|

시장보고서

상품코드

2066419

인도의 석유 및 가스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Oil and Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

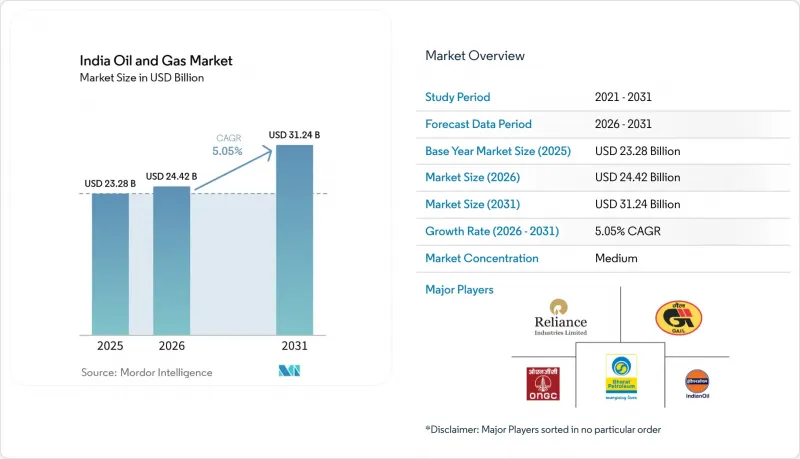

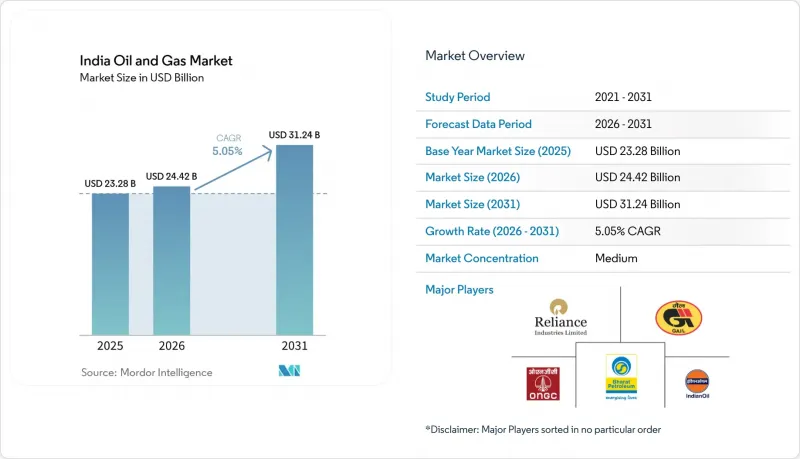

Mordor Intelligence에 의하면, 인도의 석유 및 가스 시장 규모는 2025년 232억 8,000만 달러로 평가되었고, 2026년에는 244억 2,000만 달러로 추정되고, 2026-2031년 CAGR 5.05%로 성장을 지속할 전망이며, 2031년까지 312억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 부문별(업스트림, 중류, 하류), 지역별(육상 및 해상), 서비스별(건설, 유지보수 및 턴어라운드, 해체)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

인도의 석유 및 가스 시장 동향 및 인사이트

국내 탐사 및 생산(E&P) 라이선스 입찰 요건 강화

‘미개발 광구 라이선싱 정책(OALP)’에 따라, 2025년 OALP-VIII 라운드에서는 14개의 광구가 배정되었으며, 기존에는 국영 기업으로만 제한되었던 분지에 민간 탐사 기업이 진출하게 되었습니다. 케언 오일 앤 가스(Cairn Oil &Gas)를 비롯한 독립 기업들은 현재 22개의 탐사 광구에서 지분을 보유하고 있으며, 이를 통해 평가 기간이 단축되고, 단기적인 생산량 증가로 이어지는 2차 회수 시범 사업이 촉진되고 있습니다. 수익 배분형 재정 모델에 따라 원유 가격이 하락할 경우 정부의 몫이 줄어들어, 미개발 분지의 경제성이 향상되고 있습니다. 규제 당국이 작업 계획의 주요 단계(마일스톤)를 엄격하게 적용하고 있기 때문에 사업자들은 머신러닝을 활용한 지진 탐사 도구에 의존하여 3년이라는 기간 내에 데이터 수집을 완료하고 있습니다. 이러한 동향들이 맞물려 시추 활동이 활발해지고 있으며, 이는 인도 석유 및 가스 시장에 긍정적인 영향을 미치고 있습니다.

가스 이용형 산업 클러스터의 급증

새로운 메탄올-올레핀 전환 플랜트와 직접환원철(DRI) 시설 덕분에 2027년까지 하루 1,200만 scm의 가스 수요가 추가되어, 기존의 비료 구매 업체를 넘어선 폭넓은 수요 기반이 형성되고 있습니다. 구자라트주의 다헤지-하지라 회랑만 해도 ‘테이크 오어 페이(Take or Pay)’ 계약에 따라 연간 4.2 bcm공급이 확보되어 있어, 파이프라인의 수송량을 유지하고 있습니다. 타밀나두주의 카다롤 콤플렉스에서는 2026년에 1.2 Mt 규모의 에틸렌 크래커가 가동을 시작하고, 에노아에서 공급되는 재기화 LNG를 흡수함에 따라 지역 수급 균형이 타이트해질 전망입니다. 브렌트 원유 가격이 배럴당 70달러를 초과할 경우, MMBtu당 70루피라는 통일된 요금 상한선으로 인해 파이프라인 수송은 나프타 수송과 경쟁하게 됩니다. 석탄 화력 발전소에 비해 가스 화력 발전소의 열효율이 높다는 점은 에너지 집약형 제조업체들이 환경 규제를 준수하도록 뒷받침합니다.

ESG를 배경으로 한 화석 자산에서의 자본 유출

2025년, 탄소중립 목표가 정착됨에 따라 기관 투자자들은 인도의 화석연료 관련 주식에서 약 18억 달러를 매도했습니다. 주식시장은 그동안 업스트림 프로젝트 자본의 3분의 1을 공급해 왔으나, 현재 민간 사업자들은 자금 조달을 위해 벤치마크 금리보다 150-200 베이시스 포인트 높은 스프레드를 지불할 수밖에 없어, 프로젝트의 수익성이 저하되고 있습니다. GAIL사의 21억 달러 규모의 자그디슈푸르-할디아 파이프라인은 국제 대출 기관으로부터 자금을 조달하는 데 어려움을 겪고 있어, 이 회사는 대출 한도에 근접한 국내 은행에 의존할 수밖에 없는 상황입니다. 또한, ESG 스크리닝 역시 미드스트림 및 다운스트림 프로젝트에 제약을 가하고 있습니다. 공개 체계에 따라 기업은 스코프 3 배출량을 정량화해야 할 의무가 있으며, 이는 일부 세계 펀드에게 천연가스가 불리한 입장에 놓여 있기 때문입니다. 그 결과 발생하는 자금 부족은 최종 투자 결정을 지연시키고, 인도의 석유 및 가스 시장 성장을 둔화시키고 있습니다.

부문별 분석

2025년, 업스트림 부문은 인도 석유 및 가스 시장 수익의 69.1%를 차지했으나, 성숙한 유전에서 인공 채유에 대한 의존도가 높아짐에 따라 영업이익률은 34%로 하락했고, 양수 비용은 배럴당 22달러로 상승했습니다. 하류 부문인 정유 및 석유화학은 연평균 5.4% 성장했으며, 릴라이언스사의 2025 회계연도 정유 매출총이익률은 배럴당 11.80달러를 기록했고, 처리량의 18%가 폴리머였기 때문에 싱가포르 벤치마크보다 7.30달러 높은 수준을 나타냈습니다. 중류 부문이 나머지 시장 점유율을 차지하고 있지만, 통일된 요금 상한선으로 인해 취급량이 증가하더라도 수익 상한선이 제한되고 있습니다.

가치를 창출하는 구조는 변화하고 있습니다. 이구치에서 폴리머 통에 이르기까지 분자 단계를 관리하는 통합형 기업은 더 높은 수익률을 확보하고 있습니다. 석유화학 사업의 확장은 수익률을 높이는 동시에 정유시설를 자동차 연료 시장의 경기 변동으로부터 보호해 주며, 인도의 석유 및 가스 시장에서 하류 자산의 전략적 중요성이 높아지고 있습니다. 업스트림 기업들은 카른사의 폴리머 주입법과 같은 증산 기술의 시범 사업을 통해 이에 대응하고 있으며, 이를 통해 1억 4,000만 배럴의 증산이 예상되어 하류 부문의 공정 최적화 이념을 반영하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the india oil and gas market size is expected to grow from USD 23.28 billion in 2025 to USD 24.42 billion in 2026 and is forecast to reach USD 31.24 billion by 2031 at 5.05% CAGR over 2026-2031.

This report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

India Oil and Gas Market Trends and Insights

Tightening Domestic E&P Licensing Rounds

The Open Acreage Licensing Policy awarded 14 blocks in the OALP-VIII round during 2025, bringing private explorers into basins historically reserved for state-owned firms. Cairn Oil & Gas and other independents now hold interests in 22 exploration blocks, compressing appraisal timelines and encouraging secondary-recovery pilots that raise near-term production. The revenue-sharing fiscal model lowers the government's take when crude prices soften, improving frontier basin economics. Regulators enforce strict work-program milestones, so operators rely on machine-learning seismic tools to finish data acquisition within three-year windows. These developments collectively lift drilling activity and underpin the positive impact on the Indian oil and gas market.

Surge in Gas-Based Industrial Clusters

New methanol-to-olefins and direct-reduced iron facilities added 12 million scm per day of gas demand by 2027, broadening the buyer base beyond legacy fertilizer offtakers. Gujarat's Dahej-Hazira corridor alone locked in 4.2 bcm of annual supply under take-or-pay contracts, sustaining pipeline throughput for. Tamil Nadu's Cuddalore complex will commission a 1.2 Mt ethylene cracker in 2026, absorbing regasified LNG from Ennore and tightening regional balances. A unified tariff cap of INR 70 per MMBtu keeps pipeline transport competitive with naphtha when Brent exceeds USD 70 per barrel. Higher thermal efficiency of gas-fired units relative to coal bolsters environmental compliance for energy-intensive manufacturers.

ESG-Driven Capital Flight from Fossil Assets

Institutional investors divested roughly USD 1.8 billion from Indian fossil equities in 2025 as net-zero mandates took hold. Equity markets had historically supplied one-third of upstream project capital, so private operators now pay 150-200 basis-point spreads above benchmarks to secure debt, eroding project economics. GAIL's USD 2.1 billion Jagdishpur-Haldia pipeline struggled to attract international lenders, pushing the firm toward domestic banks that approach exposure ceilings. ESG screens also constrain midstream and downstream projects because disclosure frameworks force companies to quantify Scope 3 emissions, which positions gas unfavorably for some global funds. The resulting capital scarcity delays final investment decisions and tempers growth in the Indian oil and gas market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of City-Gas Distribution Networks

- Rising Private Investments in Refinery Upgrades

- Slow Land-Acquisition for Trunk Pipelines Constrains Infrastructure Development

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Upstream held 69.1% of the Indian oil and gas market revenue in 2025, yet its operating margin fell to 34% as mature fields required more artificial lift, pushing lifting costs to USD 22 per barrel. Downstream refining and petrochemicals expanded at 5.4% a year, and Reliance's FY2025 gross refining margin of USD 11.80 per barrel exceeded the Singapore benchmark by USD 7.30 because 18% of throughput became polymers. Midstream held the balance, but a unified tariff cap limits upside even as volumes grow.

Value capture is shifting: integrated players controlling molecules from the wellhead to the barrel of polymer command higher returns. Petrochemical add-ons boost margins while insulating refineries from motor-fuel cyclicality, making downstream assets increasingly strategic to the Indian oil and gas market. Upstream firms are responding with enhanced-oil-recovery pilots such as Cairn's polymer flood that could add 140 million barrels, mirroring downstream process-optimization philosophies.

List of Companies Covered in this Report:

- Oil and Natural Gas Corporation (ONGC)

- Oil India Limited

- Reliance Industries Ltd.

- Indian Oil Corporation Ltd.

- Bharat Petroleum Corporation Ltd.

- Hindustan Petroleum Corporation Ltd.

- GAIL (India) Ltd.

- Cairn Oil & Gas (Vedanta)

- Petronet LNG Ltd.

- Adani Total Gas Ltd.

- Nayara Energy Ltd.

- ONGC Videsh Ltd.

- Oil and Natural Gas Services (OVL)

- Larsen & Toubro - Hydrocarbon

- Schlumberger India

- Halliburton India

- Baker Hughes India

- Jindal Drilling & Industries Ltd.

- Essar Oil & Gas Exploration & Production

- HPCL-Mittal Energy Ltd.

- Gujarat State Petroleum Corporation (GSPC)

- Numaligarh Refinery Ltd.

- Chennai Petroleum Corporation Ltd.

- Mangalore Refinery & Petrochemicals Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening domestic E&P licensing rounds

- 4.2.2 Surge in gas-based industrial clusters

- 4.2.3 Expansion of city-gas distribution (CGD) networks

- 4.2.4 Rising private investments in refinery upgrades

- 4.2.5 Digital oil-field adoption for mature basins

- 4.2.6 Methane-slip abatement mandates

- 4.3 Market Restraints

- 4.3.1 Feedstock volatility under Indirect Tax regime

- 4.3.2 Slow land-acquisition for trunk pipelines

- 4.3.3 High breakeven of deep-water prospects

- 4.3.4 ESG-driven capital flight from fossil assets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porter's Five Forces

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Suppliers

- 4.11.3 Bargaining Power of Buyers

- 4.11.4 Threat of Substitutes

- 4.11.5 Intensity of Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Oil and Natural Gas Corporation (ONGC)

- 6.4.2 Oil India Limited

- 6.4.3 Reliance Industries Ltd.

- 6.4.4 Indian Oil Corporation Ltd.

- 6.4.5 Bharat Petroleum Corporation Ltd.

- 6.4.6 Hindustan Petroleum Corporation Ltd.

- 6.4.7 GAIL (India) Ltd.

- 6.4.8 Cairn Oil & Gas (Vedanta)

- 6.4.9 Petronet LNG Ltd.

- 6.4.10 Adani Total Gas Ltd.

- 6.4.11 Nayara Energy Ltd.

- 6.4.12 ONGC Videsh Ltd.

- 6.4.13 Oil and Natural Gas Services (OVL)

- 6.4.14 Larsen & Toubro - Hydrocarbon

- 6.4.15 Schlumberger India

- 6.4.16 Halliburton India

- 6.4.17 Baker Hughes India

- 6.4.18 Jindal Drilling & Industries Ltd.

- 6.4.19 Essar Oil & Gas Exploration & Production

- 6.4.20 HPCL-Mittal Energy Ltd.

- 6.4.21 Gujarat State Petroleum Corporation (GSPC)

- 6.4.22 Numaligarh Refinery Ltd.

- 6.4.23 Chennai Petroleum Corporation Ltd.

- 6.4.24 Mangalore Refinery & Petrochemicals Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment