|

시장보고서

상품코드

2066696

유럽의 폴리우레탄 접착제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Polyurethane Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

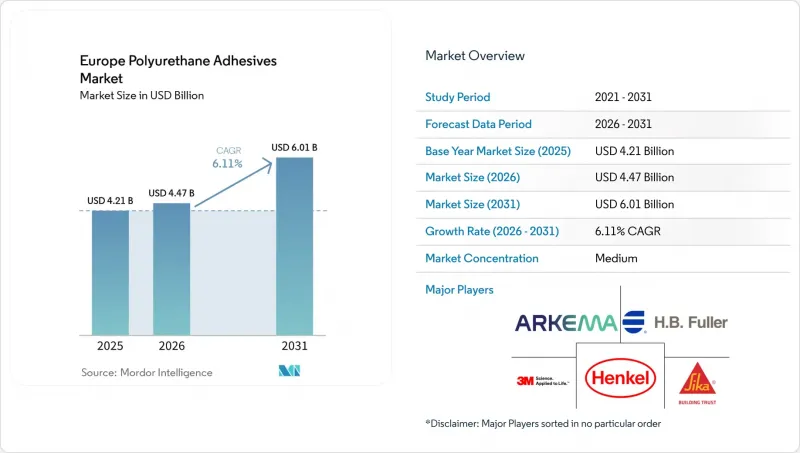

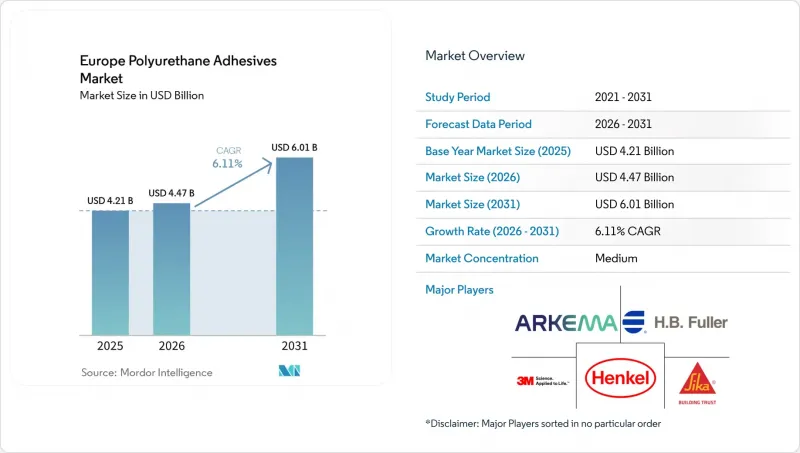

Mordor Intelligence에 의하면, 유럽의 폴리우레탄 접착제 시장 규모는 2025년에 42억 1,000만 달러로 평가되었습니다. 2026년 44억 7,000만 달러에서 2031년까지 60억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.11%를 나타낼 전망입니다.

본 보고서는 최종 사용자 산업별(항공우주, 자동차, 건축 및 건설, 신발·가죽, 목공·문짝 등), 기술별(핫멜트, 반응형, 용제계, UV 경화형, 수성), 지역별(독일, 프랑스, 이탈리아, 러시아, 스페인, 영국, 북유럽 국가, 기타 유럽)으로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 폴리우레탄 접착제 시장 동향 및 분석

자동차 경량화와 구조용 접착의 급속한 성장

유럽에서는 배터리식 전기자동차(BEV)의 생산이 크게 늘어나고 있으며, 전년 대비 뚜렷한 증가세를 보이고 있습니다. 현재 각 BEV에는 내연기관 차량에 비해 훨씬 더 많은 구조용 접착제가 사용되고 있습니다. 독일, 프랑스, 스페인의 기가팩토리가 생산량을 확대함에 따라, 구동용 배터리 접착에 사용되는 반응성 폴리우레탄 수요는 향후 몇 년 동안 전체 자동차 생산량보다 빠른 속도로 증가할 것으로 예측됩니다. 전기자동차 배터리 팩 조립 분야에서는 첨단 폴리우레탄 시스템의 도입이 점점 더 확대되고 있습니다. 이러한 시스템은 기존의 기계식 체결 부품을 대체하면서 구조적 강도와 열전도성을 제공하며, 팩 무게를 대폭 줄이는 데 기여하고 있습니다. 'SikaForce-7888 L30'은 알루미늄과 복합재료의 접합에 있어 그 효과가 입증되어, 현재 독일과 프랑스의 여러 대형 자동차 제조업체에서 채택되고 있습니다. 또한, 에보닉사의 상온 경화형 포팅 컴파운드는 높은 절연 내력을 갖추고 있어, 전기적 절연과 진동 감쇠를 모두 충족시킵니다. 이는 끊임없이 진화하는 자동차 산업에서 최신 폴리우레탄 시스템이 수행하는 중요한 역할을 여실히 보여주고 있습니다.

에너지 효율이 높은 건축 단열재의 의무화

‘건축물의 에너지 성능에 관한 지침’은 신축 건축물에 대해 제로 배출을 의무화하고, 회원국들에게 비주거용 건축물 중 에너지 효율이 가장 낮은 부분을 개보수할 것을 요구하고 있습니다. 파사드 보수 공사에서는 경질 발포 패널을 고정하기 위해 폴리우레탄계 접착제가 사용되고 있는데, 이러한 접착제의 배합은 휘발성 유기 화합물(VOC)을 규제하는 EU의 ‘데코페인트 지침’을 준수해야 합니다. 독일의 인센티브 조치로 인해 단열 파사드에 대한 수요가 크게 증가하면서, 접착제 소비량도 현저히 늘고 있습니다. 가격이 다소 비싼 편임에도 불구하고, 헨켈의 무용제형 ‘파텍스 PL 프리미엄’은 출시 직후 독일 DIY 시장에서 큰 시장 점유율을 차지했습니다. 이는 소비자들이 저배출 제품에 투자하려는 의지가 높다는 것을 보여줍니다. 북유럽의 건축 기준에는 엄격한 U값 요건이 적용되고 있으며, 핀란드의 건축 외피 1제곱미터당 접착제 사용량은 유럽 평균을 상회하고 있습니다. 이는 서유럽의 향후 소비 동향을 보여주는 것으로 보입니다.

디이소시아네이트의 가격 및 공급 변동

아시아 지역의 불가항력으로 인한 가동 중단과 홍해에서의 운송 지연으로 인해, 2025년 1분기에는 토루엔 이소시아네이트의 현물 가격이 두 자릿수 상승을 기록했으며, 유럽의 가공업체들의 원자재 비용은 전 분기 대비 최대 18% 상승했습니다. 계약 가격의 메틸렌디페닐디이소시아네이트도 마찬가지로 가격이 상승했으며, 다우사는 지정학적 혼란에 따른 원자재 가격 급등을 해결하기 위해 2026년 초에 폴리머 분산액의 가격을 폭넓게 인상했습니다. 와커 케미(Wacker Chemie)사가 눙크리츠 공장에서 알파실란계 하이브리드 제품의 생산 능력을 확대한 것은 방향족 이소시아네이트에 대한 의존도를 낮추는 수단이 되고 있지만, 단가가 높기 때문에 그 적용은 고급 용도로만 제한되고 있습니다. 중소규모 배합 제조업체들은 업스트림 공정으로의 통합에 필요한 자본이 부족하기 때문에 시장 공급 변동에 쉽게 영향을 받으며, 현물 가격이 급등할 경우 운전자금이 부족해지는 상황에 처하고 있습니다.

부문별 분석

2025년, 자동차 부문은 유럽의 폴리우레탄 접착제 시장 규모의 23.18%를 차지했습니다. 이는 배터리 팩, 구조용, 내장용 등 모든 분야에서 반응성 시스템이 필요하기 때문입니다. 전기자동차 배터리 접착에는 대량의 접착제가 필요하며, 다우(Dow)사의 ‘VORATRON’ 및 ‘SikaForce’ 플랫폼이 신규 사양의 대부분을 차지했습니다. 전기 및 전자 분야는 여전히 규모는 작지만, 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 6.58%로 가장 높은 성장세를 보일 것으로 예측됩니다. 이는 파워 반도체 모듈이 열 사이클 및 진동으로부터 보호해 주는 폴리우레탄 포팅 컴파운드의 이점을 누리기 때문입니다. 건축 및 건설 부문은 ‘건축물의 에너지 성능에 관한 지침(EPBD)’의 개정에 대응하고 있으며, 의무화된 개보수 공사에서 시장 규모의 상당 부분을 차지하고 있습니다. 유럽에서는 이탈리아와 스페인의 신발 제조업체들이 휘발성 유기 화합물(VOC) 배출량이 적은 수성 분산액을 점점 더 많이 채택하고 있으며, 매년 꾸준한 성장세를 보이고 있습니다. 의료 분야는 틈새 시장이지만, 특히 인슐린 펌프에 널리 사용되는 ‘Loctite AA 3952’와 같은 ISO 10993 인증 등급 제품에서 높은 이익률을 확보하고 있습니다. 수요 동향은 포장, 목공, 항공우주 등 각 분야에 따라 더욱 다양해지고 있으며, 목공 분야에서는 향후 몇 년 동안 습기 경화형 1액형 배합제의 소비량이 현저히 증가할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the europe polyurethane adhesives market size was valued at USD 4.21 billion in 2025 and is estimated to grow from USD 4.47 billion in 2026 to reach USD 6.01 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031).

This report is Segmented by End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Woodworking and Joinery, and More), Technology (Hot Melt, Reactive, Solvent-Borne, UV Cured, and Water-Borne), and Geography (Germany, France, Italy, Russia, Spain, United Kingdom, NORDIC Countries, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Polyurethane Adhesives Market Trends and Insights

Automotive Lightweighting and Structural Bonding Boom

Europe has seen significant growth in battery electric vehicle (BEV) production, with a notable increase compared to the previous year. Each BEV now uses significantly more structural adhesive than internal-combustion vehicles. As gigafactories in Germany, France, and Spain expand their output, the demand for reactive polyurethane in traction-battery bonding is expected to grow at a faster pace than overall automotive production in the coming years. Electric-vehicle battery pack assembly increasingly relies on advanced polyurethane systems. These systems provide structural strength and thermal conductivity while replacing traditional mechanical fasteners, resulting in a notable reduction in pack weight. SikaForce-7888 L30 has gained approval for its effectiveness in aluminum-to-composite joints and is now specified by several major car manufacturers in Germany and France. Additionally, Evonik's ambient-cure potting compounds offer high dielectric strength, addressing both electrical isolation and vibration damping, highlighting the critical role of modern polyurethane systems in the evolving automotive industry.

Energy-Efficient Building Insulation Mandates

The Energy Performance of Buildings Directive mandates zero-emission new constructions and requires member states to renovate the least energy-efficient portion of non-residential buildings. In facade retrofits, polyurethane adhesives are used to secure rigid foam panels, but these formulations must comply with the EU Decopaint Directive, which limits volatile organic compounds (VOCs). Incentives in Germany have significantly increased demand for insulated facades, driving notable growth in adhesive consumption. Despite being priced higher, Henkel's solvent-free Pattex PL Premium has gained a significant share of the German DIY market shortly after its launch, highlighting consumers' willingness to invest in low-emission products. Nordic building codes enforce strict U-value requirements, and Finland's adhesive usage per square meter of building envelope exceeds the European average, indicating potential consumption trends for Western Europe.

Diisocyanate Price and Supply Volatility

Force-majeure outages in Asia and Red Sea shipping delays lifted toluene diisocyanate spot prices by double digits in Q1 2025, raising European converters' input costs by up to 18% quarter-on-quarter. Contract methylene-diphenyl diisocyanate prices moved in tandem, and Dow passed through broad polymer dispersion hikes in early 2026 to counter feedstock inflation amid geopolitical unrest. Wacker Chemie's capacity ramp-up of alpha-silane hybrids at Nunchritz provides a hedge against aromatic-isocyanate dependency, but higher unit costs limit adoption to premium uses. Smaller formulators lack the capital to integrate upstream, leaving them exposed to merchant-supply shocks and squeezing working capital when spot prices spike.

Other drivers and restraints analyzed in the detailed report include:

- EU Green Deal Push for Low- Volatile Organic Compound (VOC), Solvent-Free Systems

- Reactive Polyurethanes in European Medical-Device Assembly

- Tightening REACH Limits on Free NCO Content

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The automotive segment accounted for 23.18% of the Europe Polyurethane Adhesives market size in 2025, as battery pack, structural, and interior applications all require reactive systems. The bonding of electric vehicle batteries required a significant amount of adhesive, with Dow's VORATRON and SikaForce platforms winning most new specifications. Electrical and electronics remain smaller but post the fastest 6.58% CAGR between 2026 and 2031 as power-semiconductor modules benefit from polyurethane potting compounds, which shield them from heat cycling and vibrations. The building and construction sector, responding to the Energy Performance of Buildings Directive (EPBD) recast, represents a significant share of the volume under mandated retrofits. In Europe, footwear manufacturers in Italy and Spain are increasingly adopting water-borne dispersions with low volatile organic compound (VOC) emissions, showing steady annual growth. While healthcare occupies a niche segment, it commands premium margins, especially for ISO 10993-certified grades like Loctite AA 3952, prominently used in insulin pumps. The demand landscape is further diversified by packaging, woodworking, and aerospace sectors, with woodworking expected to see notable consumption of moisture-cure one-component formulations in the coming years.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF

- Beardow Adams

- DELO Industrial Adhesives

- Dow Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- MAPEI S.p.A.

- Momentive Performance Materials

- PARKER HANNIFIN CORP

- Sika AG

- Soudal Holding N.V.

- Tesa Tapes (India) Private Limited

- ThreeBond Europe

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive lightweighting and structural bonding boom

- 4.2.2 Energy-efficient building insulation mandates

- 4.2.3 EU Green Deal push for low-VOC, solvent-free systems

- 4.2.4 Modular timber construction adoption

- 4.2.5 Reactive PURs in European medical-device assembly

- 4.3 Market Restraints

- 4.3.1 Diisocyanate price and supply volatility

- 4.3.2 Tightening REACH limits on free NCO content

- 4.3.3 Bio-based adhesive substitutes gaining share

- 4.4 Value Chain Analysis

- 4.5 Regulatory Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Distribution Channel Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 End-User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV-Cured

- 5.2.5 Water-borne

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF

- 6.4.4 Beardow Adams

- 6.4.5 DELO Industrial Adhesives

- 6.4.6 Dow Inc.

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat SE

- 6.4.12 MAPEI S.p.A.

- 6.4.13 Momentive Performance Materials

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Sika AG

- 6.4.16 Soudal Holding N.V.

- 6.4.17 Tesa Tapes (India) Private Limited

- 6.4.18 ThreeBond Europe

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment