|

시장보고서

상품코드

2065585

유럽의 게이밍 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Gaming GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

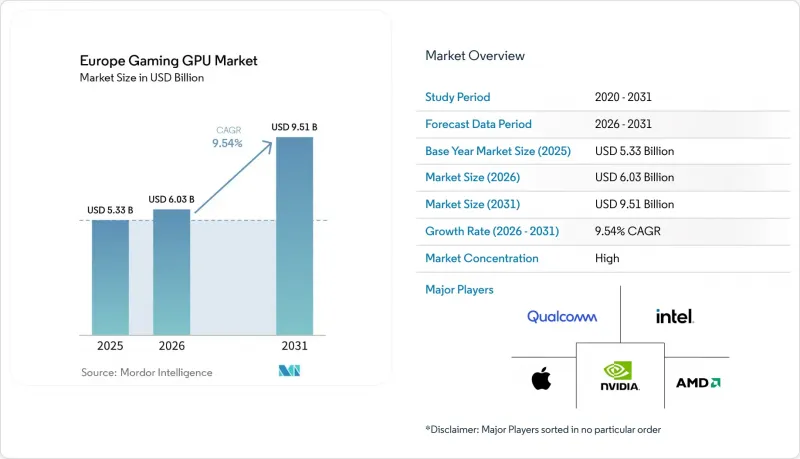

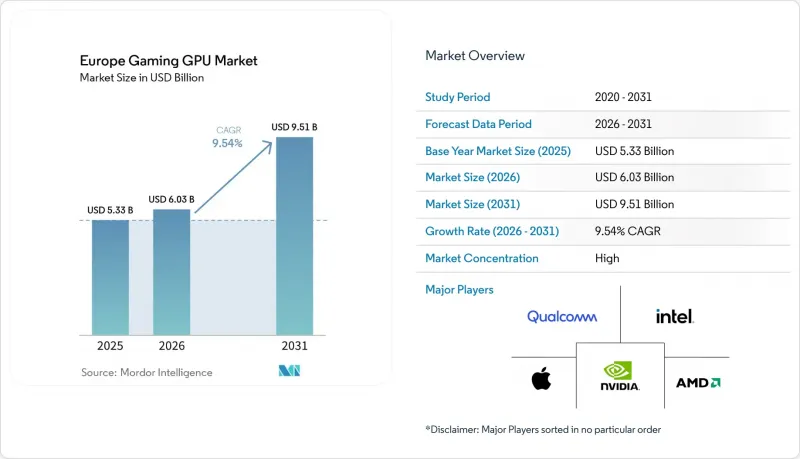

Mordor Intelligence에 의하면, 유럽의 게이밍 GPU 시장 규모는 2025년에 53억 3,000만 달러로 평가되었고, 2026년에 60억 3,000만 달러로 추정되고, 2031년까지 95억 1,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 9.54%로 성장할 전망입니다.

본 보고서는 GPU 유형별(디스크리트 GPU 및 통합형 GPU), 기기 유형별(게이밍 데스크톱, 게이밍 노트북, 스마트폰 및 태블릿(모바일 게이밍)), 최종 사용자 유형별(캐주얼 게이머, 애호가 및 프로 게이머), 메모리 유형별(GDDR6, GDDR6X, 레거시 그래픽 메모리, 통합 메모리), 그리고 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 게이밍 GPU 시장 동향 및 인사이트

e스포츠 및 경쟁형 PC 게임 참가자 증가

유럽의 e스포츠용 게이밍 수요는 매우 방대한 게이머층에 의해 지탱되고 있으며, 이 층은 시간이 지남에 따라 더 높은 성능을 중시하는 하드웨어 구매를 지속적으로 촉진하고 있습니다. Video Games Europe 및 유럽 게임 개발자 연맹(European Games Developer Federation)에 따르면, 2024년에는 6세에서 64세 사이의 유럽인 중 54%가 비디오 게임을 즐겼으며, 이로 인해 지역 전체에서 해당 하드웨어의 사용자 기반이 광범위하게 유지되었습니다. 이처럼 폭넓은 참여층 덕분에, 캐주얼한 플레이에서부터 주사율, 응답 속도, 영상 안정성이 더욱 중요해지는 체계적이고 성능을 중시하는 게이밍으로의 꾸준한 흐름이 형성되고 있습니다. 독일의 게임용 하드웨어 및 액세서리 시장은 2025년에 12% 성장하여 34억 유로(37억 1,000만 달러)에 달했습니다. 이는 비용이 높은 환경 속에서도 기업들이 여전히 게이밍 기기에 대한 지출을 아끼지 않았음을 보여줍니다. 게이밍 PC용 액세서리 매출은 13% 증가한 13억 7,000만 유로(14억 9,000만 달러)를 기록하며, 이 지역에서 가장 중요한 하드웨어 시장 중 하나인 이곳에서 부품에 대한 수요가 견조함을 보여주고 있습니다. 이로 인해 유럽의 게이밍 GPU 시장은 단일 구매 주기가 아닌, 성능을 중시하는 지속적인 업그레이드에 힘입어 계속 성장하고 있습니다.

실시간 레이 트레이싱 및 AI 업스케일링에 대한 수요

AI 업스케일링은 더 이상 선택적인 프리미엄 기능이 아니라, 유럽의 게이밍 GPU 시장에서 표준적인 구매 요인이 되었습니다. NVIDIA에 따르면, GeForce RTX 5000 세대에서 도입된 DLSS 4는 2026년 5월 기준으로 980개 이상의 게임 및 용도에서 지원되고 있다고 합니다. AMD 역시 2025년 2월, FSR 4를 탑재한 Radeon RX 9000 시리즈와 RDNA 4 아키텍처를 출시하면서 AI 지원 렌더링을 핵심 기능으로 내세웠습니다. NVIDIA는 또한 GeForce RTX 50 시리즈 하드웨어의 ‘Multi Frame Generation’ 기능을 통해 지원되는 워크로드에서 실제 프레임 출력을 최대 8배까지 향상시킬 수 있다고 밝혔습니다. 이러한 기술 덕분에, 점점 더 많은 소비자들이 기본적인 1080p 성능에 그치지 않고, 장기간에 걸쳐 높은 그래픽 설정을 유지할 수 있는 그래픽 카드를 찾고 있습니다. 이러한 변화로 인해 유럽의 게이밍 GPU 시장에서 공급업체가 충족해야 하는 기본 사양이 상향 조정되었습니다.

게이밍용 GPU 및 시스템의 높은 초기 비용

현재의 업그레이드 주기에 있어, 유럽의 게이밍 GPU 시장에서 많은 구매자들에게 초기 비용 부담은 여전히 큽니다. AMD는 2025년에 Radeon RX 9070을 549달러, RX 9070 XT를 599달러에 출시할 예정이며, 한편 인텔은 2024년 하반기에 Arc B580을 249달러에 출시했습니다. 세금이나 파트너사의 프리미엄, 시스템 전체 비용이 추가되기 전부터, 이러한 가격 수준 때문에 현행 세대의 하드웨어는 일반 가정에서 충동 구매할 만한 대상이 되기에는 한참 거리가 있습니다. 이러한 압박으로 인해, 장기적인 성능의 가치가 분명하더라도 VRAM 용량이나 레이 트레이싱 성능이 뛰어난 고사양 제품을 구매하는 적극적인 사용자층은 줄어들고 있습니다. 또한 일부 사용자들은 직접 새 제품을 구입하는 대신, 기존 시스템을 오랫동안 계속 사용하거나 스트리밍 게임 서비스를 이용하는 쪽으로 방향을 틀고 있습니다. 그 결과, 애호가층이 일반 사용자보다 더 빨리 구매를 이어가고 있기 때문에 시장 내 지출액은 판매 대수의 교체 속도보다 더 견조한 상태를 유지하고 있습니다.

부문별 분석

2025년, 유럽의 게이밍 GPU 시장에서 디스크리트 GPU는 74.44%의 점유율을 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 9.90%로 성장할 것으로 전망됩니다. 게임 성능은 여전히 지속적인 연산 능력, 더 강력한 열 여유, 그리고 고도의 시각적 워크로드에 대한 직접적인 지원에 의존하고 있기 때문에 전용 그래픽 하드웨어가 계속해서 핵심적인 역할을 수행하고 있습니다. 980개 이상의 게임 및 애플리케이션에서 NVIDIA의 DLSS 4가 채택되고 있다는 사실은 다양한 기능을 갖춘 전용 그래픽 카드가 여전히 최고의 성능을 자랑하는 이유를 보여줍니다. AMD는 2025년, RDNA 4 아키텍처, 16GB GDDR6 구성, 그리고 현세대 게임용 FSR 4를 지원하는 Radeon RX 9000 시리즈를 출시하며 그 입지를 더욱 공고히 했습니다. 실용적인 관점에서 볼 때, 유럽의 게이밍 GPU 시장에서 가장 큰 점유율은 시스템 전체에서 공유하여 사용하는 것이 아니라, 게임 플레이 전용으로 설계된 그래픽 카드가 계속해서 차지하고 있습니다.

나머지 시장 점유율은 통합형 GPU가 차지하고 있으며, 캐주얼 게임 플레이, 초슬림 기기, 그리고 클라우드 게임 접속 지점에서 여전히 중요한 역할을 하고 있습니다. 인텔의 Arc B 시리즈 출시는 가장 강력한 게이밍 수요가 여전히 별도 GPU 부문에 집중되어 있음에도 불구하고, 이 회사가 가성비를 중시하는 그래픽 분야에서도 계속해서 입지를 다지고자 한다는 점을 보여줍니다. 또한, NVIDIA와 도이치 텔레콤이 제공하는 클라우드 서비스 역시 부하가 적은 게이밍 환경에서 고성능 로컬 GPU의 필요성을 줄여주고 있으며, 이로 인해 저가형 시장에서 통합형 및 하이브리드 구성의 유효성이 유지되고 있습니다. 그럼에도 불구하고, 유럽의 게이밍 GPU 업계에서는 프리미엄급 게이밍 기능이 가장 빠르게 발전하고 있는 디스크리트 GPU가 여전히 수익과 제품 개발 측면에서 가장 큰 관심을 받고 있습니다.

2025년, 게이밍 데스크톱은 유럽 게이밍 GPU 시장 규모의 44.31%를 차지했으며, 타워형이 여전히 가장 큰 기기 카테고리로 자리매김했습니다. 이러한 장점은 업그레이드 유연성이 높고, 냉각 성능이 뛰어나며, 시스템 전체를 교체하지 않고 그래픽 카드만 교체할 수 있다는 점에 기인합니다. 애호가 중심 시장에서 데스크톱은 하드웨어를 전면적으로 교체하는 대신, 단계적으로 GPU를 업그레이드하기 위한 가장 확실한 수단으로 자리 잡고 있습니다. 2025년 독일의 게이밍 하드웨어 및 액세서리 시장 성장세는 이러한 추세를 뒷받침하고 있습니다. 이 지역에서 가장 중요한 게이밍 하드웨어 시장 중 하나인 독일에서는 부품에 대한 지출이 계속해서 활발했기 때문입니다. 이로 인해 다른 기기 유형이 확대되고 있음에도 불구하고, 유럽의 게이밍 GPU 시장은 데스크톱 부품 수요와 밀접하게 연계된 상태를 유지하고 있습니다.

게이밍 노트북 시장은 2031년까지 연평균 성장률(CAGR) 10.12%를 기록하며 성장할 것으로 예상되며, 유럽 게이밍 GPU 시장에서 가장 빠르게 성장하는 기기 유형이 될 전망입니다. ASUS는 2026년, 북유럽 시장을 겨냥해 최대 RTX 5080 노트북 GPU 및 RTX 5090 노트북 GPU를 탑재한 ‘Zephyrus G14’와 ‘G16’ 시스템을 발표하며 이러한 변화를 두드러지게 보여주었습니다. 또한, NVIDIA의 GeForce NOW가 Blackwell로 업그레이드됨에 따라, 로컬 GPU의 여유 성능이 제한적인 기기에서도 고해상도 스트리밍이 가능해져 휴대용 시스템의 매력이 한층 더 높아졌습니다. 또한, 5G 클라우드 게임 서비스를 통해 모바일 사용자는 기기의 폼 팩터를 변경하지 않고도 프리미엄급 GPU 렌더링을 경험할 수 있게 되었기 때문에 스마트폰 및 태블릿이 세 번째 경로로 추가되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the europe gaming GPU market size is projected to be USD 5.33 billion in 2025, USD 6.03 billion in 2026, and reach USD 9.51 billion by 2031, growing at a CAGR of 9.54% from 2026 to 2031.

This report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets (Mobile Gaming)), End-User Type (Casual Gamers, and Enthusiast and Professional Gamers), Memory Type (GDDR6, GDDR6X, Legacy Graphics Memory, and Unified Memory), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe Gaming GPU Market Trends and Insights

Rising Esports And Competitive PC Gaming Participation

Competitive gaming demand in Europe rests on a very large player base that continues to feed more performance-focused hardware purchases over time. Video Games Europe and the European Games Developer Federation stated that 54% of Europeans aged 6-64 played video games in 2024, which kept the addressable hardware base broad across the region. That broad participation supports a steady funnel from casual play into organized and performance-led gaming, where refresh rate, responsiveness, and visual stability matter more. Germany's games hardware and accessories segment grew 12% in 2025 to EUR 3.40 billion (USD 3.71 billion), showing that players were still willing to spend on gaming equipment even in a higher-cost environment. Gaming PC accessories rose 13% to EUR 1.37 billion (USD 1.49 billion), which points to healthy component demand in one of the region's most important hardware markets. This keeps the Europe gaming GPU market tied to repeated performance-led upgrades rather than to a single purchase cycle.

Demand for Real-Time Ray Tracing and AI-Upscaling

AI-upscaling is now a standard purchase factor in the Europe gaming GPU market rather than an optional premium feature. NVIDIA said DLSS 4, introduced with the GeForce RTX 5000 generation, had reached more than 980 games and applications by May 2026. AMD also positioned AI-assisted rendering as a core feature when it launched the Radeon RX 9000 series and RDNA 4 architecture with FSR 4 in February 2025.NVIDIA further stated that Multi Frame Generation on GeForce RTX 50 Series hardware can increase effective frame output by up to 8x in supported workloads. These technologies are pushing more buyers to look beyond basic 1080p performance and target cards that can sustain higher visual settings over a longer ownership period. That change is lifting the baseline specification that vendors must meet across the Europe gaming GPU market.

High Upfront Cost of Gaming GPUs and Systems

The current upgrade cycle still carries a high upfront cost burden for many buyers in the Europe gaming GPU market. AMD launched the Radeon RX 9070 at USD 549 and the RX 9070 XT at USD 599 in 2025, while Intel positioned the Arc B580 at USD 249 in late 2024. Even before taxes, partner premiums, and the cost of a full system are added, those levels keep current-generation hardware far from impulse-purchase territory for mainstream households. That pressure narrows the active buyer base for higher-VRAM and higher-ray-tracing tiers, even when long-term performance value is clear. It also pushes some users toward longer retention of existing systems or toward streamed gaming services instead of direct replacement. The result is a market where spending remains healthier than unit turnover because enthusiasts continue to buy sooner than mass-market users.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Gaming Laptops and Portable High-Performance PCs

- Mobile Gaming Monetization Moving Toward Higher-Fidelity Titles

- Mature Installed Base Lengthening Replacement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs commanded a 74.44% share of the Europe gaming GPU market in 2025 and are projected to expand at a 9.90% CAGR through 2031. Dedicated graphics hardware remains central because gaming performance still depends on sustained compute, stronger thermal headroom, and direct support for advanced visual workloads. NVIDIA's DLSS 4 footprint across more than 980 games and applications shows why feature-rich discrete cards continue to hold the strongest performance position. AMD reinforced that position in 2025 when it launched the Radeon RX 9000 series with RDNA 4, 16 GB GDDR6 configurations, and FSR 4 support for current-generation gaming. In practical terms, the largest slice of the Europe gaming GPU market continues to sit with cards designed for direct gaming load rather than for shared system use.

Integrated GPUs account for the remaining segment share and remain more relevant for casual play, thin devices, and cloud gaming access points. Intel's Arc B-series launch showed that the company still wants a role in value-oriented graphics, even though the strongest gaming demand remains concentrated in discrete categories. Cloud services from NVIDIA and Deutsche Telekom also reduce the need for a powerful local GPU in lighter gaming scenarios, which helps integrated and hybrid setups stay viable at the lower end. Even so, the Europe gaming GPU industry still draws most of its revenue and product attention from discrete silicon because premium gaming features are advancing fastest there.

Gaming desktops held 44.31% share of the Europe gaming GPU market size in 2025, which kept towers as the largest device category. Their lead reflects stronger upgrade flexibility, better cooling, and the ability to replace a graphics card without changing the full system. In enthusiast-led markets, desktops remain the clearest route to stepwise GPU upgrades rather than full hardware replacement. Germany's 2025 growth in gaming hardware and accessories supports that pattern because component spending remained active in one of the region's most important gaming hardware markets. That keeps the Europe gaming GPU market closely linked to desktop component demand, even as other device types expand.

Gaming laptops are projected to grow at a 10.12% CAGR through 2031, making them the fastest-growing device type in the Europe gaming GPU market. ASUS highlighted this shift in 2026 with Zephyrus G14 and G16 systems that carried up to RTX 5080 Laptop GPU and RTX 5090 Laptop GPU options in Nordic markets. NVIDIA's GeForce NOW Blackwell upgrade also increased the appeal of portable systems by enabling high-resolution streaming on devices that do not carry the same local GPU headroom. Smartphones and tablets add a third route because 5G cloud gaming services expose mobile users to premium GPU rendering without changing the device form factor.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Apple Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- GIGA-BYTE Technology Co., Ltd.

- Acer Inc.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Razer Inc.

- SAPPHIRE Technology Limited

- ASRock Inc.

- ZOTAC Technology Limited

- Palit Microsystems Ltd.

- TUL Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Esports and Competitive PC Gaming Participation

- 4.3.2 Demand for Real-Time Ray Tracing and AI-Upscaling

- 4.3.3 Rising Adoption of Gaming Laptops and Portable High-Performance PCs

- 4.3.4 Mobile Gaming Monetization Moving Toward Higher-Fidelity Titles

- 4.3.5 5G Standalone Cloud Gaming Bundles Expanding Premium GPU Exposure

- 4.3.6 16 GB VRAM Expectations Reshaping Upgrade Decisions

- 4.4 Market Restraints

- 4.4.1 High Upfront Cost of Gaming GPUs and Systems

- 4.4.2 Mature Installed Base Lengthening Replacement Cycles

- 4.4.3 GDDR6 and GDDR6X Supply Tightness Inflating Midrange GPU Prices

- 4.4.4 EU Energy and Standby Compliance Pressure on High-TDP Hardware

- 4.5 Industry Value Chain Analysis

- 4.6 Supply Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By GPU Type

- 5.1.1 Discrete GPUs

- 5.1.2 Integrated GPUs

- 5.2 By Device Type

- 5.2.1 Gaming Desktops

- 5.2.2 Gaming Laptops

- 5.2.3 Smartphones and Tablets (Mobile Gaming)

- 5.3 By End-User Type

- 5.3.1 Casual Gamers

- 5.3.2 Enthusiast and Professional Gamers

- 5.4 By Memory Type

- 5.4.1 GDDR6

- 5.4.2 GDDR6X

- 5.4.3 Legacy Graphics Memory

- 5.4.4 Unified Memory

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Incorporated

- 6.4.5 Apple Inc.

- 6.4.6 MediaTek Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 ASUSTeK Computer Inc.

- 6.4.9 Micro-Star International Co., Ltd.

- 6.4.10 GIGA-BYTE Technology Co., Ltd.

- 6.4.11 Acer Inc.

- 6.4.12 Dell Technologies Inc.

- 6.4.13 HP Inc.

- 6.4.14 Lenovo Group Limited

- 6.4.15 Razer Inc.

- 6.4.16 SAPPHIRE Technology Limited

- 6.4.17 ASRock Inc.

- 6.4.18 ZOTAC Technology Limited

- 6.4.19 Palit Microsystems Ltd.

- 6.4.20 TUL Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment