|

시장보고서

상품코드

2066632

인도의 지붕재 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

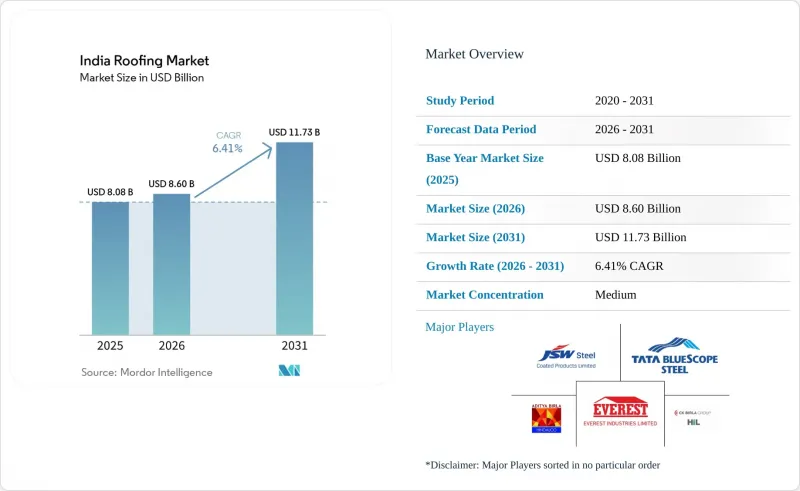

Mordor Intelligence에 의하면, 인도의 지붕재 시장 규모는 2025년 80억 8,000만 달러로 평가되었습니다. 2026년에는 86억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 6.41%로 성장을 지속하여, 2031년에는 117억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 자재 유형(아스팔트 슁글, 점토·콘크리트 기와 등), 시공 유형(신축, 지붕 재시공·개보수), 용도(주택, 상업시설, 산업 시설, 공공시설, 기타) 및 지역(북인도, 남인도, 서인도, 동·북동인도)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 지붕재 시장 동향 및 분석

가처분 소득 증가와 중산층의 확대

가처분 소득 증가로 인해 주택 소유자들은 내구 연한 연장과 냉방비 절감을 기대할 수 있는 고급 방수 시트에 대한 수요를 높이고 있습니다. 정부의 PMAY 프로그램은 도시 지역에서 1.18 crore 가구, 농촌 지역에서 2.95 crore 가구에 주택을 공급함으로써, 개보수 준비가 완료된 대규모 기반을 조성했습니다. 현재 2급 및 3급 도시에서는 열가소성 폴리올레핀(TPO)이나 EPDM 막이 일반 아스팔트 시트를 대체하는 사양이 강화된 프로젝트의 비중이 확대되고 있습니다. 각 제조업체는 이러한 잠재적 수요를 확보하기 위해 유통업체에 대한 교육을 강화하고 있는 반면, 금융기관은 비록 가격이 비싸지만 내구성이 뛰어난 시스템의 도입을 용이하게 해주는 합리적인 할부 결제 플랜의 시범 도입을 추진하고 있습니다.

정부의 인프라 구축 이니셔티브(스마트 시티 미션, PMAY)

PMAY의 표준화된 지붕 공사 템플릿을 통해, 규모의 경제를 활용하는 제조업체는 자동 롤 성형 라인에 대한 투자 비용을 회수할 수 있게 됩니다. 이와 동시에, 스마트 시티 프로젝트에서는 그린 빌딩 평가 기준이 도입되어, 이에 따라 쿨 루프용 안료와 태양광 발전에 대응하는 고정 장치가 보급되고 있습니다. 기후대(습도가 높은 연안 지역, 건조한 내륙 지역, 혹은 온대 북부 등)에 맞추어 사양을 현지화할 수 있는 공급업체는 주 정부 기관으로부터 지속적으로 수주를 따내고 있습니다. 따라서 대규모 주택 건설과 스마트 도시 인프라의 융합은 인도의 지붕재 시장에 여러 가지 예측 가능한 수익원을 가져다줄 뿐만 아니라, 최종 사용자에 대한 보조금 활용 현황을 추적하기 위한 디지털 판매 채널 강화에 대한 동기를 부여하고 있습니다.

위조 및 규격 미달 자재의 만연

비공식 유통 채널에서 판매되는 저가 지붕용 롤의 최대 30%가 IS 15965 인장 시험을 통과하지 못해 소비자의 신뢰를 훼손하고 평균 판매 가격을 끌어내리고 있습니다. 위조 로고가 명품 브랜드를 사칭함에 따라 보증 청구 건수가 급증하고 있으며, 정식 기업들은 홀로그램 라벨이나 QR 코드를 통한 진위 확인에 더 많은 비용을 지출할 수밖에 없는 실정입니다. 체계적인 사업자들은 판매점이 로트 번호를 스캔하여 즉시 진위 여부를 확인할 수 있는 모바일 앱을 활용하고 있으며, 이를 통해 재주문을 확보하고 있습니다. 규제 당국의 단속은 증가하는 추세이지만, 주마다 시행 상황에 차이가 있어 규제를 준수하는 기업들은 비용 면에서 3-5%의 불이익을 감수해야 합니다.

부문별 분석

2025년, 금속 지붕재는 인도 지붕재 시장 점유율의 26.5%를 차지했으며, 산업용 창고, 상업용 건물 및 사전 제작 건축물(PEB) 수요에 힘입어 다른 모든 소재 부문을 앞질렀습니다. 인도 지붕 업계 전반에서 금속 지붕 시스템은 시공의 신속성, 긴 수명, 외관뿐만 아니라 구조적 신뢰성이 중시되는 대스팬 용도에서 높은 수용성을 보이는 등의 이점을 계속해서 누리고 있습니다. 대형 공급업체의 판매망 확대도 중요한 요소입니다. 라스트 마일까지공급망이 넓을수록, 브랜드화된 도장 강판이 여전히 현지 조달 비중이 높고 지붕재 선정에 큰 영향을 미치는 비대도시권 건설 시장에 더 쉽게 침투할 수 있기 때문입니다. 남인도 주택 건축, 특히 경사진 지붕이 지역 건축 관행의 일부로 자리 잡은 지역에서는 점토 기와와 콘크리트 기와가 여전히 확고한 위치를 차지하고 있습니다. 그럼에도 불구하고, 내식성, 시공 속도, 그리고 유지보수 비용의 절감 효과가 전통적인 외관보다 더 중요하게 여겨지는 상업시설 및 공공시설 프로젝트에서는 금속 지붕 시스템 시장 점유율이 꾸준히 확대되고 있습니다.

아스팔트계/개질 아스팔트계 방수 시트는 2031년까지 연평균 성장률(CAGR) 8.20%를 기록하며 성장할 것으로 예상되며, 인도의 지붕재 시장에서 가장 빠르게 성장하는 제품군이 될 전망입니다. 이러한 성장은 방수 성능이 단순한 선택 사항이 아닌 필수 요건이 되는 평지붕 상업용 건물, 대규모 소매 프로젝트, 물류 단지 및 공공시설과 관련이 있습니다. 열가소성 폴리올레핀(TPO), 에틸렌·프로파일렌·디엔 단량체(EPDM), 폴리염화비닐(PVC) 등의 단층 막도, 단열 성능과 유지보수 성능이 중요시되는 고사양 상업용 지붕 분야에서 그 존재감을 높여가고 있습니다. 목재 지붕은 여전히 고급 용도나 틈새 시장에 한정되어 있습니다. 한편, 파형 섬유 시멘트, 비가소화 폴리염화비닐(UPVC), 폴리카보네이트 제품은 저가 시장에서 농촌 지역, 농업용 및 임시 구조물에 대한 수요를 지속적으로 충족시키고 있습니다. 따라서 인도의 지붕재 시장에서는 양극단에서 소재 구성이 확대되고 있으며, 사양 중심의 프로젝트에서는 고성능 프리미엄 제품이 성장하고 있는 반면, 초기 비용의 저렴함이 여전히 우선시되는 분야에서는 기본적인 대체 제품이 안정적인 수요를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the india roofing market size is expected to grow from USD 8.08 billion in 2025 to USD 8.6 billion in 2026 and is forecast to reach USD 11.73 billion by 2031 at 6.41% CAGR over 2026-2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, and More), by Construction Type (New Construction, Reroofing and Replacement), by Application (Residential, Commercial, Industrial, Institutional, Others), and by Geography (North India, South India, West India, East and North East India). The Market Forecasts are Provided in Terms of Value (USD).

India Roofing Market Trends and Insights

Rising Disposable Income & Middle-Class Expansion

Higher disposable income is steering homeowners toward premium membranes that promise extended service life and lower cooling costs. The government's PMAY program has delivered 1.18 crore homes under its urban component and 2.95 crore under its rural arm, creating a large installed base ready for upgrades. Tier-2 and Tier-3 cities now account for a growing share of specification-rich projects where thermoplastic polyolefin (TPO) and EPDM membranes displace commodity asphalt sheets. Manufacturers are amplifying dealer training to capture this latent demand, while financiers are piloting easy EMI plans that ease the adoption of costlier but more durable systems.

Government Infrastructure Initiatives (Smart Cities Mission, PMAY)

PMAY's standardized roofing templates allow scale-driven manufacturers to amortize investments in automated roll-forming lines. Simultaneously, Smart Cities projects impose green-building scorecards that popularize cool-roof pigments and solar-ready fasteners. Vendors able to localize specifications for climate zones, humid coastal, dry arid, or temperate northern win repeat orders from state agencies. The convergence of mass housing and smart municipal assets, therefore, gives the India roofing market multiple predictable revenue streams and an incentive to upgrade digital sales channels that track subsidy availment for end users.

Counterfeit/Sub-Standard Materials Prevalence

Up to 30% of low-ticket roofing rolls in informal retail channels fail IS 15965 tensile tests, eroding consumer trust and compressing average selling prices. Warranty claims surge when counterfeit logos masquerade as premium brands, forcing genuine companies to spend more on hologram labels and QR-based verification. Organized players leverage mobile apps that allow dealers to scan batch numbers and instantly confirm authenticity, thereby locking in repeat orders. Regulatory raids, though increasing, remain uneven across states, leaving compliance-paying firms at a 3-5% cost disadvantage.

Other drivers and restraints analyzed in the detailed report include:

- Solar-Rooftop Subsidies are Accelerating Metal Sandwich Demand

- Climate-Resilience Mandates in Coastal States

- Imported Bitumen & Metal Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal Roofing held 26.5% of the India roofing market share in 2025, keeping it ahead of all other material categories, driven by industrial warehousing, commercial buildings, and Pre-Engineered Buildings (PEBs). Across the India roofing industry, metal systems continue to benefit from faster installation, long service life, and stronger acceptance in large-span applications where structural reliability matters as much as appearance. The dealer footprint of large suppliers also matters because broader last-mile reach helps branded coated steel move into non-metro construction markets where local procurement still drives many roofing decisions. Clay and concrete tiles still retain a clear place in South India residential construction, especially where sloped roofs are part of local building practice. Even so, metal systems are steadily taking share in commercial and institutional projects where corrosion resistance, speed, and lower maintenance carry more weight than traditional appearance.

Bituminous/Modified Bitumen Membranes are forecast to grow at a 8.20% CAGR through 2031, making them the fastest-growing material line in the India roofing market. This growth is tied to flat-roof commercial buildings, organized retail projects, logistics parks, and institutional assets where waterproofing performance is a hard requirement rather than a discretionary feature. Single-ply membranes such as Thermoplastic Polyolefin (TPO), Ethylene Propylene Diene Monomer (EPDM), and Polyvinyl Chloride (PVC) are also becoming more visible in higher-specification commercial roofs where thermal and maintenance performance have gained importance. Wood roofing remains limited to premium and niche uses. At the same time, corrugated fiber cement, Unplasticized Polyvinyl Chloride (UPVC), and polycarbonate products continue to serve rural, agricultural, and temporary-structure demand at lower price points. In the India roofing market, the material mix is therefore widening at both ends, with premium performance products growing in specification-led projects and basic alternatives holding steady where upfront affordability still dominates.

List of Companies Covered in this Report:

- Tata BlueScope Steel

- Hindalco Industries Ltd

- JSW Steel Coated Products

- CK Birla Group (HIL Ltd)

- Everest Industries Ltd

- Bansal Roofing Products Ltd

- Metecno India Pvt Ltd

- Indian Roofing Industries Pvt Ltd

- Visaka Industries Ltd

- Ramco Industries Ltd

- Onduline India

- Interarch Building Products

- Saint-Gobain India Pvt Ltd

- Supreme Industries Ltd

- Bhushan Power & Steel Ltd

- Peninsular Roofing Products

- Vijay Roofing Systems

- JSW Everglow (JSW Steel)

- LYSAGHTA(R) Roofing Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising disposable income & middle-class expansion

- 4.2.2 Rapid urbanization & construction boom

- 4.2.3 Government infrastructure initiatives (Smart Cities Mission, PMAY)

- 4.2.4 Solar-rooftop subsidies accelerating metal sandwich demand

- 4.2.5 Climate-resilience mandates in coastal states

- 4.2.6 State-level "cool roof" policies for urban heat mitigation

- 4.3 Market Restraints

- 4.3.1 Counterfeit / sub-standard materials prevalence

- 4.3.2 Skilled-labour shortage

- 4.3.3 Imported bitumen & metal price volatility (? depreciation)

- 4.3.4 Municipal approval delays for innovative systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North India

- 5.4.2 South India

- 5.4.3 West India

- 5.4.4 East and North East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tata BlueScope Steel

- 6.4.2 Hindalco Industries Ltd

- 6.4.3 JSW Steel Coated Products

- 6.4.4 CK Birla Group (HIL Ltd)

- 6.4.5 Everest Industries Ltd

- 6.4.6 Bansal Roofing Products Ltd

- 6.4.7 Metecno India Pvt Ltd

- 6.4.8 Indian Roofing Industries Pvt Ltd

- 6.4.9 Visaka Industries Ltd

- 6.4.10 Ramco Industries Ltd

- 6.4.11 Onduline India

- 6.4.12 Interarch Building Products

- 6.4.13 Saint-Gobain India Pvt Ltd

- 6.4.14 Supreme Industries Ltd

- 6.4.15 Bhushan Power & Steel Ltd

- 6.4.16 Peninsular Roofing Products

- 6.4.17 Vijay Roofing Systems

- 6.4.18 JSW Everglow (JSW Steel)

- 6.4.19 LYSAGHTA(R) Roofing Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment