|

시장보고서

상품코드

2072682

북미의 HR 서비스 제공 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America HR Service Delivery Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

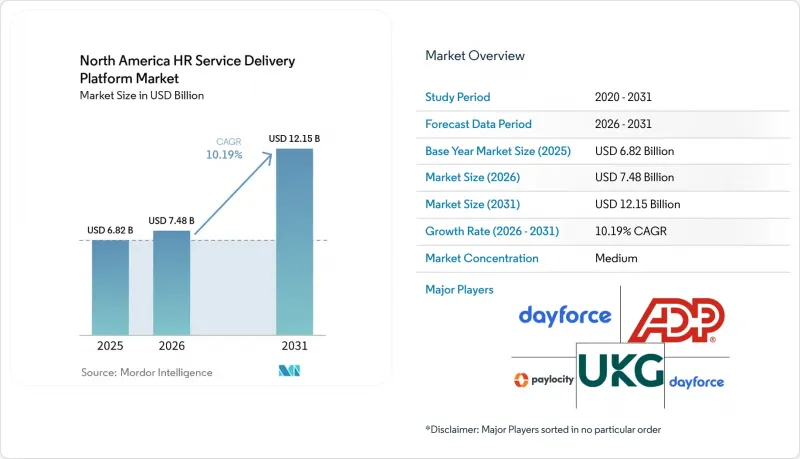

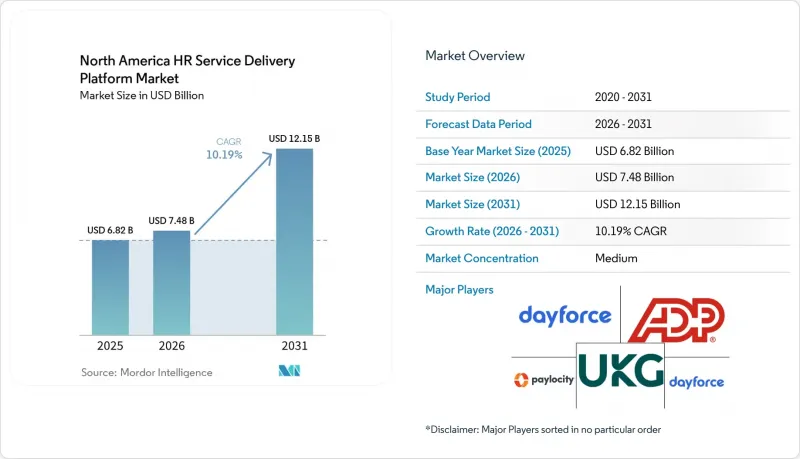

Mordor Intelligence에 의하면, 북미의 HR 서비스 제공 플랫폼 시장 규모는 2025년 68억 2,000만 달러로 평가되었고, 2026년 74억 8,000만 달러로 추정되고, 2031년까지 121억 5,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 10.19%를 나타낼 전망입니다.

본 보고서는 구성 요소별(소프트웨어 및 서비스), 도입 모델별(클라우드 기반, 온프레미스형, 하이브리드형), 기업 규모별(대기업, 중소기업), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 정보기술 및 통신, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 HR 서비스 제공 플랫폼 시장 동향 및 인사이트

기존 인사 시스템에서 클라우드로의 전환

기업들이 서로 연동되지 않은 인사 관리 도구를 단일 환경 내에서 서비스 제공, 급여 계산, 분석을 지원하는 통합 시스템으로 대체하려 하고 있기 때문에 클라우드 전환은 여전히 북미 HR 서비스 제공 플랫폼 시장에서 가장 뚜렷한 단기적 촉진요인으로 작용하고 있습니다. SAP는 2025년에 'SuccessFactors Enterprise Service Management'를 도입하여 인사 업무 처리와 지능형 셀프 서비스를 연계했습니다. 이는 고립된 모듈이 아닌, 통합된 클라우드 서비스 계층으로 나아가는 이 회사의 광범위한 움직임을 반영한 것입니다. Workday는 2026년에 Sana를 인사 및 재무 워크플로우 전반으로 확대했습니다. 이는 주요 플랫폼들이 단순한 기록 관리 업무뿐만 아니라, 작업을 수행하는 자동화를 목적으로 설계되고 있음을 보여줍니다. 또한, 마이크로소프트는 '직원 셀프 서비스 에이전트'를 도입하여, 단일 인터페이스를 통해 SharePoint, Workday, ServiceNow에 걸쳐 있는 지식 및 워크플로 소스를 연동함으로써, 파편화된 레거시 스택에서 벗어나도록 지원하고 있습니다. 많은 기업이 모든 핵심 시스템을 한꺼번에 교체하는 것은 아니기 때문에 이러한 전환에 따라 커넥터, 급여 계산 시스템과의 통합, 워크플로우 오케스트레이션에 대한 수요가 발생하고 있습니다. 그 결과, 클라우드 전환이 소프트웨어 수요를 끌어올리는 동시에 북미 HR 서비스 제공 플랫폼 시장 전반에서 도입 및 관리형 서비스 제공업체의 수익 기회를 확대되고 있습니다.

통합형 직원 셀프 서비스 및 사례 관리에 대한 수요 증가

북미 HR 서비스 제공 플랫폼 시장에서 고용주들은 서비스 데스크 인력을 증원하지 않고도 문제를 신속하게 해결하기를 원하고 있어, 통합형 직원 셀프 서비스 및 사례 관리에 대한 수요가 증가하고 있습니다. IBM은 자사의 'AskHR' 플랫폼은 현재 80개 이상의 HR 업무를 자동화하고 있으며, 연간 210만 건 이상의 직원과의 대화를 처리하고 있다고 밝혔습니다. 이는 AI 기반 셀프 서비스가 시범 기능이 아닌, 기업 규모로 운영될 수 있음을 보여줍니다. SAP는 2025년에 'SuccessFactors Enterprise Service Management'를 출시한 뒤, 그 후 '줄' 어시스턴트를 통해 서비스 해결 기능을 확장했습니다. 이를 통해 케이스 접수, 라우팅, 직원 지원을 통합한 단일 플랫폼으로의 전환이 더욱 강화되었습니다. 마이크로소프트의 '직원 셀프 서비스 에이전트' 또한, 인사 관련 지식과 업무 처리를 단일 대화형 인터페이스에 통합함으로써, 고용주가 시스템 간 전환을 없애고자 한다는 점을 보여주었습니다. 이러한 도구가 개선됨에 따라, 사례 이관은 단순한 비용 절감 조치의 범위를 넘어 서비스 품질의 일부로 자리 잡고 있습니다. 이는 인사팀이 민감한 문제나 복잡한 인재 관련 과제에 더 많은 시간을 할애할 수 있게 하기 위함입니다. 또한 문서화, 감사 추적, 직원에 대한 접근 제어와 같은 요소들 역시 조직이 범용 티켓 관리 시스템이 아닌, 인사 사례 전용으로 설계된 도구를 채택하도록 이끌고 있습니다.

데이터 개인정보 보호 및 국경을 초월한 직원 데이터 관리

데이터 개인정보 보호 및 국경을 초월한 직원 데이터 관리는 조달 절차를 지연시키고 있습니다. 이는 북미 HR 서비스 제공 플랫폼 시장에서 고용주가 급여, 사례 데이터, 보상 기록이 관할 구역 간에 어떻게 이동하는지 면밀히 검토해야 하기 때문입니다. 2026년 1월 1일부터 발효되는 캘리포니아주의 개정 CCPA 규정에 따르면, 특정 고용주는 자동화된 의사결정 활용 등 중대한 개인정보 보호 위험을 수반하는 인사 데이터를 처리하기 전에 공식적인 개인정보 보호 위험 평가를 실시해야 합니다. 다국적 기업의 경우, EU와 북미 시스템 간 직원 데이터 전송에도 체계적인 규정 준수 체제가 필요하며, 계약 체결 전에 법적 검토 및 공급업체 감사 작업이 추가됩니다. 따라서 GDPR(EU 개인정보보호규정), CCPA, PIPEDA의 각 요건에 대해 보다 통일된 규정 준수 체계를 제시할 수 있는 대규모 플랫폼이 유리한 입장에 서기 마련입니다. 소규모 도구나 틈새 시장용 도구는 기능 면에서는 여전히 경쟁력을 유지할 수 있지만, 조달 팀이 개인정보 보호 인증이나 데이터 처리 관리를 우선시할 경우 판매 주기가 길어지는 경향이 있습니다. 그 결과, 수요가 감소하는 것은 아니지만, 도입 지연이나 구매자와 공급업체 양측 모두에게 규정 준수 부담이 가중되는 결과를 초래하고 있습니다.

부문별 분석

2025년, 소프트웨어는 시장 점유율의 71.82%를 차지했으며, 북미 HR 서비스 제공 플랫폼 시장에서 가장 큰 비중을 차지했습니다. 중견 및 대기업을 불문하고, 처리량이 가장 많은 프로세스를 담당하는 핵심 인사, 급여, 보상 및 직원 서비스 관리 모듈은 여전히 구매자의 지출 기반을 이루고 있습니다. 또한, 구매자들은 개별 대시보드나 단일 기능 도구를 일상적인 워크플로우에 통합된 기능으로 대체해 나가면서, 인력 분석, 인재 관리 및 인력 관리에 대한 소프트웨어 지출을 늘리고 있습니다. 2025년 및 2026년의 제품 출시 계획은 이러한 방향성을 명확히 보여주고 있으며, 엔터프라이즈 서비스 관리 및 자율형 HCM 기능을 통해 서비스 문제 해결과 의사결정 지원의 상당 부분이 소프트웨어 계층 자체로 이전되고 있습니다. 기업들은 시스템 간 전환을 줄이고 데이터의 일관성을 높이는 종합적인 제품군을 선호하기 때문에 소프트웨어는 여전히 수익의 주축을 이루고 있습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 12.47%를 나타낼 것으로 예측되며, 북미 HR 서비스 제공 플랫폼 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 2026년 4월에는 고객을 대신해 급여 계산 및 인사 업무를 관리하는 전담 팀을 갖춘 새로운 매니지드 솔루션이 출시되었습니다. 이는 일회성 도입 작업보다 지속적인 관리 지원에 대한 수요가 증가하고 있음을 반영하고 있습니다. 또한, 다른 제공업체도 2026년 2월, 운영 지원을 필요로 하는 중소규모 고용주를 대상으로 기술과 실무 중심의 인사 지원을 결합한 번들형 인사 서비스를 일반에 제공하기 시작했습니다. AI 거버넌스, 급여 계산 관리, 데이터 스튜어드십, 그리고 본 가동 후의 튜닝은 모두 지속적인 지원이 필요하기 때문에 소프트웨어 도입 주기가 더욱 효율화되더라도 서비스 수익은 견조한 추세를 보일 것으로 전망됩니다.

2025년, 북미 HR 서비스 제공 플랫폼 시장 점유율의 65.30%를 클라우드 기반 도입이 차지했으며, SaaS가 주요 제공 모델임이 확인되었습니다. 클라우드 모델은 기능 업데이트의 신속화, 직원의 접근성 향상, 대규모 직원 기반 전반에 걸친 AI 기반 워크플로우 도입의 용이화를 지원하기 때문에 여전히 매력적입니다. 또한, 부서 간 경계를 넘어 핵심 인사, 셀프 서비스, 분석 기능을 연계하는 통합 플랫폼을 추구하는 현재의 구매 트렌드와도 부합합니다. 온프레미스 환경은 데이터 취급에 관한 규제가 더욱 엄격한 정부 기관, 국방 기관, 그리고 엄격한 규제가 적용되는 금융 업계 등 일부 조직에서 여전히 중요하게 여겨지고 있습니다. 그렇긴 하지만, 새로운 자동화 기능의 대부분이 우선 클라우드 환경에서 구축되고 있기 때문에 북미 인사 서비스 제공 업계는 클라우드 중심의 운영 모델로 계속해서 전환하고 있습니다.

하이브리드 방식은 2031년까지 연평균 성장률(CAGR) 11.93%로 확대될 것으로 예측되며, 가장 빠르게 성장하는 도입 방식이 될 전망입니다. 대규모 고용주들은 직원의 셀프 서비스, 분석, 서비스 관리를 클라우드로 전환하는 한편, 구식 온프레미스형 ERP나 급여 계산 시스템을 계속 유지하는 경우가 많습니다. 이러한 추세로 인해 하이브리드 아키텍처는 레거시 시스템과 완전한 SaaS의 중간 단계에 해당하는 임시적인 대안이라기보다는 의도적인 설계상의 선택으로 자리 잡고 있습니다. 새롭게 부상하고 있는 엣지-투-클라우드 모델은 이러한 논리를 한층 더 확장한 것으로, 고용주는 클라우드 인터페이스를 통해 직원을 대상으로 한 AI 상호작용을 수행하는 동시에, 기밀성이 높은 기록은 관리가 철저한 환경을 통해 처리할 수 있게 됩니다. 이를 통해, 전환이 진행됨에 따라 하이브리드 도입이 사라지는 것이 아니라, 북미 HR 서비스 제공 플랫폼 시장에서 클라우드의 성장과 병행하여 하이브리드 채택이 증가하고 있는 이유를 설명할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the north america HR service delivery platform market size is projected to expand from USD 6.82 billion in 2025 and USD 7.48 billion in 2026 to USD 12.15 billion by 2031, registering a CAGR of 10.19% between 2026 and 2031.

This report is Segmented by Component (Software and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, and More ), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America HR Service Delivery Platform Market Trends and Insights

Cloud Migration from Legacy Human Resources Stacks

Cloud migration remains the clearest near-term driver of the North America HR service delivery platform market, as enterprises seek to replace disconnected HR tools with unified systems that support service delivery, payroll, and analytics in a single environment. SAP introduced SuccessFactors Enterprise Service Management in 2025 to connect HR case handling with intelligent self-service, reflecting the vendor's broader move toward integrated cloud service layers rather than isolated modules. Workday expanded Sana in 2026 across HR and finance workflows, demonstrating that major platforms are now being designed for action-taking automation rather than only system-of-record tasks. Microsoft also deployed its Employee Self-Service Agent to connect knowledge and workflow sources across SharePoint, Workday, and ServiceNow through a single interface, supporting the shift away from fragmented legacy stacks. This migration is creating follow-on demand for connectors, payroll integrations, and workflow orchestration, as most enterprises are not replacing every core system at once. The result is that cloud migration is lifting software demand while also extending revenue opportunities for implementation and managed service providers across the North America HR service delivery platform market.

Rising Demand for Unified Employee Self-Service And Case Management

Demand for unified employee self-service and case management is rising because employers want faster issue resolution without adding service desk headcount across the North America HR service delivery platform market. IBM stated that its AskHR platform now automates more than 80 HR tasks and handles more than 2.1 million employee conversations each year, which shows that AI-led self-service can operate at enterprise scale rather than as a pilot feature. SAP launched SuccessFactors Enterprise Service Management in 2025 and later extended service resolution capabilities through Joule assistants, reinforcing the move toward a single platform for case intake, routing, and employee support. Microsoft's Employee Self-Service Agent also showed how employers are trying to remove system switching by bringing HR knowledge and transaction support into a single conversational interface. As these tools improve, case deflection is moving beyond a cost measure and becoming part of service quality because HR teams can spend more time on sensitive or complex workforce issues. Documentation, audit trails, and employee access controls are also driving organizations toward purpose-built HR case tools rather than generic ticketing systems.

Data Privacy And Cross-Border Employee Data Controls

Data privacy and cross-border employee data controls are slowing procurement because employers must review how payroll, case data, and compensation records move across jurisdictions in the North America HR service delivery platform market. California's amended CCPA regulations, effective January 1, 2026, required certain employers to conduct formal privacy risk assessments before processing HR data tied to significant privacy risk, including automated decision-making uses. For multinational employers, employee data transfers between the EU and North American systems also require structured compliance mechanisms, which adds legal review and vendor audit work before contracts are signed. This tends to favor larger platforms that can present a more unified compliance posture across GDPR, CCPA, and PIPEDA requirements. Smaller or niche tools can still compete on features, but they face a longer sales cycle when procurement teams prioritize privacy certifications and data-handling controls. The result is not lower demand, but slower deployment and a higher compliance burden for buyers and vendors alike.

Other drivers and restraints analyzed in the detailed report include:

- Need for Real-Time Workforce Analytics and Workflow Automation

- Hybrid and Distributed Work Models Expanding Digital Human Resources Touchpoints

- Integration Complexity With Legacy Enterprise Resource Planning And Payroll Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held a 71.82% share of the market in 2025, making it the largest component of the North America HR service delivery platform market. Core HR, payroll, and compensation, and employee service management modules remain the base of buyer spending because they handle the highest-volume processes across large and mid-sized organizations. Buyers are also directing more software spend toward people analytics, talent management, and workforce management as they replace separate dashboards and point tools with functions embedded inside daily workflows. Product releases in 2025 and 2026 clearly showed this direction, with enterprise service management and autonomous HCM capabilities moving more service resolution and decision support into the software layer itself. This keeps software as the revenue anchor because enterprises prefer broad suites that reduce switching across systems and tighten data consistency.

Services are projected to grow at a 12.47% CAGR through 2031, making it the fastest-moving component segment in the North America HR service delivery platform market. In April 2026, new managed solutions were launched with dedicated teams that administer payroll and HR operations on behalf of clients, which reflects rising demand for managed support rather than one-time implementation work. Other providers also made bundled HR services generally available in February 2026, combining technology with hands-on HR support for smaller employers seeking execution support. AI governance, payroll administration, data stewardship, and post-go-live tuning all require ongoing support, which means services revenue should remain strong even when software deployment cycles become more efficient.

Cloud-based deployment accounted for 65.30% of the North America HR service delivery platform market share in 2025, which confirmed SaaS as the leading delivery model. The cloud model continues to appeal because it supports faster feature updates, better employee access, and easier rollout of AI-enabled workflows across large workforces. It also aligns with current buying preferences for unified platforms that connect core HR, self-service, and analytics across departments. On-premises environments remain relevant for a smaller group of organizations in government, defense, and tightly regulated financial settings where data-handling restrictions are stricter. Even so, the North America HR service delivery industry continues to move toward cloud-led operating models because most new automation capabilities are being built there first.

Hybrid deployment is projected to expand at a 11.93% CAGR through 2031, making it the fastest-growing deployment approach. Large employers often retain older on-premises ERP or payroll systems while moving employee self-service, analytics, and service management to the cloud. That pattern is turning hybrid architecture into a deliberate design choice rather than a temporary midpoint between legacy and full SaaS. The emerging edge-to-cloud model extends this logic further, enabling employers to run employee-facing AI interactions through cloud interfaces while routing sensitive records through more controlled environments. This helps explain why hybrid adoption is rising alongside cloud growth in the North America HR service delivery platform market instead of disappearing as migration advances.

Complete Report Scope:

- By Component

- Software

- Core Human Resources

- Employee Service Management and Helpdesk

- Payroll and Compensation

- Workforce Management

- Talent Management

- People Analytics and Reporting

- Learning and Development

- Services

- Software

- By Deployment Model

- Cloud-Based

- On-Premises

- Hybrid

- By End User Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Workday, Inc.

- Automatic Data Processing, Inc.

- Ultimate Kronos Group, Inc.

- Dayforce, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- Bamboo HR LLC

- Hi Bob Limited

- Gusto Inc.

- Darwinbox Digital Solutions Private Limited

- Rippling People Center Inc.

- Deel Inc.

- Papaya Global Ltd.

- Remote Technology, Inc.

- isolved Inc.

- ServiceNow, Inc.

- Namely, Inc.

- Workable Technology Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration From Legacy Human Resources Stacks

- 4.2.2 Rising Demand For Unified Employee Self-Service and Case Management

- 4.2.3 Need For Real-Time Workforce Analytics and Workflow Automation

- 4.2.4 Hybrid and Distributed Work Models Expanding Digital Human Resources Touchpoints

- 4.2.5 European Union Pay Transparency Directive Forcing Harmonized Job and Pay Data

- 4.2.6 Skills-Based Workforce Planning and Internal Talent Mobility

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-Border Employee Data Controls

- 4.3.2 Integration Complexity With Legacy Enterprise Resource Planning and Payroll Systems

- 4.3.3 European Union Artificial Intelligence Act and Algorithmic Accountability For Employment Decisions

- 4.3.4 Data Sovereignty and Regional Hosting Requirements

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Core Human Resources

- 5.1.1.2 Employee Service Management and Helpdesk

- 5.1.1.3 Payroll and Compensation

- 5.1.1.4 Workforce Management

- 5.1.1.5 Talent Management

- 5.1.1.6 People Analytics and Reporting

- 5.1.1.7 Learning and Development

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Workday, Inc.

- 6.4.2 Automatic Data Processing, Inc.

- 6.4.3 Ultimate Kronos Group, Inc.

- 6.4.4 Dayforce, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Paychex, Inc.

- 6.4.8 Paycor HCM, Inc.

- 6.4.9 Bamboo HR LLC

- 6.4.10 Hi Bob Limited

- 6.4.11 Gusto Inc.

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Rippling People Center Inc.

- 6.4.14 Deel Inc.

- 6.4.15 Papaya Global Ltd.

- 6.4.16 Remote Technology, Inc.

- 6.4.17 isolved Inc.

- 6.4.18 ServiceNow, Inc.

- 6.4.19 Namely, Inc.

- 6.4.20 Workable Technology Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment