|

시장보고서

상품코드

2073061

코어 라우터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Core Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

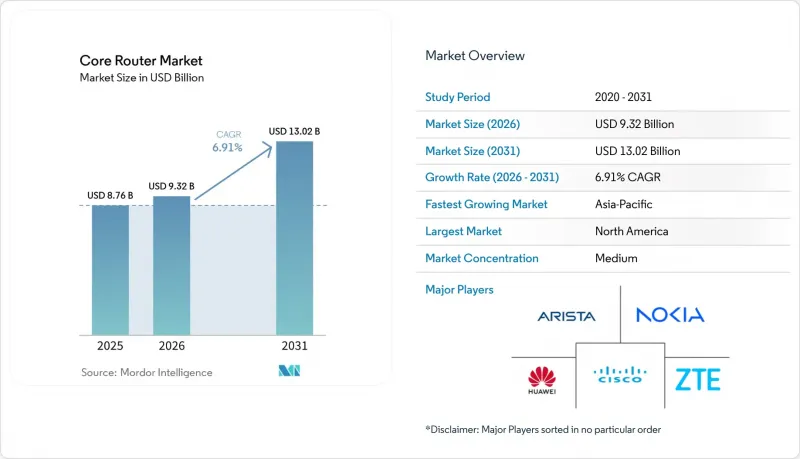

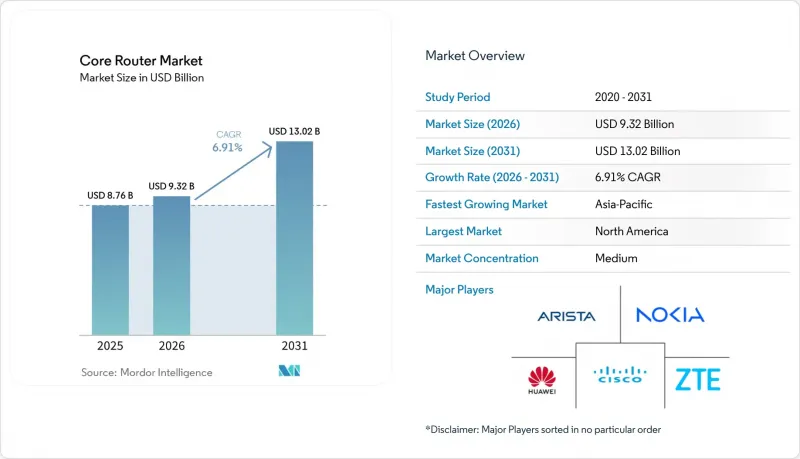

Mordor Intelligence에 의하면, 코어 라우터 시장 규모는 2025년에 87억 6,000만 달러에 이르고, 2026년에는 93억 2,000만 달러, 2031년까지 130억 2,000만 달러에 이를 것으로 예상되고 있어 2026-2031년까지 CAGR 6.91%로 성장할 전망입니다.

본 보고서는 하드웨어 아키텍처(고정형 코어 라우터, 모듈형/섀시형 코어 라우터, 기타), 처리량 등급(저처리량, 중처리량, 기타), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 제조, 정부·공공 부문, 기타), 인터페이스 밀도 등급(저밀도, 중밀도, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 코어 라우터 시장 동향 및 분석

5G 백본의 도입 확대

통신 사업자들은 4G 패킷 코어에서 더 높은 처리량, 마이크로서비스의 하위 세분화, 네트워크 슬라이싱이 필요한 독립형 5G 아키텍처로 전환하고 있습니다. 소프트뱅크는 2025년 12월에 상용 SRv6 모바일 사용자 플레인을 본격적으로 가동하여, ArcOS를 실행하는 Jericho2 ASIC에서 10밀리초 미만의 지연을 실현했습니다. 이에 이어 KDDI는 게임 및 로봇용 워크로드에 대해 지리적으로 중복된 장애 복구 기능을 제공하는 삼성의 전국 규모 5G SA 코어를 도입했습니다. 2026년 3월 에릭슨과 소프트뱅크가 체결한 계약에 따라 듀얼 모드 5G 코어 기능과 가입자 데이터의 통합이 추가되면서, 백본 라우터의 패킷 처리 부하가 증가하고 있습니다. 컨테이너화된 네트워크 기능은 데이터센터 내의 동서 방향 트래픽을 증가시켜, 스파인 라우터의 슬롯 업그레이드를 가속화하고 있습니다. 이러한 연쇄적인 영향으로 인해 5G 전송은 코어 라우터 시장에서 여전히 가장 중요한 성장 요인 중 하나로 자리 잡고 있습니다.

하이퍼스케일 데이터센터의 확대

알파벳은 2026년 인프라 투자로 1,750억-1,850억 달러를 예산에 반영했으며, 각 하이퍼스케일러 기업의 총 지출액은 6,900억 달러를 넘어 수백 개에 달하는 새로운 가용성 영역 구축을 뒷받침하고 있습니다. 알리스타의 R4 섀시는 800 Gbps 포트 576개와 HyperPort 3.2 Tbps 인터페이스를 갖추고 있으며, 실험실 테스트에서 AI 작업 실행 시간을 44% 단축했습니다. 화웨이의 CloudEngine XH9230-128DQ-LC 고정형 스위치는 완전한 수냉 방식을 채택하여 51.2 Tbps의 처리 능력을 실현하고, 랙 활용도를 2배로 높였습니다. 이러한 플랫폼들은 비트당 전력 소비를 줄이면서 GPU 클러스터의 성장을 지속하고, 엄격한 PUE 목표를 달성하고 있습니다. 워크로드가 메가 캠퍼스로 집중됨에 따라, 고밀도 코어 라우터는 중요한 집약 지점이 되어 코어 라우터 시장을 테라비트 패브릭으로 이끌고 있습니다.

높은 초기 설비 투자액

800Gbps 인터페이스를 탑재한 섀시의 가격은 100만 달러 이상이며, 광 모듈, 이중화된 전원 공급 장치(PSU), 지원 계약 등으로 인해 총 소유 비용이 더욱 증가합니다. 지역 통신사들은 규제상의 의무나 서비스 품질 저하가 예산상의 신중함을 상회할 때까지 업그레이드를 미루고 있습니다. 인도의 결제 네트워크는 SONiC의 화이트박스 라우터로 전환함으로써 총 비용을 40% 절감했으며, 라쿠텐 모바일도 디스어그리게이트형 하드웨어를 통해 설비 투자(CAPEX)를 절반으로 줄였지만, 소규모 통신 사업자의 경우 멀티벤더 스택을 통합할 기술 인력이 부족합니다. 그 결과, 많은 중견 통신사업자들이 여전히 통합형 시스템을 발주하고 있어, 코어 라우터 시장 전체의 판매량 증가세를 둔화시키고 있습니다.

부문별 분석

모듈형 섀시 플랫폼은 현장에서 교체 가능한 라인 카드, 이중화된 제어 플레인, 검증된 페일오버 소프트웨어를 통해 2025년 코어 라우터 시장 점유율의 58.42%를 차지했습니다. 이러한 섀시를 활용한 코어 라우터 시장 규모는 검증된 가용성 벤치마크를 중시하는 기존 통신 사업자들의 수십 년에 걸친 교체 주기의 혜택을 받고 있습니다. 내장된 텔레메트리 기능과 캐리어급 클럭킹 기능을 통해 규제 환경에서의 규정 준수 절차가 간소화됩니다. 그러나 비트당 비용이라는 지표로 보면, 시판되는 실리콘을 채택한 화이트박스 단말기가 우위를 점하고 있습니다.

AT&T의 백본 네트워크에서는 현재 하루 840PB 트래픽의 80% 이상을 범용 ASIC에서 구동되는 DriveNets 소프트웨어를 통해 처리하고 있으며, 디스어그리게이트형 라우터 시장은 연평균 성장률(CAGR) 8.94%로 확대되고 있습니다. Comcast와 KDDI도 이 모델을 재현하고 있으며, SONiC는 하이퍼스케일러형 도입에 있어 사실상 운영 체제 역할을 하고 있습니다. 초기 시스템 통합은 여전히 복잡하지만, 성공적인 구축 사례를 통해 인식되는 위험은 줄어들고 있습니다. 하이퍼스케일러들이 툴체인을 오픈소스로 공개함에 따라 서비스 제공업체에 대한 신뢰도가 높아지고 있으며, 코어 라우터 시장에서 디어그리게이션의 추세가 지속되고 있습니다.

100 Gbps를 초과하는 초고속 처리량 라우터는 2025년에 시장 매출의 62.18%를 차지할 것으로 보이며, AI 클러스터의 백엔드 네트워크, DCI 링크, 5G 사용자 플레인 게이트웨이에 힘입어 2031년까지 연평균 성장률(CAGR) 7.82%로 성장할 전망입니다. 시스코의 “Silicon One G300”는 25.6Tbps의 패브릭을 구현하여, 통신 사업자가 지연 시간이 중요한 워크로드에서 3계층 토폴로지를 2계층으로 통합할 수 있게 됩니다. 네덜란드의 KPN이 800Gbps 코히런트 전송에 도입한 주니퍼의 모듈형 라우터 ‘PTX12000”는 노키아의 FP5 포토닉 프로세서를 채택하여, 이전 세대에 비해 비트당 전력 소비를 75% 줄였으며, 유럽 규제 당국이 요구하는 지속가능성 요건을 직접 충족하고 있습니다.

10-100Gbps의 고처리량 플랫폼은 여전히 기업 캠퍼스 코어 및 지역 집약 지점에서 사용되고 있지만, 통신 사업자들이 운영상의 복잡성과 설치 면적을 줄이기 위해 트래픽을 더 적은 수의 대용량 장치로 집약함에 따라 그 점유율은 점차 줄어들고 있습니다. 10-100Gbps 범위에 속하는 미드레인지 플랫폼은 여전히 캠퍼스 및 코어 네트워크에서 사용되고 있지만, 통신 사업자들이 초대용량 노드로의 통합을 추진함에 따라 그 점유율은 줄어들고 있습니다. 저용량 대역 플랫폼은 여전히 산업용 IoT 및 지방의 백홀에서 사용되고 있습니다. QSFP-DD800 광 모듈의 양산 및 수냉식 1.6Tbps 모듈의 개발이 로드맵에 포함된 점을 고려할 때, 초대용량 부문은 앞으로도 기술 발전의 방향을 주도하며 코어 라우터 시장에서의 매출 점유율을 지속적으로 확대해 나갈 것으로 보입니다.

지역별 분석

북미는 하이퍼스케일러의 자본 투자 프로그램과 Open RAN 시범 도입이 막대한 포트 수를 흡수함에 따라, 2025년 지출의 36.22%를 차지했습니다. Alphabet, Microsoft, Amazon, Meta 등 4개사는 2026년 인프라 구축에 총 약 6,900억 달러를 책정하고 있으며, 800 Gbps 인터페이스를 갖춘 고대역폭 섀시에 대한 수주를 주도하고 있습니다. AT&T가 미국 전역 규모로 진행하는 ‘DriveNets”라는 전개는 해당 지역에서 분산형 소프트웨어 스택의 조기 도입을 시사하고 있습니다. 알래스카의 GCI 등 지역 통신 사업자들은 듀얼 모드 5G 코어 운영을 에릭슨에 위탁하고 있으며, 혹독한 기후에도 불구하고 도입을 가속화하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 7.88%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 소프트뱅크의 SRv6 도입은 일본 내 고도화된 라우팅 프로토콜에 대한 수요가 높음을 보여줍니다. KDDI의 DriveNets 제휴는 개방형 아키텍처에 대한 폭넓은 수용을 입증하고 있습니다. 인도의 HFCL과 Vodafone Idea 간의 계약에서는 섀시를 교체하지 않고 10Gbps 노드를 100Gbps로 확장함으로써, 비용 효율성을 중시하는 혁신이 두드러집니다. 중국의 각 하이퍼스케일러 기업들은 무손실 이더넷 패브릭이 필요한 AI 메가클러스터를 구축하고 있는 반면, 한국의 통신 사업자들은 자율주행차를 위해 5G SA 슬라이싱을 도입하고 있습니다.

유럽에서는 에너지 효율에 관한 법규, 5G SA로의 업그레이드, 엣지 데이터센터 구축이 진행되는 가운데, 꾸준히 발전하고 있습니다. Wind Tre의 네트워크 통합과 노키아, 텔레포니카 에스파냐와의 독점 계약은 초저지연 지역 시설로의 전환을 상징합니다. 중동에서는 스마트시티 목표 달성을 위해 광섬유 백홀에 대한 투자가 진행되고 있으며, 아프리카에서는 2026년 3월 에티오피아와 에릭슨(Ericsson)이 체결한 프로젝트 등 현대화 협정을 통해 서비스가 미치지 않는 지역의 주민들에게도 4G/5G 통신 범위가 확대되고 있습니다. 라틴아메리카에서는 거시경제적 제약이 심화되고 있음에도 불구하고, 브라질과 아르헨티나에서 5G 통신 범위가 확대되면서 코어 라우터 시장 수요를 견인하는 ‘쌍둥이 엔진”은 북미와 아시아태평양으로 구성되어 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the core router market size reached USD 8.76 billion in 2025 and is expected to reach USD 9.32 billion in 2026 and USD 13.02 billion by 2031, growing at a CAGR of 6.91% from 2026 to 2031.

This report is Segmented by Hardware Architecture (Fixed Core Routers, Modular/Chassis-based Core Routers, and More), Throughput Class (Low Throughput, Mid Throughput, and More), End User Industry (BFSI, IT and Telecom, Manufacturing, Government and Public Sector, and More), Interface Density Class (Low Density, Medium Density, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Core Router Market Trends and Insights

Rising 5G Backbone Deployments

Operators are migrating from 4G packet cores to standalone 5G architectures that demand higher throughput, microservice granularity, and network slicing. SoftBank's commercial SRv6 mobile user plane went live in December 2025, proving sub-10 ms latency on Jericho2 ASICs running ArcOS. KDDI followed with a nationwide Samsung 5G SA core that delivers geo-redundant failover for gaming and robotics workloads. Ericsson's March 2026 deal with SoftBank adds dual-mode 5G core functions and subscriber data consolidation, increasing packet-processing loads on backbone routers. Containerized network functions amplify east-west traffic inside data centers, accelerating slot upgrades on spine routers. The cascading impact keeps 5G transport among the most material growth levers for the core router market.

Hyperscale Data Center Expansion

Alphabet budgeted USD 175 billion-USD 185 billion for 2026 infrastructure, and combined hyperscaler outlays top USD 690 billion, underwriting hundreds of new availability zones. Arista's R4 chassis offers 576 ports of 800 Gbps and HyperPort 3.2 Tbps interfaces that trimmed AI job time by 44% in lab tests. Huawei's CloudEngine XH9230-128DQ-LC fixed switch pushes 51.2 Tbps using full liquid cooling, doubling rack utilization. These platforms lower power per bit, meeting stringent PUE targets while sustaining GPU cluster growth. As workloads centralize into mega-campuses, high-density core routers become critical aggregation points, propelling the core router market toward terabit fabrics.

High Initial Capital Expenditure

Chassis with 800 Gbps interfaces list above USD 1 million, and optics, redundant PSUs, and support contracts amplify lifetime cost. Regional carriers delay upgrades until regulatory mandates or service degradation override budget caution. Indian payments networks cut total cost by 40% after shifting to SONiC white-box routers, and Rakuten Mobile halved CAPEX with disaggregated hardware, yet smaller operators lack the engineering staff to integrate multivendor stacks. Consequently, many mid-tier providers still order integrated systems, muting unit volume growth across the core router market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in AI-Driven Traffic Engineering

- Cloud Service Provider CAPEX Upswing

- Supply-Chain Volatility in High-Speed ASICs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modular chassis platforms captured 58.42% of the core router market share in 2025 through field-replaceable line cards, redundant control planes, and mature failover software. The core router market size for these chassis benefited from decades-long refresh cycles among incumbent telcos that value proven availability benchmarks. Their embedded telemetry and carrier-grade clocking simplify compliance in regulated environments. However, cost-per-bit metrics favor merchant-silicon white-box devices.

Disaggregated routers are expanding at an 8.94% CAGR as AT&T's backbone now moves more than 80% of its 840 PB daily load on DriveNets software running across generic ASICs. Comcast and KDDI are replicating this model, and SONiC has become the de facto operating system for hyperscaler-style deployments. Although initial systems integration remains complex, successful reference builds are reducing perceived risk. As hyperscalers open-source toolchains, service providers gain confidence, sustaining momentum for disaggregation within the core router market.

Ultra-high-throughput routers exceeding 100 Gbps commanded 62.18% of market revenue in 2025 and will grow at a 7.82% CAGR through 2031, driven by AI cluster back-end networks, DCI links, and 5G user-plane gateways. Cisco's Silicon One G300 enables 25.6 Tbps fabrics, letting operators collapse three-tier topologies into two layers for latency-critical workloads. Juniper's PTX12000 modular router, deployed by KPN in the Netherlands for 800 Gbps coherent transport, uses Nokia's FP5 photonic processor to achieve a 75% per-bit power reduction compared with prior generations, directly addressing sustainability mandates from European regulators.

High-throughput platforms above 10 Gbps but below 100 Gbps continue to serve enterprise campus cores and regional aggregation points, yet their share is eroding as operators consolidate traffic onto fewer, higher-capacity devices to reduce operational complexity and footprint. Mid-range platforms in the 10-100 Gbps span still serve campus cores, yet their share erodes as operators consolidate onto fewer ultra-high-capacity nodes. Low tiers linger in industrial IoT or rural backhaul. With QSFP-DD800 optics in volume and liquid-cooled 1.6 Tbps modules on the roadmap, the ultra-high segment will continue guiding technology direction and grabbing wallet share inside the core router market.

Complete Report Scope:

- By Hardware Architecture

- Fixed Core Routers

- Modular / Chassis-based Core Routers

- Disaggregated (White-box) Core Routers

- By Throughput Class

- Low Throughput (<1 Gbps)

- Mid Throughput (1-10 Gbps)

- High Throughput (10-100 Gbps)

- Ultra-High (>100 Gbps)

- By End User Industry

- BFSI

- IT and Telecom

- Manufacturing

- Government and Public Sector

- Healthcare and Lifesciences

- Retail and E-commerce

- Education

- Other End User Industries

- By Interface Density Class

- Low Density (<64 ports)

- Medium Density (64-256 ports)

- High Density (>256 ports)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America generated 36.22% of 2025 spending as hyperscaler capital programs and Open RAN pilots absorbed vast port volumes. Alphabet, Microsoft, Amazon, and Meta together earmarked nearly USD 690 billion for 2026 infrastructure builds, funneling orders to high-bandwidth chassis with 800 Gbps interfaces. AT&T's nationwide DriveNets rollout shows the region's early adoption of disaggregated software stacks. Rural carriers, such as GCI in Alaska, outsource dual-mode 5G core operations to Ericsson, accelerating deployments despite harsh climates.

Asia-Pacific is the fastest-growing territory at a 7.88% CAGR. SoftBank's SRv6 launch illustrates Japan's appetite for advanced routing protocols. KDDI's DriveNets partnership underscores broader acceptance of open architectures. India's HFCL contract with Vodafone Idea expands 10 Gbps nodes to 100 Gbps without chassis swaps, highlighting cost-sensitive innovation. Chinese hyperscalers are erecting AI mega-clusters that demand lossless Ethernet fabrics, while South Korean telcos deploy 5G SA slicing for autonomous vehicles.

Europe advances steadily as energy-efficiency legislation, 5G SA upgrades, and edge data center rollouts unfold. Wind Tre's network consolidation and Nokia's exclusive deal with Telefonica Espana exemplify the move toward ultra-low-latency regional facilities. The Middle East invests in fiber backhaul to meet smart-city targets, and Africa's modernization agreements, such as Ethio-Ericsson's March 2026 project, extend 4G/5G coverage to underserved populations. Latin America widens 5G coverage in Brazil and Argentina, albeit under tighter macro constraints, leaving North America and Asia-Pacific as the twin engines of volume for the core router market.

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- ZTE Corporation

- Arista Networks, Inc.

- Extreme Networks, Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Ciena Corporation

- Ericsson AB

- NEC Corporation

- Ribbon Communications Inc.

- Edgecore Networks Corporation

- ADVA Optical Networking SE

- ADTRAN Holdings, Inc.

- Infinera Corporation

- Casa Systems, Inc.

- ALE International SAS (Alcatel-Lucent Enterprise)

- Fujitsu Limited

- Tellabs Access LLC

- DriveNets Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising 5G Backbone Deployments

- 4.2.2 Hyperscale Data Center Expansion

- 4.2.3 Surge in AI-Driven Traffic Engineering

- 4.2.4 Cloud Service Provider CAPEX Upswing

- 4.2.5 Adoption of Disaggregated Routing Architectures

- 4.2.6 Sustainability-Focused Hardware Refresh Programs

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Expenditure

- 4.3.2 Supply-Chain Volatility in High-Speed ASICs

- 4.3.3 Skills Gap in Programmable Networking

- 4.3.4 Long Depreciation Cycles Limiting Refresh Rates

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Hardware Architecture

- 5.1.1 Fixed Core Routers

- 5.1.2 Modular / Chassis-based Core Routers

- 5.1.3 Disaggregated (White-box) Core Routers

- 5.2 By Throughput Class

- 5.2.1 Low Throughput (<1 Gbps)

- 5.2.2 Mid Throughput (1-10 Gbps)

- 5.2.3 High Throughput (10-100 Gbps)

- 5.2.4 Ultra-High (>100 Gbps)

- 5.3 By End User Industry

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Manufacturing

- 5.3.4 Government and Public Sector

- 5.3.5 Healthcare and Lifesciences

- 5.3.6 Retail and E-commerce

- 5.3.7 Education

- 5.3.8 Other End User Industries

- 5.4 By Interface Density Class

- 5.4.1 Low Density (<64 ports)

- 5.4.2 Medium Density (64-256 ports)

- 5.4.3 High Density (>256 ports)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Huawei Technologies Co., Ltd.

- 6.4.3 Nokia Corporation

- 6.4.4 ZTE Corporation

- 6.4.5 Arista Networks, Inc.

- 6.4.6 Extreme Networks, Inc.

- 6.4.7 Dell Technologies Inc.

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 Ciena Corporation

- 6.4.10 Ericsson AB

- 6.4.11 NEC Corporation

- 6.4.12 Ribbon Communications Inc.

- 6.4.13 Edgecore Networks Corporation

- 6.4.14 ADVA Optical Networking SE

- 6.4.15 ADTRAN Holdings, Inc.

- 6.4.16 Infinera Corporation

- 6.4.17 Casa Systems, Inc.

- 6.4.18 ALE International SAS (Alcatel-Lucent Enterprise)

- 6.4.19 Fujitsu Limited

- 6.4.20 Tellabs Access LLC

- 6.4.21 DriveNets Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment