|

시장보고서

상품코드

2065587

북미의 게이밍 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Gaming GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

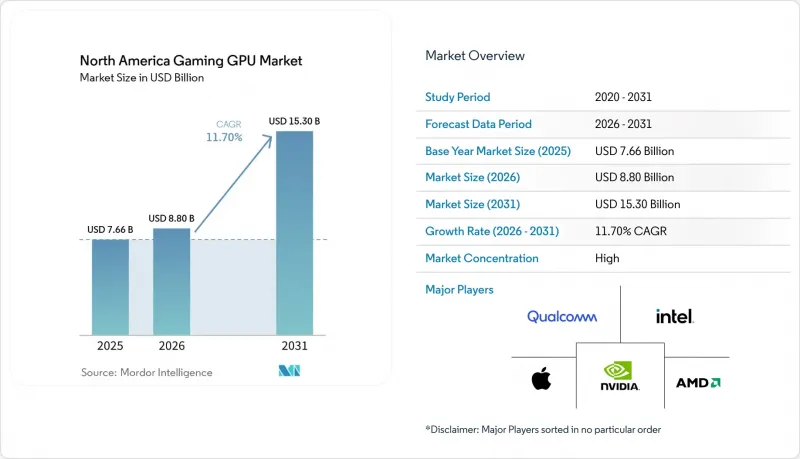

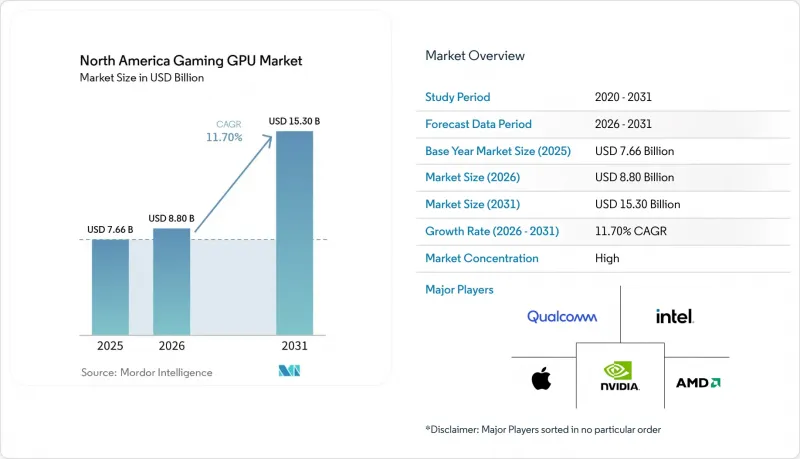

Mordor Intelligence에 의하면, 북미의 게이밍 GPU 시장 규모는 2025년 76억 6,000만 달러로 평가되었고, 2026년 88억 달러로 추정되고, 2031년까지 153억 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 11.70%를 나타낼 전망입니다.

본 보고서는 GPU 유형별(디스크리트 GPU 및 통합형 GPU), 기기 유형별(게이밍 데스크톱, 게이밍 노트북, 스마트폰 및 태블릿(모바일 게이밍)), 최종 사용자 유형별(캐주얼 게이머, 애호가 및 프로 게이머), 메모리 유형별(GDDR6, GDDR6X, 레거시 그래픽 메모리, 통합 메모리), 그리고 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 게이밍 GPU 시장 동향 및 인사이트

AI 기반 업스케일링과 뉴럴 렌더링이 업그레이드 주기를 완전히 새롭게 바꾸다.

북미의 게이밍 GPU 시장에서 최신 시각적 성능의 향상은 최신 하드웨어 플랫폼에 달려 있기 때문에 AI를 활용한 프레임 생성은 이제 순수한 렌더링 성능만큼이나 중요해졌습니다. NVIDIA는 CES 2026에서 초고해상도 처리를 위한 2세대 트랜스포머 모델과 새로운 ‘다이나믹 멀티 프레임 제너레이션’ 기능을 탑재한 DLSS 4.5를 발표했으나, 이러한 기능들은 RTX 50 시리즈의 Blackwell GPU로만 제한되었습니다. 이러한 하드웨어적 제약은 구매자의 행동을 변화시키고 있습니다. 구형 그래픽 카드에서도 게임을 실행하는 것은 가능하지만, 신형 모델과 동등한 이미지 재구성, 레이턴시 처리, 혹은 프레임 전송 경험을 제공할 수는 없기 때문입니다. AMD 역시 ML을 활용한 렌더링을 더욱 적극적으로 추진하고 있으며, FSR SDK 2.2에서는 RDNA 4를 위해 ML 기반의 ‘FSR 업스케일링 4.1’과 ‘레이 리제너레이션 1.1’을 추가하는 한편, 구형 하드웨어를 위한 분석 기반의 폴백 모드도 유지하고 있습니다. 이러한 기술에 최적화된 주요 타이틀이 늘어남에 따라, 북미 게이밍 GPU 시장에서는 업그레이드 주기가 단축되고, 비주얼 스택의 모든 기능을 최대한 활용할 수 있는 그래픽 카드에 대한 수요가 높아지고 있습니다. 이로 인해 하드웨어 출시와 강력한 소프트웨어 생태계를 결합하여 각 제품 계층 간 기능을 명확하게 구분할 수 있는 벤더에게 경쟁 우위가 생기고 있습니다.

AAA급 게임과 레이 트레이싱이 GPU의 최소 사양을 높입니다.

또한, 현재의 하이엔드 게임에서는 레이 트레이싱이나 AI 지원 렌더링이 선택 사항이 아닌 표준 사양으로 간주되고 있기 때문에 북미 게이밍 GPU 시장은 상위 모델로 이동하고 있습니다. NVIDIA는 5세대 텐서 코어, 4세대 RT 코어, PCIe Gen 5 및 GDDR7 지원을 핵심으로 한 Blackwell GeForce RTX 50 시리즈를 개발했는데, 이는 프리미엄 게이밍 워크로드가 어떻게 진화하고 있는지를 보여줍니다. 그 후, 이 회사는 2026년 4월 RTX 5060 출시를 통해 해당 기능 세트를 메인스트림 시장까지 확대했으며, 299달러 가격대의 제품에서 DLSS 4와 멀티프레임 제너레이션을 구현했습니다. AMD는 Computex 2025에서 Radeon RX 9060 XT와 FSR 4 지원을 발표하며 이에 대응했고, 메인스트림 시장에서의 경쟁이 기존의 그래픽 처리량과 마찬가지로 뉴럴 렌더링 기능에도 크게 좌우된다는 사실을 입증했습니다. 이로 인해 더 많은 구매자들이 중상급 및 매니아급 사양으로 눈을 돌리고 있습니다. 이는 고주사율 디스플레이에서 부드러운 게임 플레이를 구현하기 위해서는 단순히 셰이더 수가 많을 뿐만 아니라, 전용 AI 및 레이 트레이싱 블록에 대한 의존도가 높아지고 있기 때문입니다. 그 결과, 북미 게이밍 GPU 시장에서 주요 게임의 출시가 이전보다 더 강력한 동력이 되어 고성능 그래픽 카드에 대한 지출을 촉진하고 있습니다.

관세 및 무역 조치로 인한 수입 비용 상승

제232조는 2026년 1월 15일부터 특정 수입 반도체 및 파생 제품에 25%의 관세를 부과함으로써 북미 게이밍 GPU 시장의 가격 구조를 변화시켰습니다. 애드인 보드의 대부분은 미국 이외의 지역에서 조립되므로, 이 추가 관세로 인해 소매 마진, 물류 비용, 유통 마진이 적용되기 전의 입고 비용이 상승하게 됩니다. 이러한 영향을 가장 잘 흡수하지 못하는 것은 보급형 가격대인데, 이 가격대에서는 구매자가 가격 변동에 민감할 뿐만 아니라, 보드 파트너가 다른 부분에서 가격 인상분을 상쇄할 수 있는 유연성이 낮기 때문입니다. 또한, 이 정책으로 인해 공급망은 지역별 조립 거점 선정에 대해 보다 신중하게 재검토하게 될 것이며, 단기적으로는 소매 가격이 높은 수준을 유지할 것으로 보이지만, 장기적으로는 제조 거점 이전을 촉진할 가능성이 있습니다. 캐나다와 멕시코도 여전히 그 압박을 느끼고 있습니다. 이 지역의 가격 결정은 대개 미국의 유통 채널에서 시작되어, 이후 인근 시장으로 파급되기 때문입니다. 그 결과, 신제품 출시에 대한 관심은 여전히 높은 수준을 유지하고 있음에도 불구하고, 북미 게이밍 GPU 시장의 판매량 회복 속도는 둔화되고 있습니다.

부문별 분석

2025년, 디스크리트 GPU는 북미 게이밍용 그래픽 처리 장치(GPU) 시장 점유율의 86.67%를 차지했으며, 이 부문은 2031년까지 연평균 성장률(CAGR) 12.12%로 확대될 것으로 전망됩니다. 이러한 규모와 성장 속도의 조합은 북미 게이밍 GPU 업계가 공유형 실리콘 솔루션이 아닌, 여전히 전용 그래픽 하드웨어에 의해 정의되고 있음을 보여줍니다. NVIDIA의 RTX 50 시리즈 ‘Blackwell’ 아키텍처는 5세대 텐서 코어와 4세대 RT 코어를 통해 성능의 최저 기준을 높임으로써, 2025-2026년 출시된 게이밍용 디스크리트 제품의 매력을 한층 더 높였습니다. 또한, RTX 5060 및 관련 Blackwell 제품들은 보다 합리적인 가격대에서 이러한 기능을 이용할 수 있게 함으로써, 타겟 구매층을 하이엔드층에만 국한되지 않고 더욱 확대하는 데 기여했습니다.

통합형 GPU는 북미 게이밍 GPU 시장에서 여전히 소규모 부문에 머물러 있지만, 성능이 향상됨에 따라 가벼운 게임 플레이나 가성비를 중시하는 시스템의 경우 충분히 고려해 볼 만한 선택지가 되고 있습니다. 인텔의 ‘팬서 레이크’ Arc B390은 벤치마크에서 이전 AMD 890M iGPU를 능가했으며, 엔트리급 게임에서는 RTX 4050 노트북급에 가까운 결과를 보여줌으로써, 내장 그래픽의 기준선이 얼마나 빠르게 상승하고 있는지를 보여주고 있습니다. 그렇긴 하지만, 공유 메모리의 대역폭, 더욱 엄격해진 전력 소비 제한, 그리고 고부하 레이 트레이싱 처리 시의 낮은 성능 등의 요인으로 인해, 요구 사항이 까다로운 게임 플레이 시나리오에서는 통합형 그래픽스가 여전히 독립형 그래픽 카드에 미치지 못하는 상황입니다. 따라서 북미 게이밍 GPU 시장에서 예측 기간 동안 전용 그래픽 카드가 매출, 수익성 및 제품 차별화의 기반이 될 것으로 전망됩니다.

2025년, 북미 게이밍 GPU 시장 규모에서 게이밍 데스크톱은 54.31%의 점유율을 차지했습니다. 이 추세는 여전히 최대 성능의 디스크리트 GPU, 더 큰 전력 예산, 폭넓은 업그레이드 유연성, 그리고 얇은 모바일 시스템에서는 사용할 수 없는 맞춤형 냉각 방식을 선호하는 열성적인 DIY 사용자층의 강세를 반영하고 있습니다. 또한, 블랙웰 세대는 PCIe Gen 5를 기반으로 구축된 최초의 소비자용 GPU 라인업이었기 때문에 순수한 성능 향상은 물론 호환성 측면에서도 플랫폼의 쇄신을 촉진하여 새로운 데스크톱 PC 구축을 뒷받침했습니다. 따라서 북미 게이밍 GPU 시장에서 데스크톱 PC는 여전히 핵심적인 수익 기반이며, 프리미엄 사양이나 애드인 보드의 다양성을 가장 쉽게 수익화할 수 있는 분야입니다.

게이밍 노트북 시장은 2031년까지 연평균 성장률(CAGR) 12.67%로 성장할 것으로 예상되며, 북미 게이밍 GPU 시장에서 가장 빠르게 성장하고 있는 기기 유형입니다. 이러한 성장은 열 설계의 개선, OEM 제조업체들의 폭넓은 지원, 그리고 프리미엄급 게이밍 성능을 희생하지 않으면서도 첨단 AI 지원 렌더링을 구현할 수 있는 휴대용 시스템에 대한 소비자들의 수용도가 높아지고 있음을 반영합니다. NVIDIA의 RTX 50 시리즈 노트북 출시로 인해 ASUS, Lenovo, HP, MSI 등 각 브랜드의 광범위한 OEM 공급 및 사전 예약을 통해 해당 지역 전체에서 하이엔드 게이밍 노트북의 보급이 촉진되었습니다. 스마트폰 및 태블릿은 2031년까지 가장 규모가 작은 기기 부문으로 남아 있을 것이지만, 퀄컴(Qualcomm)과 미디어텍(MediaTek)이 플래그십 모바일 칩에 콘솔급 렌더링 기능을 탑재함에 따라 그 그래픽 성능은 급속히 향상되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the north america gaming GPU market size is projected to expand from USD 7.66 billion in 2025 and USD 8.80 billion in 2026 to USD 15.30 billion by 2031, registering a CAGR of 11.70% between 2026 to 2031.

This report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets (Mobile Gaming)), End-User Type (Casual Gamers, and Enthusiast and Professional Gamers), Memory Type (GDDR6, GDDR6X, Legacy Graphics Memory, and Unified Memory), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Gaming GPU Market Trends and Insights

AI Upscaling And Neural Rendering Refresh The Upgrade Cycle

In the North America gaming GPU market, AI frame generation is now as important as raw rendering power because the newest visual gains are tied to the latest hardware platforms. NVIDIA introduced DLSS 4.5 at CES 2026 with a second-generation transformer model for super resolution and a new Dynamic Multi Frame Generation capability, and those features were limited to RTX 50-series Blackwell GPUs. That hardware gating changes buyer behavior because an older card can still run a game, yet it cannot deliver the same image reconstruction, latency handling, or frame delivery experience as a newer model. AMD is also pushing further into ML-assisted rendering, with the FSR SDK 2.2 adding ML-powered FSR Upscaling 4.1 and Ray Regeneration 1.1 for RDNA 4 while still keeping analytical fallback modes for older hardware. As more major titles are optimized around these techniques, the North America gaming GPU market is shifting toward shorter upgrade windows and stronger demand for cards that can unlock the full visual stack. This gives an advantage to vendors that can pair hardware launches with a strong software ecosystem and clear feature separation across each product tier.

AAA Titles And Ray Tracing Raise Baseline GPU Requirements

The North America gaming GPU market is also moving upward because current high-end games treat ray tracing and AI-assisted rendering as baseline expectations rather than as optional extras. NVIDIA built the Blackwell GeForce RTX 50 family around fifth-generation Tensor Cores, fourth-generation RT Cores, PCIe Gen 5, and GDDR7 support, which shows how premium gaming workloads are evolving. The company then extended that feature set into the mainstream tier with the RTX 5060 launch in April 2026, which brought DLSS 4 and Multi Frame Generation to a USD 299 product level. AMD responded at Computex 2025 with the Radeon RX 9060 XT and FSR 4 support, confirming that mainstream competition now depends on neural rendering capability as much as on conventional graphics throughput. This pushes more buyers toward upper mid-range and enthusiast configurations, because smooth play on high refresh displays increasingly depends on dedicated AI and ray-tracing blocks instead of only raw shader count. As a result, major game releases now have a stronger ability to move spending toward higher performance cards in the North America gaming GPU market.

Tariff And Trade Actions Raise Import Costs

Section 232 changed pricing conditions in the North America gaming GPU market by imposing a 25% duty on certain imported semiconductors and derivative products from January 15, 2026. Because a large share of add-in-board supply is assembled outside the United States, the added duty lifts landed cost before retail margin, logistics cost, and channel markup are applied. That is hardest to absorb at entry price points, where buyers are more sensitive to price changes and board partners have less flexibility to offset the increase elsewhere. The policy also pushes supply chains to review regional assembly choices more closely, which may support longer-term manufacturing shifts even while near-term shelf prices remain elevated. Canada and Mexico still feel part of that pressure because pricing decisions for the region often start in the U.S. channel and then spread across neighboring markets. The result is a slower unit recovery path for the North America gaming GPU market, even when interest in new launches remains solid.

Other drivers and restraints analyzed in the detailed report include:

- Esports, Streaming, And Creator Demand Sustain Premium GPU Spend

- Mobile AAA Pipelines Expand Gaming GPU Demand

- Elevated GDDR Pricing Pressures GPU Affordability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs held 86.67% of the North America Gaming Graphics Processing Unit (GPU) market share in 2025, and the segment is projected to expand at a 12.12% CAGR through 2031. This combination of scale and speed shows that the North America gaming GPU industry is still being defined by dedicated graphics hardware rather than by shared silicon solutions. NVIDIA's RTX 50-series Blackwell architecture raised the performance floor with fifth-generation Tensor Cores and fourth-generation RT Cores, which reinforced the appeal of discrete gaming products across 2025 and 2026 launches. The RTX 5060 and related Blackwell products also widened access to those features at lower price points, which helped extend the addressable buyer base beyond only the top end.

Integrated GPUs remained the smaller tier in the North America gaming GPU market, even as their performance improved enough to become a credible option for lighter play and value-focused systems. Intel's Panther Lake Arc B390 was benchmarked above the earlier AMD 890M iGPU and near RTX 4050 laptop-class results in entry-level titles, which shows how quickly the baseline is rising for integrated graphics. Even so, shared memory bandwidth, tighter power limits, and weaker performance under heavier ray-traced loads still keep integrated options below discrete cards in demanding play scenarios. That is why dedicated graphics should continue to anchor revenue, profitability, and product differentiation across the forecast period in the North America gaming GPU market.

Gaming desktops accounted for a 54.31% share of the North America Gaming Graphics Processing Unit (GPU) market size in 2025. That lead reflects the strength of enthusiast builders who still prefer full-power discrete cards, larger power budgets, broader upgrade flexibility, and custom cooling that is not available in thinner mobile systems. The Blackwell generation also encouraged fresh desktop builds because it was the first consumer GPU line built around PCIe Gen 5, which added a compatibility reason for platform refresh beyond raw performance gains. In the North America gaming GPU market, desktops therefore remain the core revenue base where premium specifications and add-in-board variety are easiest to monetize.

Gaming laptops are projected to grow at a 12.67% CAGR through 2031, making them the fastest-expanding device type in the North America gaming GPU market. That growth reflects better thermal design, broader OEM support, and stronger consumer acceptance of portable systems that can deliver advanced AI-assisted rendering without giving up premium gaming performance. NVIDIA's laptop rollout for the RTX 50 family, including broad OEM availability and pre-orders across ASUS, Lenovo, HP, MSI, and other brands, helped normalize premium notebook gaming across the region. Smartphones and tablets remain the smallest device segment through 2031, but their graphics capability is rising quickly as Qualcomm and MediaTek bring console-like rendering features into flagship mobile chips.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Apple Inc.

- MediaTek Inc.

- Palit Microsystems Ltd.

- ASUSTeK Computer Inc.

- Acer Inc.

- Lenovo Group Limited

- Dell Technologies Inc.

- HP Inc.

- Micro-Star International Co., Ltd.

- GIGABYTE Technology Co., Ltd.

- ASRock Inc.

- ZOTAC Technology Limited

- PNY Technologies, Inc.

- SAPPHIRE Technology Limited

- TUL Corporation

- Pine Technology Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI Upscaling and Neural Rendering Refresh the Upgrade Cycle

- 4.2.2 AAA Titles and Ray Tracing Raise Baseline GPU Requirements

- 4.2.3 Esports, Streaming, and Creator Demand Sustain Premium GPU Spend

- 4.2.4 Mobile AAA Pipelines Expand Gaming GPU Demand

- 4.2.5 Vapor-Chamber Designs Unlock Thinner High-Performance Gaming Laptops

- 4.2.6 Unreal Engine 5 Mobile Toolchains Improve Premium Phone GPU Monetization

- 4.3 Market Restraints

- 4.3.1 Tariff and Trade Actions Raise Import Costs

- 4.3.2 Elevated GDDR Pricing Pressures GPU Affordability

- 4.3.3 Stronger Integrated Graphics Erode Entry-Level Discrete Demand

- 4.3.4 Notebook Thermal Limits Constrain Real-World Performance Gains

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By GPU Type

- 5.1.1 Discrete GPUs

- 5.1.2 Integrated GPUs

- 5.2 By Device Type

- 5.2.1 Gaming Desktops

- 5.2.2 Gaming Laptops

- 5.2.3 Smartphones and Tablets

- 5.3 By End-User Type

- 5.3.1 Casual Gamers

- 5.3.2 Enthusiast and Professional Gamers

- 5.4 By Memory Type

- 5.4.1 GDDR6

- 5.4.2 GDDR6X

- 5.4.3 Legacy Graphics Memory

- 5.4.4 Unified Memory

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Incorporated

- 6.4.5 Apple Inc.

- 6.4.6 MediaTek Inc.

- 6.4.7 Palit Microsystems Ltd.

- 6.4.8 ASUSTeK Computer Inc.

- 6.4.9 Acer Inc.

- 6.4.10 Lenovo Group Limited

- 6.4.11 Dell Technologies Inc.

- 6.4.12 HP Inc.

- 6.4.13 Micro-Star International Co., Ltd.

- 6.4.14 GIGABYTE Technology Co., Ltd.

- 6.4.15 ASRock Inc.

- 6.4.16 ZOTAC Technology Limited

- 6.4.17 PNY Technologies, Inc.

- 6.4.18 SAPPHIRE Technology Limited

- 6.4.19 TUL Corporation

- 6.4.20 Pine Technology Holdings Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment