|

시장보고서

상품코드

2065743

의료 ERP 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Healthcare Enterprise Resource Planning (ERP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

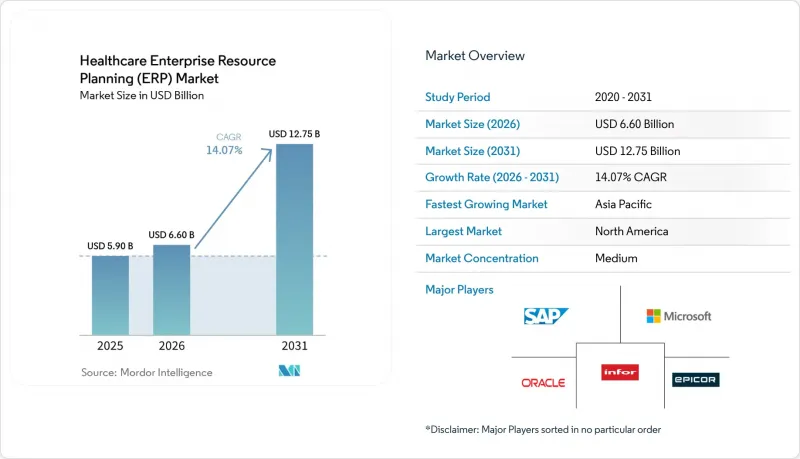

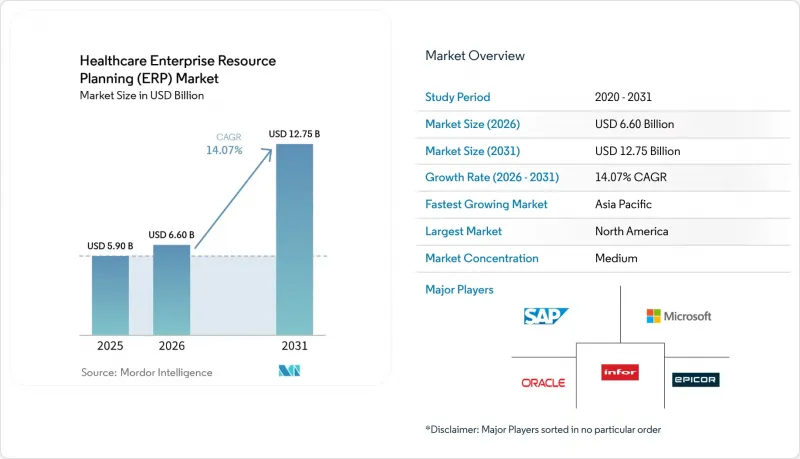

Mordor Intelligence에 의하면, 의료 ERP 시장 규모는 2025년 59억 달러, 2026년 66억 달러에서 2031년까지 127억 5,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 14.07%를 나타낼 전망입니다.

본 보고서는 배포 모델(클라우드 기반, On-Premise형, 하이브리드형), 구성 요소(소프트웨어 및 서비스), 기능(재무 및 회계, 공급망·물류 등), 최종 사용자(병원, 진료소·외래수술센터(ASC), 제약·바이오기술 기업, 의료기기 제조업체 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 의료 ERP 시장 동향과 인사이트

ERP 제품군에 AI 기반 분석 기능 통합

인공지능은 단순한 상황 설명형 대시보드에서 벗어나, 인력 배치, 재고, 수술 일정을 실시간으로 조정하는 자율적인 의사결정 단계로 전환되고 있습니다. Oracle은 2024년에 Fusion Cloud 제품군 전체에 생성형 AI를 통합하여, 재무 팀이 총계정원장(G/L)과 상호작용함으로써 분개 전표 입력 작업을 자동화할 수 있도록 했습니다. 인포 클라우드 스위트 헬스케어는 머신러닝을 활용하여 외과 의사의 선호도를 바탕으로 임플란트 수요를 예측함으로써, 미국 내 여러 병원에서 폐기물을 줄였습니다. 커뮤니티 헬스 시스템즈(Community Health Systems)는 AI를 활용한 수익 사이클 모듈을 가동한 지 6개월 만에 보험 청구 불승인률이 18% 감소했다고 보고했으며, 이를 통해 4,700만 달러의 환급금을 회수했습니다(chs.net). 특히 인건비가 가장 높은 분야에서 월별 결산을 5일 이내에 완료할 수 있는 능력은 경쟁상 필수 요건으로 자리 잡고 있습니다. 각 벤더사는 핵심 거래 처리 기능이 아닌 AI 기능을 통한 차별화를 경쟁하고 있으며, 이것이 전체 연평균 성장률(CAGR)을 3.2포인트 끌어올리는 요인이 되고 있습니다.

환자별 비용 가시화에 대한 수요 증가

일괄 지급 제도나 예측 지급 제도에서는 환자 및 시술 수준에서 세밀한 비용 배분이 요구됩니다. 기존의 야간 일괄 처리에 의한 원가 계산만으로는 불충분하기 때문에 현재는 실시간 엔진이 의료 자재의 사용 현황, 근로 시간 기록, 약제 조제 현황을 발생 즉시 파악하여 몇 시간 이내에 이익률 하락을 지적할 수 있게 되었습니다. CostFlex를 시범 도입한 미국 내 400병상 규모의 병원에서는 사례별 변동 폭을 22% 줄임으로써, 치료 성과를 저해하지 않으면서도 더 저렴한 임플란트로 대체하는 데 성공했습니다. Infinx사에 따르면, 재무 데이터와 임상 데이터가 즉시 연동된 결과, 사전 승인 처리 시간이 14% 단축되었습니다. CMS(미국 의료보험센터)가 2027년까지 병원에 지급하는 보상금의 30%를 비용 대비 효과 지표에 연동하기로 함에 따라, 실시간 인사이트에 대한 수요가 북미에서 아시아태평양으로 확대되고 있습니다. 이러한 요인으로 인해 CAGR은 2.8포인트 상승했습니다.

높은 초기 라이선스 및 도입 비용

엔터프라이즈 프로젝트에서는 범위 확대나 데이터 마이그레이션 과정에서 발생하는 실수가 드러나면서, 예산을 30-50% 초과하는 경우가 종종 있습니다. 오하이오주의 유니버시티 호스피털스는 4억 달러를 투자해 구축한 에픽(Epic) 시스템에 추가로 8,000만 달러의 컨설팅 및 하드웨어 비용이 필요했다고 밝혔습니다. 한편, 트리니티 헬스의 8억 달러 규모 시스템 도입으로 인해 다른 IT 프로젝트들이 불가피하게 지연되었습니다. 500만-1,000만 달러의 예산을 책정한 중규모 병원의 경우, 숨겨진 인터페이스 비용으로 인해 총 비용이 2,000만 달러 가까이 불어나는 일이 종종 있습니다. 수익성이 낮은 지방 의료기관들은 최신 ERP 도입을 완전히 미루고 있으며, 그 결과 스프레드시트에 의존하는 업무 프로세스가 장기화되면서 규정 준수 위험이 높아지고 있습니다. 인플레이션으로 인한 컨설팅 비용 급등이 계속해서 부담으로 작용하며, 전 세계 연평균 성장률(CAGR)을 2.1포인트 끌어내리고 있습니다.

부문별 분석

하이브리드 클라우드 도입은 2031년까지 연평균 성장률(CAGR) 17.60%로 확대되고 있습니다. 2025년에는 클라우드가 의료 ERP 시장의 46.20%를 차지했으나, 최고정보책임자(CIO)들은 지연이나 데이터 주권 등의 이유로 전자건강기록 및 특정 분석 기능을 여전히 On-Premise 환경에서 운영하고 있습니다. 하이브리드 환경에서는 재무 및 공급망 부서를 우선적으로 이전함으로써 설비 투자(CAPEX)를 줄이면서, 지역의 데이터 현지화 규정에도 대응할 수 있습니다. On-Premise 도입 규모는 축소되는 추세이지만, 10년 이상 된 미들웨어에 대한 투자를 안고 있는 대학 부속 의료센터 내에서는 여전히 유지되고 있습니다. 모나쉬 헬스(Monash Health)의 단계적 도입을 통해 5년 동안 총 비용을 34% 절감한 한편, 사우디아라비아의 알라지 메디신(Alrajhi Medicine)도 유사한 구성으로 수천 명의 사용자를 지원하고 있습니다. 이 모델의 성장은 개인정보 보호 규제가 강화되는 가운데, 의료 ERP 시장이 도입의 민첩성을 얼마나 중시하고 있는지를 여실히 보여주고 있습니다.

두 번째 호재는 공급업체의 방침입니다. SAP는 2027년에 ECC의 메인스트림 유지보수를 종료할 예정이며, Oracle의 최신 라이선스 조건에서도 클라우드 계약 갱신을 권장하고 있습니다. 데이터센터에서 완전히 이전할 수 없는 병원에서는 On-Premise 임상 관리 시스템과 클라우드상의 관리 모듈을 연동하기 위해 컨테이너화된 미들웨어를 선택하고 있습니다. 따라서 하이브리드 방식이 확산됨에 따라 의료 ERP 시장 규모는 관세, 운송, 다중 통화 회계 등이 복잡성을 더하는 대규모 시스템이나 국경을 초월한 그룹에서 그 우위를 더욱 확대해 나갈 것입니다.

2025년 시점에서도 매출의 61.00%는 여전히 소프트웨어가 차지하고 있지만, 일부 병원에서는 임상 워크플로우를 ERP 템플릿에 매핑하기 위한 인력을 배치하고 있어 서비스 부문은 연평균 15.40%의 속도로 성장하고 있습니다. 컨설팅, 통합, 관리형 서비스를 포함하는 의료 ERP 시장은 2031년까지 50억 달러를 넘어설 것으로 전망됩니다. Nordic Consulting과 Pivot Point는 12개월 이내에本番 가동을 보장하는 정액제 마이그레이션 패키지를 제공합니다. 자격을 갖춘 인력 부족(ERP 관련 평균 채용 기간 89일)으로 인해 아웃소싱 수요는 계속해서 증가하고 있습니다.

로우코드 플랫폼은 설정 작업을 줄여주지만, 완전히 없애주는 것은 아닙니다. 비용 센터, 카탈로그 품목, 보조금 코드를 기존 객체에 매핑하려면 여전히 전문 지식이 필요합니다. 제약 기업들은 21 CFR Part 11에 따른 검증의 복잡성에 직면해 있으며, 문서화 및 테스트 스크립트 작성 업무가 급증하고 있습니다. 구독형 라이선싱으로 인해 소프트웨어의 이익률이 압박을 받는 가운데, 각 벤더사가 자체적으로 도입 지원 부서를 강화하고 있어 의료 ERP 시장의 수익 구조는 계속해서 서비스 분야로 이동하고 있습니다.

지역별 분석

2025년, 북미는 매출의 41.70%를 차지했습니다. ONC의 HTI-1 최종 규정에 따라, 정보 차단에 대한 정의가 재무 데이터로도 확대되었으며, 청구 및 보험 청구 정보 교환 시 인증된 FHIR API의 사용이 의무화되었습니다. 미국 병원만 해도 연간 900억-1,000억 달러를 IT에 투자하고 있는 반면, 캐나다에서는 재무 보고의 표준화를 도모하기 위해 주 전체 차원에서 ERP 도입을 시범적으로 추진하고 있습니다. 멕시코의 민간 병원들은 의료 관광객을 유치하고 국제 인증을 획득하기 위해 ERP 도입을 추진하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 16.80%로 성장하고 있습니다. 중국 국가위생건강위원회는 2030년까지 3차 병원의 95%를 디지털화하는 것을 목표로 하고 있으며, 3만 개 시설에 ERP 및 EHR을 패키지로 도입하는 것을 추진하고 있습니다. 2024년에 도입된 일본의 ‘마이넘버 건강보험증’은 본인 부담금을 실시간으로 정산하기 위해 백오피스 시스템과의 통합이 필요한 반면, 인도의 ‘아유슈만 바라트 디지털 미션’에서는 6억 명의 국민에게 통합 ID가 발급되면서, 클라우드 ERP로만 처리할 수 있을 정도의 거래량이 급증하고 있습니다. 호주의 ‘마이 헬스 레코드(My Health Record)’는 국가 디지털 헬스 전략의 일환으로 재무 데이터와 임상 데이터를 연계하고 있습니다.

유럽은 매출의 약 4분의 1을 차지하고 있으며, 독일, 영국, 프랑스가 이를 주도하고 있습니다. GDPR(EU 개인정보보호규정)에 따른 막대한 벌금으로 인해, 공급업체들은 해당 지역 내 데이터 보관을 보장할 수밖에 없게 되었습니다. 독일의 의무화된 전자 환자 기록(ePA)은 임상 데이터와 재무 데이터를 연계하고 있으며, 영국의 NHS 연합 데이터 플랫폼은 200개 이상의 트러스트에 걸친 지표를 통합하고 있습니다. 2025년부터 유럽 건강 데이터 공간(European Health Data Space)이 도입됨에 따라, 국경을 초월한 청구 데이터에 관한 요건이 도입될 예정입니다. 남미는 소규모 기반에서 성장하고 있으며, 브라질에서는 민간 병원 체인의 시설 개선이 진행되고 있고, 아르헨티나에서는 공립 병원의 현대화가 추진되고 있습니다. 중동은 두 자릿수의 연평균 성장률(CAGR)을 기록하고 있으며, 사우디아라비아의 1,000억 사우디 리얄(266억 3,000만 달러) 규모의 ‘비전 2030’ 투자나, 아랍에미리트의 ‘스마트 두바이 헬스’ 프로그램 등이 대표적인 사례이며, 이 모든 것이 의료 ERP 시장의 성장을 뒷받침하는 요인이 되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the healthcare ERP market size is projected to expand from USD 5.90 billion in 2025 and USD 6.60 billion in 2026 to USD 12.75 billion by 2031, registering a CAGR of 14.07% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premise, and Hybrid), Component (Software and Services), Function (Finance and Accounting, Supply Chain and Logistics, and More), End User (Hospitals, Clinics and Ambulatory Surgical Centers, Pharmaceutical and Biotechnology Companies, Medical Device Manufacturers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Enterprise Resource Planning (ERP) Market Trends and Insights

Integration Of AI Driven Analytics Into ERP Suites

Artificial intelligence is shifting from descriptive dashboards to autonomous decisions that adjust staffing, inventory, and surgical scheduling in real time. Oracle embedded generative AI across its Fusion Cloud suite in 2024, allowing finance teams to converse with the ledger and automate journal entries. Infor CloudSuite Healthcare deployed machine learning to forecast implant demand using surgeon preference cards, reducing waste across multiple U.S. hospitals. Community Health Systems documented an 18% drop in claim denials six months after activating AI-powered revenue-cycle modules, translating into USD 47 million in recovered reimbursements chs.net. The ability to close monthly books in under five days is becoming a competitive necessity, especially where labor costs are highest. Vendors are racing to differentiate on AI capabilities rather than core transaction processing, magnifying the driver's 3.2-point boost to the overall CAGR.

Rising Demand For Real Time Patient Costing Visibility

Bundled payments and prospective payment systems require granular cost attribution at the patient and procedure level. Traditional overnight batch costing is inadequate, so real-time engines now capture supply usage, labor stamps, and pharmacy dispenses as they occur, flagging margin leakage within hours. A 400-bed U.S. hospital piloting CostFlex cut per-case variance by 22% and enabled lower cost implant substitutions without harming outcomes. Infinx reported 14% faster prior-authorization turnaround, where finance and clinical data interfaced instantly. As CMS ties 30% of hospital reimbursement to cost-efficiency metrics by 2027, demand for real-time insight is spreading from North America to Asia-Pacific. The driver adds 2.8 percentage points to the CAGR.

High Upfront Licensing And Implementation Costs

Enterprise projects often exceed budgets by 30-50% as scope expands and data migration missteps surface. University Hospitals in Ohio said its USD 400 million Epic build needed another USD 80 million in consulting and hardware, while Trinity Health's USD 800 million rollout forced other IT projects into limbo. Mid-size hospitals budgeting USD 5-10 million often see hidden interface costs push totals to near USD 20 million. Rural facilities with thin margins postpone modern ERP altogether, prolonging spreadsheet-driven processes that elevate compliance risk. Inflation-driven consulting rates keep pressure high, shaving 2.1 points from CAGR worldwide.

Other drivers and restraints analyzed in the detailed report include:

- Migration Toward Value Based Reimbursement Models

- Post Pandemic Acceleration Of Cloud First Hospital IT Strategies

- Data Security Concerns Around Multi Tenant Cloud Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid cloud installations are advancing at a 17.60% CAGR through 2031. Although cloud captured 46.20% of the healthcare ERP market share in 2025, chief information officers still keep electronic health records and certain analytics on-premise for latency and sovereignty reasons. Hybrid lets finance and supply chain migrate first, easing capex while meeting regional data-localization rules. On-premise footprints shrink but persist inside academic medical centers, housing decade-old middleware investments. Monash Health's split deployment cut total cost by 34% in five years, while Saudi Arabia's Alrajhi Medicine supports thousands of users in a similar setup. The model's growth underscores how the healthcare ERP market rewards deployment agility amid tightening privacy mandates.

A second tailwind is vendor policy. SAP sunsets ECC mainstream maintenance in 2027, and Oracle's latest license terms favor cloud renewals. Hospitals unable to fully exit data centers are selecting containerized middleware to bridge on-premise clinical engines with cloud-resident administrative modules. The healthcare ERP market size for hybrid deployments will therefore widen its lead among large systems and cross-border groups where customs, shipping, and multi-currency accounting add complexity.

Software still accounted for 61.00% of revenue in 2025, but services are expanding at 15.40% each year, as a few hospitals retain staff to map clinical workflows into ERP templates. The healthcare ERP market, including consulting, integration, and managed services, will exceed USD 5 billion by 2031. Nordic Consulting and Pivot Point are packaging fixed-fee migrations that promise go-lives in under 12 months. Shortages of qualified staff, average ERP vacancy sits at 89 days, keep driving outsourcing demand.

Low-code platforms reduce but do not eliminate configuration work; mapping cost centers, catalog items, and grant codes into pre-built objects still requires domain expertise. Pharmaceutical firms face additional validation complexity under 21 CFR Part 11, swelling documentation and test-script workloads. As subscription licensing compresses software margins, vendors themselves are ramping up implementation arms, ensuring the healthcare ERP market continues to shift its revenue mix toward services.

Geography Analysis

North America commanded 41.70% of revenue in 2025. ONC's HTI-1 Final Rule extended information-blocking definitions to financial data, compelling the use of certified FHIR APIs for billing and claims exchange. U.S. hospitals alone invest USD 90-100 billion in IT annually, while Canada pilots province-wide ERP rollouts to harmonize fiscal reporting. Mexican private hospitals are embracing ERPs to attract medical tourists and secure international accreditations.

Asia-Pacific is expanding at 16.80% CAGR. China's National Health Commission targets 95% digitization of tertiary hospitals by 2030, pushing ERP and EHR bundles into 30,000 facilities. Japan's My Number insurance card, launched in 2024, requires back-office integration for real-time copay adjudication, and India's Ayushman Bharat Digital Mission gives 600 million citizens unified IDs, spiking transaction volumes that only cloud ERPs can handle. Australia's My Health Record ties financial and clinical data together as part of its national digital health strategy.

Europe held roughly one-quarter of sales, led by Germany, the United Kingdom, and France. GDPR's stiff fines force vendors to guarantee regional data residency. Germany's mandatory ePA aligns clinical and fiscal datasets, and the U.K. NHS Federated Data Platform unifies metrics across more than 200 trusts. The implementation of the European Health Data Space from 2025 introduces cross-border billing data requirements. South America grows off a smaller base, with Brazil upgrading private chains and Argentina modernizing public hospitals. The Middle East enjoys double-digit CAGR, exemplified by Saudi Arabia's SAR 100 billion (USD 26.63 billion) Vision 2030 investment and the United Arab Emirates' Smart Dubai Health program, all catalysts for the healthcare ERP market.

- SAP SE

- Oracle Corporation

- Infor, Inc.

- Microsoft Corporation

- Epicor Software Corporation

- Workday, Inc.

- Cerner Corporation

- McKesson Corporation

- Sage Group plc

- QAD Inc.

- Unit4 N.V.

- Syspro (Pty) Ltd

- IFS AB

- Ramco Systems Limited

- Acumatica, Inc.

- Deltek, Inc.

- Aptean, Inc.

- Kronos Incorporated

- Global Shop Solutions, Inc.

- Plex Systems, Inc.

- NetSuite Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of AI Driven Analytics Into ERP Suites

- 4.2.2 Rising Demand for Real Time Patient Costing Visibility

- 4.2.3 Migration Toward Value Based Reimbursement Models

- 4.2.4 Post Pandemic Acceleration of Cloud First Hospital IT Strategies

- 4.2.5 Government Mandates for Interoperable Financial Reporting

- 4.2.6 Emergence of Industry Specific Low Code ERP Platforms

- 4.3 Market Restraints

- 4.3.1 High Upfront Licensing and Implementation Costs

- 4.3.2 Data Security Concerns Around Multi Tenant Cloud Deployments

- 4.3.3 Shortage of Healthcare IT Staff Skilled in ERP Migration

- 4.3.4 Integration Complexities With Legacy Clinical Systems

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Deployment Model

- 5.1.1 Cloud Based

- 5.1.2 On Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Function

- 5.3.1 Finance and Accounting

- 5.3.2 Supply Chain and Logistics

- 5.3.3 Human Resources

- 5.3.4 Customer Relationship Management

- 5.3.5 Inventory and Material Management

- 5.3.6 Other Functions

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Clinics and Ambulatory Surgical Centers

- 5.4.3 Pharmaceutical and Biotechnology Companies

- 5.4.4 Medical Device Manufacturers

- 5.4.5 Health Insurance Providers

- 5.4.6 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Infor, Inc.

- 6.4.4 Microsoft Corporation

- 6.4.5 Epicor Software Corporation

- 6.4.6 Workday, Inc.

- 6.4.7 Cerner Corporation

- 6.4.8 McKesson Corporation

- 6.4.9 Sage Group plc

- 6.4.10 QAD Inc.

- 6.4.11 Unit4 N.V.

- 6.4.12 Syspro (Pty) Ltd

- 6.4.13 IFS AB

- 6.4.14 Ramco Systems Limited

- 6.4.15 Acumatica, Inc.

- 6.4.16 Deltek, Inc.

- 6.4.17 Aptean, Inc.

- 6.4.18 Kronos Incorporated

- 6.4.19 Global Shop Solutions, Inc.

- 6.4.20 Plex Systems, Inc.

- 6.4.21 NetSuite Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment