|

시장보고서

상품코드

2066693

아시아태평양의 폴리우레탄 접착제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Polyurethane Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

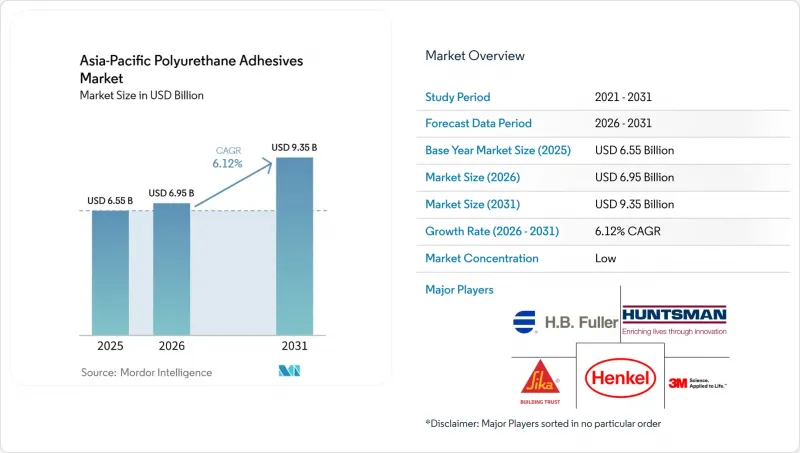

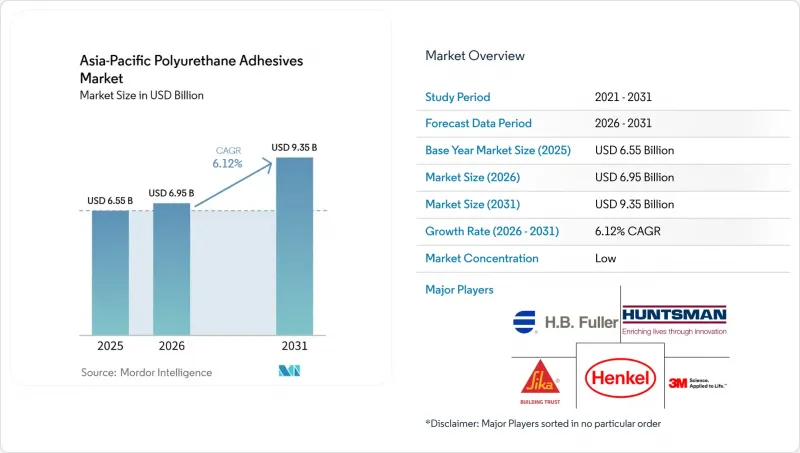

Mordor Intelligence에 의하면, 아시아태평양의 폴리우레탄 접착제 시장 규모는 2025년 65억 5,000만 달러로 평가되었습니다. 2026년에는 69억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 6.12%로 성장을 지속하여, 2031년에는 93억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 최종 사용자 산업별(항공우주, 자동차, 의료, 포장 등), 기술별(핫멜트, 반응형, 용제계, UV 경화형, 수성), 지역별(호주, 중국, 인도, 인도네시아, 일본, 말레이시아, 싱가포르, 한국, 태국, 기타 아시아태평양)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 폴리우레탄 접착제 시장 동향 및 분석

포스트 코로나 시대에 건축 외피 개보수 공사의 급증

소유주들이 운영 비용 절감을 추구하고 탄소 중립 목표 달성에 힘쓰는 가운데, 주요 도시의 개보수 예산은 증가 추세를 보이고 있습니다. 중국은 획기적인 조치로 저탄소 건설에 무려 5,500억 달러를 투자했으며, 그 결과 특히 단열 패널 접착 및 방수 시트 분야에서 폴리우레탄 수요가 증가했습니다. 싱가포르의 ‘육상 교통 마스터플랜 2040’에 따라, 신설되는 철도역에는 내화성 경질 발포 접착제가 채택되고 있습니다. 이러한 접착제는 상온 경화 시에도 노후화된 강재나 콘크리트에 접착될 수 있도록 설계되었습니다. 습기 경화형 제품은 표면의 오염 물질에 대한 내성이 있어 가동 중단 시간을 단축할 수 있기 때문에 시장에서 빠르게 보급되고 있습니다. 이러한 추세는 인도의 스마트시티 개발 지역이나 일본의 노후화된 고층 빌딩에서도 볼 수 있습니다. 그러나 저렴한 중국산 MDI의 유입이 과제로 대두되고 있으며, 이는 컨버터의 이익률을 압박할 가능성이 있습니다. 그럼에도 불구하고, 독자적인 프라이머와 현장 교육을 결합한 해당 부문공급업체들은 가격 압박 속에서도 시장 점유율을 확보하는 데 성공하고 있습니다.

전기자동차 주행 거리 연장을 위한 자동차 경량화 추진

자동차 제조업체들은 기존의 리벳이나 에폭시 수지 대신 2액형 폴리우레탄을 점점 더 많이 채택하고 있습니다. 이러한 폴리우레탄은 셀 모듈의 접착, 알루미늄 하우징의 밀봉, 그리고 열전도성이 있는 틈새 충전재의 형성에 탁월합니다. H.B. 풀러사의 ‘UR4515GF’는 70°C에서 120분간 경화시킨 후, E-코팅 강판 위에서 20.05 MPa의 랩 전단 강도를 달성하여 전기자동차(EV) 자동 조립 라인에 최적입니다. 2025년에 출시된 헨켈의 ‘Technomelt PUR 6260 ECO’는 60% 이상이 재생 가능한 원료로 구성되어 있으며, 불과 50°C에서 연화되기 때문에 오븐의 에너지 소비를 줄이고 열에 민감한 기판을 보호합니다. OEM 각사가 1회 충전당 주행 거리를 600km 이상으로 늘려가는 가운데, 접착제 대체로의 전환이 두드러지고 있습니다. 또한, 연평균 성장률(CAGR) 7.12%를 기록하며 성장하고 있는 인도의 자동차 부문은 현지 조달 할당 기준을 충족하는 현지 혼합 제조업체들에게 큰 비즈니스 기회를 제공합니다.

가연성 코어 자재에 대한 방화 규제의 강화

건축 분야에서 폴리우레탄계 접착제에 대한 방화 안전 기준이 강화됨에 따라, 시험 부담과 배합상의 제약이 발생하여 시장 성장 억제요인으로 작용하고 있으며, 이로 인해 특정 건축 분야에서의 도입이 지연되고 있습니다. 호주의 AS 5637.1 그룹 번호 제도에 따르면, 접착제 층이 수축하거나 용융된 경우, 본래는 기준을 충족하는 패널 어셈블리라 하더라도 비용이 많이 드는 실규모 화재 시험을 받아야 할 가능성이 있습니다. 한국의 연구진은 수성 폴리우레탄에 인산화 폴리비닐알코올과 마그네슘·알루미늄 층상 이중수산화물을 첨가함으로써, 최대 발열량을 30% 저감시켰으나, 접착 강도는 0.70 MPa 이상을 유지했습니다. 이러한 첨가제는 점도와 비용을 증가시키기 때문에 프로젝트 보험사가 의무화하기 전까지는 도입이 더딘 임베디드니다.

부문별 분석

2025년, 아시아태평양의 폴리우레탄계 접착제 시장 규모 중 포장 분야가 28.24%를 차지했습니다. 이는 스낵 과자, 의약품 및 전자상거래 배송용 봉투에 사용되는 유연 라미네이트 형식이 기여한 결과입니다. 성장의 핵심은 수 초 이내에 기밀 밀봉을 형성하고, 용제계 제품에 비해 에너지 소비를 줄여주는 습기 경화형 반응성 핫멜트입니다. 질소 분위기 하에서 그라비아 인쇄기를 도입한 지역의 라미네이팅 공장에서는 결로로 인한 결함을 방지할 수 있어, 인스턴트 라면 및 조미료용 로트 규모 확대를 뒷받침하고 있습니다. 자동차 분야는 톤수 기준으로는 규모가 작지만, 전기자동차용 배터리 모듈, 경량 차체 패널, 방음 폼 분야에서 2액형 폴리우레탄 및 열가소성 폴리우레탄 필름에 대한 수요가 증가하고 있어 연평균 성장률(CAGR) 6.94%로 성장하고 있습니다. 현재 아시아태평양의 폴리우레탄계 접착제 시장에서는 열전도율 2 W/m*K 이상을 인증받을 수 있고, GB/T 33014 측면 충돌 시험 프로토콜에 부합하는 충돌 시뮬레이션 데이터를 제공할 수 있는 공급업체가 주목받고 있습니다.

건설용 접착제는 단열 개보수 공사의 수혜를 입고 있지만, 중국의 3급 도시에서는 프로젝트 승인이 지연되고 있다는 과제에 직면해 있습니다. 베트남과 인도네시아의 신발 공장에서는 VOC를 90-95% 줄일 수 있는 수성 폴리우레탄 분산액으로의 전환이 진행되고 있습니다. 통기성이 뛰어난 폴리우레탄으로 코팅된 의료용 테이프는 하이드로콜로이드 층과의 호환성이 뛰어나, 말레이시아의 상처 관리 제품 수출을 확대되고 있습니다. 목공 업계에서는 엔지니어드 우드 바닥재에 반응형 핫멜트 접착제를 채택하고 있으며, 클램핑 시간이 50% 단축됨에 따라 새로운 건조로를 도입하지 않고도 생산 라인의 생산 능력을 향상시키고 있습니다. 이러한 틈새 분야들은 포장 및 자동차 산업의 경기 사이클이 둔화되더라도 전반적으로 기초적인 성장을 유지하고 있으며, 아시아태평양의 폴리우레탄계 접착제 시장에서 수요 기반을 폭넓게 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the asia-Pacific polyurethane adhesives market size is expected to grow from USD 6.55 billion in 2025 to USD 6.95 billion in 2026 and is forecast to reach USD 9.35 billion by 2031 at a 6.12% CAGR over 2026-2031.

This report is Segmented by End-User Industry (Aerospace, Automotive, Healthcare, Packaging, and More), Technology (Hot Melt, Reactive, Solvent-Borne, UV Cured Adhesives, and Water-Borne), and Geography (Australia, China, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Thailand, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Polyurethane Adhesives Market Trends and Insights

Surge in Building-Envelope Retrofits Post-COVID Era

As owners pursue lower operating costs and commit to net-zero goals, refurbishment budgets in major cities are on the rise. In a significant move, China invested a whopping USD 550 billion into low-carbon construction, subsequently boosting the demand for polyurethanes, especially in insulation-panel bonding and waterproofing membranes. Under Singapore's Land Transport Master Plan 2040, newly added rail stations are opting for fire-resistant rigid-foam adhesives. These adhesives are designed to bond with aged steel or concrete, even at ambient cure. Moisture-curing grades are flourishing in the market due to their ability to tolerate surface contaminants, thereby reducing downtime. This trend is mirrored in India's smart-city corridors and Japan's aging high-rise buildings. However, the influx of inexpensive Chinese MDI poses a challenge, potentially squeezing margins for converters. Yet, segment suppliers who combine unique primers with on-site training are managing to capture market share, even amidst pricing pressures.

Automotive Lightweighting Push for EV Range Extension

Automakers are increasingly turning to two-component polyurethanes, moving away from traditional rivets and epoxies. These polyurethanes are adept at bonding cell modules, sealing aluminum housings, and creating thermally conductive gap fillers. H.B. Fuller's UR4515GF achieves a lap-shear strength of 20.05 MPa on E-coat steel after a 70 °C, 120-minute cure, making it a perfect fit for automated EV assembly lines. Launched in 2025, Henkel's Technomelt PUR 6260 ECO boasts over 60% renewable feedstock and softens at a mere 50 °C, leading to energy savings in ovens and safeguarding heat-sensitive substrates. With OEMs extending their ranges to exceed 600 km per charge, the shift towards adhesive substitution becomes evident. Furthermore, India's automotive sector, growing at a CAGR of 7.12%, presents lucrative opportunities for local formulators who align with localization quotas.

Fire-Safety Regulatory Scrutiny on Combustible Cores

Heightened fire-safety standards for polyurethane adhesives in construction applications impose testing burdens and formulation constraints that act as a market restraint, slowing adoption in certain building segments. Australia's AS 5637.1 group-number scheme can push an otherwise compliant panel assembly into costly full-scale fire tests if the adhesive layer shrinks or melts. Korean researchers cut peak heat-release rate 30% by adding phosphorylated polyvinyl alcohol plus magnesium-aluminum layered double hydroxides to water-borne polyurethane, yet bonding strength held above 0.70 MPa. Such additives raise viscosity and cost, so adoption lags until mandated by project insurers.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Packaging Shift to High-Performance Laminates

- 3C Electronics Adoption of Low-VOC PUR Hot-Melts

- OEM Qualification Cycles Delaying Tech Substitution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging represented 28.24% of the Asia-Pacific polyurethane adhesives market size in 2025 thanks to flexible-laminate formats used for snacks, pharmaceuticals, and e-commerce mailers. Growth hinges on moisture-curing reactive hot-melts that deliver hermetic seals within seconds and cut energy versus solvent-borne lines. Regional laminate plants that install nitrogen-inerted gravure presses avoid condensation defects, supporting bigger lot sizes for instant noodles and condiments. Automotive uses, although smaller in tonnage, grow at 6.94% CAGR as EV battery modules, lightweight body panels, and acoustic foams demand two-component polyurethanes and thermoplastic polyurethane films. The Asia-Pacific polyurethane adhesives market now prizes suppliers able to certify thermal conductivity >=2 W/m*K and provide crash simulation data that meet GB /T 33014 side-impact protocols.

Construction adhesives benefit from insulation retrofits but face slow project approvals in China's tier-3 cities. Footwear factories in Vietnam and Indonesia convert to water-based polyurethane dispersions that slash VOCs by 90-95%. Medical tapes coated with breathable polyurethane interact well with hydrocolloid layers, expanding wound-care exports from Malaysia. Woodworking taps reactive hot-melts for engineered-wood flooring because clamp times drop 50%, boosting line capacity without new kilns. These niche areas collectively sustain baseline growth even if packaging or automotive cycles soften, keeping demand broad-based within the Asia-Pacific polyurethane adhesives market.

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- BASF

- Dow Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co., Ltd.

- Huntsman Corporation

- ITW Performance Polymers

- Jowat SE

- Kangda New Materials (Group) Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in building-envelope retrofits post-COVID era

- 4.2.2 Automotive lightweighting push for EV range extension

- 4.2.3 E-commerce packaging shift to high-performance laminates

- 4.2.4 3C electronics adoption of low-VOC PUR hot-melts

- 4.2.5 Green-building regulations spurring rigid panel bonding

- 4.3 Market Restraints

- 4.3.1 Volatility in MDI/TDI feedstock prices

- 4.3.2 Fire-safety regulatory scrutiny on combustible cores

- 4.3.3 OEM qualification cycles delaying tech substitution

- 4.4 Value Chain Analysis

- 4.5 Regulatory Analysis

- 4.6 Distribution Channel Analysis

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-user Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 By Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 BASF

- 6.4.5 Dow Inc.

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Hubei Huitian New Materials Co., Ltd.

- 6.4.9 Huntsman Corporation

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat SE

- 6.4.12 Kangda New Materials (Group) Co., Ltd.

- 6.4.13 NANPAO RESINS CHEMICAL GROUP

- 6.4.14 Permabond LLC

- 6.4.15 Pidilite Industries Ltd.

- 6.4.16 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment