ltd.

- 6.4.4 DHL Group

- 6.4.5 Kuehne+Nagel

- 6.4.6 DSV A/S (Including DB Schenker)

- 6.4.7 CMA CGM Group (Including CEVA Logistics)

- 6.4.8 Nippon Express Holdings

- 6.4.9 NYK Line (Including Yusen Logistics Global Management Co., Ltd)

- 6.4.10 A.P. Moller-Maersk

- 6.4.11 SF Holdings (KEX-SF)

- 6.4.12 SITC International Holdings Co., Ltd.

- 6.4.13 Toll Group

- 6.4.14 Rhenus Logistics

- 6.4.15 AIT Worldwide Logistics, Inc.

- 6.4.16 SEKO Logistics

- 6.4.17 CIMC Logistics (CIMC Shilianda)

- 6.4.18 Huamao International Freight Forwarding Co., Ltd.

- 6.4.19 CTS International Logistics Corporation

- 6.4.20 Basenton Logistics Co., Ltd.

- 6.4.21 Shenzhen King-Hor Supply Chain Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment