|

시장보고서

상품코드

2072678

HR 서비스 제공 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)HR Service Delivery Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

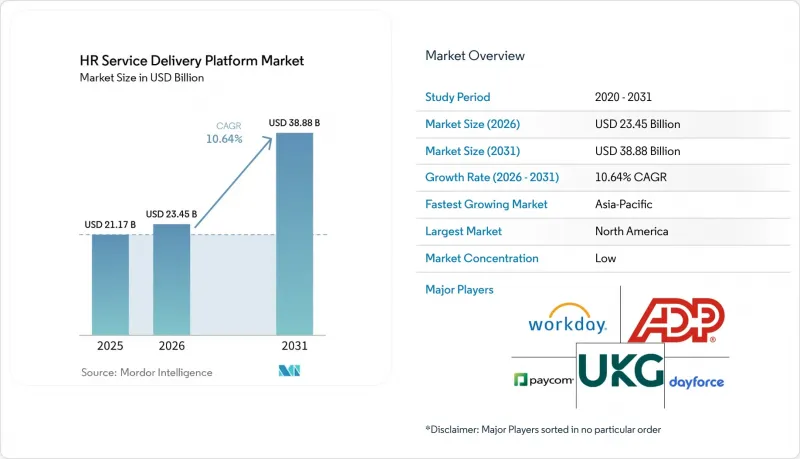

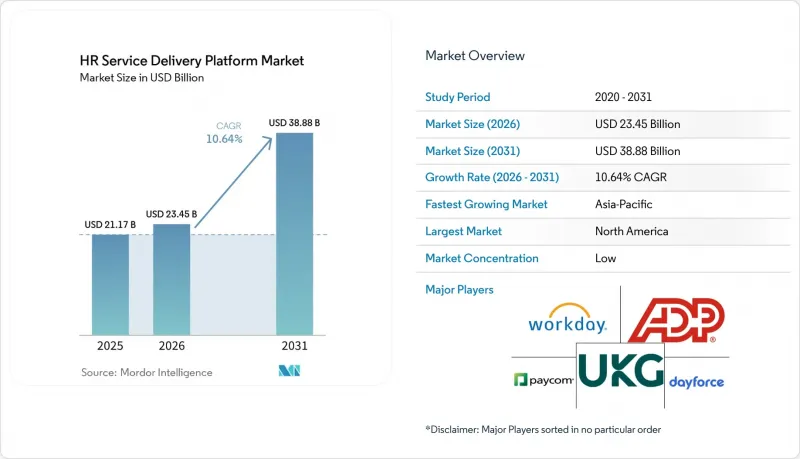

Mordor Intelligence에 의하면, HR 서비스 제공 플랫폼 시장 규모는 2025년 212억 7,000만 달러로 평가되었고, 2026년에는 234억 5,000만 달러로 추정되고, 2031년까지 388억 8,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 10.64%로 성장할 전망입니다.

본 보고서는 구성 요소별(소프트웨어 및 서비스), 도입 모델별(클라우드 기반, 온프레미스형, 하이브리드형), 기업 규모별(대기업 및 중소기업), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 정보기술 및 통신, 소매 및 전자상거래 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 HR 서비스 제공 플랫폼 시장 동향 및 인사이트

기존 인사 시스템에서 클라우드로의 전환

HR 서비스 제공 플랫폼 시장에서 클라우드 전환은 더 이상 단순한 비용 문제의 차원을 넘어, 현재는 사업 연속성의 핵심 요소로 자리 잡고 있습니다. Strada는 2025년 7월 보고서에서 기업의 약 40%가 여전히 노후화된 온프레미스 HR 및 ERP 시스템을 운영하고 있으며, 예산 제약과 통합의 복잡성이 각각 42%의 변혁 계획에 영향을 미치고 있다고 보고했습니다. 이 조사 결과는 중요한 의미를 지닙니다. 왜냐하면, 전환 지연으로 인한 불이익이 현재 더 커지고 있기 때문입니다. 특히, SAP ECC가 2025년 12월에 지원이 종료되고, Microsoft Dynamics GP도 2029년에 지원이 종료될 예정인 만큼, 구형 시스템 환경을 계속 사용하는 조직의 경우 보안 및 기능 측면에서의 위험이 커지고 있습니다. 미국 연방 정부는 OPM(인사관리국)과 OMB(행정관리예산국)가 'Federal HR 2.0'을 발표함으로써, 이러한 방향성을 한층 더 강화했습니다. 이 프로그램은 2026 회계연도에 시작되며, 100개 이상의 기존 인사 시스템을 단일 상용 플랫폼으로 통합하는 것을 목표로 하고 있습니다. 또한 ISG는 2027년 말까지 83%의 기업이 인사 기술의 핵심으로 SaaS 또는 하이브리드 클라우드를 도입할 것으로 예측하고 있으며, 이는 인사 서비스 제공 플랫폼 시장에서 전환을 위한 유예 기간이 급속히 좁아지고 있음을 시사합니다. 따라서 도입 기간을 단축하고, 라이선스 비용 절감뿐만 아니라 운영상의 이점도 입증할 수 있는 벤더는 인사 서비스 제공 플랫폼 시장 전체에서 더욱 확고한 입지를 차지하고 있다고 할 수 있습니다.

통합형 직원 셀프 서비스 및 사례 관리에 대한 수요 증가

또한, HR 서비스 제공 플랫폼 시장은 파편화된 HR 헬프데스크 모델과 직원 지원 워크플로우의 느린 속도에 대한 불만으로도 성장 동력을 얻고 있습니다. 맥킨지는 2025년 보고서에서 유럽의 핵심 HR 프로세스 중 생성형 AI를 통해 강화된 비율은 고작 19%에 불과하며, 32%는 여전히 시범 운영 단계에 머물러 있다고 지적했는데, 이는 라우팅, 검색, 해결을 대규모로 자동화할 수 있는 플랫폼에 여전히 큰 여지가 남아 있음을 시사합니다. 이와 유사한 수요는 서비스 조직의 설계 측면에서도 두드러지게 나타나고 있으며, 전문화된 인사 공유 서비스 센터가 충분히 활용되지 못하고 있는 실정입니다. 이는 많은 기업이 공통 플랫폼을 통해 서비스 제공을 일원화함으로써 얻을 수 있는 효율화의 이점을 아직 충분히 누리지 못하고 있음을 의미합니다. UKG는 의료 분야에서 이 모델의 가치를 입증했습니다. 이 회사의 'Rapid Hire' 기능을 통해 반복적인 채용 업무의 최대 90%가 자동화되었고, 채용까지 소요되는 기간이 10일 단축되었으며, 심각한 인력 부족에 직면한 고객사에서 지원부터 채용까지의 전환율이 3배 증가했습니다. 그 결과, 인사 서비스 제공 플랫폼 시장에서는 직원용 셀프 서비스, 사례 관리, 지식 기반 정보 접근, 워크플로우 자동화를 단일 운영 계층에 통합한 플랫폼에 대한 수요가 증가하고 있습니다.

데이터 개인정보 보호 및 국경을 초월한 직원 데이터 관리

개인정보 보호 및 국경을 넘는 데이터 전송에 관한 규정은 여전히 HR 서비스 제공 플랫폼 시장에서 가장 뚜렷한 걸림돌 중 하나입니다. 다국적 기업들이 표준 계약 조항, 데이터 이전 영향 평가 및 하도급 처리자의 거버넌스를 플랫폼 운영에 직접 반영해야 할 필요성이 대두됨에 따라, 이 문제는 더 이상 법적 검토에만 국한되지 않습니다. 유럽 데이터 보호 위원회(EDPB)는 2026년 4월, GDPR(EU 개인정보보호규정) 제42조 및 제46조에 근거한 국제 데이터 이전을 위한 최초의 인증 기반 체계로서 'Europrivacy'을 승인함으로써, 공급업체가 기존의 이전 프레임워크와 병행하여 준수해야 할 새로운 규정 준수 절차를 확립했습니다. 의료, 금융 서비스, 공공 부문의 구매자들은 EU에 기반을 둔 인프라와 보다 강력한 현지 보관 관리 체계를 갖춘 공급업체를 점점 더 선호하고 있기 때문에 조달에 미치는 영향은 이미 뚜렷하게 나타나고 있습니다. 독일, 프랑스, 베네룩스 국가 등 시장에서는 GDPR(EU 개인정보보호규정) 제28조에 따른 실사 절차 역시 현지 호스팅 및 데이터 처리 체인 전반에 걸쳐 명확한 설명 책임을 입증할 수 있는 공급업체에 대한 평가를 뒷받침하고 있으며, 이는 인사 서비스 제공 시장에서 전 세계적으로 표준화된 플랫폼의 유연성을 제한하고 있습니다.

부문별 분석

2025년, HR 서비스 제공 플랫폼 시장에서 소프트웨어가 71.21%를 차지했으며, 이는 정기적인 라이선스 수익이 여전히 이 부문의 핵심 수익원임을 보여줍니다. HR 서비스 제공 플랫폼 업계에서 구매자들은 핵심 HR, 직원 서비스 관리, 급여 계산, 인력 관리, 인재 관리 도구, 분석, 학습 등의 기능을 개별 제품으로 따로 모은 것이 아니라, 하나의 제품군 내에서 연동된 형태로 제공하는 것을 점점 더 선호하고 있습니다. 이러한 추세는 지속적인 AI 출시, 규정 준수 업데이트, 모듈 확장을 통해 장기적으로 업데이트 및 교차 판매 활동이 강화되는 모델을 뒷받침하고 있습니다. 그 결과, 고객들이 단일 공급업체 하에서 어느 정도까지 통합해야 할지 논의하고 있음에도 불구하고, 소프트웨어는 여전히 HR 서비스 제공 플랫폼 시장을 독점하고 있습니다.

서비스 부문은 2031년까지 연평균 성장률(CAGR) 12.43%로 성장할 것으로 예상되며, 규모는 작지만 가장 빠르게 성장하는 구성 요소가 될 전망입니다. 플랫폼의 범위가 확대되고 일상 업무에 깊이 통합됨에 따라, 도입, 관리형 서비스, 규정 준수 자문 서비스에 대한 수요가 증가하는 추세이므로, 이는 소프트웨어 부문의 우위를 훼손하지 않습니다. 벤더의 지원, 고객 성공 프로그램, 관리형 서비스는 중소기업(SMB) 중 HCM을 도입한 기업들에게 가치 실현의 핵심 요소로 자리 잡고 있으며, 이는 이러한 방향성과 일치합니다. HR 서비스 제공 플랫폼 시장에서 소프트웨어 시장 규모는 여전히 크지만, 운영 모델이 복잡해짐에 따라 고객은 배포, 통합, 정책 조정에 대한 지원이 필요하기 때문에 서비스 계층의 중요성이 커지고 있습니다.

2025년, HR 서비스 제공 플랫폼 시장에서 클라우드 기반 도입이 64.90%를 차지했습니다. 이는 인프라 비용 절감, 기능 제공의 신속화, 그리고 분산된 전 직원을 대상으로 한 정책 업데이트의 용이성을 반영한 것입니다. 이러한 경향은 온프레미스 환경의 오버헤드 없이 분석, 셀프 서비스, 지속적인 구성 변경을 지원하는 호스팅형 환경으로 HR 서비스 제공 플랫폼 시장이 광범위하게 전환되고 있는 상황과 일치합니다. 워크데이는 2025년 11월, EU 역내에서의 완전한 데이터 거주권과 EU 거점에서의 운영을 갖춘 'Workday EU Sovereign Cloud'을 출시하며, 이러한 방향성을 한층 더 강화했습니다. 이는 각 벤더들이 클라우드 모델에서 거리를 두는 것이 아니라, 클라우드 모델 내에서 규제상의 우려 사항을 해결하고 있음을 보여줍니다. 또한, 연방인사청(OPM)과 연방관리예산청(OMB)도 ‘연방 HR 2.0’을 통해 2028 회계연도까지 100개 이상의 구형 연방 시스템을 상용 플랫폼으로 이전하겠다는 방침을 발표함으로써, 이와 유사한 이전을 시사했습니다.

하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 11.87%로 확대될 것으로 예상되며, 이는 일부 고용주들이 규정 준수 및 관리를 위해 여전히 혼합 아키텍처를 필요로 하고 있음을 보여줍니다. 금융 서비스, 의료, 정부 기관의 구매 담당자들은 셀프 서비스 및 분석을 위해 클라우드의 민첩성을 추구하는 한편, 특정 급여 및 인사 데이터에 대해서는 온프레미스 환경에서 관리하기를 원하는 경우가 많습니다. 이러한 경향은 HR 서비스 제공 플랫폼 시장에서 하이브리드 방식의 성장이 클라우드로의 전환을 주저하는 것을 의미하는 것이 아니라, 데이터 보관 규정 및 내부 위험 정책에 대응하기 위한 것임을 시사합니다. 따라서 HR 서비스 제공 플랫폼 업계에서는 계속해서 '클라우드 퍼스트' 설계가 주류를 이루는 한편, 법적 및 운영상의 조건으로 인해 보다 세분화된 도입 옵션이 요구되는 분야에서는 하이브리드 아키텍처가 확대될 것입니다.

지역별 분석

2025년, 북미는 HR 서비스 제공 플랫폼 시장의 41.71%를 차지했으며, 지역별로는 가장 큰 수익 기반이 되었습니다. 그 수요의 대부분은 미국이 차지하고 있는데, 이는 기업의 SaaS 도입률이 세계 평균을 지속적으로 상회하고, 대기업들이 인력 관리 시스템의 현대화를 대규모로 추진해 왔기 때문입니다. 연방 정부의 'HR 2.0'은 이러한 동향을 보여주는 가장 명확한 공식적인 신호가 되었습니다. OPM(인사관리국)과 OMB(행정관리예산국)이 100개가 넘는 정부 기관의 인사 시스템을 단일 상용 HCM 플랫폼으로 통합하는 사업을 시작했으며, 이에 따른 10년간의 계약 규모는 10억 달러를 넘어설 것으로 예측됩니다. 캐나다에서는 13개 주 및 준주에 걸쳐 규정 준수 부담이 발생하고 있기 때문에 법규 자동 갱신 기능과 급여 계산과의 연동성이 강화된 플랫폼이 유리해지면서 새로운 수요원으로 부상하고 있습니다. 멕시코 역시 제조업의 성장과, 특히 시간제 근로자가 대다수를 차지하는 환경에서 발생하는 국경을 초월한 인재 관리 수요를 통해 HR 서비스 제공 플랫폼 시장을 뒷받침하고 있습니다.

유럽은 HR 서비스 제공 플랫폼 시장에서 여전히 규제가 가장 엄격한 지역 중 하나이며, 그 복잡성 또한 강력한 상업적 촉진요인으로 작용하고 있습니다. 지침(EU) 2023/970에 따라, 회원국은 2026년 6월 7일까지 '임금 투명성 지침'을 국내법에 반영해야 할 의무가 부과됨에 따라, 고용주는 직무 구조의 통일 및 보고를 위한 인사 데이터와 급여 데이터의 통합을 추진해야 하는 상황에 놓여 있습니다. 직원 수가 250명 이상인 고용주는 2026년 데이터를 바탕으로 2027년부터 연례 남녀 임금 격차 보고를 시작하게 되었으며, 이에 따라 플랫폼 도입을 위한 시스템 준비 기간이 단축되었습니다. 독일, 영국, 프랑스, 네덜란드는 여전히 해당 지역에서 가장 큰 수익 시장이지만, 현지 호스팅 및 GDPR(EU 개인정보보호규정) 대응 여부가 공급업체 선정에 있어 점점 더 중요한 요소로 대두되고 있습니다. 또한 러시아에서는 연방법 제242-FZ호에 따라 데이터 현지화가 핵심 요건으로 의무화되어 있어, 전 세계적인 클라우드 도입 모델의 적용 범위가 제한되고 있으며, 해당 국가에서는 여전히 제약이 많은 상황이 지속되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.21%를 나타낼 것으로 예측되며, HR 서비스 제공 플랫폼 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 이 지역의 성장은 다국적 기업의 사업 확장, 중견 기업의 디지털화 가속화, 그리고 일부 이용 사례에서 세계 솔루션보다 각국 고유의 규제에 더 잘 대응하는 현지 공급업체의 부상에 기인합니다. 중국에서는 Kingdee AI HR이나 Yonyou와 같은 플랫폼이 현지 노동, 세무, 사회보험 요건을 중심으로 구축되어 있어 이러한 추세를 여실히 보여주고 있습니다. 또한, 인도 역시 Darwinbox가 2025년 3월에 1억 4,000만 달러를 조달하고, 보다 광범위한 국제적 사업 확장의 일환으로 본사를 싱가포르로 이전함에 따라 그 중요성이 커지고 있습니다. 일본에서도 2026년 4월 SmartHR의 등록 기업 수가 8만 개사를 돌파하며, 노무 관리 클라우드 업체로서 7년 연속 1위를 유지한 것이 또 하나의 분명한 징후가 되었습니다. 이는 아시아태평양의 인사 서비스 제공 플랫폼 시장이 전 세계의 기존 기업들로만 정의되는 것은 아니라는 점을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the HR service delivery platform market size is expected to increase from USD 21.27 billion in 2025 to USD 23.45 billion in 2026 and reach USD 38.88 billion by 2031, growing at a CAGR of 10.64% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HR Service Delivery Platform Market Trends and Insights

Cloud Migration from Legacy Human Resources Stacks

Cloud migration in the HR service delivery platform market has moved beyond a cost discussion and now sits at the center of operating resilience. Strada reported in July 2025 that nearly 40% of businesses still ran aging on-premise HR and ERP systems, and that budget limits and integration complexity each affected 42% of transformation plans. That finding matters because delayed migration now carries a larger penalty, especially after SAP ECC reached end-of-life in December 2025 and Microsoft Dynamics GP moved toward support expiry in 2029, which raises security and capability risk for organizations that stay on older stacks. The U.S. federal government reinforced this direction when OPM and OMB announced Federal HR 2.0, a program that begins in fiscal 2026 and aims to consolidate more than 100 legacy HR systems onto a single commercial platform. ISG also projected that 83% of companies will have SaaS or hybrid cloud at the core of their HR technology by the end of 2027, suggesting that the migration window in the HR service delivery platform market is narrowing quickly. Vendors that can shorten deployment time and show operational gains, not just license savings, are therefore in a stronger position across the HR service delivery platform market.

Rising Demand for Unified Employee Self-Service And Case Management

The HR service delivery platform market is also being pushed by frustration with fragmented HR helpdesk models and slow employee support workflows. McKinsey reported in 2025 that only 19% of core HR processes in Europe had been enhanced with generative AI, while another 32% remained in pilot stages, leaving a large room for platforms that can automate routing, search, and resolution at scale. The same demand is evident in service organization design, where specialized HR shared-services centers remain underused, meaning many companies have not yet captured the efficiency gains from centralizing service delivery on a common platform. UKG showed the value of this model in healthcare, where its Rapid Hire capability automated up to 90% of repetitive hiring tasks, reduced time-to-hire by 10 days, and tripled apply-to-hire conversion rates for customers operating under acute staffing pressure. As a result, the HR service delivery platform market is seeing stronger demand for platforms that combine employee self-service, case management, knowledge access, and workflow automation into a single operating layer.

Data Privacy And Cross-Border Employee Data Controls

Privacy and cross-border transfer rules remain one of the clearest brakes on the HR service delivery platform market. The challenge is no longer limited to legal review because multinational employers now need standard contractual clauses, transfer impact assessments, and sub-processor governance embedded directly into platform operations. The EDPB approved Europrivacy in April 2026 as the first certification-based mechanism for international data transfers under Articles 42 and 46 of the GDPR, creating a new compliance path that vendors must support alongside older transfer frameworks. Procurement effects are already visible because buyers in healthcare, financial services, and the public sector increasingly favor vendors with EU-based infrastructure and stronger local residency controls. In markets such as Germany, France, and the Benelux, due diligence under GDPR Article 28 is also pushing evaluations toward vendors that can demonstrate local hosting and clearer accountability across data-handling chains, narrowing the flexibility of globally standardized platforms in the HR service delivery market.

Other drivers and restraints analyzed in the detailed report include:

- Need For Real-Time Workforce Analytics And Workflow Automation

- Hybrid And Distributed Work Models Expanding Digital Human Resources Touchpoints

- Integration Complexity with Legacy Enterprise Resource Planning and Payroll Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 71.21% of the HR service delivery platform market in 2025, which shows that recurring licenses remain the core commercial engine for the category. In the HR service delivery platform industry, buyers increasingly want core HR, employee service management, payroll, workforce management, talent tools, analytics, and learning, all connected within one suite rather than stitched together as separate products. That preference supports a model where continuous AI releases, compliance updates, and module expansion reinforce renewal and cross-sell activity over time. The result is that software continues to dominate the HR service delivery platform market, even as customers debate how far they should consolidate under a single vendor.

Services are projected to grow at a 12.43% CAGR through 2031, making it the faster-growing component, even though it starts from a smaller base. This does not weaken the software case because implementation, managed services, and compliance advisory demand tend to rise as platforms become broader and more embedded in daily operations. Vendor support, client success programs, and managed services are becoming central to value realization for SMB HCM buyers, which aligns with this direction. The HR service delivery platform market size for software remains larger, but the services layer is becoming more durable because customers need help with rollout, integration, and policy alignment as the operating model grows more complex.

Cloud-based deployment accounted for 64.90% of the HR service delivery platform market in 2025, reflecting lower infrastructure costs, faster feature delivery, and easier policy updates across distributed workforces. That position aligns with the wider shift in the HR service delivery platform market toward hosted environments that support analytics, self-service, and continuous configuration change without on-premises overhead. Workday reinforced this direction in November 2025 when it launched Workday EU Sovereign Cloud with full EU data residency and EU-based operations, showing that vendors are addressing regulatory concerns inside the cloud model rather than stepping away from it. OPM and OMB also signaled the same transition when Federal HR 2.0 set out to move more than 100 legacy federal systems onto a commercial platform by fiscal 2028.

Hybrid deployment is forecast to grow at a 11.87% CAGR through 2031, indicating that some employers still need a mixed architecture for compliance and control. Financial services, healthcare, and government buyers often want cloud agility for self-service and analytics while keeping selected payroll or personnel data in locally controlled environments. That pattern means hybrid growth in the HR service delivery platform market is not a sign of cloud hesitation, but a response to residency rules and internal risk policy. The HR service delivery platform industry, therefore, continues to favor cloud-first design, while hybrid architecture expands where legal and operating conditions require more segmented deployment choices.

Complete Report Scope:

- By Component

- Software

- Core Human Resources

- Employee Service Management and Helpdesk

- Payroll and Compensation

- Workforce Management

- Talent Management

- People Analytics and Reporting

- Learning and Development

- Services

- Software

- By Deployment Model

- Cloud-Based

- On-Premises

- Hybrid

- By End User Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 41.71% of the HR service delivery platform market share in 2025, which made it the leading regional revenue base. The United States accounted for most of that demand because enterprise SaaS adoption remained above global averages and large employers continued to modernize workforce systems at scale. Federal HR 2.0 became the clearest public signal of this trend when OPM and OMB set out to consolidate more than 100 agency HR systems onto a single commercial HCM platform, with a 10-year contract expected to exceed USD 1 billion. Canada introduces a new source of demand, as 13 provinces and territories create a multi-jurisdictional compliance burden that favors platforms with automated legislative updates and stronger payroll alignment. Mexico also supports the HR service delivery platform market through manufacturing growth and cross-border workforce administration needs, especially in high-volume hourly labor settings.

Europe remains one of the most regulation-heavy parts of the HR service delivery platform market, and that complexity is also becoming a strong commercial driver. Directive (EU) 2023/970 required member states to transpose the Pay Transparency Directive by June 7, 2026, which pushed employers to harmonize job structures and combine HR and payroll data for reporting. Employers with 250 or more workers will begin annual gender pay gap reporting in 2027 based on 2026 data, which tightened the system-readiness window for platform deployment. Germany, the United Kingdom, France, and the Netherlands remain the largest revenue markets in the region, while local hosting and GDPR readiness increasingly shape vendor selection. Russia also maintains a more restricted profile because Federal Law No. 242-FZ mandates data localization as a core requirement, limiting the scope for global cloud deployment models.

Asia-Pacific is projected to grow at a 15.21% CAGR through 2031, making it the fastest-growing geography in the HR service delivery platform market. Growth in this region comes from multinational expansion, faster digitization among mid-sized employers, and the rise of local vendors that handle country-specific rules better than global suites in some use cases. China illustrates that pattern through platforms such as Kingdee AI HR and Yonyou, which are built around local labor, tax, and social insurance requirements. India has also become more important after Darwinbox raised USD 140 million in March 2025 and shifted its headquarters to Singapore as part of a broader international scale-up. Japan added another clear signal in April 2026 when SmartHR passed 80,000 registered companies and secured its seventh consecutive year as the leading labor-management cloud vendor, which shows that the HR service delivery platform market in Asia-Pacific is not defined by global incumbents alone.

- Workday, Inc.

- Automatic Data Processing, Inc.

- Ultimate Kronos Group, Inc.

- Dayforce, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- Bamboo HR LLC

- Hi Bob Limited

- Personio SE and Co. KG

- Darwinbox Digital Solutions Private Limited

- Rippling People Center Inc.

- Deel Inc.

- Papaya Global Ltd.

- Remote Technology, Inc.

- Zalaris ASA

- Zellis UK Limited

- isolved, Inc.

- ServiceNow, Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration From Legacy Human Resources Stacks

- 4.2.2 Rising Demand For Unified Employee Self-Service and Case Management

- 4.2.3 Need For Real-Time Workforce Analytics and Workflow Automation

- 4.2.4 Hybrid and Distributed Work Models Expanding Digital Human Resources Touchpoints

- 4.2.5 European Union Pay Transparency Directive Forcing Harmonized Job and Pay Data

- 4.2.6 Skills-Based Workforce Planning and Internal Talent Mobility

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-Border Employee Data Controls

- 4.3.2 Integration Complexity With Legacy Enterprise Resource Planning and Payroll Systems

- 4.3.3 European Union Artificial Intelligence Act and Algorithmic Accountability For Employment Decisions

- 4.3.4 Data Sovereignty and Regional Hosting Requirements

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry-Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Core Human Resources

- 5.1.1.2 Employee Service Management and Helpdesk

- 5.1.1.3 Payroll and Compensation

- 5.1.1.4 Workforce Management

- 5.1.1.5 Talent Management

- 5.1.1.6 People Analytics and Reporting

- 5.1.1.7 Learning and Development

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Workday, Inc.

- 6.4.2 Automatic Data Processing, Inc.

- 6.4.3 Ultimate Kronos Group, Inc.

- 6.4.4 Dayforce, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Paychex, Inc.

- 6.4.8 Paycor HCM, Inc.

- 6.4.9 Bamboo HR LLC

- 6.4.10 Hi Bob Limited

- 6.4.11 Personio SE and Co. KG

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Rippling People Center Inc.

- 6.4.14 Deel Inc.

- 6.4.15 Papaya Global Ltd.

- 6.4.16 Remote Technology, Inc.

- 6.4.17 Zalaris ASA

- 6.4.18 Zellis UK Limited

- 6.4.19 isolved, Inc.

- 6.4.20 ServiceNow, Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment