|

시장보고서

상품코드

2065595

아시아태평양의 게이밍 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Gaming GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

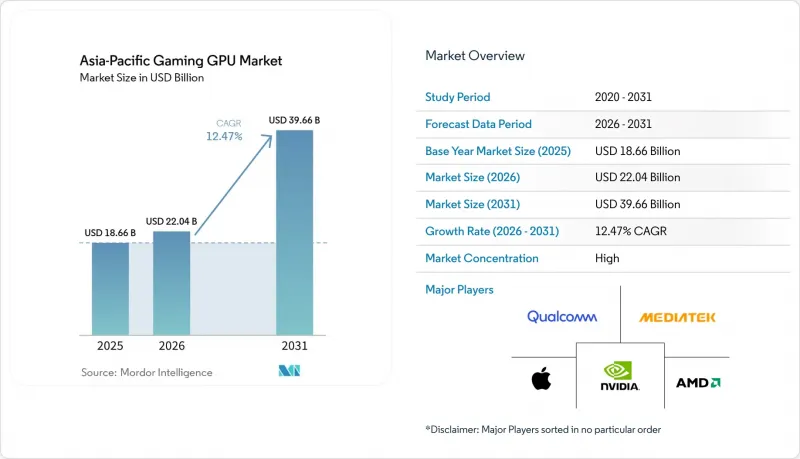

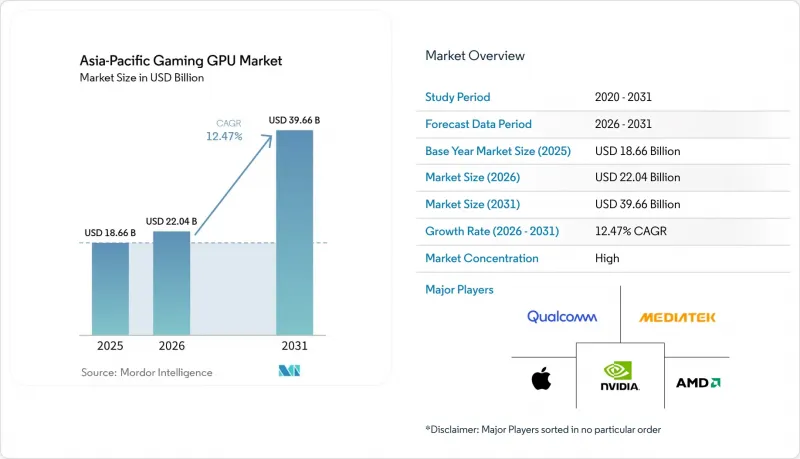

Mordor Intelligence에 의하면, 아시아태평양 게이밍 GPU 시장 규모는 2025년 186억 6,000만 달러로 평가되었고, 2026년에는 220억 4,000만 달러로 추정되고, 2026-2031년 CAGR 12.47%로 성장을 지속할 전망이며, 2031년에는 396억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 GPU 유형별(디스크리트 GPU 및 통합형 GPU), 기기 유형별(게이밍 데스크톱, 게이밍 노트북, 스마트폰 및 태블릿(모바일 게이밍)), 최종 사용자 유형별(캐주얼 게이머, 애호가 및 프로 게이머), 메모리 유형별(GDDR6, GDDR6X, 기타 메모리 유형, 통합 메모리), 그리고 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 게이밍 GPU 시장 동향 및 분석

e스포츠 상금 총액과 캠퍼스 리그가 GPU 업그레이드 주기를 연장

체계적으로 조직된 e스포츠 대회는 특히 학생들을 대상으로 고성능 게이밍에 대한 인식을 높이는 캠퍼스 형식을 통해 해당 지역 전체의 하드웨어 수요를 견인하는 원동력이 되고 있습니다. OPPO가 주최하는 ‘Hyper Legend Cup x Mobile Legends Bang Bang Campus Series 2026’에는 인도네시아, 필리핀, 말레이시아, 싱가포르에서 1,400개 이상의 팀이 등록했으며, 총 상금은 지난 대회 5만 2,000달러에서 10만 달러로 증가했습니다. 에이서(Acer)의 ‘프레데터 리그 아시아태평양 2026’도 이러한 추세를 뒷받침하고 있습니다. 아시아태평양의 14개 이상의 지역에서 팀이 모인 이 지역 대회를 통해, 스폰서가 제공한 하드웨어가 선수와 관중들 사이에서 더욱 널리 알려지게 되었기 때문입니다. 상금 체계가 더욱 공식화됨에 따라, 구매자들은 GPU 업그레이드를 단순한 선택적 구매가 아닌, 훈련 및 경쟁을 위한 실질적인 요건으로 인식하기 시작했습니다. 이러한 영향은 아시아·태평양 지역의 게이밍 GPU 시장에서 특히 두드러집니다. 이 지역에서는 프리미엄급 게이밍 하드웨어와의 첫 접점이 학교 컴퓨터실, 토너먼트, 조직화된 게임 행사장 등에서 이루어지는 경우가 많기 때문입니다.

AI 업스케일링과 프레임 생성이 중급 GPU의 유용성을 높입니다.

AI 업스케일링은 특히 구매자들이 프레임 출력과 시스템 총 비용을 면밀히 비교하는 시장에서 중급 게이밍 그래픽 카드의 가치 판단 기준을 바꿔 놓았습니다. NVIDIA는 2026년, GeForce RTX 50 시리즈 GPU를 위해 초고해상도를 구현하는 2세대 트랜스포머 모델과 6배 멀티프레임 생성 모드를 갖춘 DLSS 4.5를 도입했습니다(NVIDIA.COM). 이에 대해 AMD는 2026년 5월, FSR 4의 하드웨어 가속을 통한 업스케일링 기능을 Radeon RX 7000 시리즈를 포함한 이전 세대의 RDNA 3 및 RDNA 3.5 제품으로도 확대 적용한다고 발표했으며, 7월부터 이를 적용하기 시작했습니다. 이러한 움직임으로 인해, 일부 일반 사용자들의 경우 소프트웨어 개선을 통해 기존 하드웨어에서도 더 높은 화질과 프레임 속도를 얻을 수 있게 되었기 때문에 기기 교체 시기가 미뤄지게 될 것입니다. 한편, 아시아태평양의 게이밍 GPU 시장에서 애호가층의 업그레이드 속도를 높이는 계기가 될 것입니다. 왜냐하면 최신 프레임 생성 기능의 진가를 최대한 발휘하기 위해서는 여전히 현행 세대의 하드웨어가 필요하기 때문입니다.

첨단 GPU 및 상호 연결 기술에 대한 수출 규제

수출 규제는 제품의 입수 가능성을 제한하고 지역별 공급 우선순위를 재조정하기 때문에 아시아태평양의 게이밍 GPU 시장에 있어 여전히 가장 뚜렷한 구조적 위험 요인으로 남아 있습니다. 미국 산업안보국(BIS)은 2026년 1월 15일, 더욱 엄격한 규정 준수 조건 하에 중국 및 마카오로 수출되는 고성능 컴퓨팅용 반도체에 대한 라이선스 발급 규정을 개정하는 최종 규칙을 발표했습니다. 게이밍 제품이 직접적인 대상이 아니더라도, 인증 및 심사 요건의 변경은 보드 파트너, OEM, 채널 유통업체가 이용하는 동일한 공급망에 영향을 미칩니다. 이로 인해 중국 시장에서의 고가 제품 사업은 전망을 예측하기 어려워지며, 판매량이 저가 제품이나 중국 이외 시장으로 이동할 가능성이 있습니다. 그 결과, 지역별 성장 양상에 편차가 발생하게 되며, 고급 제품공급 상황은 소비자 수요뿐만 아니라 규정 준수 요건에 의해 점점 더 좌우되게 될 것입니다.

부문별 분석

디스크리트 GPU는 2026-2031년 연평균 성장률(CAGR) 13.02%를 기록하며 성장할 것으로 예상되며, 아시아태평양의 게이밍 GPU 시장에서 계속해서 중심적인 위치를 차지할 전망입니다. 경쟁이 치열한 게임 플레이, 높은 주사율의 디스플레이, AI 기반 렌더링 기능에는 통합형 솔루션이 일반적으로 제공할 수 있는 수준 이상의 그래픽 처리 능력이 여전히 필요하기 때문에 프리미엄 및 메인스트림 PC 게이밍 시장에서 그 입지는 여전히 견고하게 유지되고 있습니다. 또한, 이 부문은 아시아태평양의 여러 국가에서 자리 잡은 PC 게임 문화의 혜택도 누리고 있습니다. 이 국가들에서는 게임 시설이나 헤비 유저에 의한 시스템 업데이트 빈도가 일반 가정보다 더 높습니다. 이러한 추세 덕분에, 초보 소비자층의 지출이 불안정해지더라도 재구매 수요가 뒷받침되고 있습니다.

2025년 1월에 발표된 GeForce RTX 5090 및 RTX 5080을 포함한 NVIDIA의 Blackwell 세대는 게이밍 시스템의 성능 상한선을 높였으며, 새로운 하드웨어 주기에 대한 기대감을 높였습니다. NVIDIA는 2025 회계연도 매출이 전년 대비 114% 증가한 1,305억 달러를 기록했다고 보고했으며, 그래픽 부문 내에서는 급속히 확장되는 데이터센터 사업과 더불어 게이밍이 여전히 최대의 수익원으로 자리 잡고 있습니다. 아시아태평양의 게이밍 GPU 시장 하위 모델 부문에서는 통합형 GPU의 점유율이 확대되고 있습니다. 이는 최신 소비자용 프로세서 덕분에 보급형 게이밍 노트북과 일반 노트북 간의 성능 격차가 줄어들었기 때문입니다. AMD는 2026년 1분기 클라이언트 및 게이밍 부문 매출이 전년 동기 대비 23% 증가한 36억 달러를 기록했다고 보고했으나, 하반기에는 메모리 및 부품 비용 상승으로 인해 게이밍 수요가 위축될 가능성이 있다고 경고했습니다.

2025년, 아시아태평양의 게이밍 GPU 시장 규모 중 게이밍 데스크톱이 45.61%를 차지했습니다. 이는 해당 지역의 전용 게이밍 환경, e스포츠 경기장, 그리고 업그레이드가 가능한 시스템의 견고한 기반을 반영한 것입니다. 데스크톱은 사용자가 기기 전체를 새로 구입하지 않고도 그래픽 카드만 교체할 수 있기 때문에 모듈식 업그레이드의 이점을 계속해서 누리고 있습니다. 이를 통해 개인 사용자는 물론, 인터넷 카페, 트레이닝 센터, 지역 e스포츠 경기장 등의 법인 사용자들에게도 장비 교체 비용을 절감할 수 있습니다. 아시아태평양의 게이밍 GPU 시장에서 이러한 교체 모델 덕분에 많은 구매자들에게 프리미엄 플래그십 그래픽 카드가 감당하기 어려운 가격대가 되었음에도 불구하고, 데스크톱 수요는 여전히 견조하게 유지되고 있습니다.

게이밍 노트북 시장은 2026-2031년 연평균 성장률(CAGR) 12.98%를 나타낼 것으로 예측되며, 이러한 성장세는 휴대용 기기의 성능이 얼마나 급속도로 향상되고 있는지를 보여줍니다. ASUS는 2026년 1월, 최대 135W TGP의 NVIDIA GeForce RTX 5090 노트북용 GPU를 탑재한 16인치 듀얼 스크린 OLED 게이밍 노트북 ‘Zephyrus Duo’를 발표했습니다. 이는 프리미엄 모바일 시스템이 데스크톱급 성능에 대한 기대치에 얼마나 근접했는지를 보여주는 것이었습니다. 또한 ASUS는 인텔, AMD, 엔비디아의 각 옵션을 갖춘 새롭게 단장한 ‘Zephyrus G14’ 및 ‘G16’ 모델도 발표했습니다. 이로써 고성능 영역을 벗어나지 않으면서도 휴대성을 중시하는 구매자들에게 선택의 폭이 넓어졌습니다. 스마트폰, 태블릿, 핸드헬드 PC는 아시아태평양의 게이밍 GPU 업계에 여전히 중요한 위치를 차지하고 있지만, 그 경제성은 각기 다릅니다. 왜냐하면 이러한 장치에서는 개별 애드인 보드보다 프리미엄 SoC나 통합 그래픽 플랫폼이 가치의 대부분을 차지하고 있기 때문입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the asia-Pacific gaming GPU market size is expected to grow from USD 18.66 billion in 2025 to USD 22.04 billion in 2026 and is forecast to reach USD 39.66 billion by 2031 at 12.47% CAGR over 2026-2031.

This report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets (Mobile Gaming)), End-User Type (Casual Gamers, and Enthusiast and Professional Gamers), Memory Type (GDDR6, GDDR6X, Other Memory Types, and Unified Memory), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Gaming GPU Market Trends and Insights

Esports Prize Pools And Campus Leagues Expanding GPU Upgrade Cycles

Structured esports competition is acting as a hardware demand engine across the region, especially through campus formats that make high-performance gaming more visible to students. OPPO's Hyper Legend Cup x Mobile Legends Bang Bang Campus Series 2026 drew more than 1,400 team registrations across Indonesia, the Philippines, Malaysia, and Singapore, and the prize pool reached USD 100,000, up from USD 52,000 in the prior cycle. Acer's Predator League Asia-Pacific 2026 also reinforced this pattern, because a regional event with teams from more than 14 APAC territories gave sponsored hardware stronger visibility among players and spectators. As prize structures become more formal, buyers start to view GPU upgrades as a practical requirement for training and competition rather than a discretionary purchase. That effect is especially relevant in the Asia-Pacific gaming GPU market, where first exposure to premium gaming hardware often happens in school labs, tournaments, and organized gaming venues.

AI Upscaling And Frame Generation Raising Mid-Tier GPU Utility

AI upscaling has changed the value equation for mid-range gaming cards, especially in markets where buyers compare frame output closely against total system cost. NVIDIA introduced DLSS 4.5 in 2026 with a second-generation transformer model for super resolution and a 6x Multi Frame Generation mode for GeForce RTX 50 Series GPUs NVIDIA.COM. AMD answered in May 2026 by extending FSR 4 hardware-accelerated upscaling to older RDNA 3 and RDNA 3.5 products, including the Radeon RX 7000 series, with rollout starting in July. This shift delays replacement for some casual buyers, because existing hardware can now deliver better image quality and frame rates through software improvements. At the same time, it accelerates upgrades among enthusiasts in the Asia-Pacific gaming GPU market, because the newest frame generation features still require current-generation hardware to unlock their full value.

Export Controls On Advanced GPUs And Interconnects

Export controls remain the clearest structural risk to the Asia-Pacific gaming GPU market because they narrow product availability and reshape regional supply priorities. The U.S. Bureau of Industry and Security issued a final rule on January 15, 2026, that revised export licensing for advanced computing semiconductors to China and Macau under stricter compliance conditions. Even when gaming products are not the direct target, changes in certification and review requirements affect the same supply chains used by board partners, OEMs, and channel distributors. This makes the premium end of the China business less predictable and can shift volumes toward lower-tier products or non-China markets. The result is a more uneven regional growth pattern, with high-end availability increasingly shaped by compliance rules rather than only by consumer demand.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Gaming Rollouts Broadening Access To High-Fidelity Play

- Premium Mobile SoCs Bringing Hardware Ray Tracing To Mobile Games

- Advanced Packaging And VRAM Tightness Inflating Board Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs are projected to advance at a 13.02% CAGR from 2026 to 2031, which keeps them at the center of the Asia-Pacific gaming GPU market. Their position remains strong in premium and mainstream PC gaming because competitive play, higher refresh displays, and AI-led rendering features still require more graphics headroom than integrated solutions can usually provide. The segment also benefits from the organized PC gaming culture in several APAC countries, where gaming venues and heavy-use players refresh systems more often than casual households. That pattern supports repeat demand even when entry-tier consumer spending becomes uneven.

NVIDIA's Blackwell generation, including the GeForce RTX 5090 and RTX 5080, introduced in January 2025, lifted the performance ceiling for gaming systems and raised expectations for new hardware cycles. NVIDIA reported fiscal 2025 revenue of USD 130.5 billion, up 114% year over year, with gaming remaining the largest contributor within its Graphics segment alongside a rapidly scaling data center business. Integrated GPUs are gaining more ground at the low end of the Asia-Pacific gaming GPU industry, because newer client processors have narrowed the performance gap for entry gaming and mixed-use laptops. AMD reported Client and Gaming revenue of USD 3.6 billion in the first quarter of 2026, up 23% year over year, but it also warned that gaming demand would face pressure from higher memory and component costs later in the year.

Gaming desktops held 45.61% of the Asia-Pacific gaming GPU market size in 2025, which reflected the region's strong base of dedicated gaming setups, esports venues, and upgradable systems. Desktops continue to benefit from modular upgrades, because buyers can replace the graphics card without replacing the full device. That lowers refresh costs for individuals and for institutional buyers such as gaming cafes, training centers, and local esports venues. In the Asia-Pacific gaming GPU market, this replacement model keeps desktop demand durable even when premium flagship cards move out of reach for many buyers.

Gaming laptops are forecast to expand at a 12.98% CAGR from 2026 to 2031, and that pace shows how quickly portable performance is improving. ASUS announced the Zephyrus Duo in January 2026 as a 16-inch dual-screen OLED gaming laptop with up to an NVIDIA GeForce RTX 5090 Laptop GPU at 135W TGP, which showed how close premium mobile systems had moved toward desktop-class performance expectations. ASUS also introduced refreshed Zephyrus G14 and G16 models with Intel, AMD, and NVIDIA options, which widened the choice set for buyers seeking portability without leaving the high-performance bracket. Smartphones, tablets, and handheld PCs remain important to the Asia-Pacific gaming GPU industry, but their economics differ because premium SoCs and integrated graphics platforms drive more of their value than discrete add-in boards.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Qualcomm Technologies, Inc.

- Intel Corporation

- MediaTek Inc.

- Apple Inc.

- Moore Threads

- Samsung Electronics Co., Ltd.

- ASUSTeK Computer Inc.

- Micro-Star INT'L CO., LTD.

- ZOTAC Technology Limited

- Palit Microsystems Ltd.

- SAPPHIRE Technology Limited

- TUL Corporation

- Acer Inc.

- Lenovo Group Limited

- Dell Inc.

- HP Development Company, L.P.

- Razer Inc.

- ASRock Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Esports Prize Pools and Campus Leagues Expanding GPU Upgrade Cycles

- 4.3.2 AI Upscaling and Frame Generation Raising Mid-Tier GPU Utility

- 4.3.3 Cloud Gaming Rollouts Broadening Access to High-Fidelity Play

- 4.3.4 Premium Mobile SoCs Bringing Hardware Ray Tracing to Mobile Games

- 4.3.5 Handheld PC Spillover Lifting Demand for Laptop-Class GPUs

- 4.3.6 China Localization Efforts Diversifying Gaming GPU Supply

- 4.4 Market Restraints

- 4.4.1 Export Controls on Advanced GPUs and Interconnects

- 4.4.2 Advanced Packaging and VRAM Tightness Inflating Board Costs

- 4.4.3 Integrated and Unified Memory Designs Compressing Entry-Tier Demand

- 4.4.4 Power and Thermal Limits in Compact Gaming Devices

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By GPU Type

- 5.1.1 Discrete GPUs

- 5.1.2 Integrated GPUs

- 5.2 By Device Type

- 5.2.1 Gaming Desktops

- 5.2.2 Gaming Laptops

- 5.2.3 Smartphones and Tablets (Mobile Gaming)

- 5.3 By End-User Type

- 5.3.1 Casual Gamers

- 5.3.2 Enthusiast and Professional Gamers

- 5.4 By Memory Type

- 5.4.1 GDDR6

- 5.4.2 GDDR6X

- 5.4.3 Legacy Graphics Memory

- 5.4.4 Unified Memory

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Qualcomm Technologies, Inc.

- 6.4.4 Intel Corporation

- 6.4.5 MediaTek Inc.

- 6.4.6 Apple Inc.

- 6.4.7 Moore Threads

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Micro-Star INT'L CO., LTD.

- 6.4.11 ZOTAC Technology Limited

- 6.4.12 Palit Microsystems Ltd.

- 6.4.13 SAPPHIRE Technology Limited

- 6.4.14 TUL Corporation

- 6.4.15 Acer Inc.

- 6.4.16 Lenovo Group Limited

- 6.4.17 Dell Inc.

- 6.4.18 HP Development Company, L.P.

- 6.4.19 Razer Inc.

- 6.4.20 ASRock Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment