|

시장보고서

상품코드

2066597

인도의 배터리 에너지 저장 시스템(BESS) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Battery Energy Storage System (BESS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

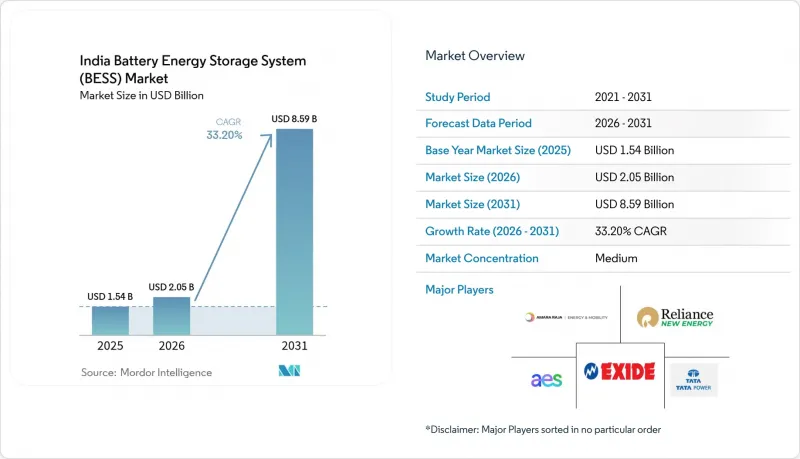

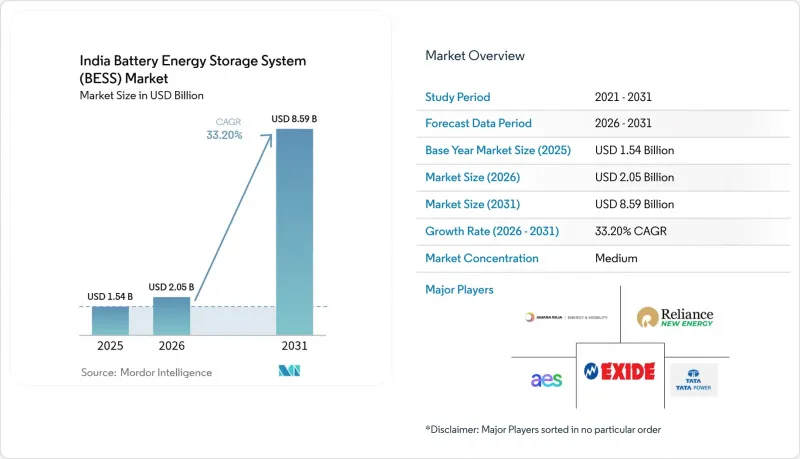

Mordor Intelligence에 의하면, 인도의 배터리 에너지 저장 시스템(BESS) 시장 규모는 2025년에 15억 4,000만 달러로 평가되었고, 2026년 20억 5,000만 달러로 추정되고, 2031년까지 85억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 33.2%를 나타낼 전망입니다.

본 보고서는 배터리 유형별(리튬이온, 납축전지, 흐름전지, 나트륨이온전지 등), 연결 방식별(계통 연계형 및 독립형), 구성 요소별(배터리 팩 및 랙, 에너지 관리 소프트웨어 등), 에너지 용량 범위별(10 MWh 미만, 10-100 MWh, 500 MWh 이상 등), 그리고 최종 사용자 용도별(전력 회사, 상업 및 산업용, 주거용)로 분류되어 있습니다.

인도의 배터리 에너지 저장 시스템(BESS) 시장 동향 및 분석

리튬 이온 배터리 비용의 감소

중국의 기가팩토리가 생산을 확대하고 양극재의 화학 성분이 개선됨에 따라, 인산철 리튬 배터리 가격은 2024년 2분기에 kWh당 89달러까지 하락하여 2023년 수준보다 14% 낮아졌습니다. 이러한 하락으로 인해 100 MWh 규모의 유틸리티 프로젝트에 대한 설비 투자액은 2022년 4,000만 달러에서 2024년에는 약 3,000만 달러로 감소했으며, 이용률이 높은 지역에서는 균등화 저장 비용이 1 kWh당 5 루피 미만의 수준으로 떨어졌습니다. 각 개발사는 CATL 및 BYD와 수년에 걸친 공급 계약을 체결해 놓았으며, 이는 2024년 수입 셀의 68%를 차지하고 있어 단기 프로젝트는 가격 급등의 영향을 덜 받게 됩니다. LFP의 6,000회 사이클 수명은 25년짜리 전력구매계약(PPA)과 일치하여, 수명 중간에 발생할 수 있는 교체 위험을 최소화합니다. 리튬 탄산염은 2024년 초 톤당 8만 5,000달러에 달했다가 1만 2,000달러까지 하락했으나, 현재 인도의 입찰 대부분에는 원자재 가격 변동을 헤지하기 위한 지수 연동 조항이 포함되어 있습니다.

정부의 VGF 및 PLI 인센티브

전력부가 2023년 6월에 시작한 ‘Viability Gap Funding(VGF)’는 대상 독립형 BESS의 설비 투자액의 최대 40%를 한도로 하는 일시적인 보조금을 제공하고 있으며, 1MW당 6.6 카롤 루피의 상한선이 설정되어 있습니다. 2024년 9월까지 이 제도는 8개 프로젝트에 대해 총 1,200 MWh(총액 4,800 카롤 루피)의 보조금을 승인했으며, 5억 8,000만 달러 규모의 민간 자본 투자를 촉진했습니다. 이와 병행하여, 첨단 화학 배터리를 대상으로 하는 PLI 프로그램에서는 현지 부가가치율 50% 및 최소 생산 능력 5GWh를 조건으로, 5년 동안 매출액의 6%에 해당하는 인센티브가 제공됩니다. Reliance, Ola Electric, Rajesh Exports는 2024년에 총 50 GWh 규모의 수주를 확보했으며, 2025년 하반기 생산 개시를 목표로 하고 있습니다. 이러한 조치로 인해 수입 셀과 국산 셀 간의 착륙 비용 격차는 2023년 22%에서 2027년까지 8%로 축소될 전망입니다.

자산군 및 수수료 상한에 관한 규제상의 모호성

비용 회수 규정은 주마다 다르며, BESS를 발전의 한 형태로 분류하는 주도 있고, 송전의 한 형태로 분류하는 주도 있습니다. BESS가 태그가 부착된 송전에 관여하는 경우, 수익은 지출 후 12-18개월 후에 책정되는 규제 요금에 좌우되게 되며, 이는 안정적인 현금 흐름을 추구하는 주식 투자자들을 멀어지게 하는 요인이 되고 있습니다. 국가 지침안에서는 원가 가산 방식의 요금을 적용하는 독립된 자산 등급의 신설이 제안되었으나, 2024년 말 시점에서 최종 규정은 여전히 미정이었습니다. SECI의 요금 상한선(1kWh당 5.50-6.00 루피)은 가중평균자본비용이 11%를 초과할 경우 수익을 압박합니다. 금융 기관은 DSCR(부채 상환 커버리지 비율)을 1.4배 이상으로 요구하고 있으며, 이는 kWh당 6.50 루피에 가까운 손익분기점 요금을 의미합니다. 우타르프라데시 주, 비하르 주, 서벵골 주에서는 송전료 및 뱅킹 요금을 명확히 하는 BESS 관련 명령이 아직 발표되지 않아 불확실성이 지속되고 있습니다.

부문별 분석

2025년 기준으로 리튬 이온 배터리가 설치 용량의 92.15%를 차지했으며, 그중 LFP가 75%를 차지했습니다. 이는 6,000 사이클의 수명과 사막 기후에서 매우 중요한 고유한 열적 안정성 덕분입니다. 개발 사업자가 에너지 밀도보다 수명 주기 비용을 우선시한 결과, NMC 시장 점유율은 17%로 떨어졌습니다. 리튬 티타네이트는 초고속 응답이 요구되는 시장을 겨냥한 틈새 선택지로 1% 미만의 점유율을 유지하고 있지만, 납산 배터리는 1,500회 사이클의 수명으로는 더 이상 설비 투자 절감분을 상쇄할 수 없게 되어 점유율이 4.2%로 하락했습니다. 흐름 전지와 나트륨 이온 전지 시장 점유율을 합치면 2.6%이지만, 비용이 낮아지면 장시간 축전이 가능해질 가능성이 있습니다.

가격 하락에 따라 인도의 배터리 에너지 저장 시스템 시장에서 리튬 이온 배터리가 주도적인 입지를 공고히할 것으로 예상되지만, Reliance의 50 MWh 바나듐 유닛과 같은 시범 규모의 흐름형 배터리가 계절별 에너지 저장의 경제성을 검증하고 있습니다. 개발업체들은 수동식 공랭 방식을 통해 시스템 전체 비용을 12-15% 절감할 수 있다는 점에서 LFP를 선호하고 있습니다. 또한, 리튬 이온 배터리의 모듈성은 건설 기간을 단축시켜 SECI의 엄격한 가동 개시 일정을 충족하는 데 중요한 요소가 되고 있습니다.

Off-grid 및 마이크로그리드의 도입은 통신탑, 광산, 도서 지역의 송전망에서 디젤 발전기가 태양광 발전과 에너지 저장을 결합한 하이브리드 시스템으로 대체됨에 따라 연평균 36.9%의 성장률을 보일 것으로 전망됩니다. Bharti Airtel이 2,500곳에 이 시스템을 도입한 결과, 2024년에는 1,800만 리터의 디젤 연료를 절약하고 운영 비용(OPEX)을 140카롤 루피 절감했습니다. 그렇긴 하지만, SECI 입찰 및 부대 서비스에 따른 수익에 힘입어 2025년 발전 용량의 78.30%는 여전히 계통 연계형 시스템이 차지하고 있습니다. 가상 발전소(VPP) 소프트웨어를 통해 소규모 시스템을 통합하여 전력망 서비스에 활용할 수 있게 됨에 따라, 인도의 배터리 시장은 점차 분산형 자산으로 전환될 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the india battery energy storage system market size was valued at USD 1.54 billion in 2025 and estimated to grow from USD 2.05 billion in 2026 to reach USD 8.59 billion by 2031, at a CAGR of 33.2% during the forecast period (2026-2031).

This report is Segmented by Battery Type (Lithium-Ion, Lead-Acid, Flow Battery, Sodium-Ion, and More), Connection Type (On-Grid and Off-Grid), Component (Battery Pack and Racks, Energy Management Software, and More), Energy Capacity Range (Below 10 MWh, 10 To 100 MWh, Above 500 MWh, and More), and End-User Application (Utility, Commercial and Industrial, and Residential).

India Battery Energy Storage System (BESS) Market Trends and Insights

Declining Lithium-Ion Battery Costs

Lithium iron phosphate cell prices fell to USD 89 per kWh in Q2 2024, 14% below the 2023 level, after Chinese gigafactories ramped up their output and cathode chemistries improved. The drop cut the capex of a 100 MWh utility project from USD 40 million in 2022 to about USD 30 million in 2024, pushing levelized storage costs below INR 5 per kWh in high-utilization nodes. Developers have locked in multi-year supply contracts with CATL and BYD, covering 68% of imported cells in 2024, thereby insulating near-term projects from price spikes. LFP's 6,000-cycle life aligns with 25-year PPAs, minimizing mid-life replacement risk. Although lithium carbonate hit USD 85,000 per tonne in early 2024 before easing to USD 12,000, most Indian bids now include indexation clauses that hedge raw-material volatility.

Government VGF & PLI Incentives

The Ministry of Power's Viability Gap Funding, launched in June 2023, offers a one-time grant up to 40% of the eligible standalone BESS capex, capped at INR 6.6 crore per MW. By September 2024, the scheme had sanctioned 1,200 MWh across eight projects, valued at INR 4,800 crore, catalyzing USD 580 million of private equity investment. In parallel, the PLI program for advanced-chemistry cells provides a 6% sales incentive for five years, contingent on 50% local value addition and 5 GWh minimum capacity; Reliance, Ola Electric, and Rajesh Exports secured 50 GWh of awards in 2024 with first production targeted for late 2025. These levers shrink the landed-cost differential between imported and domestic cells from 22% in 2023 to a projected 8% by 2027.

Asset-Class & Tariff-Cap Regulatory Ambiguity

Cost-recovery rules vary by state, with some classifying BESS as a form of generation, while others classify it as a form of transmission. Where BESS is involved in tagged transmission, returns depend on regulated tariffs set 12-18 months after expenditure, which deters equity investors who seek stable cash flows. Draft national guidelines proposed a separate asset class with cost-plus tariffs, but the final rules were still pending as of late 2024. SECI tariff caps, between INR 5.50 and INR 6.00 per kWh, squeeze returns when the weighted average cost of capital exceeds 11%. Lenders request DSCR above 1.4x, implying breakeven tariffs closer to INR 6.50 per kWh. Uncertainty persists in Uttar Pradesh, Bihar, and West Bengal, where no BESS orders clarify wheeling or banking charges.

Other drivers and restraints analyzed in the detailed report include:

- 500 GW Renewables Target Creates Storage Gap

- Mandatory Energy Storage Obligation for DISCOMs

- Import-Heavy Battery Supply Chain Raises Capex

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion batteries held 92.15% of the installed capacity in 2025, with LFP accounting for 75% due to their 6,000-cycle life and intrinsic thermal stability, which is critical for desert climates. NMC's share slipped to 17% as developers prioritized lifecycle cost over energy density. Lithium titanate remains a niche option under 1% for ultra-fast response markets, while lead-acid fell to 4.2% because its 1,500-cycle life no longer offsets capital expenditure savings. Flow and sodium-ion chemistries together make up 2.6% but offer long-duration potential once costs fall.

As prices drop, the Indian battery energy storage systems market expects lithium-ion to cement its lead, though pilot flow batteries, such as Reliance's 50 MWh vanadium unit, test seasonal storage economics. Developers favor LFP because passive air cooling reduces balance-of-system spend by 12-15%. Lithium-ion's modularity also speeds construction timelines, a key factor in meeting SECI's tight commissioning schedules.

Off-grid and microgrid installations are projected to grow at a 36.9% annual rate as telecom towers, mines, and island grids replace diesel generators with solar-plus-storage hybrids. Bharti Airtel's 2,500-site rollout saved 18 million liters of diesel in 2024 and reduced operating expenses (opex) by INR 140 crore. Nevertheless, on-grid systems still comprise 78.30% of the 2025 capacity, driven by SECI tenders and ancillary services revenues. The Indian battery energy storage systems market balance is expected to tilt gradually toward distributed assets as virtual power plant software enables the aggregation of smaller systems into grid services.

List of Companies Covered in this Report:

- AES Corporation

- Tata Power Renewable Energy Ltd.

- Exide Energy Solutions Ltd.

- Amara Raja Energy & Mobility Ltd.

- Reliance New Energy Ltd.

- Adani Energy Solutions Ltd.

- JSW Energy Ltd.

- Fluence Energy Inc.

- Hitachi Energy India Ltd.

- Delta Electronics India Pvt Ltd.

- Panasonic Holdings Corp.

- LG Energy Solution Ltd.

- BYD Co. Ltd.

- CATL

- Toshiba Corporation

- Sterling & Wilson Energy Storage

- Siemens Energy India

- GE Vernova (Grid Solutions)

- Sungrow Power Supply Co. (India)

- NEC Energy (India JV)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining lithium-ion battery costs

- 4.2.2 Government VGF & PLI incentives

- 4.2.3 500 GW renewables target creates storage gap

- 4.2.4 Mandatory Energy Storage Obligation for DISCOMs

- 4.2.5 Surge of multi-hour standalone BESS tenders

- 4.2.6 Peak-tariff arbitrage demand from C&I & data centers

- 4.3 Market Restraints

- 4.3.1 Asset-class & tariff-cap regulatory ambiguity

- 4.3.2 Import-heavy battery supply chain raises capex

- 4.3.3 Tender undersubscription & execution delays

- 4.3.4 Geopolitical critical-minerals supply risks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO))

- 5.1.2 Lead-acid

- 5.1.3 Flow Battery (Vanadium Redox, Zinc-Bromine)

- 5.1.4 Sodium-ion

- 5.1.5 Other Battery Technologies (NiCd, Hybrid Super-capacitors)

- 5.2 By Connection Type

- 5.2.1 On-Grid (Utility Interconnected)

- 5.2.2 Off-Grid (Micro-Grid, Hybrid)

- 5.3 By Component

- 5.3.1 Battery Pack and Racks

- 5.3.2 Power Conversion System (PCS)

- 5.3.3 Energy Management Software (EMS)

- 5.3.4 Balance-of-Plant and Services

- 5.4 By Energy Capacity Range

- 5.4.1 Below 10 MWh

- 5.4.2 10 to 100 MWh

- 5.4.3 100 to 500 MWh

- 5.4.4 Above 500 MWh

- 5.5 By End-user Application

- 5.5.1 Utility

- 5.5.2 Commercial and Industrial

- 5.5.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 AES Corporation

- 6.4.2 Tata Power Renewable Energy Ltd.

- 6.4.3 Exide Energy Solutions Ltd.

- 6.4.4 Amara Raja Energy & Mobility Ltd.

- 6.4.5 Reliance New Energy Ltd.

- 6.4.6 Adani Energy Solutions Ltd.

- 6.4.7 JSW Energy Ltd.

- 6.4.8 Fluence Energy Inc.

- 6.4.9 Hitachi Energy India Ltd.

- 6.4.10 Delta Electronics India Pvt Ltd.

- 6.4.11 Panasonic Holdings Corp.

- 6.4.12 LG Energy Solution Ltd.

- 6.4.13 BYD Co. Ltd.

- 6.4.14 CATL

- 6.4.15 Toshiba Corporation

- 6.4.16 Sterling & Wilson Energy Storage

- 6.4.17 Siemens Energy India

- 6.4.18 GE Vernova (Grid Solutions)

- 6.4.19 Sungrow Power Supply Co. (India)

- 6.4.20 NEC Energy (India JV)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment