|

시장보고서

상품코드

2065556

석유 및 가스 전사적 자원 계획(ERP) : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Oil And Gas Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

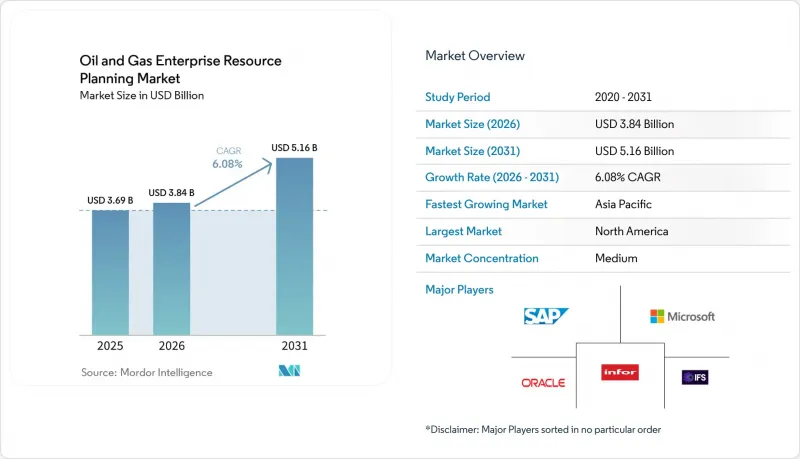

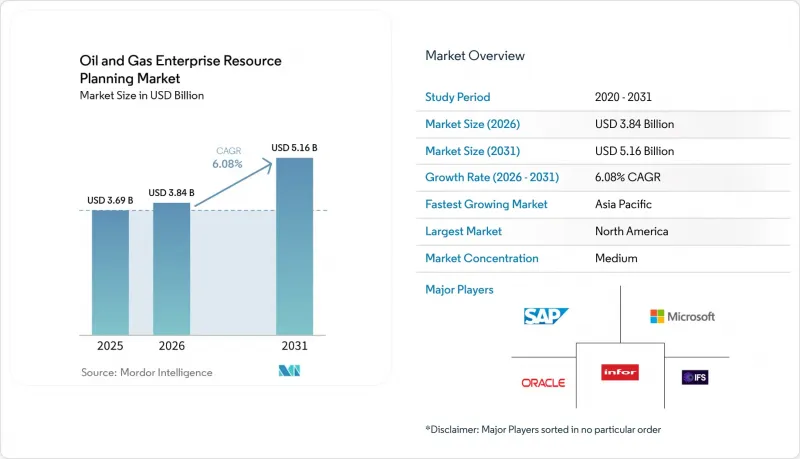

Mordor Intelligence에 의하면, 석유 및 가스 전사적 자원 계획(ERP) 시장 규모는 2025년에 36억 9,000만 달러로 평가되었습니다. 2026년에 38억 4,000만 달러에 달하고, 2031년까지 51억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 6.08%로 성장할 전망입니다.

본 보고서는 구성 요소별(재무 관리 모듈, 자산 관리 모듈, 공급망 관리 모듈, 기타 구성 요소), 배포 방식별(클라우드, On-Premise, 하이브리드), 기업 규모별(중소기업, 대기업), 용도별(업스트림 공정, 미드스트림 공정, 다운스트림 공정, 유전 서비스), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 석유 및 가스 전사적 자원 계획(ERP) 시장 동향 및 인사이트

클라우드 기반 ERP 솔루션 도입 확대

각 하이퍼스케일러 기업들이 지역별 데이터센터와 업계 인증 보안 프레임워크를 구축함에 따라, 2025년에는 클라우드가 석유 및 가스 전사적 자원 계획(ERP) 시장의 62.10%를 차지했습니다. S-OIL은 14개의 레거시 모듈을 단일 클라우드 인스턴스로 통합하여, 월말 결산 기간을 12일에서 5일로 단축했습니다. 한편, 샤르자 국립 석유 공사는 재무 및 조달 업무의 워크로드를 퍼블릭 클라우드로 이전하는 한편, 생산 데이터는 On-Premise에서 유지했습니다. 연평균 성장률(CAGR) 13.10%를 기록한 이러한 하이브리드형 성장세는 사업자들이 실시간 SCADA 스트림을 On-Premise에서 유지하면서 기업 기능을 탄력적인 인프라로 이전하는 것을 선호하는 경향을 보여줍니다. 이러한 추세는 사용량에 따른 과금 모델을 뒷받침하고 있으며, 이를 통해 중소기업은 초기 투자 비용을 최대 60%까지 절감할 수 있습니다. 사우디아라비아와 아랍에미리트에서 데이터 거점 확보가 이전을 더욱 가속화하고 있습니다.

AI를 활용한 예측 유지보수의 부상

예기치 못한 가동 중단이 한 번 발생할 때마다 업스트림 사업자는 약 3,800만 달러의 손실을 입기 때문에 예측 유지보수는 단기적으로 가장 높은 ROI를 가져다줍니다. ERP의 자산 관리 모듈에 통합된 분석 솔루션은 진동 및 압력 데이터를 처리하여 30-45일 후의 고장을 예측함으로써, 계획된 턴어라운드 기간 중에 수리를 수행할 수 있도록 합니다. 아부다비의 초기 도입 기업에 따르면, 조달을 실시간 생산 일정과 연동한 결과 재고 보유 비용이 15% 절감되었다고 합니다. 엣지 컴퓨팅을 통해 알고리즘이 광산 입구까지 확장되어, 네트워크 업그레이드 없이도 밀리초 단위의 낮은 지연 시간을 실현하고 있습니다. 현재 각 벤더사는 유지보수 로그를 분석하여 작업 지시서를 자동으로 작성하고 기술자를 파견하는 생성형 도구를 함께 제공하고 있으며, 이를 통해 평균 수리 시간(MTTR)을 5분의 1 이상 단축하고 있습니다.

높은 도입 비용과 전환 비용

총 소유 비용(TCO)은 12명의 사용자를 대상으로 한 클라우드 도입의 경우 5만 달러부터, 업스트림·중류·하류 부문에 걸친 다국적 기업의 시스템 교체 시에는 5,000만 달러 이상에 달할 전망입니다. 수십 년에 걸친 시추공 로그 및 파트너사의 기록 데이터를 이전하는 데는 18-24개월이 소요되며, 이로 인해 예산이 두 자릿수 비율로 증가할 가능성이 있습니다. 또한, 직원들이 새로운 업무 흐름에 적응하는 과정에서 사업자는 변경 관리 비용도 부담하게 됩니다. 구독형 라이선스를 통해 지출은 자본 지출에서 운영 예산으로 전환되지만, 중규모 생산 업체의 경우에도 다년간의 계약 시 연간 50만 달러를 초과하는 경우가 있습니다. 이러한 경제적 요인으로 인해 상품 가격이 하락할 경우, 업그레이드 속도가 둔화됩니다.

부문별 분석

자산 관리는 2025년 수익의 29.40%를 차지했습니다. 이는 해상 시설의 가동 중단으로 인해 생산이 수 주간 중단되어, 불가항력으로 인한 위약금이 발생할 가능성이 있기 때문입니다. 운영자가 더 많은 센서를 설치하고 실시간 데이터를 AI 엔진에 입력함에 따라, 이 모듈과 관련된 석유 및 가스 전사적 자원 계획(ERP) 시장 규모는 꾸준히 확대될 전망입니다. 작업 지시서의 자동화와 재무 분개를 결합한 벤더는 통합 보고서의 구현을 목표로 하는 생산자들 사이에서 더욱 빠르게 도입되고 있습니다. 반면, 프로젝트 관리 모듈은 합작 투자 형태의 시추 프로젝트에서 세밀한 비용 추적이 요구됨에 따라 연평균 성장률(CAGR) 11.80%를 기록하며 성장하고 있습니다.

프로젝트 관리는 특히 심해 분지에서 진행되는 복잡한 자본 프로젝트나 파트너에 대한 배분과 관련해 주목을 받고 있습니다. 공급망 관리는 파이프, 시추 유체 및 주요 예비 부품에 있어 여전히 중요하지만, 많은 기업이 이미 조달 주기를 최적화함에 따라 그 성장세는 둔화되고 있습니다. 재무 관리는 여전히 핵심 분야이지만, 예산은 ESG 및 예측 분석과 같은 부가 기능으로 전환되고 있습니다. 인적 자본 관리는 안전 인증 갱신 요건이 까다로운 시장에서 그 중요성이 더욱 커지고 있습니다.

2025년, 석유 및 가스 전사적 자원 계획(ERP) 시장에서 클라우드 도입 비중은 62.10%를 차지했으나, 하이브리드 모델이 연평균 성장률(CAGR) 13.10%로 가장 빠른 성장세를 기록했습니다. 만안 지역 국가들의 운영업체들은 주권법에 따라, 급증하는 트래픽을 처리할 수 있는 용량을 확보하기 위해 생산 데이터용 On-Premise 클러스터와 기업 업무용 퍼블릭 클라우드를 결합하여 사용하고 있습니다. 하이브리드 도입의 배경에는 지연 시간 관련 요구 사항도 있습니다. 자동화된 유정 제어 시퀀싱에서는 왕복 시간이 50밀리초 미만이어야 하기 때문입니다. On-Premise형 솔루션의 석유 및 가스 전사적 자원 계획(ERP) 시장 규모는 계속 축소되고 있으며, 주로 제재 대상 지역이나 통신 환경이 제한된 지역에서 여전히 자리를 지키고 있습니다.

하이브리드 환경에서는 우물 식별자나 공급업체 기록의 불일치가 통합 보고서의 정확성을 저해할 가능성이 있으므로, 엄격한 마스터 데이터 거버넌스가 요구됩니다. 기업들은 기록을 동기화하기 위해 미들웨어나 API 게이트웨이에 20만-50만 달러를 투자하는 경우가 많습니다. 복잡성은 높아지지만, 이 모델은 장애 발생 시나 유지보수 기간 중에 워크로드를 로컬 노드와 클라우드 노드 간에 전환할 수 있으므로 높은 복원력을 제공합니다.

지역별 분석

북미는 2025년에도 44.90%의 점유율을 유지했으며, 그 기반이 되는 것은 퍼미안 분지의 셰일 생산과 멕시코만 심해 개발에 대한 투자입니다. SEC의 기후 변화 정보 공시 규정에 따라 탄소 배출량 통합 보고에 대한 수요가 증가하고 있으며, 기업들은 감사 기한을 맞추기 위해 ERP와 배출량 센서를 통합하고 있습니다. 캐나다의 오일샌드 기업은 채굴 현장과 정제 공장에서 수집된 데이터를 통합하기 위해 맞춤형 모듈을 추가한 반면, 멕시코의 서비스 기업은 레거시 시스템을 현대화함으로써 가동 시간이 향상되었다고 밝혔습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지의 연평균 성장률(CAGR)은 11.30%입니다. 중국의 국영 석유 회사는 액화천연가스(LNG) 터미널과 장기 판매 계약을 연계하기 위해 ERP 시스템 업그레이드를 추진하고 있습니다. 인도의 업스트림 부문 사업자들은 크리슈나·고다바리 심해 블록의 합작 사업 장부를 디지털화하여, 탄화수소 총국(Directorate General of Hydrocarbons)의 전자 제출 의무를 준수하고 있습니다. 호주의 액화천연가스(LNG) 수출업체들은 ERP를 활용하여 수십억 달러 규모의 엔지니어링 마일스톤을 모니터링하고 있습니다.

중동에서는 국내 주요 기업들이 사업 다각화를 추진하고 현지 클라우드 업체와의 제휴를 확대해 나가는 가운데, ERP 도입이 급속도로 진행되고 있습니다. 사우디아라비아의 데이터 주권 관련 법률에 따라 공급업체들은 국내에서 호스팅을 제공해야만 하지만, 한편 아부다비 국영 석유공사(ADNOC)는 자사의 SAP 환경 내에 수백 개의 AI 도구를 도입하고 있습니다. 유럽에서는 수십년전부터 사용되어 온 SCADA 시스템이 여전히 가동 중인 북해의 브라운필드 자산의 현대화에 주력하고 있습니다. 아프리카의 신흥 산유국들은 막대한 설비 투자를 피하기 위해 클라우드를 선호하고 있지만, 해상 대역폭이 제한적이어서 실시간 복제에 지연이 발생하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the oil and gas ERP market size is projected to be USD 3.69 billion in 2025, USD 3.84 billion in 2026, and reach USD 5.16 billion by 2031, growing at a CAGR of 6.08% from 2026 to 2031.

This report is Segmented by Component (Financial Management Module, Asset Management Module, Supply Chain Management Module, and Other Components), Deployment Mode (Cloud, On-Premise, and Hybrid), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Application (Upstream, Midstream, Downstream, and Oilfield Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Oil And Gas Enterprise Resource Planning Market Trends and Insights

Growing Adoption Of Cloud-Based ERP Solutions

Cloud captured 62.10% of the oil and gas ERP market in 2025 after hyperscalers launched region-specific data centers and industry-certified security frameworks. S-OIL consolidated 14 legacy modules into a single cloud instance and cut month-end close from 12 days to 5, while Sharjah National Oil Corporation moved finance and procurement workloads to public cloud but retained production data on-premise. Hybrid growth at a 13.10% CAGR shows that operators prefer to keep real-time SCADA streams local and shift corporate functions to elastic infrastructure. This pattern supports consumption-based pricing, which trims upfront capital outlay by up to 60% for smaller firms. Data residency guarantees in Saudi Arabia and the United Arab Emirates further accelerate migrations.

Rise Of AI-Driven Predictive Maintenance

Each unplanned shutdown costs an upstream operator nearly USD 38 million, so predictive maintenance drives the highest near-term ROI. Analytics suites embedded in ERP asset modules process vibration and pressure data to predict failures 30-45 days ahead, enabling repairs during planned turnarounds. Early adopters in Abu Dhabi report a 15% drop in inventory carrying costs after synchronizing procurement with real-time production schedules. Edge computing pushes algorithms to the wellhead, delivering millisecond latency without network upgrades. Vendors now bundle generative tools that read maintenance logs, auto-create work orders, and dispatch technicians, shrinking mean time to repair by more than one-fifth.

High Implementation And Switching Costs

Total cost of ownership ranges from USD 50,000 for a twelve-user cloud roll-out to more than USD 50 million for a multinational swap-out across upstream, midstream, and downstream units. Data migration of decades of well logs and partner records can stretch 18-24 months and lift budgets by double-digit percentages. Operators also absorb change-management expenses as employees adapt to new workflows. Subscription licenses shift spend from capital to operating budgets, yet multi-year commitments can still top USD 500,000 annually for midsize producers. Such economics dampen upgrade velocity when commodity prices soften.

Other drivers and restraints analyzed in the detailed report include:

- Integration Of Asset And Financial Management

- Increasing Regulatory And Compliance Demands

- Data Security And Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Asset Management retained 29.40% of 2025 revenue because offshore outages can halt production for weeks and trigger force majeure penalties. The oil and gas ERP market size tied to this module is set to expand steadily as operators install more sensors and feed real-time data into AI engines. Vendors that pair work-order automation with financial posting see faster adoption among producers striving for integrated reporting. In contrast, the Project Management Module grows at 11.80% CAGR as joint-venture drilling campaigns demand granular cost tracking.

Project Management gains traction in complex capital projects and partner allocations, particularly in deepwater basins. Supply Chain Management continues to matter for tubulars, drilling fluids, and critical spares, yet its growth lags because many firms have already optimized procurement cycles. Financial Management remains foundational, though budgets shift toward ESG and predictive analytics add-ons. Human Capital Management becomes more relevant in markets with strict safety certification renewal requirements.

Cloud deployment held 62.10% of the oil and gas ERP market share in 2025, yet hybrid models posted the fastest growth at a 13.10% CAGR. Operators in Gulf states mix on-premises clusters for production data with public cloud for corporate functions to comply with sovereignty laws and enable burst capacity. Hybrid adoption also stems from latency needs, as automated well-control sequences tolerate less than 50 milliseconds round-trip time. The oil and gas ERP market size for on-premises solutions continues to shrink, surviving mainly in sanctioned regions or areas with limited connectivity.

Hybrid environments require strict master data governance because inconsistent well identifiers or vendor records can corrupt consolidated statements. Firms often invest USD 200,000-500,000 in middleware and API gateways to synchronize records. Despite the added complexity, the model offers resilience because workloads can swing between local and cloud nodes during outages or maintenance windows.

Geography Analysis

North America retained 44.90% share in 2025, anchored by Permian shale output and Gulf of Mexico deepwater spends. SEC climate-disclosure rules drive demand for embedded carbon reporting, and operators integrate ERP with emissions sensors to meet audit timelines. Canadian oil sands firms add custom modules to blend data from mining dispatch and upgrader units, while Mexican service companies cite uptime gains after modernizing legacy systems.

Asia-Pacific is the fastest-growing region, with a 11.30% CAGR through 2031. National oil companies in China are upgrading ERPs to link liquefied natural gas terminals to long-term sales contracts. Indian upstream operators digitize joint venture ledgers for Krishna-Godavari deepwater blocks, complying with the Directorate General of Hydrocarbons' e-submission mandates. Australian liquefied natural gas exporters leverage ERP to monitor billion-dollar engineering milestones.

The Middle East sees rapid adoption as national champions pursue diversification agendas and local-cloud partnerships. Saudi data-sovereignty laws steer vendors toward in-kingdom hosting, while Abu Dhabi National Oil Company rolls out hundreds of AI tools inside its SAP landscape. Europe focuses on modernizing Brownfield North Sea assets where decades-old SCADA systems still run. Emerging African producers prefer cloud to avoid high capital outlays, though limited offshore bandwidth slows real-time replication.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- IFS AB

- Epicor Software Corporation

- Deltek, Inc.

- Enertia Software, Inc.

- Quorum Business Solutions, LLC

- P2 Energy Solutions, Inc.

- Unit4 N.V.

- Acumatica, Inc.

- Odoo S.A.

- Sage Group plc

- Ramco Systems Limited

- QAD Inc.

- Workday, Inc.

- ABB Ltd

- Honeywell International Inc.

- Siemens AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of Asset and Financial Management to Improve Operational Efficiency

- 4.2.2 Growing Adoption of Cloud-Based ERP Solutions

- 4.2.3 Increasing Regulatory and Compliance Requirements in Oil and Gas Industry

- 4.2.4 Rise of AI-Driven Predictive Maintenance Modules Reducing Unplanned Downtime

- 4.2.5 Emergence of Joint Venture Accounting Automation for Complex Partnership Models

- 4.2.6 Demand for Integrated ESG and Carbon Reporting Capabilities within ERP Suites

- 4.3 Market Restraints

- 4.3.1 High Implementation and Switching Costs

- 4.3.2 Data Security and Sovereignty Concerns for Cloud Deployments

- 4.3.3 Shortage of Domain-Specific ERP Talent for Oil and Gas Digital Transformations

- 4.3.4 Legacy Production Systems Integration Complexity in Brownfield Assets

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.1.1 Bargaining Power of Suppliers

- 4.8.1.2 Bargaining Power of Buyers

- 4.8.1.3 Threat of Substitutes

- 4.8.1.4 Intensity of Competitive Rivalry

- 4.8.1 Threat of New Entrants

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Financial Management Module

- 5.1.2 Asset Management Module

- 5.1.3 Supply Chain Management Module

- 5.1.4 Project Management Module

- 5.1.5 Human Capital Management Module

- 5.1.6 Other Components

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Application

- 5.4.1 Upstream

- 5.4.2 Midstream

- 5.4.3 Downstream

- 5.4.4 Oilfield Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 Nigeria

- 5.5.6.2 South Africa

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 IFS AB

- 6.4.6 Epicor Software Corporation

- 6.4.7 Deltek, Inc.

- 6.4.8 Enertia Software, Inc.

- 6.4.9 Quorum Business Solutions, LLC

- 6.4.10 P2 Energy Solutions, Inc.

- 6.4.11 Unit4 N.V.

- 6.4.12 Acumatica, Inc.

- 6.4.13 Odoo S.A.

- 6.4.14 Sage Group plc

- 6.4.15 Ramco Systems Limited

- 6.4.16 QAD Inc.

- 6.4.17 Workday, Inc.

- 6.4.18 ABB Ltd

- 6.4.19 Honeywell International Inc.

- 6.4.20 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment