|

시장보고서

상품코드

2073026

공급망 탄소 관리 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Supply Chain Carbon Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

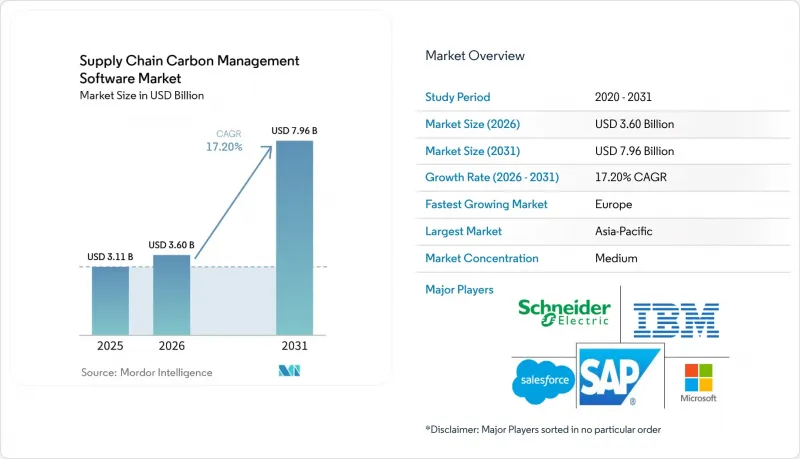

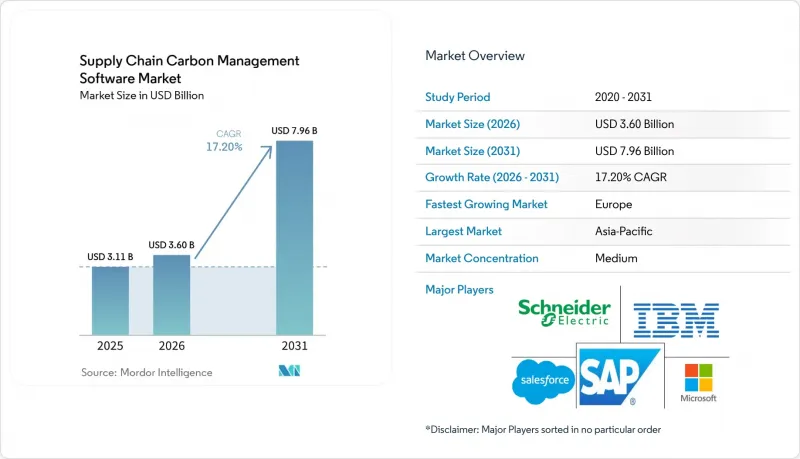

Mordor Intelligence에 의하면, 공급망 탄소 관리 소프트웨어 시장 규모는 2025년에 31억 1,000만 달러로 평가되었고, 2026년 36억 달러로 추정되고, 2031년까지 79억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 17.20%를 나타낼 전망입니다.

본 보고서는 제공 분야별(소프트웨어 및 서비스), 배포 모델별(클라우드, 온프레미스, 하이브리드), 기업 규모별(대기업 및 중소기업), 용도별(탄소 회계 및 배출량 추적 등), 최종 이용 산업별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 제조업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 공급망 탄소 관리 소프트웨어 시장 동향 및 인사이트

전 세계 공급망 전반에서 거세지는 스코프 3 공시 압력

공급망 탄소 관리 소프트웨어 시장에서는 전 세계 공급업체 네트워크 전반에 걸쳐, 보다 엄격한 Scope 3 정보 공개를 요구하는 기업들의 강력한 수요가 나타나고 있습니다. CSRD에 따라 최초로 보고서를 제출한 기업은 2025년에 2024 회계연도의 스코프 3 데이터를 보고함으로써, 이후 보고서를 제출할 기업들이 충족해야 할 증거 수준 및 재현성에 관한 모범 사례를 제시하는 기준을 확립했습니다. ESRS E1에서는 스코프 3가 기후 보고의 핵심으로 자리 잡고 있으며, 기업은 계속해서 모든 관련 범주를 평가하고 매년 일관된 방법을 적용해야 합니다. 공급업체 데이터는 다양한 시스템, 지역, 보고 형식에서 수집되므로, 수작업으로 파일을 관리하는 방식으로는 이러한 요구 사항을 충족하기 어렵습니다. 캘리포니아주의 기후 정보 공개 프레임워크 역시 미국에 본사를 둔 다국적 기업들에 대해 유사한 압력을 가하고 있어, 공급망 탄소 관리 소프트웨어 시장은 더 이상 유럽에 의해서만 형성되는 것이 아닙니다. 그 결과, 공급업체 데이터 수집, 배출 계수 적용, 감사 기록 관리, 그리고 대규모 보증 대응형 보고를 지원할 수 있는 플랫폼으로의 전환이 가속화되고 있습니다.

AI를 활용한 공급업체 데이터 통합 도입

공급망 탄소 관리 소프트웨어 시장이 확대되고 있는 또 다른 이유는 기업들이 데이터의 누락보다는 데이터의 불일치로 인해 어려움을 겪고 있다는 점에 있습니다. 공급업체의 배출량 기록은 대개 청구서, 제품 기록, 수명 주기 데이터베이스, ERP 내보내기 데이터 등에 분산되어 있으며, 각 출처마다 서로 다른 단위, 경계, 가정이 사용되고 있습니다. 따라서 데이터 조화는 단순한 보조 기능이 아니라 소프트웨어의 핵심적인 작업이 되었습니다. 2026년 3월, EcoVadis와 Watershed는 제휴를 맺고, 공급업체의 1차 데이터와 자동화된 신뢰도 평가를 결합함으로써, 시장이 단순한 데이터 수집을 넘어 신뢰도 점수 산정 및 증거 검증 단계로 전환되고 있음을 보여주었습니다. 2026년 5월, EcoVadis는 Workiva를 통해 자사의 네트워크를 확장하고, 공급업체의 탄소 데이터를 감사 대응 결과물이 필요한 보고 워크플로우와 더욱 긴밀하게 연계했습니다. 그 결과, 공급망 탄소 관리 소프트웨어 시장에서는 데이터 품질을 평가하고, 이상치를 감지하며, 대량공급업체 입력 데이터를 정식 보증 프로세스로 전환할 수 있는 공급업체가 높이 평가받고 있습니다.

공급업체 데이터의 심각한 누락과 배출 계수의 낮은 품질

공급망 탄소 관리 소프트웨어 시장에서 가장 큰 실무적 제약은 여전히 공급업체 데이터의 품질에 있습니다. 많은 기업들은 공급업체가 완전한 1차 배출 데이터를 제공하지 않거나, 검증하기 어려운 형식으로 제공하기 때문에 여전히 2차 추정치에 의존하고 있습니다. 이로 인해 보고서의 품질이 저하될 뿐만 아니라, 후속 단계의 계획 도구의 가치도 제한받게 됩니다. 일반적인 배출 계수가 현장 수준이나 국가 수준의 상황을 반영하지 못하는 경우, 이 문제는 더욱 심각해져 전 세계 공급망의 탄소 기준선에 중대한 왜곡을 초래할 가능성이 있습니다. SAP는 2026년 업데이트를 통해 농업 및 산업용 원자재에 대해 국가별 배출 계수를 추가함으로써 이 문제의 일부를 해결했습니다. 이는 구매자 측의 지리적 세분화에 대한 수요가 증가하고 있음을 보여줍니다. 공급업체의 참여가 개선되고 배출 계수 라이브러리의 정확도가 높아질 때까지는 공급망 탄소 관리 소프트웨어 시장이 조달 네트워크가 분산된 기업들의 도입 지연 문제에 계속해서 직면하게 될 것입니다.

부문별 분석

2025년 공급망 탄소 관리 소프트웨어 시장 매출액 중 솔루션이 68.74%를 차지했으며, 소프트웨어 라이선스가 여전히 지출의 가장 큰 비중을 차지했습니다. 이러한 우위는 기업이 우선 배출량 측정, 공급업체 데이터 수집 및 보고 관리에 필요한 핵심 플랫폼을 확보하는 초기 기업 구매 패턴을 반영한 것입니다. 또한, 구매자가 이 솔루션을 선호한 이유로는 향후 보증, 계획, 제품 수준 분석을 지원할 수 있는 공통 데이터 모델을 구축할 수 있다는 점이 꼽힙니다. 공급망 탄소 관리 소프트웨어 업계의 초기 구축 단계에서 대기업들은 외부 자문 지원을 추가하기 전에 안정적인 시스템이 필요했기 때문에 이 '플랫폼 우선'의 접근 방식은 타당했습니다. 솔루션 부문은 SaaS를 통한 제공의 이점도 누리고 있으며, 이를 통해 기업은 도입을 신속하게 진행할 수 있게 되었고, 분산된 공급업체 네트워크 전반에 걸쳐 시스템을 보다 쉽게 업데이트할 수 있게 되었습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 17.65%로 확대될 것으로 예상되며, 가장 빠르게 성장하는 분야로 꼽히고 있습니다. 이러한 성장은 많은 기업이 소프트웨어 구매라는 첫 단계를 넘어, 현재는 복잡한 공급업체 생태계 전반에 걸쳐 소프트웨어를 활용하기 위한 지원이 필요하다는 점을 보여줍니다. CSRD 보증 워크플로우, 공급업체와의 협업, 데이터 정제, 배출 계수 대조 등은 모두 업무 부담이 커서 사내 팀만으로는 감당하기 어려운 경우가 많습니다. ERM과 Carbmee의 제휴는 소프트웨어 기능과 서비스 중심의 실행을 결합하여 제조 밸류체인 내의 Scope 3 감축 활동을 추진함으로써 이러한 변화를 반영하고 있습니다. 따라서 공급망 탄소 관리 소프트웨어 시장은 서비스가 초기 설정에 그치지 않고, 지속적인 데이터 관리, 공급업체와의 연계, 탈탄소화의 지속적인 실행까지 포함하는 모델로 전환되고 있습니다. 이러한 추세로 인해, 장기적인 도입 주기를 지원하고 초기 도입 완료 후에도 측정 가능한 성과를 제공할 수 있는 벤더나 파트너의 입지가 강화될 것입니다.

공급망 탄소 관리 소프트웨어 시장에서 2025년 매출의 65.12%를 클라우드 도입이 차지했으며, 이것이 주요 제공 모델로 자리 잡고 있습니다. 클라우드 플랫폼은 대규모 사내 인프라가 필요 없이 조달, 재무, 물류 시스템에서 데이터를 자동으로 수집함으로써 조기에 시장 점유율을 확보했습니다. 또한, 신속한 구축, 초기 비용 절감, 공급업체 네트워크 전반으로의 손쉬운 확장을 원하는 지속가능성 팀의 요구 사항도 충족시키고 있습니다. 많은 중견 기업에게 클라우드 시스템은 사내 서버의 유지 관리 부담을 줄여주는 동시에, 실시간 보고서 작성 요구에도 부응했습니다. 공급망 탄소 관리 소프트웨어 시장에서 클라우드가 차지하는 주도적인 위상은 규제 및 보고 요건이 얼마나 빠르게 변화하고 있는지를 반영하고 있습니다. 이는 구매자들이 빈번한 업데이트와 기능 도입의 용이성을 중요하게 여기기 때문입니다.

하이브리드 방식은 2031년까지 연평균 성장률(CAGR) 17.85%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 도입 형태입니다. 이러한 성장은 클라우드 규모의 연결성을 필요로 하면서도, 기밀성이 높은 공급업체 데이터 및 운영 데이터를 관리된 지역 환경 내에 보관해야 하는 기업들에 기인한 것입니다. 이 요건은 데이터 거버넌스 및 데이터 소재지 요건이 시스템 설계의 선택지를 좌우하는 유럽에서 특히 중요합니다. SAP의 실적 관리 아키텍처는 이러한 방향성을 보여주고 있습니다. 기업은 클라우드 환경에서 탄소 데이터를 산출하고, 필요에 따라 그 결과를 온프레미스 시스템에 공개할 수 있습니다. 온프레미스 배포는 국방, 정부 및 엄격하게 규제되는 공급망 분야에서 여전히 중요한 역할을 하고 있지만, 공급업체의 신속한 온보딩이나 지속적인 업데이트와 같은 요구 사항에는 그다지 적합하지 않습니다. 그 결과, 공급망 탄소 관리 소프트웨어 시장에서는 규정 준수 관리와 실용적인 확장성을 결합한 하이브리드 모델이 점점 더 많은 지지를 얻고 있습니다.

지역별 분석

2025년, 유럽은 매출 점유율 34.56%를 차지했으며, 공급망 탄소 관리 소프트웨어 시장에서 1위를 차지했습니다. 해당 지역은 정책 수립에서 실제 운영으로의 전환 과정에서 가장 앞서 있다고 할 수 있습니다. 이는 대기업들이 이미 CSRD 관련 요건에 따라 스코프 3 보고 주기를 완전히 마쳤기 때문입니다. 또한, 유럽공급망 탄소 관리 소프트웨어 시장은 CSRD, EU 배출권 거래 제도(ETS), CBAM, 그리고 제품 여권 도입 준비와 같은 요인들이 복합적으로 작용하여 기업 차원과 제품 차원 모두에서 데이터 수요를 창출하고 있다는 점에서도 혜택을 보고 있습니다. 독일은 자동차 및 산업 공급망이 제품의 탄소 발자국에 대한 요구 사항과 공급업체 데이터의 상세한 수집 요건 모두에 크게 노출되어 있기 때문에 특히 두드러집니다. 프랑스와 네덜란드 역시 보고 제도 도입, 수출입 활동, 그리고 대기업의 높은 집중도로 인해 계속해서 중요한 수요 거점으로 자리 잡고 있습니다.

북미는 미국의 다국적 기업, 캘리포니아주의 공시 의무, 그리고 대기업들의 적극적인 자율 목표 설정을 바탕으로 지역별 시장 중 2위의 규모를 차지하고 있습니다. 미국의 구매 기업들은 복잡한 국내외 공급망 전반에 걸친 전사적 배출량 산정을 지원할 수 있는 시스템이 필요하기 때문에 계속해서 투자를 진행하고 있습니다. 캐나다에서도 탄소 가격 제도와 국경을 넘는 고객 보고 요건으로 인해 유사한 요구가 대두되고 있으며, 여러 관할 구역에 걸친 보고 로직을 갖춘 소프트웨어가 요구되고 있습니다. 남미는 여전히 도입의 최전선에 있지만, 브라질에서는 기업의 지속가능성에 대한 기대가 높아지고, 그린 파이낸스 활동이 체계적인 배출량 보고를 뒷받침함에 따라 그 기세가 더욱 거세지고 있습니다.

아시아태평양은 2031년까지 18.12%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측되며, 공급망 탄소 관리 소프트웨어 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 해당 지역은 국내 기후 정책과 유럽 및 북미 고객들의 수출 관련 규정 준수 요건에 따라 형성되어 있습니다. 중국은 '이산화탄소 배출 정점 도달·탄소 중립' 목표와 배출권 거래 제도의 광범위한 발전을 통해, 스코프 3 및 기업의 탄소 데이터를 더욱 중요한 과제로 자리매김하고 있습니다. 인도에서는 '에너지 절약 체계', '탄소 크레딧 거래 제도' 및 상장 기업에 대한 BRSR 핵심 요건을 통해 시장에 활기가 더해지고 있습니다. 일본에서는 GX 자금, 지속가능성에 관한 지침, 상장 기업에 대한 공시 압박을 통해 프리미엄 수요가 뒷받침되고 있습니다. 한편, 중동 및 아프리카에서는 '사우디 비전 2030', 'UAE 넷제로 2050', 그리고 남아프리카공화국과 나이지리아의 탄소 정책 수립과 연계된 기업의 탈탄소화 노력에 힘입어, 시장이 조기에 확대되기 시작하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the supply chain carbon management software market size was valued at USD 3.11 billion in 2025 and estimated to grow from USD 3.60 billion in 2026 to reach USD 7.96 billion by 2031, at a CAGR of 17.20% during the forecast period (2026-2031).

This report is Segmented by Offering (Software, and Services), Deployment Model (Cloud, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Carbon Accounting and Emissions Tracking, and More), End-Use Industry (IT and Telecom, BFSI, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Supply Chain Carbon Management Software Market Trends and Insights

Rising Scope 3 Disclosure Pressure Across Global Supply Chains

The supply chain carbon management software market is seeing strong demand from companies that now need more rigorous Scope 3 disclosures across global supplier networks. The first CSRD filers reported 2024 fiscal-year Scope 3 data in 2025, creating a live benchmark for the level of evidence and repeatability that later filers now need to meet. ESRS E1 kept Scope 3 at the center of climate reporting, meaning companies still need to assess all relevant categories and apply consistent methods year over year. That requirement is difficult to manage in manual files because supplier data comes from many systems, geographies, and reporting formats. California's climate disclosure framework is intensifying the same pressure on U.S.-based multinationals, so the supply chain carbon management software market is no longer being shaped solely by Europe. The result is a faster move toward platforms that can collect supplier data, apply emissions factors, maintain audit trails, and support assurance-ready reporting at scale.

Adoption of AI-Based Supplier Data Harmonization

The supply chain carbon management software market is also expanding because enterprises are struggling less with missing data than with inconsistent data. Supplier emissions records often sit across invoices, product records, life cycle databases, and ERP exports, and each source uses different units, boundaries, and assumptions. That makes harmonization a core software task rather than a supporting feature. In March 2026, EcoVadis and Watershed partnered to combine supplier primary data with automated reliability grading, demonstrating how the market is moving toward confidence scoring and evidence checks rather than simple data intake. In May 2026, EcoVadis expanded the same network through Workiva, further connecting supplier carbon data with reporting workflows that require audit-ready outputs. As a result, the supply chain carbon management software market is rewarding vendors that can rank data quality, detect outliers, and move high-volume supplier inputs into formal assurance processes.

High Supplier Data Gaps and Poor Emissions Factor Quality

The biggest practical constraint in the supply chain carbon management software market remains supplier data quality. Many enterprises still rely on secondary estimates because suppliers do not provide complete primary emissions data, or they do so in formats that cannot be easily verified. That weakens reporting quality and also limits the value of downstream planning tools. The challenge becomes harder when generic emissions factors do not reflect site-level or country-level conditions, which can materially distort carbon baselines for global supply chains. SAP addressed part of this issue in its 2026 updates by adding more country-specific factors for agricultural and industrial commodities, indicating that buyer demand for geographic granularity is growing. Until supplier participation improves and emissions factor libraries become more precise, the supply chain carbon management software market will continue to face slower adoption among companies with fragmented sourcing networks.

Other drivers and restraints analyzed in the detailed report include:

- Digital Product Passport Readiness in Export-Oriented Manufacturing

- Procurement-Led Decarbonization Programs in Large Enterprises

- Integration Burden With Legacy ERP, TMS, And MES Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 68.74% of 2025 revenue in the supply chain carbon management software market, with software licenses remaining the largest component of spending. That lead reflected early enterprise buying patterns, in which companies first secured the core platform needed for emissions measurement, supplier data capture, and reporting controls. Buyers also preferred solutions because they established a common data model that could later support assurance, planning, and product-level analysis. In the early build-out stage of the supply chain carbon management software industry, this platform-first approach made sense because large enterprises needed a stable system before adding external advisory support. The solutions segment also benefited from SaaS delivery, which enabled companies to onboard faster and update their systems more easily across distributed supplier networks.

The services segment is projected to expand at a 17.65% CAGR through 2031, which makes it the fastest-growing component. That rise shows that many enterprises have moved past the first step of buying software and now need help using it across complex supplier ecosystems. CSRD assurance workflows, supplier outreach, data cleaning, and emissions factor matching are all work-intensive tasks that internal teams often cannot absorb. The ERM and Carbmee partnership reflects this shift by combining software capabilities with service-led execution to drive Scope 3 reduction work in manufacturing value chains. The supply chain carbon management software market is therefore moving toward a model in which services extend beyond setup to include continuous data management, supplier engagement, and decarbonization follow-through. That pattern strengthens vendors and partners that can support long implementation cycles and deliver measurable outcomes after the initial deployment is complete.

Cloud deployment accounted for 65.12% of 2025 revenue in the supply chain carbon management software market, making it the dominant delivery model. Cloud platforms gained early market share by enabling automated data ingestion from procurement, finance, and logistics systems without the need for extensive internal infrastructure. They also meet the needs of sustainability teams that want faster setup, lower upfront costs, and easier expansion across supplier networks. For many mid-sized adopters, cloud systems reduced the burden of maintaining internal servers while supporting live reporting needs. Cloud leadership in the supply chain carbon management software market also reflects how quickly regulatory and reporting requirements evolve, because buyers value frequent updates and easier feature rollouts.

Hybrid deployment is projected to grow at a 17.85% CAGR through 2031, which makes it the fastest-growing mode. This growth comes from enterprises that need cloud-scale connectivity but still must keep sensitive supplier or operational data within controlled regional environments. That requirement is particularly relevant in Europe, where data governance and residency expectations shape system design choices. SAP's footprint management architecture demonstrates this direction, as companies can calculate carbon data in cloud environments and publish results back to on-premises systems when needed. On-premises deployments still hold a role in defense, government, and tightly regulated supply chains, but they are less aligned with the need for fast supplier onboarding and continuous updates. As a result, the supply chain carbon management software market is increasingly favoring hybrid models that combine compliance control with practical scalability.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small And Medium Enterprises

- By Application

- Carbon Footprint Measurement and Tracking

- Emissions Reporting and Compliance

- Supplier Engagement and Data Collection

- Product Carbon Footprint Assessment

- Climate Risk Analysis

- Decarbonization Strategy and Planning

- By End-Use Industry

- Manufacturing

- Retail and E-Commerce

- Transportation and Logistics

- Energy and Utilities

- Food and Beverage

- IT and Telecom

- BFSI

- Construction and Infrastructure

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe held a 34.56% revenue share in 2025, making it the leading position in the supply chain carbon management software market. The region moved furthest from policy planning to live implementation because large companies have already completed full Scope 3 reporting cycles under CSRD-linked requirements. The supply chain carbon management software market also benefits in Europe from the combined effect of CSRD, the EU Emissions Trading System, CBAM, and product passport preparation, which together create both corporate and product-level data needs. Germany stands out because its automotive and industrial supply chains face high exposure to both product carbon footprint demands and deep supplier data collection requirements. France and the Netherlands also remain important demand centers due to reporting adoption, import-export activity, and a high concentration of large enterprises.

North America represented the second-largest regional market, supported by U.S. multinationals, California disclosure mandates, and strong voluntary target-setting among large companies. Buyers in the United States continue to invest because they need systems that can support enterprise-wide emissions accounting across complex domestic and overseas supplier networks. Canada adds a similar need through carbon pricing and cross-border customer reporting requirements, which favor software with multi-jurisdiction reporting logic. South America remains at the forefront of adoption, but Brazil is building momentum as corporate sustainability expectations rise and green finance activity drives structured emissions reporting.

Asia-Pacific is projected to post the fastest CAGR of 18.12% through 2031, making it the strongest growth region in the supply chain carbon management software market. The region is being shaped by domestic climate policies and by export-linked compliance needs from customers in Europe and North America. China is pushing Scope 3 and enterprise carbon data higher on the agenda through its dual-carbon goals and the broader evolution of its emissions trading framework. India is adding momentum through the Energy Conservation framework, the Carbon Credit Trading Scheme, and BRSR Core expectations for listed companies. Japan supports premium demand through GX funding, sustainability guidance, and listed-company disclosure pressure, while the Middle East and Africa are beginning to see earlier traction through enterprise decarbonization efforts tied to Saudi Vision 2030, UAE Net Zero 2050, and carbon policy development in South Africa and Nigeria.

- IBM Corporation

- SAP SE

- Microsoft Corporation

- Schneider Electric SE

- Salesforce, Inc.

- Sphera Solutions, Inc.

- Workiva Inc.

- ENGIE SA

- Watershed, Inc.

- Persefoni AI, Inc.

- Plan A ESG GmbH

- Greenly SAS

- Emitwise Ltd.

- Sweep SAS

- Carbon Direct, Inc.

- Carbmee GmbH

- Cority Software Inc.

- Diligent Corporation

- Wolters Kluwer N.V.

- Sinai Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Scope 3 Disclosure Pressure Across Global Supply Chains

- 4.2.2 Adoption of AI-Based Supplier Data Harmonization

- 4.2.3 Digital Product Passport Readiness in Export-Oriented Manufacturing

- 4.2.4 Procurement-Led Decarbonization Programs in Large Enterprises

- 4.2.5 Carbon Credit and Internal Carbon Price Workflow Integration

- 4.2.6 Embedded Carbon Analytics in ERP and Procurement Suites

- 4.3 Market Restraints

- 4.3.1 High Supplier Data Gaps and Poor Emissions Factor Quality

- 4.3.2 Integration Burden with Legacy ERP, TMS, and MES Systems

- 4.3.3 Audit-Grade Cybersecurity and Data Privacy Concerns

- 4.3.4 Budget Sensitivity Among Mid-Market and SME Buyers

- 4.4 Industry Macroeconomic Factors and Their Impact

- 4.5 Industry Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small And Medium Enterprises

- 5.4 By Application

- 5.4.1 Carbon Footprint Measurement and Tracking

- 5.4.2 Emissions Reporting and Compliance

- 5.4.3 Supplier Engagement and Data Collection

- 5.4.4 Product Carbon Footprint Assessment

- 5.4.5 Climate Risk Analysis

- 5.4.6 Decarbonization Strategy and Planning

- 5.5 By End-Use Industry

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-Commerce

- 5.5.3 Transportation and Logistics

- 5.5.4 Energy and Utilities

- 5.5.5 Food and Beverage

- 5.5.6 IT and Telecom

- 5.5.7 BFSI

- 5.5.8 Construction and Infrastructure

- 5.5.9 Government and Public Sector

- 5.5.10 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 SAP SE

- 6.4.3 Microsoft Corporation

- 6.4.4 Schneider Electric SE

- 6.4.5 Salesforce, Inc.

- 6.4.6 Sphera Solutions, Inc.

- 6.4.7 Workiva Inc.

- 6.4.8 ENGIE SA

- 6.4.9 Watershed, Inc.

- 6.4.10 Persefoni AI, Inc.

- 6.4.11 Plan A ESG GmbH

- 6.4.12 Greenly SAS

- 6.4.13 Emitwise Ltd.

- 6.4.14 Sweep SAS

- 6.4.15 Carbon Direct, Inc.

- 6.4.16 Carbmee GmbH

- 6.4.17 Cority Software Inc.

- 6.4.18 Diligent Corporation

- 6.4.19 Wolters Kluwer N.V.

- 6.4.20 Sinai Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment