|

시장보고서

상품코드

2072728

탄소 정보공개 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Carbon Disclosure Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

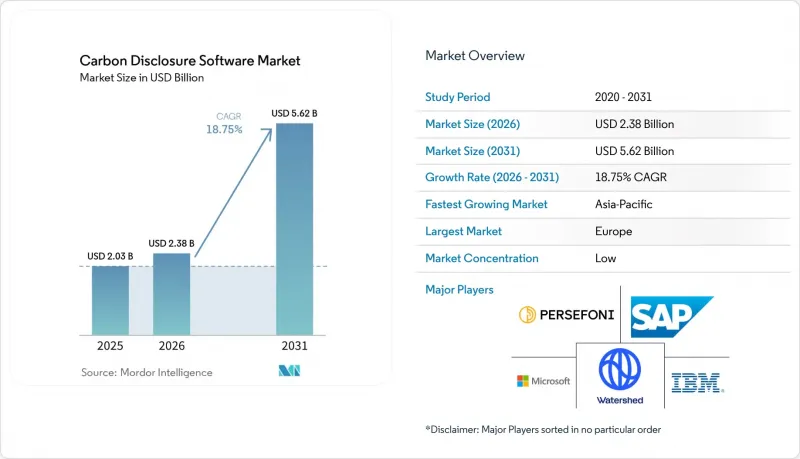

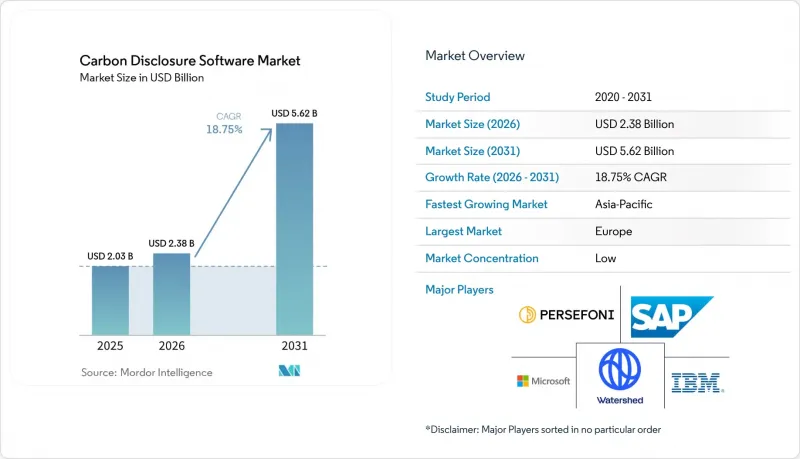

Mordor Intelligence에 의하면, 탄소 정보공개 소프트웨어 시장 규모는 2025년에 20억 3,000만 달러로 평가되었고, 2026년에 23억 8,000만 달러로 추정되고, 2031년까지 56억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 18.75%로 성장할 전망입니다.

본 보고서는 도입 형태별(클라우드 기반, 온프레미스형, 하이브리드형), 기업 규모별(대기업, 중소기업), 기능 범위별(공시 데이터 관리, 보고 및 규제 공시 등), 최종 사용자 산업 분야별(공업 제조, 에너지 및 유틸리티 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 탄소 정보공개 소프트웨어 시장 동향 및 인사이트

전 세계 기후 정보 공개 의무 확대

탄소 정보공개 소프트웨어 시장은 현재 여러 관할 구역에서 동시에 공식적인 기후 변화 보고를 의무화하는 규제가 확대되고 있는 데 힘입어 성장하고 있습니다. 유럽에서는 CSRD(기업 지속가능성 보고 지침)의 틀과 2026년 3월의 옴니버스 개정안에 따라, 개정된 직원 수 및 매출액 기준을 초과하는 대규모 기업에 대한 공시 의무가 유지됨에 따라, 소프트웨어 도입을 위한 광범위한 규정 준수 기반이 확보되었습니다. 이 점은 중요합니다. 왜냐하면 기업들은 현재 단편적인 스프레드시트를 관리하는 것이 아니라, 계산 방법, 출처 문서 및 보증에 대한 기록을 체계적으로 보관할 수 있는 시스템을 필요로 하고 있기 때문입니다. 북미 및 아시아태평양에서는 주별 규제, 단계적 보고 프로그램, 그리고 새로운 국가 차원의 기후 변화 공시 기준을 통해 추가적인 수요가 발생하고 있습니다. 이를 통해 단일 규제상의 지연으로 인해 지출이 완전히 중단될 위험이 완화되었습니다. 또한, 중국 재정부(財政部)는 2025년 12월에 '기업 지속가능성 공시 기준 제1호 : 기후(시행)'를 공포했습니다. 이는 아시아태평양의 탄소 정보공개 소프트웨어 시장에 있어 또 하나의 공식적인 정책적 기반이 될 것입니다.

스코프 3 공급업체 데이터의 디지털화가 진전되고 있습니다.

스코프 3 보고는 여전히 탄소 정보공개 소프트웨어 시장에 있어 가장 강력한 성장 요인 중 하나입니다. 이는 공급업체 정보가 필수적이면서도 대규모로 수집하기 어렵기 때문입니다. Sphera가 2026년에 1,000명 이상의 지속가능성 리더를 대상으로 실시한 조사에 따르면, 73%의 조직이 자발적으로 스코프 3 데이터를 공개하고 있으며, 89%는 이를 더욱 확대할 계획인 반면, 현재 데이터의 정확성에 대해서는 '어느 정도 자신감이 있다'라고 답한 비율은 고작 45%에 그쳤으며, 보고에 대한 의욕과 준비 상황 사이에 큰 괴리가 있음을 보여주고 있습니다. 이러한 격차로 인해, 1차 공급업체 데이터를 수집하고, 추정값과 검증된 입력 데이터를 구분하며, 여러 범주에 걸쳐 활용 가능한 감사 추적을 유지할 수 있는 플랫폼에 대한 안정적인 수요가 발생하고 있습니다. 또한, 대규모 구매업체들이 중소 공급업체에 대해 반복적으로 동일한 데이터를 요구함에 따라, 정보 공개가 단순한 정기 업무에서 조달, 지속가능성, 재무 팀에 걸쳐 진행되는 지속적인 업무 흐름으로 변화하고 있으며, 이로 인해 탄소 정보공개 소프트웨어 시장도 혜택을 보고 있습니다. 공급업체에 대한 요구 사항이 기계 판독 가능성으로 전환되고 그 빈도도 증가함에 따라, 제출 데이터를 표준화하고 불일치하는 원본 기록을 대조하는 소프트웨어가 보고 체계의 핵심을 이루고 있습니다.

높은 데이터 품질과 조사 방법의 복잡성

탄소 정보공개 소프트웨어 시장은 수집된 배출량 데이터와 감사에 대응할 수 있는 공개 입력 데이터 간의 격차라는 여전히 큰 장벽에 직면해 있습니다. 2025년에 발표된 조사에 따르면, 많은 중소기업은 자동화된 보고 시스템이나 조사 기법에 대한 전문 지식이 부족한 것으로 나타났으며, CSRD 도입 첫해의 비용은 5,000유로(5,400달러)에서 1만 8,000유로(1만 9,440달러)에 이르는 것으로 나타났습니다. 이로 인해 소규모 기업 입장에서는 조기 도입이 어려워지고 있습니다. 이 과제는 단순히 데이터의 입수 가능성 문제에만 그치지 않습니다. 왜냐하면 보증 심사 담당자들은 데이터 출처의 투명성, 1차 데이터와 2차 데이터의 구분, 그리고 여러 범주를 아우르는 재현 가능한 관리 체계를 점점 더 요구하고 있기 때문입니다. 출처 추적 기능이 충분히 갖춰지지 않은 초기 탄소 공개 도구를 도입한 기업들은 보고 기한이 다가오는 가운데, 현재 전환 작업에 직면해 있습니다. 그 결과, 탄소 정보공개 소프트웨어 시장의 일부에서 도입 주기가 길어지면서 단기적인 전환 속도가 둔화되고 있습니다.

부문별 분석

2025년, 탄소 정보공개 소프트웨어 시장의 66.42%를 클라우드 기반 솔루션이 차지하면서, 인프라 요구 사항이 낮고 확장성이 뛰어난 플랫폼에 대한 구매자들의 선호도가 두드러지게 나타났습니다. 규제 내용의 변경, 협업에 대한 수요, ERP와의 통합은 통합된 소프트웨어 환경에서 관리가 용이하기 때문에 탄소 정보공개 소프트웨어 시장은 클라우드 제공 방식으로 전환되었습니다. Watershed, Persefoni, Sweep 등의 전용 벤더들은 신속한 업데이트, 분산형 사용자 액세스, 공유 데이터 워크플로우를 제품 설계의 핵심으로 삼음으로써 이 모델의 보급에 기여했습니다. 한편, 데이터 소재지 규제나 내부 보안 기준으로 인해 운영 데이터의 자유로운 이동이 제한되는 정부 기관, 유틸리티체, 금융 기관에서는 온프레미스 구축이 여전히 중요한 선택지로 남아 있습니다.

하이브리드 방식은 탄소 정보공개 소프트웨어 시장에서 가장 빠르게 성장하고 있는 부문으로, 2026-2031년 연평균 성장률(CAGR) 19.87%를 나타낼 것으로 전망됩니다. 수요가 가장 높은 분야는 산업 및 에너지 분야입니다. 이러한 분야에서 기업들은 클라우드를 활용한 분석 및 보고서 작성을 원하면서도, 기밀성이 높은 플랜트 데이터나 운영 데이터에 대해서는 여전히 보다 엄격한 내부 관리 하에 두기를 원하고 있습니다. 이러한 경향은 탄소 배출 기록이 생산량, 시설의 처리 능력 또는 제품 수준의 계산과 연계되어 있으며, 구매자가 이를 외부 환경으로 완전히 이전하는 것을 원하지 않는 경우에 더욱 두드러집니다. 각 벤더사는 보안이 강화된 데이터 게이트웨이와 로컬 검증 계층을 제공함으로써 이에 대응하고 있으며, 탄소 정보공개 소프트웨어 시장은 클라우드를 통한 보고서 작성 속도와 원본 데이터에 대한 보다 강력한 관리 기능을 모두 지원할 수 있게 되었습니다.

2025년 기준으로 대기업이 탄소 정보공개 소프트웨어 시장의 64.15%를 차지했습니다. 이는 일찍부터 규정 준수 대응 경험을 쌓아왔습니다는 점과, 여러 프레임워크를 지원하는 소프트웨어 도입에 필요한 예산 규모를 반영한 것입니다. 탄소 정보공개 소프트웨어 시장이 처음에 가장 빠르게 성장한 곳은 대기업이었습니다. 이는 이러한 구매자가 자회사, 금융 기관, 감사인, 그리고 여러 보고 체계를 동시에 조율해야 했기 때문입니다. 또한, 이 그룹은 투자자나 이사회의 면밀한 검토를 견딜 수 있는 공식적인 관리 체계, 지속적인 보증 지원, 그리고 통합된 기록에 대한 필요성도 더욱 컸습니다. 지속가능성 연계 채권(SLB)은 이러한 추세를 더욱 강화했습니다. 발행사는 널리 채택된 시장 원칙에 따라 온실가스 배출 실적에 대해 매년 독립적인 검증을 받아야 하며, 이는 일회성 제출 작업이 아니라 지속적인 플랫폼 이용을 촉진하고 있기 때문입니다.

탄소 정보공개 소프트웨어 시장에서 2026-2031년 중소기업(SME) 부문 시장 규모가 연평균 성장률(CAGR) 21.34%라는 가장 높은 성장률을 보일 것으로 전망됩니다. 이러한 수요의 상당 부분은 공급망을 통해 발생하고 있는데, 이는 대규모 구매 기업들이 의무적인 규제가 직접 적용되지 않는 경우에도 중소 공급업체들에게 1차 배출량 데이터 제공을 요구하고 있기 때문입니다. 2025년에 발표된 조사에 따르면, 중소기업의 CSRD 도입 첫해 비용은 5,000유로(5,400달러)에서 1만 8,000유로(1만 9,440달러) 사이인 것으로 나타났으며, 이는 저비용의 가이드가 포함된 도구가 점차 보급되고 있는 이유를 설명해 줍니다. 그 결과, 탄소 정보공개 소프트웨어 시장은 2단계 구조로 진화하고 있으며, 복잡한 조직에 대응하는 엔터프라이즈급 시스템과 공급업체 네트워크 내에서 도입을 놓고 경쟁하는 경량형 셀프서비스형 도구가 공존하는 형태를 띠고 있습니다.

지역별 분석

2025년, 유럽은 매출의 35.12%를 차지했으며, 탄소 정보공개 소프트웨어 시장에서 가장 규모가 큰 지역 점유율을 유지했습니다. 해당 지역이 계속해서 선두를 유지하고 있는 이유는 대기업에서 기후 변화 보고가 이미 정책 수립 단계에서 실제 제출, 보증 심사, 공급업체 선정 단계로 넘어가고 있기 때문입니다. 2026년 3월 개정에서는 직원 수 1,000명 이상이고 순매출액이 4억 5,000만 유로(4억 8,600만 달러)를 초과하는 기업을 대상으로 의무화를 도입하는 데 초점이 맞추어졌으며, 대상 범위는 좁아졌지만, 대상 중 최대 규모의 기업들에게는 견고한 보고 시스템의 중요성이 더욱 커졌습니다. 배터리 탄소 발자국 신고 요건을 포함한 제품 수준의 추적성 규정은 유럽 제조업 전반에 걸쳐 플랫폼에 대한 수요를 더욱 높이고 있습니다.

북미는 자발적인 보고, 투자자들의 압력, 그리고 주 차원의 공시 규정에 힘입어 탄소 배출 정보 공시 소프트웨어 시장에서 여전히 2위 지역 클러스터의 위치를 유지하고 있습니다. 연방 정부의 기후 변화 정보 공개 방침이 여전히 불투명한 상황에서도, 캘리포니아주 SB 253 법안에 따라 대기업들은 스코프 3 대응 준비에 계속 주력하고 있습니다. 또한, 이 지역은 사업 활동 및 공급망 전반에 걸친 감사 가능한 배출량 데이터가 필요한 기업용 소프트웨어 구매자, 금융 기관, 다국적 기업으로 구성된 견고한 기반으로부터도 혜택을 받고 있습니다. 남미는 현재 규모는 작지만, 브라질 상장기업에 대한 ESG 요건 및 ISSB 지침에 부합하는 체계의 구축에 힘입어, 탄소 정보공개 소프트웨어 시장의 향후 수요는 점차 확대되고 있습니다.

아시아태평양은 탄소 정보공개 소프트웨어 시장에서 가장 빠르게 성장하고 있는 지역으로, 2026-2031년 연평균 성장률(CAGR) 24.63%를 나타낼 것으로 전망됩니다. 일본의 ISSB 기준에 부합하는 공시 절차, 호주의 단계적인 스코프 3 도입, 그리고 중국의 기후 변화 공시 프레임워크가 해당 지역을 보다 공식적인 규정 준수로 이끌고 있습니다. 중국 재무부는 2025년 12월에 '기업 지속가능성 공시 기준 제1호 : 기후(시행)'를 공포했으며, 생태환경부는 이미 2025년 3월에 자발적 온실가스 공개 지침을 발표하여, 이를 통해 기업의 보고와 관련된 정책 기반이 강화되었습니다. 또한, 이 지역이 세계 제조업의 주요 생산 거점이라는 점도 중요한 요인으로 작용하고 있습니다. 이는 공급업체들이 유럽 및 북미의 고객들로부터 더 많은 탄소 데이터 제공 요청을 받고 있기 때문입니다. 아프리카와 중동은 절대적인 규모로 볼 때 여전히 작지만, 정부 주도 금융 프로그램, 거래소 요건 및 공공 부문의 보고 의무로 인해 탄소 정보공개 소프트웨어의 대상 시장은 꾸준히 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.07According to Mordor Intelligence, the carbon disclosure software market size is projected to be USD 2.03 billion in 2025, USD 2.38 billion in 2026, and reach USD 5.62 billion by 2031, growing at a CAGR of 18.75% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Functional Scope (Disclosure Data Management, Reporting and Regulatory Disclosure, and More), End-User Industry (Industrial Manufacturing, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Carbon Disclosure Software Market Trends and Insights

Expanding Global Climate Disclosure Mandates

The carbon disclosure software market is being driven by the expanding set of rules that now require formal climate reporting across several jurisdictions simultaneously. In Europe, the CSRD framework and the March 2026 Omnibus revision maintained disclosure obligations for larger entities above the revised employee and turnover thresholds, thereby preserving a large compliance base for software adoption. That matters because companies now need systems that can store calculation methods, source documentation, and assurance trails in a structured way, rather than keeping fragmented spreadsheets. North America and Asia-Pacific add another layer of demand through state rules, phased reporting programs, and newer national climate disclosure standards, reducing the risk that a single regulatory delay can fully halt spending. China's Ministry of Finance also issued Corporate Sustainable Disclosure Standard No. 1, Climate (Trial) in December 2025, which adds another formal policy anchor for the carbon disclosure software market in Asia-Pacific.

Rising Scope 3 Supplier Data Digitization

Scope 3 reporting remains one of the strongest growth supports for the carbon disclosure software market because supplier information is both essential and difficult to collect at scale. Sphera's 2026 survey of more than 1,000 sustainability leaders found that 73% of organizations voluntarily disclose Scope 3 data, 89% plan further expansion, and only 45% have limited confidence in the accuracy of their current data, indicating a wide gap between reporting ambition and readiness. That gap creates steady demand for platforms that can gather primary supplier data, separate estimates from verified inputs, and preserve a usable audit trail across categories. The carbon disclosure software market also benefits when large buyers repeatedly request the same data from smaller suppliers, turning disclosure from a periodic task into an ongoing workflow across procurement, sustainability, and finance teams. As supplier requests become more machine-readable and more frequent, software that standardizes submissions and reconciles inconsistent source records is becoming part of the core reporting stack.

High Data Quality And Methodology Complexity

The carbon disclosure software market still faces a major barrier in the gap between collected emissions data and audit-ready disclosure inputs. Research published in 2025 showed that many SMEs lack automated reporting systems and methodological expertise, and that first-year CSRD implementation costs ranged from EUR 5,000 (USD 5,400) to EUR 18,000 (USD 19,440), making early adoption difficult for smaller firms. This challenge goes beyond simple data availability because assurance reviewers increasingly expect source transparency, visibility into primary-versus-secondary data, and repeatable controls across categories. Companies that bought earlier carbon tools without strong provenance features are now facing migration work as reporting deadlines tighten. The result is longer implementation cycles and slower near-term conversion for parts of the carbon disclosure software market.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Shift To Cloud-Native Sustainability Stacks

- Generative AI For Automated Data Collection And Reconciliation

- SME Budget And Change-Management Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based solutions accounted for 66.42% of the carbon disclosure software market share in 2025, underscoring buyers' preference for scalable platforms with lower infrastructure requirements. The carbon disclosure software market leaned toward cloud delivery because regulatory content changes, collaboration needs, and ERP integrations are easier to manage in a centralized software environment. Purpose-built vendors such as Watershed, Persefoni, and Sweep helped normalize this model by building their products from the start around faster updates, distributed user access, and shared data workflows. On-premises deployment remained relevant for government users, utilities, and financial institutions where data residency rules or internal security standards limit the free movement of operating data.

Hybrid deployment is the fastest-growing segment of the carbon disclosure software market, with a projected CAGR of 19.87% from 2026 to 2031. Demand is strongest in industrial and energy settings where enterprises want cloud analytics and reporting but still keep sensitive plant or operational data under tighter internal control. This pattern becomes more visible when carbon records are tied to production yields, facility throughput, or product-level calculations that buyers do not want to move entirely into external environments. Vendors are responding with secure data gateways and local validation layers, so the carbon disclosure software market can support both cloud reporting speed and stronger control over source data

Large enterprises held 64.15% of the carbon disclosure software market in 2025, reflecting earlier compliance exposure and the budget capacity needed for multi-framework software rollouts. The carbon disclosure software market first expanded most rapidly in larger organizations because these buyers had to align subsidiaries, lenders, auditors, and multiple reporting frameworks simultaneously. This group also had a stronger need for formal controls, recurring assurance support, and centralized records that could withstand investor and board scrutiny. Sustainability-linked debt reinforced that pattern because issuers need annual independent verification of greenhouse gas performance under widely used market principles, which supports recurring platform use rather than one-time filing activity.

Small and medium enterprises are projected to grow at the fastest CAGR of 21.34% from 2026 to 2031 in the carbon disclosure software market. Much of this demand is coming through supply chains, as large buyers now ask smaller suppliers for primary emissions data even when mandatory rules do not directly cover those suppliers. Research published in 2025 showed that first-year CSRD implementation costs for SMEs ranged from EUR 5,000 (USD 5,400) to EUR 18,000 (USD 19,440), which explains why lower-cost, guided tools are gaining traction. The carbon disclosure software market is therefore evolving into a two-tier structure, with enterprise-grade systems serving complex organizations and lighter self-serve tools competing for adoption within supplier networks.

Complete Report Scope:

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Functional Scope

- Disclosure Data Management

- Reporting and Regulatory Disclosure

- Assurance, Verification and Audit Readiness

- Disclosure Analytics and Performance Insights

- Climate Disclosure Scenario Analysis

- By End-user Industry

- Industrial Manufacturing

- Energy and Utilities

- BFSI

- Retail and Consumer Goods

- IT and Telecom

- Healthcare and Life Sciences

- Government and Public Sector

- Transportation and Logistics

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Europe accounted for 35.12% of revenue in 2025 and held the largest regional position in the carbon disclosure software market. The region remains ahead because climate reporting has already moved from policy design into live filing, assurance review, and vendor selection across large enterprises. The March 2026 revision, which focused mandatory coverage on companies with more than 1,000 employees and net turnover above EUR 450 million (USD 486 million), narrowed the scope but increased the importance of robust reporting systems for the largest in-scope entities. Product-level traceability rules, including the battery carbon-footprint declaration requirement, add another layer of platform demand across European manufacturing.

North America remained the second-largest regional cluster in the carbon disclosure software market, supported by voluntary reporting, investor pressure, and state-level disclosure rules. California's SB 253 kept large enterprises focused on Scope 3 readiness, even while the federal climate disclosure agenda remained less predictable. The region also benefits from a deep base of enterprise software buyers, lenders, and multinational companies that need auditable emissions data across their operations and supply chains. South America is smaller today, but listed company ESG requirements in Brazil and the development of a framework aligned with ISSB guidance are widening future demand for the carbon disclosure software market.

Asia-Pacific is the fastest-growing region in the carbon disclosure software market, with a projected CAGR of 24.63% from 2026 to 2031. Japan's ISSB-aligned filing path, Australia's phased Scope 3 rollout, and China's climate disclosure framework are pushing the region toward more formal compliance. China's Ministry of Finance issued Corporate Sustainable Disclosure Standard No. 1, Climate (Trial) in December 2025, and the Ministry of Ecology and Environment had already published voluntary greenhouse gas disclosure guidance in March 2025, which strengthened the policy base for enterprise reporting. The region's role as the main production base for global manufacturing also matters because suppliers are receiving more carbon data requests from customers in Europe and North America. The Middle East and Africa remain smaller in absolute terms, but sovereign finance programs, exchange requirements, and public-sector reporting are steadily expanding the addressable market for carbon disclosure software.

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Sweep SAS

- Plan A Technologies GmbH

- Normative AB

- Greenly SAS

- Emitwise Limited

- SINAI Technologies Inc.

- CarbonChain Limited

- Climatiq GmbH

- Workiva, Inc.

- FigBytes Inc.

- Carbon Direct, Inc.

- Green Project Technologies, Inc.

- Sustain.Life, Inc.

- Novisto Inc.

- Position Green AB

- IBM Envizi ESG Suite

- Briink GmbH

- Sphera Solutions, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Global Climate Disclosure Mandates

- 4.2.2 Rising Scope 3 Supplier Data Digitization

- 4.2.3 Enterprise Shift To Cloud-Native Sustainability Stacks

- 4.2.4 Audit-Ready Carbon Data For Sustainability-Linked Finance

- 4.2.5 EU Digital Product Passport And Product-Level Traceability

- 4.2.6 Generative AI For Automated Data Collection And Reconciliation

- 4.3 Market Restraints

- 4.3.1 High Data Quality And Methodology Complexity

- 4.3.2 SME Budget And Change-Management Constraints

- 4.3.3 Supplier Data Privacy And Commercial Sensitivity Concerns

- 4.3.4 Fragmented Global Reporting Standards And Overlapping Frameworks

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Functional Scope

- 5.3.1 Disclosure Data Management

- 5.3.2 Reporting and Regulatory Disclosure

- 5.3.3 Assurance, Verification and Audit Readiness

- 5.3.4 Disclosure Analytics and Performance Insights

- 5.3.5 Climate Disclosure Scenario Analysis

- 5.4 By End-user Industry

- 5.4.1 Industrial Manufacturing

- 5.4.2 Energy and Utilities

- 5.4.3 BFSI

- 5.4.4 Retail and Consumer Goods

- 5.4.5 IT and Telecom

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Government and Public Sector

- 5.4.8 Transportation and Logistics

- 5.4.9 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Persefoni AI, Inc.

- 6.4.2 Watershed Technology, Inc.

- 6.4.3 Sweep SAS

- 6.4.4 Plan A Technologies GmbH

- 6.4.5 Normative AB

- 6.4.6 Greenly SAS

- 6.4.7 Emitwise Limited

- 6.4.8 SINAI Technologies Inc.

- 6.4.9 CarbonChain Limited

- 6.4.10 Climatiq GmbH

- 6.4.11 Workiva, Inc.

- 6.4.12 FigBytes Inc.

- 6.4.13 Carbon Direct, Inc.

- 6.4.14 Green Project Technologies, Inc.

- 6.4.15 Sustain.Life, Inc.

- 6.4.16 Novisto Inc.

- 6.4.17 Position Green AB

- 6.4.18 IBM Envizi ESG Suite

- 6.4.19 Briink GmbH

- 6.4.20 Sphera Solutions, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment