|

시장보고서

상품코드

2065543

조달 전사적 자원 계획(ERP) : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Procurement Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

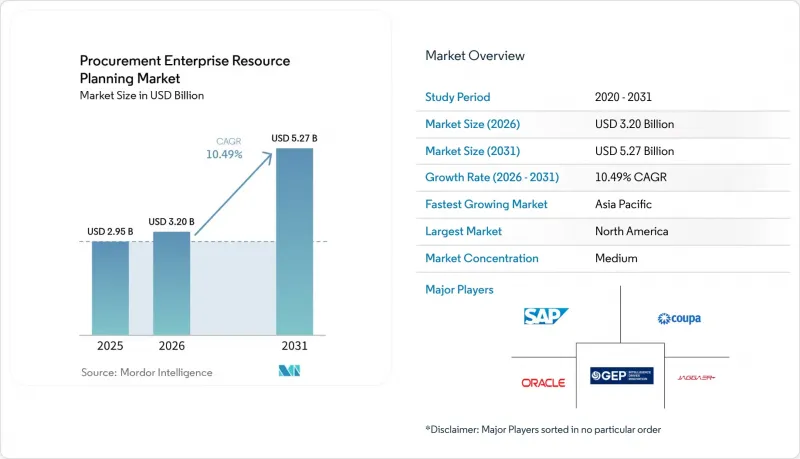

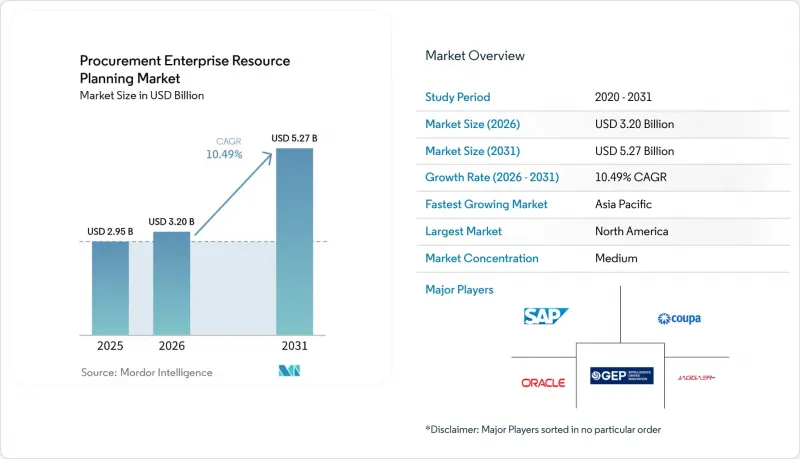

Mordor Intelligence에 의하면, 조달 전사적 자원 계획(ERP) 시장 규모는 2026년에 32억 달러에 달하고, 2031년까지 52억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 10.49%로 성장할 전망입니다.

본 보고서는 배포 방식(클라우드, On-Premise, 하이브리드), 모듈(P2P, S2C 등), 조직 규모(대기업, 중소기업), 최종 사용자 산업(제조, 소매 및 전자상거래, 의료 및 제약, IT 및 통신 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 조달 전사적 자원 계획(ERP) 시장 동향 및 인사이트

클라우드 기반 조달 솔루션 도입 가속화

클라우드 도입을 통해 기업은 하드웨어 교체 주기의 부담에서 벗어나, 수요가 급증할 때에도 유연하게 확장할 수 있게 됩니다. 구독 방식을 통해 초기 라이선스 비용이 절감되어, 중견 기업의 구매자들도 고급 기능을 이용할 수 있게 됩니다. 멀티테넌트 아키텍처를 통해 업무에 지장을 주는 업그레이드 없이 분기마다 AI 기능이 강화되며, 업계 사례에 따르면 여러 레거시 시스템을 마이그레이션한 결과 사이클 타임이 40% 단축된 것으로 나타났습니다. 계절적 변동이 심한 업계에서는 클라우드의 탄력성을 활용함으로써 비수기에 과도한 컴퓨팅 리소스 할당을 억제하고, 총 소유 비용(TCO)을 절감할 수 있습니다.

지출 분석 및 공급업체 리스크 평가를 위한 AI와 ML의 통합

머신러닝 엔진은 발주서, 납품 실적 및 외부 리스크 데이터를 분석하여 동적인 공급업체 스코어카드를 생성합니다. 조기 도입 기업들은 테일 지출을 통합한 후 첫 해에 상당한 비용 절감이 있었습니다고 보고하고 있습니다. 자연어 처리 기술을 통해 지급 조건 및 위약 조항이 자동으로 추출되고, 통합된 채무 일정이 작성됨으로써, 향후 상황을 고려한 재협상이 촉진됩니다. 에이전트형 AI가 저가 발주서 초안 작성과 승인 절차 설정을 일상적으로 수행하므로, 카테고리 매니저는 전략적인 조달 활동에 집중할 수 있습니다.

기존 ERP 통합의 복잡성과 막대한 전환 비용

수십년전의 시스템에서는 조달 데이터가 독자적인 형식으로 저장되어 있기 때문에 예산의 40%를 소모하고 마이그레이션 기간을 18개월 이상으로 연장할 가능성이 있는 비용이 많이 드는 맞춤형 파이프라인을 구축할 수밖에 없습니다. 중복된 공급업체 레코드나 특별 주문 워크플로는 정리하거나 재구성해야 합니다. 한편, 적시 생산 방식을 채택한 제조업체들은 전환 기간 중 발생할 수 있는 가동 중단으로 인한 불이익을 우려하고 있습니다. 이러한 요인들이 클라우드 도입을 지연시키고, 조달 전사적 자원 계획(ERP) 시장 전체의 성장을 둔화시키고 있습니다.

부문별 분석

2025년, 클라우드 기반 솔루션은 조달 전사적 자원 계획(ERP) 시장 점유율의 67.92%를 차지했습니다. 구매 기업들은 자본 지출을 예측 가능한 운영비로 전환하고, 자회사 전체로의 확대를 가속화하는 구독 모델로 전환하고 있습니다. 벤더들은 현재 상시 연결형 아키텍처에 기반한 AI 기반 지출 대시보드 및 협업 도구를 번들로 제공하고 있으며, 이로 인해 클라우드에 대한 선호도가 더욱 높아지고 있습니다. 국가 안보 및 주권 데이터에 관한 규제로 인해 외부 호스팅이 금지된 경우, On-Premise 배포가 계속 이루어지고 있습니다. 'RISE with SAP' 등의 프로그램을 통해 제공되는 하이브리드 토폴로지를 통해 모듈을 단계적으로 전환할 수 있어, 업무 중단 위험을 줄이고 규정 준수를 지원합니다.

하이브리드 모델은 엄격한 감사 요건과 확장 가능한 혁신의 필요성 사이에서 균형을 맞추려는 기업에게 매력적입니다. 제약 기업들은 간접 조달을 클라우드로 전환하는 한편, 원자재 조달은 On-Premise 방식으로 유지하는 경우가 많은 반면, 제조업체들은 동기화 전에 지연에 민감한 데이터를 로컬 에지 노드에서 처리합니다. 다양한 환경을 아우르는 원활한 데이터 흐름을 지원하는 벤더는 조달 전사적 자원 계획(ERP) 시장에서 향후 성장을 위한 우위를 확보하고 있습니다.

P2P(Procure-to-Pay)는 발주부터 지급에 이르는 프로세스를 자동화하는 기반적인 역할을 수행하고 있기 때문에 2025년 매출의 55.12%를 계속 차지했습니다. 한편, 계약 수명주기 관리(CLM)는 AI를 활용한 텍스트 추출 기능을 통해 계약 갱신을 놓치거나 가격 개정 조항이 반영되지 않는 것을 방지할 수 있기 때문에 연평균 성장률(CAGR) 11.01%를 기록하며 성장하고 있습니다. 최신 플랫폼에서는 CLM을 발주서 작성과 직접 연동하여, 협상된 조건을 수작업으로 다시 입력할 필요 없이 실행 가능한 발주서로 변환함으로써, 협상을 통한 비용 절감 효과를 확보하고 있습니다.

지출 분석 엔진은 카테고리별 수요를 예측하고, 테일 지출의 통합 대상을 파악하는 한편, 공급업체 관리 포털은 제3자 위험 점수를 일원화하여 관리합니다. S2C(Source-to-Contract) 제품군은 RFP(제안 요청서)의 전체 라이프사이클을 디지털화하고, 내부 통제 요건을 충족하는 감사 가능한 기록을 보관합니다. 이러한 모듈식 구조의 폭넓은 기능을 통해, 기업은 조달 전사적 자원 계획(ERP) 시장의 성숙도가 높아짐에 따라 전략적 기능으로 확장해 나갈 수 있게 됩니다.

지역별 분석

북미는 2025년 매출의 33.64%를 차지했습니다. 이는 성숙한 ERP 생태계와 통일된 조달 프로세스를 의무화한 엄격한 투명성 규정에 힘입은 결과입니다. 기후 변화 정보 공개 의무화에 따라 공급업체 수준의 탄소 배출량을 기록하는 플랫폼 도입이 확대되고 있으며, 캐나다의 강제노동법에서는 ERP 감사 기록을 바탕으로 작성된 연례 실사 보고서의 제출이 의무화되어 있습니다. 멕시코에서 일고 있는 니어쇼어링의 물결은 통관 서류와 품질 지표를 통합하는 국경을 초월한 조달 솔루션에 대한 수요를 더욱 부추기고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 10.76%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 중국과 인도의 제조업체들은 수출 기준을 충족하고 사이클 타임을 단축하기 위해 조달 업무의 디지털화를 추진하고 있는 반면, 일본 기업들은 공급업체의 성과를 ‘인더스트리 4.0’ 품질 대시보드에 통합하고 있습니다. 동남아시아의 신흥 경제국에서는 증가하는 외국인 투자를 지원하기 위해 다국어 지원 및 세무 규정 준수를 충족하는 조달 포털이 도입되고 있으며, 토큰화된 결제 인프라를 통해 분산된 은행 네트워크를 넘나드는 공급업체에 대한 결제가 원활해지고 있습니다.

유럽 시장은 인권 및 환경 평가를 의무화하는 지침에 따라 형성되어 있습니다. 독일의 한 대형 자동차 제조업체는 ERP 플랫폼을 통해 수천 개의 2차 공급업체를 관리하고 ESG 지표를 추적하고 있으며, 영국 기업은 브렉시트 이후 영국과 EU의 서로 다른 규정 준수 요건을 조율해야 합니다. 프랑스의 부패방지법은 공급업체 온보딩 과정에서 이해상충 점검을 장려하고 있습니다. 남미, 중동 및 아프리카에서도 각국 정부가 전자입찰 포털을 도입하고, 다국적 기업들이 전 세계적인 시스템 제품군을 현지 자회사에 확대 적용함에 따라 조달 업무의 현대화가 가속화되고 있으며, 조달 전사적 자원 계획(ERP) 시장이 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the procurement enterprise resource planning(ERP) market size is projected to be USD 3.20 billion in 2026 and reach USD 5.27 billion by 2031, growing at a CAGR of 10.49% over 2026-2031.

This report is Segmented by Deployment Mode (Cloud, On-Premises, and Hybrid), Module (Procure-To-Pay, Source-To-Contract, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Manufacturing, Retail and E-Commerce, Healthcare and Pharmaceutical, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Procurement Enterprise Resource Planning Market Trends and Insights

Accelerating Adoption of Cloud-Based Procurement Suites

Cloud deployment frees enterprises from hardware refresh cycles and supports elastic scaling during demand spikes. Subscription economics cut upfront license costs, making advanced capabilities accessible to mid-market buyers. Multi-tenant architectures deliver quarterly AI enhancements without disruptive upgrades, and industry examples show 40% reductions in cycle time after migrating multiple legacy systems. Seasonal sectors benefit from cloud elasticity, which curbs overprovisioned compute during off-peak months, improving the total cost of ownership.

Integration of AI and ML for Spend Analytics and Supplier Risk Scoring

Machine-learning engines mine purchase orders, delivery performance, and external risk data to generate dynamic supplier scorecards. Early adopters report considerable cost savings in the first year after consolidating tail spend. Natural-language processing automatically extracts payment terms and penalty clauses, creating centralized obligation calendars that trigger proactive renegotiations. Agentic AI routinely drafts low-value purchase orders and routes approvals, allowing category managers to focus on strategic sourcing.

Legacy ERP Integration Complexity and High Migration Costs

Decades-old systems store procurement data in proprietary formats, forcing costly custom pipelines that can consume 40% of the budget and extend cutover beyond 18 months. Duplicate supplier records and bespoke workflows must be cleansed or rebuilt, while just-in-time manufacturers fear downtime penalties during transition. Those factors delay cloud adoption and slow the overall growth of the Procurement ERP market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for End-to-End Source-to-Pay Automation Among Large Enterprises

- Increasing Regulatory Emphasis on Supply-Chain Transparency and ESG Compliance

- Persistent Data Security and Privacy Concerns in Cloud Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based solutions commanded 67.92% of the Procurement ERP market share in 2025. Buyers are shifting to subscription models that convert capital expenses into predictable operating expenses and accelerate rollout across subsidiaries. Vendors now bundle AI-powered spend dashboards and collaboration tools that depend on always-connected architectures, reinforcing cloud preference. On-premises deployments persist where national security or sovereign data rules prohibit external hosting. Hybrid topologies, offered under programs like RISE with SAP, allow gradual module migration, mitigating disruption risk and supporting compliance.

Hybrid models appeal to companies balancing strict audit mandates with the need for scalable innovation. Pharmaceutical firms often keep ingredient sourcing on-premises while moving indirect procurement to the cloud, while manufacturers process latency-sensitive data at local edge nodes before synchronization. Vendors that support seamless data flow across environments position themselves for additional growth in the Procurement ERP market.

Procure-to-Pay retained 55.12% of 2025 revenue thanks to its foundational role in automating requisition-to-payment processes. However, Contract Lifecycle Management is growing at a 11.01% CAGR because AI text-extraction prevents missed renewals and uncaptured escalators. Modern platforms link CLM directly to requisition creation, turning negotiated terms into executable purchase orders without manual re-keying, which protects negotiated savings.

Spend-analysis engines forecast category demand and identify tail-spend consolidation, while supplier-management portals centralize third-party risk scores. Source-to-Contract suites now digitize the entire RFP life cycle, capturing auditable records that meet internal control requirements. This modular breadth enables enterprises to scale into strategic functionality as the Procurement ERP market maturity increases.

Geography Analysis

North America accounted for 33.64% of 2025 revenue, driven by mature ERP ecosystems and stringent transparency rules that compelled unified procurement processes. Climate-disclosure mandates drive the adoption of platforms that record supplier-level carbon emissions, and Canadian forced-labor laws require annual due diligence reports captured by ERP audit trails. Mexico's nearshoring wave further stimulates cross-border procurement suites that integrate customs documentation and quality metrics.

Asia-Pacific is the fastest-growing region at a 10.76% CAGR. Chinese and Indian manufacturers digitize procurement to meet export standards and reduce cycle times, while Japanese firms embed supplier performance into Industry 4.0 quality dashboards. Emerging Southeast Asian economies deploy multi-language, tax-compliant procurement portals to support rising foreign investment, and tokenized payment rails ease supplier settlement across fragmented banking networks.

Europe's market is shaped by directives mandating human rights and environmental assessments. German automotive giants manage thousands of tier-two suppliers on ERP platforms to track ESG metrics, and United Kingdom companies must reconcile divergent UK and EU compliance after Brexit. France's anti-corruption law drives conflict-of-interest checks at supplier onboarding. Procurement modernization is also accelerating in South America, the Middle East, and Africa as governments adopt e-tender portals and multinationals extend global suites to local subsidiaries, broadening the Procurement ERP market footprint.

List of Companies Covered in this Report:

- SAP SE

- Coupa Software Incorporated

- Oracle Corporation

- Jaggaer LLC

- Ivalua Inc.

- GEP Worldwide LLC

- Basware Oyj

- Zycus Inc.

- Proactis Holdings Limited

- Tradeshift Holdings Inc.

- Workday Inc.

- Infor Inc.

- Precoro Inc.

- Procurify Technologies Inc.

- Vroozi Inc.

- Medius Sverige AB

- Synertrade SES AG

- Xeeva Inc.

- Scanmarket A/S

- BirchStreet Systems LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Adoption of Cloud-Based Procurement Suites

- 4.2.2 Integration of AI and ML for Spend Analytics and Supplier Risk Scoring

- 4.2.3 Rising Demand for End-to-End Source-to-Pay Automation Among Large Enterprises

- 4.2.4 Increasing Regulatory Emphasis on Supply-Chain Transparency and ESG Compliance

- 4.2.5 Cross-Border Tokenized Payment Rails Enabling Real-Time Supplier Settlement

- 4.2.6 Agentic Procurement Bots Reducing Sourcing Cycle Time in Mid-Market Firms

- 4.3 Market Restraints

- 4.3.1 Legacy ERP Integration Complexity and High Migration Costs

- 4.3.2 Persistent Data Security and Privacy Concerns in Cloud Deployments

- 4.3.3 Shortage of Procurement-Tech Talent to Configure AI Workflows

- 4.3.4 Algorithmic Bias Risks in AI-Driven Supplier Selection Engines

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Module

- 5.2.1 Procure-to-Pay (P2P)

- 5.2.2 Source-to-Contract (S2C)

- 5.2.3 Contract Lifecycle Management (CLM)

- 5.2.4 Spend Analysis

- 5.2.5 Supplier Management

- 5.2.6 Other Modules

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-commerce

- 5.4.3 Healthcare and Pharmaceutical

- 5.4.4 Banking Financial Services and Insurance (BFSI)

- 5.4.5 Information Technology and Telecom

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Coupa Software Incorporated

- 6.4.3 Oracle Corporation

- 6.4.4 Jaggaer LLC

- 6.4.5 Ivalua Inc.

- 6.4.6 GEP Worldwide LLC

- 6.4.7 Basware Oyj

- 6.4.8 Zycus Inc.

- 6.4.9 Proactis Holdings Limited

- 6.4.10 Tradeshift Holdings Inc.

- 6.4.11 Workday Inc.

- 6.4.12 Infor Inc.

- 6.4.13 Precoro Inc.

- 6.4.14 Procurify Technologies Inc.

- 6.4.15 Vroozi Inc.

- 6.4.16 Medius Sverige AB

- 6.4.17 Synertrade SES AG

- 6.4.18 Xeeva Inc.

- 6.4.19 Scanmarket A/S

- 6.4.20 BirchStreet Systems LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment