|

시장보고서

상품코드

2072837

인도의 의약품 물류 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

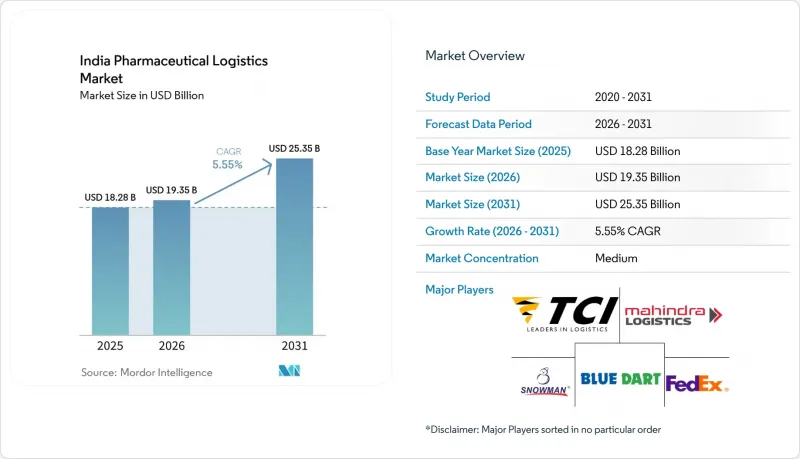

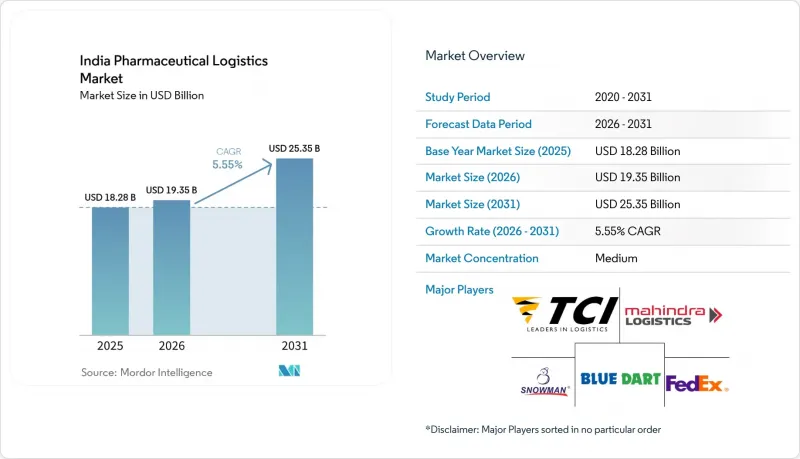

Mordor Intelligence에 의하면, 인도의 의약품 물류 시장 규모는 2025년 182억 8,000만 달러로 평가되었고, 2026년에는 193억 5,000만 달러로 추정되고, 2031년까지 253억 5,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 5.55%로 성장할 전망입니다.

인도는 세계 최대의 제네릭 의약품 공급국으로서 전 세계 제네릭 의약품 수출량의 20%를 차지하고 있으며, 이러한 역할로 인해 국내 및 수출용 유통 흐름의 규모와 복잡성은 계속해서 확대되고 있습니다. 본 보고서는 물류 기능별(수송, 창고 및 유통, 부가가치 서비스), 운영 모드별(콜드체인, 비콜드체인), 제품 유형별(처방약, 일반의약품, 생물학적 제제, 백신, 임상시험용 자재, 세포 및 유전자 치료, 의료기기, 동물용 의약품) 및 지역별(북부, 중부, 기타)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

인도의 의약품 물류 시장 동향 및 인사이트

정부의 생산 연계형 인센티브 제도

인도의 의약품 물류 시장 수요는 의약품 및 원료의약품을 대상으로 한 생산 연계형 인센티브(PLI) 프로그램에 따른 시장 규모 확대에 힘입어 증가하고 있습니다. 2025년 12월 기준으로, 이러한 제도에 따른 누적 투자액은 41,943 카롤 루피(46억 6,000만 달러)에 달했으며, 당초 약속 목표였던 17,275 카롤 루피(19억 2,000만 달러)의 2배 이상을 기록했습니다. 두 제도에 따른 누적 매출액은 1,988개 제품으로 3,35,036 카롤 루피(372억 8,000만 달러)에 달했으며, 이 중 수출액은 2,15,248 카롤 루피(239억 5,000만 달러)를 차지했습니다. 이는 생산 연계형 인센티브가 이미 국내 및 수출 채널 전반에서 물류량 증가를 주도하고 있음을 보여줍니다. 더 중요한 변화는 제품 구성에서 찾아볼 수 있습니다. 이 프로그램은 기존의 경구용 고형 제제보다 더 엄격한 온도 관리 및 취급 관리가 필요한 바이오의약품, 복잡한 제네릭 의약품, 그리고 자가면역 치료제를 우대하고 있기 때문입니다. 2026-27년도 연방 예산에서는 'Biopharma SHAKTI' 이니셔티브에 대해 5년간 10,000 카롤 루피(11억 1,000만 달러)의 지원이 결정되었으며, 1,000곳 이상의 인증 임상시험 시설을 구축하는 것이 목표로 제시되었습니다. 이는 전문적인 운송 및 규제를 준수하는 창고 수요가 장기간에 걸쳐 지속될 것임을 시사합니다.

온도 관리가 필요한 생물학적 제제 및 백신 수요 증가

인도의 의약품 물류 시장은 온도에 민감한 의약품으로의 전환이 가속화되면서 성장하고 있습니다. 인도는 유니세프의 전 세계 백신 조달량의 60%를 공급하고 있으며, DPT 및 BCG 백신의 전 세계 수요의 40%-70%를 충족시키고 있기 때문에 백신 취급 능력은 물류 계획의 핵심 요소로 자리 잡고 있습니다. 동시에, 2026년부터 2030년에 걸쳐 40종 이상의 주요 브랜드 의약품 특허가 잇달아 만료됨에 따라, 인도 제약사들은 일반적으로 2℃-8℃의 온도 관리가 필요한 바이오의약품, GLP-1 아날로그, 그리고 특수 주사제로 사업을 전환하고 있습니다. 이로 인해 감도가 높은 치료제가 아닌, 주로 대량의 경구용 고형제를 위해 구축된 콜드체인에 부담이 가중되고 있습니다. 쿠네 앤 나겔(Kune & Nagel)사는 API 및 백신 수출업체를 지원하기 위해 2025년 12월 방갈로르에서 2026년 5월 하이데라바드에서 HealthChain 인증을 받은 크로스독을 추가로 설치했습니다. 이는 물류 사업자들이 이러한 새로운 품목 구성에 맞추어 자산 재설계를 추진하고 있음을 보여줍니다.

대도시권 이외 지역의 파편화된 콜드체인 인프라

인도 의약품 물류 시장의 성장은 여전히 기준을 충족하는 콜드체인 인프라의 불균형한 분포로 인해 제약을 받고 있습니다. 네트워크는 소수의 대도시권이나 제조 거점에 집중된 상태인 반면, 2급·3급 도시나 지방의 회랑 지역에서는 온도 조절이 가능한 운송·보관 서비스가 충분히 제공되지 않고 있습니다. 인도에는 3,500개 이상의 콜드체인 사업자가 있지만, WHO-GDP 기준을 충족하는 곳은 고작 8%-10%에 불과하며, 네트워크의 대부분은 민감한 의약품을 취급하는 데 필요한 품질 기준에 미치지 못하는 상태입니다. 블루다트의 국내 사업 책임자는 2026년, 바이오의약품, 인슐린, 백신이 도시 지역 수요 거점을 넘어 유통되기 시작했음에도 불구하고, 2차 및 3차 도시와 농촌 지역에서의 온도 관리 운송 및 보관은 여전히 제한적이라고 밝혔습니다. 소규모 지역 사업자들은 검증, 비상 전원 및 지속적인 모니터링 시스템에 드는 비용을 감당하지 못하는 경우가 많으며, 이로 인해 주요 운송 경로 외 지역의 네트워크 품질 개선이 지연되고 있습니다.

부문별 분석

2025년, 인도의 의약품 물류 시장에서 운송 부문이 54.07%의 점유율을 차지했으며, 이는 도로 화물 운송이 여전히 국내 의약품 유통의 핵심 운송 수단임을 뒷받침하고 있습니다. 인도의 630만 km에 달하는 도로망은 750개 이상의 지역으로의 배송을 뒷받침하고 있으며, 이러한 지역에서는 대체 수단보다 직접적인 접근성이 더 중요하기 때문에 트럭은 여전히 없어서는 안 될 존재입니다. 항공 화물은 운송량이 적은 물품, 바이오 의약품, 임상시험용 자재 및 긴급 API(유효 성분) 운송의 경우, 1kg당 수익이 훨씬 더 높습니다. 특히 미국, 유럽, 아세안 시장으로의 수출 경로에서 이러한 경향이 두드러집니다. 해상 운송 및 내륙 수로는 운송 시간이 길기 때문에 필요한 기준에 따른 온도 관리 및 모니터링을 유지하기 어려우며, 의약품 용도로의 활용은 여전히 제한적입니다.

부가가치 서비스는 연평균 성장률(CAGR) 8.38%로 가장 빠른 성장세를 보일 것으로 예상되며, 이는 인도의 의약품 물류 업계가 단순한 운송 및 보관 계약의 범위를 넘어 진화하고 있음을 보여줍니다. 제약 기업의 고객들은 통합 계약에서 포장, 키트 구성, 일련번호 부여 지원, 역물류 및 문서 관리를 결합하는 사례가 늘고 있습니다. 또한, 습도 관리, 로트 분리, 온도 매핑, GDP 준수 SOP 이행이 더 이상 선택적 서비스가 아니라 일상 업무의 일부가 되었기 때문에 창고 보관 및 유통 업무도 활발해지고 있습니다. 철도 운송 규모는 여전히 작은 편이지만, 2026년 5월 하이데라바드에서 나바 셰바 구간을 주 1회 운행하기 시작한 마스쿠 콘코르사의 냉장 운송 노선은 화물 밀도가 충분히 높은 지역에서는 의약품 전용 철도 노선이 효과적으로 운영될 수 있음을 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the india pharmaceutical logistics market size is expected to increase from USD 18.28 billion in 2025 to USD 19.35 billion in 2026 and reach USD 25.35 billion by 2031, growing at a CAGR of 5.55% over 2026-2031.

India's role as the world's largest supplier of generic medicines, accounting for 20% of global generic drug exports by volume, continues to expand the scale and complexity of domestic and export distribution flows. This report is Segmented by Logistics Function (Transportation, Warehousing and Distribution, Value-Added Services), by Mode of Operation (Cold-Chain, Non-Cold-Chain), by Product Type (Prescription Drugs, OTC, Biologics, Vaccines, Clinical Trial Materials, Cell and Gene Therapies, Medical Devices, Veterinary Medicine), and by Region (North, Central, and More). The Market Forecasts are in Value (USD).

India Pharmaceutical Logistics Market Trends and Insights

Government Production-Linked Incentive Schemes

India pharmaceutical logistics market demand is rising with the scale-up created by the pharmaceutical and bulk drug PLI programs. As of December 2025, cumulative investment under these schemes reached INR 41,943 crores (USD 4.66 billion) and was more than double the initial commitment target of INR 17,275 crores (USD 1.92 billion). Cumulative sales under both schemes reached INR 3,35,036 crores (USD 37.28 billion) across 1,988 products, including exports worth INR 2,15,248 crores (USD 23.95 billion), indicating that production-linked incentives are already driving higher logistics volumes across domestic and export channels. The more important shift is in the product mix, as the program favors biopharmaceuticals, complex generics, and autoimmune therapies that require tighter thermal and handling controls than conventional oral solids. Union Budget 2026-27 also backed the Biopharma SHAKTI initiative with INR 10,000 crores (USD 1.11 billion) over 5 years and a target of more than 1,000 accredited clinical trial sites, which points to a longer cycle of specialized transport and compliant warehousing demand.

Rising Demand for Temperature-Controlled Biologics and Vaccines

India's pharmaceutical logistics market is being driven by a faster shift toward temperature-sensitive medicines. India supplies 60% of UNICEF's global vaccine procurement and meets 40%-70% of global demand for DPT and BCG vaccines, keeping vaccine handling capacity central to logistics planning. At the same time, the patent cliff for more than 40 major branded drugs between 2026 and 2030 is steering Indian manufacturers toward biologics, GLP-1 analogs, and specialty injectables that usually require 2 °C-8 °C control. This is putting pressure on a cold chain built primarily for bulk oral solids rather than for sensitive therapies. Kuehne+Nagel added HealthChain-certified cross-docks in Bengaluru in December 2025 and in Hyderabad in May 2026 to support API and vaccine exporters, indicating that providers are redesigning assets around this new mix.

Fragmented Cold-Chain Infrastructure Beyond Metros

India pharmaceutical logistics market expansion is still limited by the uneven spread of compliant cold infrastructure. The network remains concentrated in a small group of metros and manufacturing hubs, while Tier 2, Tier 3, and rural corridors stay underserved for temperature-controlled transport and storage. More than 3,500 cold-chain operators exist in India, yet only 8%-10% meet WHO-GDP standards, leaving a large share of the network below the quality level required for sensitive pharmaceutical handling. Blue Dart's National Operations Head stated in 2026 that temperature-controlled transport and storage remain limited across Tier II, Tier III, and rural regions, even as biologics, insulin, and vaccines move beyond urban demand centers. Smaller regional operators often cannot absorb the cost of validation, backup power, and continuous monitoring systems, which slows network quality improvement outside the main corridors.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of E-Pharmacy and D2C Drug Distribution

- RFID-Based Track-and-Trace Mandates by CDSCO

- High Compliance Cost of Evolving GDP Audits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for 54.07% of the India pharmaceutical logistics market share in 2025, which confirms that road freight remains the core movement layer for domestic pharmaceutical distribution. Trucks remain essential because India's 6.3 million km of road network supports deliveries to more than 750 districts, where direct reach matters more than modal substitution. Air freight carries lower volume but earns much higher revenue per kilogram for biologics, clinical trial materials, and urgent API shipments, especially on export lanes to the United States, Europe, and ASEAN markets. Sea and inland waterways remain limited for pharmaceutical use because long transit windows make temperature control and monitoring harder to sustain at the required standards.

Value-added services are projected to record the fastest growth at 8.38% CAGR, which shows that the India pharmaceutical logistics industry is moving beyond pure transport and storage contracts. Pharmaceutical customers are increasingly combining packaging, kitting, serialization support, reverse logistics, and documentation management inside integrated agreements. Warehousing and distribution is also becoming more active because humidity control, batch segregation, temperature mapping, and GDP-compliant SOP execution are now part of routine operations rather than optional services. Rail remains small, but the weekly Maersk-CONCOR reefer corridor from Hyderabad to Nhava Sheva launched in May 2026 shows that dedicated pharma rail routes can work where shipment density is high enough.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services and Others

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Product Type

- Prescription Drugs

- OTC Drugs

- Biologics and Biosimilars

- Vaccines and Blood Products

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices and Diagnostics

- Veterinary Medicine

- Others

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- DHL Group

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- FedEx

- United Parcel Service of America, Inc. (UPS)

- Blue Dart Express Pvt. Ltd.

- Allcargo Logistics Pvt. Ltd.

- TCI Express

- Mahindra Logistics, Ltd.

- Snowman Logistics

- ColdEx Logistics

- Safexpress Pvt. Ltd.

- Gati-KWE

- FM Logistic

- CMA CGM Group (Including CEVA Logistics)

- NYK Line (Including Yusen Logistics)

- TVS Supply Chain Solutions

- Stellar Value Chain Solutions

- Crystal Logistic Cool Chain

- ColdStar Logistics

- Celcius Logistics

- Life Care Logistic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Logistics in Pharmaceutical

- 4.2 Pharmaceutical Spending Trends

- 4.3 Market Drivers

- 4.3.1 Growth of Domestic Pharmaceutical Manufacturing Clusters

- 4.3.2 Government Production-Linked Incentive (PLI) Schemes

- 4.3.3 Rising Demand for Temperature-Controlled Biologics and Vaccines

- 4.3.4 Expansion of E-Pharmacy and D2C Drug Distribution

- 4.3.5 RFID-Based Track-and-Trace Mandates by CDSCO

- 4.3.6 Surge in Reverse Logistics Due to Expiry-Date Compliance

- 4.4 Market Restraints

- 4.4.1 Fragmented Cold-Chain Infrastructure Beyond Metros

- 4.4.2 High Compliance Cost of Evolving GDP Audits

- 4.4.3 Scarcity of Rail-Side Pharma-Grade Warehouses

- 4.4.4 Prospective Carbon-Tax on Diesel Reefer Fleets

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Pharmaceutical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Medical Devices and Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Region

- 5.4.1 North

- 5.4.2 Central

- 5.4.3 West

- 5.4.4 East

- 5.4.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne+Nagel

- 6.4.3 DSV A/S (Including DB Schenker)

- 6.4.4 FedEx

- 6.4.5 United Parcel Service of America, Inc. (UPS)

- 6.4.6 Blue Dart Express Pvt. Ltd.

- 6.4.7 Allcargo Logistics Pvt. Ltd.

- 6.4.8 TCI Express

- 6.4.9 Mahindra Logistics, Ltd.

- 6.4.10 Snowman Logistics

- 6.4.11 ColdEx Logistics

- 6.4.12 Safexpress Pvt. Ltd.

- 6.4.13 Gati-KWE

- 6.4.14 FM Logistic

- 6.4.15 CMA CGM Group (Including CEVA Logistics)

- 6.4.16 NYK Line (Including Yusen Logistics)

- 6.4.17 TVS Supply Chain Solutions

- 6.4.18 Stellar Value Chain Solutions

- 6.4.19 Crystal Logistic Cool Chain

- 6.4.20 ColdStar Logistics

- 6.4.21 Celcius Logistics

- 6.4.22 Life Care Logistic

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment