|

시장보고서

상품코드

2065548

프로젝트 기반 전사적 자원 계획(ERP) : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Project-Based Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

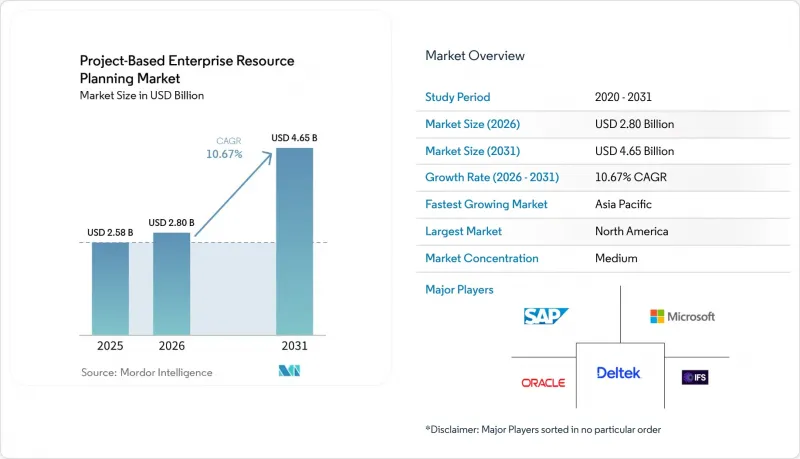

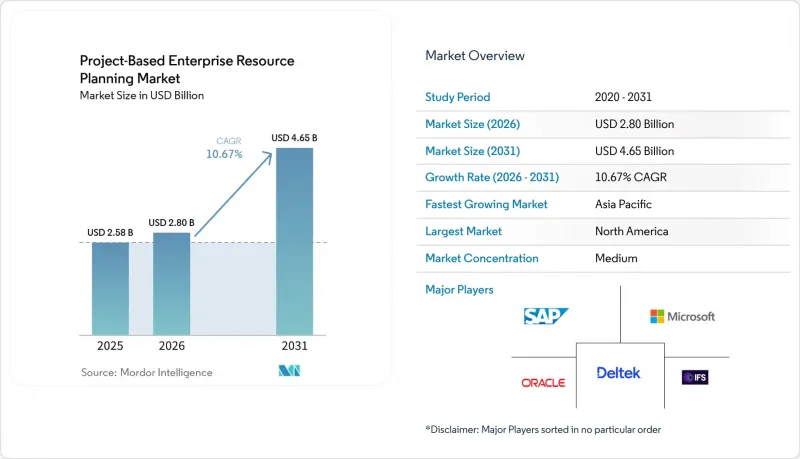

Mordor Intelligence에 의하면, 프로젝트 기반 전사적 자원 계획(ERP) 시장 규모는 2025년 25억 8,000만 달러로 평가되었습니다. 2026년 28억 달러에서 2031년까지 46억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 10.67%를 나타낼 것으로 예측됩니다.

본 보고서는 배포 방식(On-Premise, 클라우드/SaaS, 하이브리드), 조직 규모(대기업, 중소기업), 구성 요소(소프트웨어, 서비스), 최종 사용자 산업(건설 및 엔지니어링, 전문 서비스, 항공우주 및 방위, 정부·공공 서비스, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 프로젝트 기반 전사적 자원 계획(ERP) 시장 동향 및 인사이트

재택근무와 분산형 프로젝트 팀의 도입

2025년, 원격 및 하이브리드 근무 방식이 정착되면서 기업들은 VPN 접속이나 데스크톱 클라이언트에 의존하는 On-Premise형 시스템을 폐지할 수밖에 없게 되었습니다. 현재 클라우드 네이티브 프로젝트 기반 전사적 자원 계획(ERP) 시장 플랫폼에는 모바일 인터페이스가 기본으로 탑재되어 있어, 현장 엔지니어들은 어떤 기기에서든 근무 기록표를 제출하거나 변경 지시서를 승인할 수 있게 되었습니다. 이를 통해 항공우주 및 전문 서비스 분야의 파일럿 도입 사례에서 승인 주기가 40% 단축되었습니다. 시간 기록이 몇 시간 이내에 등록됨으로써 청구 가능한 가동률이 향상되고, 수작업으로 인한 지연으로 인해 손실될 뻔했던 이익률이 유지됩니다. 구매자들은 타사 도구를 거치는 대신, 채팅, 문서 관리, 워크플로 승인 기능을 ERP 내에 직접 통합한 공급업체를 점점 더 선호하는 추세입니다. 이러한 통합을 통해 사용자 교육이 간소화되고 통합에 따른 부대 비용이 절감되므로, 원격 협업은 중요한 구매 기준이 되고 있습니다. 그 결과, 분산형 팀을 위한 경험을 최적화한 솔루션 제공업체가 경쟁 입찰에서 유리한 고지를 점하고 있습니다.

SaaS 및 구독형 가격 모델로의 전환

각 벤더들이 On-Premise 버전의 지원 종료일을 발표하는 가운데, 프로젝트 기반 전사적 자원 계획(ERP) 시장은 구독형 계약으로 결정적으로 전환되고 있습니다. Epicor의 2026년 1월까지의 로드맵에 따르면, 고객에게 4년의 전환 기간이 주어졌으며, 이 기한으로 인해 의사결정 주기가 단축되고 클라우드 도입이 가속화되고 있습니다. SaaS는 서버 하드웨어 비용을 절감해 주지만, 그 대신 설비 투자를 지속적인 운영 비용으로 전환하게 되어, 장기적으로는 영구 라이선스의 상각비를 초과할 가능성이 있습니다. 지속적인 기능 업데이트와 유연한 사용자 수 확장을 중시하는 기업에게는 이러한 상충 관계가 매력적이지만, 직원 수가 안정적인 조직은 구독의 총 생애 비용을 신중하게 평가해야 합니다. 전환 기간이 촉박해짐에 따라, 리스크 회피 성향이 강한 업계조차 데이터 변환 프로젝트를 가속화할 수밖에 없게 되었으며, 이는 프로젝트 기반 전사적 자원 계획(ERP) 시장 전체에서 클라우드 매출의 두 자릿수 성장을 뒷받침하고 있습니다.

기존 ERP 플랫폼에서 전환하는 데 드는 높은 비용

과거 데이터 이전, 맞춤형 통합 재구축 및 사용자 교육에는 18-24개월이 소요되며, 복잡한 추출 작업의 경우 예산을 30% 이상 초과할 가능성이 있습니다. 15년 동안 사용해 온 Deltek 시스템을 교체하는 한 중견 엔지니어링 기업은 전환 기간 동안 기존 시스템의 비용 코드를 매핑하고, 유효한 계약에 대한 감사 추적을 유지해야 합니다. NetSuite의 ‘SuiteSuccess’나 Unit4의 로우코드 구성은 일정을 단축하는 데 도움이 되지만, 투자 장벽이 높기 때문에 리스크 회피 성향이 강한 CFO들을 주저하게 만들고 있습니다. 대규모 도입의 경우, 신속한 구현 프레임워크의 신뢰성이 입증되기 전까지는 높은 전환 비용으로 인해 프로젝트 기반 전사적 자원 계획(ERP) 시장의 일부에서 도입 속도가 둔화될 것입니다.

부문별 분석

기업들이 프라이빗 클라우드의 데이터베이스와 퍼블릭 클라우드의 협업 모듈을 결합함에 따라, 하이브리드 구성은 2031년까지 연평균 성장률(CAGR) 17.80%로 확대되고 있습니다. 2025년에는 클라우드 도입이 프로젝트 기반 전사적 자원 계획(ERP) 시장의 52.12%를 차지하며, 공급업체가 관리하는 보안 및 자동 업그레이드에 대한 구매자의 신뢰가 입증되었습니다. 예를 들어, 건설 대기업의 경우 기밀성이 높은 재무 데이터는 사설 인프라에 보관하면서, 현장 엔지니어를 지원하기 위해 모바일 현장 서비스 및 분석 워크로드를 퍼블릭 SaaS에 배치하는 방안을 고려할 수 있습니다. 벤더들이 혁신을 클라우드 버전으로 한정하고 있기 때문에 On-Premise 방식의 프로젝트 기반 전사적 자원 계획(ERP) 시장 규모는 축소되는 추세이지만, 에어갭 네트워크가 필요한 국방 및 중요 인프라 분야의 고객들 사이에서는 여전히 수요가 유지되고 있습니다.

도입 모델을 선택하는 조직은 구독료, 데이터 전송 비용, 통합 비용 등 총비용과 확장성의 유연성을 저울질하며 평가했습니다. 마이크로소프트의 단계적 Dynamics 365 옵션과 SAP의 RISE 프로그램은 운영 위험을 줄이는 단계적 전환을 촉진하고 있습니다. 모듈을 단계적으로 전환할 수 있는 하이브리드형 솔루션은 고도로 맞춤화된 레거시 스택으로 인해 어려움을 겪고 있는 기업들에게 매력적인 선택지입니다. 그 결과, 기업들이 규정 준수와 신속한 혁신을 모두 추구하는 가운데, 하이브리드형은 프로젝트 기반 전사적 자원 계획(ERP) 시장에서 여전히 가장 빠르게 성장하고 있는 부문으로 자리 잡고 있습니다.

2025년 기준으로 프로젝트 기반 전사적 자원 계획(ERP) 시장에서 대기업의 점유율은 60.29%를 차지했으나, 중소기업 부문은 2031년까지 연평균 성장률(CAGR) 15.60%를 기록하며 성장하고 있습니다. 구독형 가격 책정을 통해 자본 측면의 장벽이 해소됩니다. 예를 들어, 직원 200명의 건축 사무소의 경우, 첫해에 5만-10만 달러로 코어 모듈을 도입할 수 있으며, 이는 기존 On-Premise 방식 비용의 5분의 1에 해당합니다. 2026년 1월 Net at Work가 BHE Consulting을 인수한 것은 시스템 통합사업자들이 중견 기업 시장에서의 성장에 관심을 보이고 있음을 보여줍니다. 모듈식 라이선싱 체계를 통해 중소기업은 수익이 허용하는 범위 내에서 조달 기능이나 분석 기능을 추가할 수 있으며, 소프트웨어 비용을 계약에 따른 수입과 연동시킬 수 있습니다.

전문 서비스, 건설, IT 컨설팅 업계가 도입을 주도하고 있습니다. 이는 해당 업계의 이익률이 실시간 데이터 수집과 신속한 청구에 달려 있기 때문입니다. 환율 변동과 거시경제의 불안정성은 여전히 남미와 아프리카에서의 도입을 저해하고 있지만, 유연한 결제 조건과 지역별로 호스팅되는 데이터센터를 제공하는 공급업체 덕분에 이러한 장벽은 점차 낮아지고 있습니다. 한때는 세계적 기업에만 국한되었던 기능을 이용할 수 있게 됨에 따라, 중소기업은 프로젝트 기반 전사적 자원 계획(ERP) 시장의 기능 로드맵에 대해 점점 더 큰 영향력을 행사하게 될 것입니다.

지역별 분석

북미는 성숙한 생태계, 높은 IT 예산, 그리고 방위 및 전문 서비스 산업의 집적 덕분에 2025년 프로젝트 기반 전사적 자원 계획(ERP) 시장 매출의 34.26%를 차지했습니다. 미국의 연방 정부 기관은 자본 투자 프로그램을 관리하기 위해 엔터프라이즈 프로젝트 관리 소프트웨어를 도입했으며, 캐나다와 멕시코의 제조업체들은 니어쇼어 공급망을 조정하기 위해 ERP 시스템을 통합했습니다. 인증 컨설턴트로 구성된 풍부한 인력과 AI의 조기 실증은 해당 지역의 리더십 유지에 기여하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있으며, 2031년까지의 연평균 성장률(CAGR)은 13.70%입니다. 중국의 ‘일대일로’ 프로젝트, 인도의 전자 청구서 발행 의무화, 아세안(ASEAN) 국가들의 제조업 확대가 견조한 수요를 뒷받침하고 있습니다. 호주 및 뉴질랜드에서는 광업 분야의 도입률이 높은 반면, 일본에서는 스마트 팩토리 구상을 지원하기 위해 ERP 시스템 업그레이드가 진행되고 있습니다. 인력 부족과 다양한 데이터 저장 장소에 관한 법률이 지역별 클라우드 존의 형성을 촉진하고, 하이브리드 모델의 보급을 가속화하고 있습니다.

유럽에서는 비즈니스 기회와 규제상의 역풍이 균형을 이루고 있습니다. GDPR(EU 개인정보보호규정), 지속가능성 보고서, 의료기기 규제로 인해 규정 준수 요건이 강화됨에 따라, 구매자들은 감사 기능이 내장된 플랫폼으로 눈을 돌리고 있습니다. 독일, 영국, 프랑스, 이탈리아가 자동차, 항공우주, 엔지니어링 분야의 지출을 주도하고 있습니다. 중동에서는 경제 다각화 전략과 연계된 메가 프로젝트에 대한 투자가 진행되고 있으며, 합작 사업 및 이슬람 금융에 대응할 수 있는 ERP가 요구되고 있습니다. 남미의 성장은 통화 변동성으로 인해 브라질과 아르헨티나로 한정되어 있으며, 아프리카에서의 도입은 인프라 부족에도 불구하고 광업 및 통신 분야에서 남아프리카공화국과 나이지리아가 주도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the project-Based enterprise resource planning (ERP) market size is projected to expand from USD 2.58 billion in 2025 and USD 2.80 billion in 2026 to USD 4.65 billion by 2031, registering a CAGR of 10.67% during 2026-2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud/SaaS, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Component (Software, and Services), End-User Industry (Construction and Engineering, Professional Services, Aerospace and Defense, Government and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Project-Based Enterprise Resource Planning Market Trends and Insights

Adoption Of Remote Work And Distributed Project Teams

Remote and hybrid work models became permanent in 2025, forcing companies to retire on-premises systems that rely on VPN access and desktop clients. Cloud-native Project-Based ERP market platforms now ship with mobile interfaces that let field engineers submit timecards and approve change orders from any device, cutting approval cycles by 40% in aerospace and professional-services pilots. Billable utilization climbs when time entries are captured within hours, protecting margins that would otherwise be eroded by manual delays. Buyers increasingly prefer vendors that embed chat, document management, and workflow approvals directly inside the ERP rather than through third-party tools. This consolidation simplifies user training and reduces integration overhead, making remote collaboration a key purchase criterion. As a result, solution providers that optimize experiences for distributed teams are winning competitive bids.

Transition To SaaS And Subscription-Based Pricing Models

The Project-Based ERP market is shifting decisively toward subscription contracts as vendors announce sunset dates for on-premises releases. Epicor's January 2026 roadmap gives customers four years to migrate, a deadline that compresses decision cycles and accelerates cloud adoption. SaaS eliminates server hardware costs, yet it converts capital expenditure into recurring operating expense that can exceed perpetual-license amortization over long horizons. Firms that value continuous feature updates and elastic user scaling find the trade-off attractive, whereas organizations with stable headcounts must carefully evaluate lifetime subscription totals. Migration windows are pushing even risk-averse industries to accelerate data-conversion projects, reinforcing double-digit growth in cloud revenue across the Project-Based ERP market.

High Switching Costs From Legacy ERP Platforms

Migrating historical data, rebuilding custom integrations, and training users can consume 18-24 months and overrun budgets by 30% in complex carve-outs. A mid-sized engineering firm replacing a 15-year-old Deltek instance must map legacy cost codes and maintain audit trails for active contracts during cutover. NetSuite's SuiteSuccess and Unit4's low-code configuration help compress timelines, yet the investment hurdle deters risk-averse CFOs. Until accelerated implementation frameworks prove reliable at scale, high switching costs will temper adoption velocity in parts of the Project-Based ERP market.

Other drivers and restraints analyzed in the detailed report include:

- Integration Of AI-Driven Project Analytics

- Growing Complexity Of Compliance In Project Accounting

- Shortage Of Skilled Project-ERP Implementation Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid configurations are expanding at 17.80% CAGR through 2031 as enterprises pair private-cloud databases with public-cloud collaboration modules. Cloud installations captured 52.12% of the Project-Based ERP market share in 2025, confirming buyer confidence in vendor-managed security and automatic upgrades. A construction conglomerate might hold sensitive financials on private infrastructure but place mobile field-service and analytics workloads in public SaaS to support site engineers. The Project-Based ERP market size for on-premises deployments is shrinking as vendors limit innovation to cloud editions, yet it persists in defense and critical infrastructure accounts that require air-gapped networks.

Organizations choosing deployment models assess total cost across subscription, data egress, and integration charges versus the flexibility to scale. Microsoft's tiered Dynamics 365 options and SAP's RISE program encourage phased migrations that reduce operational risk. Hybrid offerings that allow incremental module shifts appeal to firms burdened by heavily customized legacy stacks. Consequently, hybrid remains the fastest-growing slice of the Project-Based ERP market as businesses seek both compliance and rapid innovation.

Large enterprises held a 60.29% share of the Project-Based ERP market in 2025, yet small and medium enterprises are growing at a 15.60% CAGR through 2031. Subscription pricing removes capital barriers: a 200-person architectural firm can deploy core modules for USD 50,000-100,000 in year one, a fifth of historical on-premises costs. Net at Work's January 2026 purchase of BHE Consulting underscores integrator interest in mid-market growth. Modular licensing lets SMEs add procurement or analytics when revenue allows, aligning software expense with contract inflows.

Professional services, construction, and IT consultancies lead adoption because margins depend on real-time capture and prompt billing. Currency fluctuations and macroeconomic volatility still curb adoption in South America and Africa, but vendors that offer flexible payment terms and regionally hosted data centers are reducing barriers. As capabilities once reserved for global enterprises become accessible, SMEs will exert growing influence on functional roadmaps within the Project-Based ERP market.

Geography Analysis

North America accounted for 34.26% of the Project-Based ERP market revenue in 2025, owing to mature ecosystems, high IT budgets, and a concentration of defense and professional services. U.S. federal agencies adopted enterprise project management software to track capital programs, while Canadian and Mexican manufacturers integrated ERP systems to coordinate nearshore supply chains. A deep bench of certified consultants and early AI experimentation helps the region maintain leadership.

Asia-Pacific is growing fastest, with a 13.70% CAGR through 2031. China's Belt and Road projects, India's electronic invoicing mandates, and ASEAN manufacturing expansion are fueling robust demand. Australia and New Zealand have high deployment rates in mining, and Japan is upgrading its ERP systems to support smart-factory initiatives. Talent shortages and diverse data-residency laws are driving regional cloud zones and accelerating hybrid models.

Europe balances opportunity with regulatory headwinds. GDPR, sustainability reporting, and the Medical Device Regulation elevate compliance requirements, steering buyers toward platforms with built-in audit capabilities. Germany, the United Kingdom, France, and Italy dominate spend across automotive, aerospace, and engineering. The Middle East invests in megaprojects tied to diversification agendas, seeking ERP that supports joint ventures and Islamic finance. South American growth is localized to Brazil and Argentina due to currency volatility, and Africa's uptake is led by South Africa and Nigeria in mining and telecom despite infrastructure gaps.

- Deltek, Inc.

- IFS AB

- Unit4 N.V.

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- Workday, Inc.

- Acumatica, Inc.

- Ramco Systems Limited

- SYSPRO (Proprietary) Limited

- Priority Software Ltd.

- QAD Inc.

- Sage Group plc

- Totvs S.A.

- NetSuite Inc.

- FinancialForce.com, Inc.

- Aptean, Inc.

- Plex Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Remote Work and Distributed Project Teams

- 4.2.2 Transition to SaaS and Subscription-Based Pricing Models

- 4.2.3 Integration of AI-Driven Project Analytics

- 4.2.4 Growing Complexity of Compliance in Project Accounting

- 4.2.5 Demand for Unified Bid-to-Cash Visibility Across Projects

- 4.2.6 Rising Investment in Public Infrastructure Megaprojects

- 4.3 Market Restraints

- 4.3.1 High Switching Costs from Legacy ERP Platforms

- 4.3.2 Shortage of Skilled Project-ERP Implementation Specialists

- 4.3.3 Data Security Concerns in Multi-Tenant Cloud Environments

- 4.3.4 Budget Constraints in SMEs Amid Macroeconomic Uncertainty

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud/SaaS

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Component

- 5.3.1 Software

- 5.3.2 Services

- 5.4 By End-User Industry

- 5.4.1 Construction and Engineering

- 5.4.2 Professional Services

- 5.4.3 Aerospace and Defense

- 5.4.4 Government and Utilities

- 5.4.5 Healthcare

- 5.4.6 IT and Telecom

- 5.4.7 Manufacturing

- 5.4.8 Oil and Gas

- 5.4.9 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Deltek, Inc.

- 6.4.2 IFS AB

- 6.4.3 Unit4 N.V.

- 6.4.4 Oracle Corporation

- 6.4.5 SAP SE

- 6.4.6 Microsoft Corporation

- 6.4.7 Infor, Inc.

- 6.4.8 Epicor Software Corporation

- 6.4.9 Workday, Inc.

- 6.4.10 Acumatica, Inc.

- 6.4.11 Ramco Systems Limited

- 6.4.12 SYSPRO (Proprietary) Limited

- 6.4.13 Priority Software Ltd.

- 6.4.14 QAD Inc.

- 6.4.15 Sage Group plc

- 6.4.16 Totvs S.A.

- 6.4.17 NetSuite Inc.

- 6.4.18 FinancialForce.com, Inc.

- 6.4.19 Aptean, Inc.

- 6.4.20 Plex Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment