|

시장보고서

상품코드

2073146

중소기업용 라우터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Small Business Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

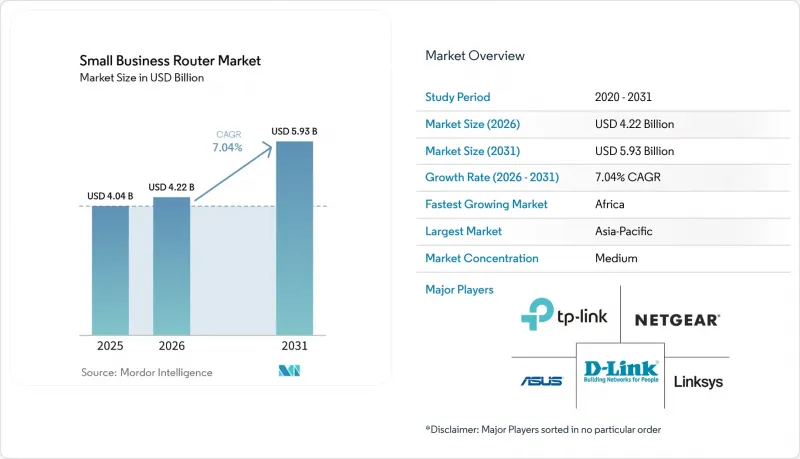

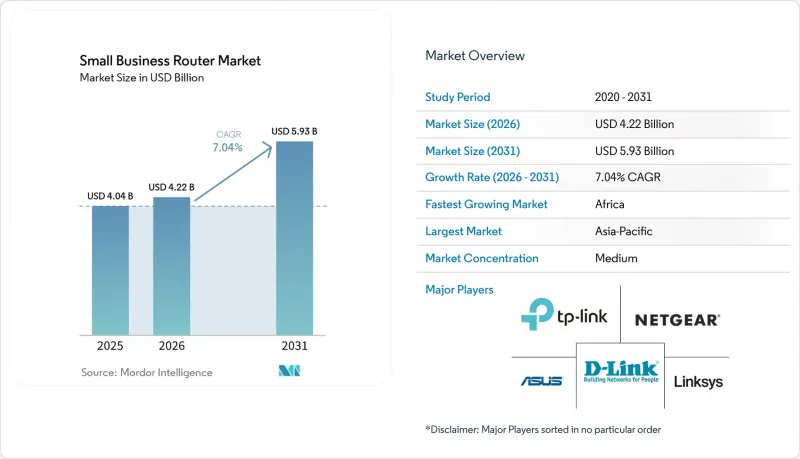

Mordor Intelligence에 의하면, 중소기업용 라우터 시장 규모는 2025년에 40억 4,000만 달러로 평가되었고 2026년 42억 2,000만 달러에서 2031년까지 59억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.04%를 나타낼 전망입니다.

본 보고서는 제품 유형(유선 라우터, 무선 라우터, 하이브리드 라우터), 포트 수(1-4포트, 5-8포트, 8포트 이상), WAN 기술(이더넷 광대역, XDSL, LTE/5G, 광섬유), 판매 채널(직접 판매, 유통업체 및 VAR, 전자상거래), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 중소기업용 라우터 시장 동향 및 인사이트

중소기업에서의 하이브리드 근무 모델 보급 확대

하이브리드 근무 방식의 도입으로 인해 중소기업은 일반 소비자용 라우터를 고해상도 비디오 스트림, 가상 사설망(VPN) 터널, 그리고 지연에 민감한 용도를 위한 서비스 품질(QoS) 정책을 동시에 지원하는 장치로 교체해야 할 필요에 직면해 있습니다. 2025년에 실시된 동료 심사를 거친 연구에 따르면, 하이브리드 근무 방식 덕분에 중소기업의 생산성이 4.8% 향상되었으며, 네트워크 연결 업그레이드에 대해 측정 가능한 투자 수익률(ROI)이 실현된 것으로 밝혀졌습니다. 2025년 중소기업을 대상으로 실시한 조사에 따르면, 응답자의 47%가 지난 12개월 동안 새로운 기술을 도입했으며, 그중 38%는 저지연·고처리량 연결이 필요한 인공지능(AI) 도구를 도입한 것으로 나타났습니다. 다른 업계 조사에 따르면, 중소기업의 86%가 열악한 통신 환경이 업무에 부정적인 영향을 미치고 있다고 응답한 반면, 5G 도입이 영국 경제에 790억 파운드(1,000억 달러)의 기여를 가져올 가능성이 있는 것으로 밝혀졌습니다. 이러한 변화에 따라 멀티 기가비트 이더넷 포트, Wi-Fi 6E 트라이밴드 무선, 그리고 게스트, 직원, IoT 트래픽을 분리할 수 있는 통합 보안 기능을 갖춘 라우터에 대한 수요가 급증하고 있습니다. 2025년 8월, ASUS는 모바일 근무자 및 하이브리드 근무자를 대상으로 2.5기가비트/초의 WAN, 5G/4G USB 테더링, 최대 30개 서비스 제공업체를 지원하는 가상 사설망(VPN) 기능을 사전 설치한 Wi-Fi 7 지원 미니 여행용 라우터 ‘RT-BE58 Go”를 발매했습니다.

클라우드 애플리케이션에 대한 인터넷 대역폭 수요 증가

고객 관계 관리(CRM), 기업 자원 계획(ERP), 협업을 위한 SaaS(Software-as-a-Service) 플랫폼으로의 전환에 따라 중소기업들은 비대칭 디지털 가입자 회선(ADSL)이나 케이블 연결에서 광섬유 및 5G 고정 무선 접속으로의 업그레이드를 추진하고 있습니다. 한 통신 사업자의 보고에 따르면, 현재 서비스를 제공하고 있는 고정 무선 접속 거점은 2,460만 곳에 달하며, 이는 광대역 서비스 제공이 가능한 거점의 21.2%를 차지하고 있습니다. 한편, 두 주요 경쟁사를 합치면 시장 점유율은 37.8%에 달하며, 고정 무선 접속을 통한 광대역 서비스 제공 가능 거점 수는 145% 증가했습니다. 캐나다 중소기업을 대상으로 한 조사에 따르면, 63%가 5G가 자사 사업에 이점을 가져다줄 것이라고 응답했으며, 영국의 소매업을 영위하는 중소기업 중 40%가 5G 연결에 투자하고 있습니다. 클라우드 애플리케이션 제공업체는 화상 회의의 경우 동시 접속 사용자 1인당 최소 5메가비트/초, 실시간 협업의 경우 10메가비트/초의 업로드 속도를 권장하고 있으며, 이로 인해 중소기업은 여러 WAN 링크를 결합하거나 딥 패킷 인스펙션(DPI)을 활용해 트래픽 우선순위를 지정할 수 있는 라우터를 도입해야 하는 상황에 직면해 있습니다. 2025년, DrayTek은 Vigor 2767 시리즈를 출시했습니다. 이 시리즈는 이더넷, xDSL, LTE 인터페이스에 걸친 SD-WAN 부하 분산을 통합하여, 여러 통신 사업자의 대역폭을 통합할 수 있게 해줍니다. 이러한 추세는 단일 통신 사업자의 서비스가 불안정한 시장에서 특히 두드러지며, 하이브리드 라우터가 장애 복구 및 부하 분산을 실현하고 있습니다.

소규모 기업의 가격 민감도

직원 수가 10명 미만인 초소규모 기업의 경우, 네트워크 장비에 대한 연간 예산이 500달러 미만인 경우가 많아 SD-WAN, Wi-Fi 6E 또는 통합 보안 어플라이언스를 탑재한 고급 라우터의 도입이 제한되고 있습니다. 2026년 2월에는 메모리 가격 급등이 600%에 달하면서, 공급업체의 이익률이 압박을 받는 동시에 100달러 미만의 보급형 모델 구입이 제한되었습니다. 신흥 시장의 중소기업들은 통화 약세와 자금 조달 제한으로 인해 예산 면에서 더욱 큰 제약을 겪고 있습니다. 2026년 3월, 연방통신위원회(FCC)가 해외산 라우터를 모두 “대상 목록”에 추가하기로 결정함에 따라 조건부 승인 절차가 발동되어 규정 준수 비용이 증가했습니다. 이러한 비용 증가는 공급업체에서 구매자에게 전가되고 있습니다. 중국산 라우터는 미국 수입액 점유율이 1.1%까지 하락한 반면, 베트남산 기기는 38.3%까지 상승했습니다. 이는 물류비 및 관세 부담을 가중시킨 공급망 재편을 반영한 것입니다. 이에 대해 각 벤더사는 단계적인 제품 라인업을 통해 대응하고 있으며, D-Link의 ‘DBR-600-P”는 이 회사의 플래그십 모델인 “DBR-X3000-AP”보다 저렴한 가격으로 기본적인 Wi-Fi 6 및 방화벽 기능을 제공합니다. 이러한 제약이 가장 심각한 곳은 아프리카와 남미이며, 이 지역에서는 중소기업들이 고도의 기능보다 연결성을 우선시하여 라우터의 수명을 5년 이상 연장하는 경우가 많습니다.

부문별 분석

유선, 무선 및 셀룰러 WAN 인터페이스를 통합한 하이브리드 라우터 시장은 기업들이 원활한 장애 복구 및 대역폭 집약을 요구함에 따라 2031년까지 연평균 10.82%의 성장률을 보일 것으로 전망됩니다. 모빌리티 및 게스트 접속에 대한 수요로 인해, 2025년 시점에서도 무선 모델은 중소기업용 라우터 시장의 48.13%를 차지하고 있습니다. 상시 접속 환경에서 단일 링크의 장애는 운영 비용 증가로 이어지기 때문에 하이브리드 부문이 가장 빠르게 성장할 것으로 예측됩니다. Zyxel의 “Nebula FWA515”는 5G WAN과 듀얼 2.5기가비트 LAN을 통합하고 있으며, 변동하는 네트워크 환경에서도 연속성과 성능을 보장하는 멀티 액세스 아키텍처를 위한 기능의 융합을 보여줍니다.

이러한 융합으로 인해 카테고리 간의 경계가 점점 더 모호해지고 있으며, 많은 무선 라우터가 SIM 슬롯이나 USB 기반의 셀룰러 백업 기능을 탑재함으로써 사실상 ‘하이브리드 퍼스트” 아키텍처로 전환하고 있습니다. 유선 모델은 구리선 인프라에서 확정적인 처리량이 필요한 제조 시스템이나 POS 환경과 같은 틈새 용도에서 계속해서 활용되고 있습니다. ASUS의 RT-BE88U는 10G RJ-45 및 SFP+ 포트를 탑재하고 있으며, 자동 멀티 WAN 및 4G/5G 테더링을 지원합니다. 이는 하이엔드 유선 장치조차도 중복성, 확장성 및 성능 최적화 요구 사항을 충족하기 위해 하이브리드 플랫폼으로 진화하고 있음을 보여줍니다.

5-8포트를 탑재한 라우터는 2025년 시장 규모의 46.37%를 차지했으나, 컨텐츠 제작 기업이나 데이터 집약형 중소기업이 10기가비트 이더넷을 도입함에 따라 8포트를 초과하는 기종은 2031년까지 연평균 10.53%의 성장률을 보일 것으로 전망됩니다. 라우터에 PoE(Power-over-Ethernet) 기능을 통합함으로써, 비디오 감시 시스템, Wi-Fi 6E 액세스 포인트, 음성 인프라에 단일 장치에서 직접 전원을 공급할 수 있게 되어, 기기 과다 설치를 방지하고 있습니다. D-Link의 DGS-1250 스위치는 멀티 기가비트 라우터의 업링크와 체인 연결이 가능하여, 여러 개의 고대역폭 엔드포인트가 동시에 작동하는 고밀도 네트워크 환경에서 배선을 간소화하고 확장성을 향상시킵니다.

1-4포트 부문은 인터넷 접속에 주로 무선 연결이나 USB 기반 5G 동글에 의존하는 초소규모 기업들 사이에서 여전히 중요한 위치를 차지하고 있습니다. 선진국 시장에서는 광섬유 비용의 하락으로 인해 2.5기가비트 및 10기가비트 포트로의 업그레이드가 가속화되고 있으며, 이는 처리 능력이 강화된 고밀도 라우터에 대한 향후 수요를 견인하고 있습니다. ASUS의 “ZenWiFi BQ16 Pro”는 메쉬 노드에 듀얼 10기가비트 포트를 통합하고 있으며, 소규모 비즈니스 이용 사례에 적합한 소형 소비자용 설계에서도 멀티기가 유선 백홀로의 광범위한 전환이 진행되고 있음을 보여줍니다.

지역별 분석

2025년, 아시아태평양은 중소기업용 라우터 시장의 34.29%를 차지했습니다. 이는 중국 공업정보화부가 수립한 “2025-2027년 중소기업 디지털화 추진 계획”에 이끌린 것입니다. 이 계획은 4만 개의 중소기업을 대상으로 하며, 재정 보조금 및 자금 지원을 통해 2027년까지 클라우드 도입률 40% 이상을 달성하는 것을 목표로 하고 있습니다. TP-Link는 2025년 10월, 인도에 세계 최대 규모의 공장을 설립할 것이라고 발표했습니다. 투자액은 100카롤 루피(1,200만 달러)를 넘어섰으며, 직원 수를 확대하는 한편, 2025년 7월에는 Wi-Fi 7, IoT, 인공지능에 특화된 연구개발 센터를 개설했습니다. 일본과 한국은 Wi-Fi 7 라우터를 조기에 도입한 국가이며, ASUS는 2025년 10월, 전용 AI 코어와 엣지 컴퓨팅 워크로드를 위한 네이티브 Docker Engine 지원을 특징으로 하는 ‘ROG Rapture GT-BE19000AI”를 발매했습니다. 동남아시아에서는 2025년에 운영을 시작한 ‘2Africa” 케이블 등 해저 케이블에 대한 투자의 혜택을 누리고 있습니다. 이 케이블은 아프리카, 유럽, 아시아의 33개국을 연결하여 클라우드 애플리케이션의 지연 시간을 줄여줍니다.

북미는 여전히 고부가가치 시장이며, 캐나다의 “디지털 도입 프로그램”에서는 중소기업이 전자상거래, 사이버 보안, 클라우드 기반 도구를 도입할 수 있도록 지원하기 위해 40억 캐나다 달러(29억 6,000만 달러)를 투입하여, 최대 15,000 캐나다 달러(1만 1,100 달러)의 보조금 및 최대 100,000 캐나다 달러(7만 4,000 달러)의 대출을 제공합니다. 미국 국립과학재단(NSF)은 2025년에 “TechAccess AI-Ready America”를 출범시키고, 인공지능(AI) 인프라 확충에 1억 6,800만-2억 2,400만 달러를 투자하기로 결정했습니다. 이에 따라 엣지 AI 워크로드를 지원할 수 있는 라우터에 대한 수요가 증가할 것으로 예측됩니다. 멕시코에서는 5G 고정 무선 접속(FWA)의 도입이 확대되고 있으며, 통신 사업자들은 광섬유 인프라가 구축되지 않은 도시 주변 지역의 중소기업을 주요 대상으로 삼고 있습니다. 유럽은 규제 체계가 세분화되어 있는 것이 특징이며, 유럽연합(EU)의 무선기기 지침에서는 EN 18031 보안 규격 준수가 의무화되어 있지만, Zyxel의 “Nebula FWA515”는 이를 충족하는 최초의 네트워크 제품 중 하나라고 내세우고 있습니다.

아프리카는 대규모 광섬유 구축과 정부의 디지털화 이니셔티브에 힘입어 2031년까지 연평균 11.90%의 성장률이 예상되며, 이는 모든 지역 중 가장 빠른 성장률입니다. 나이지리아의 D-VIBE 프로젝트는 아프리카개발은행으로부터 2억 달러, 세계은행으로부터 5억 달러의 자금을 조달하는 데 성공했으며, 9만 킬로미터의 광섬유를 설치하여 서비스가 미치지 않는 지역 사회와 중소기업을 연결할 예정입니다. 디지털 인프라 성숙도 측면에서 남아프리카공화국과 모로코가 아프리카 대륙을 선도하고 있으며, “아프리카 디지털 인프라 지수”에서 남아프리카공화국은 88점, 모로코는 79점을 기록했습니다. 사우디아라비아와 아랍에미리트(UAE) 등 중동 시장에서는 자유무역지대나 혁신 지구에서 사업을 전개하는 중소기업을 대상으로, 고밀도 Wi-Fi 6E 및 5G 라우터가 필요한 스마트시티 구상에 대한 투자가 진행되고 있습니다. 남미는 환율 변동과 제한된 정부 보조금에 제약을 받고 있으며, 브라질과 아르헨티나가 최대 시장을 차지하고 있지만, 예산상의 압박으로 인해 라우터 업그레이드가 지연되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the small business router market size was valued at USD 4.04 billion in 2025 and is estimated to grow from USD 4.22 billion in 2026 to reach USD 5.93 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031).

This report is Segmented by Product Type (Wired Routers, Wireless Routers, Hybrid Routers), Port Count (1-4 Ports, 5-8 Ports, More Than 8 Ports), WAN Technology (Ethernet Broadband, XDSL, LTE/5G, Fiber), Sales Channel (Direct Sales, Distributors and VARs, E-Commerce), and GeographY. The Market Forecasts are Provided in Terms of Value (USD).

Global Small Business Router Market Trends and Insights

Growing Adoption of Hybrid Work Models by Small Businesses

Hybrid work arrangements are compelling small businesses to replace consumer-grade routers with devices that support simultaneous high-definition video streams, virtual private network tunnels, and quality-of-service policies for latency-sensitive applications. A peer-reviewed study in 2025 found that hybrid work improved small and medium enterprise productivity by 4.8%, creating a measurable return on investment for connectivity upgrades. A 2025 small business survey reported that 47% of respondents implemented new technology in the past 12 months, with 38% deploying artificial intelligence tools that require low-latency, high-throughput connections. Another industry study found that 86% of small and medium enterprises stated poor connectivity negatively impacted operations, while 5G deployment could contribute GBP 79 billion (USD 100 billion) to the United Kingdom economy. The shift is accelerating demand for routers with multi-gigabit Ethernet ports, Wi-Fi 6E tri-band radios, and integrated security features that can segment guest, employee, and Internet of Things traffic. In August 2025, ASUS launched the RT-BE58 Go, a Wi-Fi 7 mini travel router with 2.5 gigabit per second WAN, 5G/4G USB tethering, and pre-installed virtual private network support for up to 30 service providers, targeting mobile and hybrid workers.

Rising Internet Bandwidth Demands for Cloud Applications

Migration to software-as-a-service platforms for customer relationship management, enterprise resource planning, and collaboration is driving small businesses to upgrade from asymmetric digital subscriber line and cable connections to fiber and 5G fixed wireless access. One telecom operator reported 24.6 million fixed wireless access locations in service, representing 21.2% of broadband serviceable locations, while two major competitors combined for 37.8% coverage and 145% growth in fixed wireless access broadband serviceable locations. A survey of Canadian small and medium businesses found that 63% believe 5G will benefit their operations, while 40% of United Kingdom retailer small and medium businesses are investing in 5G connectivity.Cloud application providers recommend minimum upload speeds of 5 megabits per second per concurrent user for video conferencing and 10 megabits per second for real-time collaboration, pushing small businesses toward routers that can bond multiple WAN links or prioritize traffic using deep packet inspection. In 2025, DrayTek introduced the Vigor2767 series, integrating SD-WAN load balancing across Ethernet, xDSL, and LTE interfaces, enabling bandwidth aggregation from multiple carriers. The trend is particularly pronounced in markets with unreliable single-carrier service, where hybrid routers provide failover and load distribution.

Price Sensitivity Among Micro-Enterprises

Micro-enterprises with fewer than 10 employees often allocate less than USD 500 annually for networking equipment, constraining the adoption of advanced routers with SD-WAN, Wi-Fi 6E, or integrated security appliances. Memory price inflation surged 600% in February 2026, compressing vendor margins and limiting the availability of entry-level models below USD 100. Small businesses in emerging markets face additional budget constraints due to currency depreciation and limited access to financing. The Federal Communications Commission's March 2026 decision to add all foreign-produced routers to its Covered List triggered conditional approval processes that increased compliance costs, which vendors are passing to buyers. China-origin routers fell to 1.1% of the United States import value share, while Vietnam-origin devices rose to 38.3%, reflecting a supply chain reconfiguration that added logistics and tariff expenses. Vendors are responding by introducing tiered product lines, with D-Link's DBR-600-P offering basic Wi-Fi 6 and firewall features at a lower price than its flagship DBR-X3000-AP. The constraint is most acute in Africa and South America, where small businesses prioritize connectivity over advanced features and often extend router lifecycles beyond five years.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Availability of Affordable Wi-Fi 6 Routers

- Emergence of Subscription Based Network-as-a-Service Offerings

- Supply Chain Disruptions for Semiconductor Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid routers, which merge wired, wireless, and cellular WAN interfaces, are projected to expand at 10.82% annually through 2031 as firms seek seamless failover and bandwidth aggregation. Wireless models still account for 48.13% of the small-business router market in 2025 due to mobility and guest-access requirements. The hybrid segment is expected to grow fastest because single-link outages impose higher operational costs in always-connected environments. Zyxel's Nebula FWA515 integrates 5G WAN with dual 2.5 gigabit LAN, demonstrating feature convergence toward multi-access architectures that ensure continuity and performance under fluctuating network conditions.

Convergence is increasingly blurring category boundaries, with many wireless routers incorporating SIM slots or USB-based cellular backup, effectively shifting toward hybrid-first architectures. Wired models continue to serve niche applications such as manufacturing systems and point-of-sale environments that require deterministic throughput over copper infrastructure. ASUS's RT-BE88U, equipped with 10G RJ-45 and SFP+ ports, supports automatic multi-WAN and 4G/5G tethering, indicating that even high-end wired devices are evolving into hybrid platforms to address redundancy, scalability, and performance-optimization requirements.

Routers offering 5-8 ports captured 46.37% of the 2025 value, but units with more than 8 ports are projected to grow at 10.53% annually through 2031 as content-creation firms and data-intensive small businesses adopt 10 gigabit Ethernet. Power-over-Ethernet integration within routers is reducing equipment sprawl by enabling video surveillance systems, Wi-Fi 6E access points, and voice infrastructure to be powered directly from a single device. D-Link's DGS-1250 switches can be chained from multi-gigabit router uplinks, simplifying cabling and improving scalability in dense network environments where multiple high-bandwidth endpoints operate simultaneously.

The 1-4 port segment remains relevant among micro-enterprises that depend primarily on wireless connectivity and USB-based 5G dongles for internet access. In developed markets, declining fiber costs are accelerating upgrades to 2.5-gigabit and 10-gigabit ports, driving future demand for higher-density routers with enhanced throughput capabilities. ASUS's ZenWiFi BQ16 Pro integrates dual 10-gigabit ports into a mesh node, highlighting a broader transition toward multi-gig wired backhaul even in compact, consumer-oriented designs adapted for small-business use cases.

Complete Report Scope:

- By Product Type

- Wired Routers

- Wireless Routers

- Hybrid Routers

- By Port Count

- 1-4 Ports

- 5-8 Ports

- More Than 8 Ports

- By WAN Technology

- Ethernet Broadband

- xDSL

- LTE/5G

- Fiber

- By Sales Channel

- Direct Sales

- Distributors and VARs

- E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific held 34.29% of the small business router market in 2025, driven by China's Ministry of Industry and Information Technology Small and Medium Enterprise Digital Empowerment Plan for 2025-2027, which targets 40,000 SMEs and aims to achieve a cloud adoption rate exceeding 40% by 2027 through fiscal subsidies and financing support. TP-Link announced its largest global factory in India in October 2025, with an investment exceeding INR 100 crore (USD 12 million), and expanded its workforce while unveiling a research and development center focused on Wi-Fi 7, Internet of Things, and artificial intelligence in July 2025. Japan and South Korea are early adopters of Wi-Fi 7 routers, with ASUS launching the ROG Rapture GT-BE19000AI in October 2025, featuring a dedicated artificial intelligence core and native Docker Engine support for edge computing workloads. Southeast Asia is benefiting from subsea cable investments such as the 2Africa cable, which became operational in 2025 and connects 33 countries across Africa, Europe, and Asia, reducing latency for cloud applications.

North America remains a high-value market, with Canada's Digital Adoption Program allocating CAD 4 billion (USD 2.96 billion) in grants up to CAD 15,000 (USD 11,100) and loans up to CAD 100,000 (USD 74,000) to help small businesses adopt e-commerce, cybersecurity, and cloud-based tools. The United States National Science Foundation launched TechAccess AI-Ready America in 2025, committing USD 168 to 224 million to expand artificial intelligence infrastructure, which will drive demand for routers capable of supporting edge artificial intelligence workloads. Mexico is experiencing growth in 5G fixed wireless access deployments, with carriers targeting small businesses in peri-urban zones lacking fiber infrastructure. Europe is characterized by fragmented regulatory frameworks, with the European Union Radio Equipment Directive mandating compliance with EN 18031 security standards, which Zyxel's Nebula FWA515 claims to meet as among the first network products.

Africa is forecast to grow at 11.90% annually through 2031, the fastest rate among all geographies, driven by large-scale fiber deployments and government digitalization initiatives. Nigeria's D-VIBE project secured USD 200 million from the African Development Bank and USD 500 million from the World Bank to deploy 90,000 kilometers of fiber, connecting underserved communities and small businesses. South Africa and Morocco lead the continent in digital infrastructure maturity, with the Africa Digital Infrastructure Index scoring South Africa at 88 and Morocco at 79. Middle East markets such as Saudi Arabia and the United Arab Emirates are investing in smart city initiatives that require high-density Wi-Fi 6E and 5G routers for small businesses operating in free zones and innovation districts. South America is constrained by currency volatility and limited government subsidies, with Brazil and Argentina representing the largest markets but facing budget pressures that delay router upgrades.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Netgear, Inc.

- TP-Link Technologies Co., Ltd.

- Ubiquiti Inc.

- MikroTikls SIA

- DrayTek Corp.

- D-Link Corporation

- ASUSTeK Computer Inc.

- Zyxel Communications Corp.

- Peplink International Limited

- Fortinet, Inc.

- Juniper Networks, Inc.

- Edgecore Networks Corporation

- Ruijie Networks Co., Ltd.

- Cambium Networks Corporation

- Sophos Ltd.

- WatchGuard Technologies, Inc.

- Belkin International, Inc.

- Cradlepoint, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Hybrid Work Models by Small Businesses

- 4.2.2 Rising Internet Bandwidth Demands for Cloud Applications

- 4.2.3 Increasing Availability of Affordable Wi-Fi 6 Routers

- 4.2.4 Emergence of Subscription Based Network-as-a-Service Offerings

- 4.2.5 Integration of SD-WAN Features into Entry-Level Routers

- 4.2.6 Government Small Business Digitalization Incentives

- 4.3 Market Restraints

- 4.3.1 Price Sensitivity Among Micro-Enterprises

- 4.3.2 Supply Chain Disruptions for Semiconductor Components

- 4.3.3 Growing Preference for All-in-One Cellular Hotspots over Routers

- 4.3.4 Limited IT Expertise in Very Small Offices Delaying Upgrades

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Wired Routers

- 5.1.2 Wireless Routers

- 5.1.3 Hybrid Routers

- 5.2 By Port Count

- 5.2.1 1-4 Ports

- 5.2.2 5-8 Ports

- 5.2.3 More Than 8 Ports

- 5.3 By WAN Technology

- 5.3.1 Ethernet Broadband

- 5.3.2 xDSL

- 5.3.3 LTE/5G

- 5.3.4 Fiber

- 5.4 By Sales Channel

- 5.4.1 Direct Sales

- 5.4.2 Distributors and VARs

- 5.4.3 E-commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Hewlett Packard Enterprise Company

- 6.4.3 Netgear, Inc.

- 6.4.4 TP-Link Technologies Co., Ltd.

- 6.4.5 Ubiquiti Inc.

- 6.4.6 MikroTikls SIA

- 6.4.7 DrayTek Corp.

- 6.4.8 D-Link Corporation

- 6.4.9 ASUSTeK Computer Inc.

- 6.4.10 Zyxel Communications Corp.

- 6.4.11 Peplink International Limited

- 6.4.12 Fortinet, Inc.

- 6.4.13 Juniper Networks, Inc.

- 6.4.14 Edgecore Networks Corporation

- 6.4.15 Ruijie Networks Co., Ltd.

- 6.4.16 Cambium Networks Corporation

- 6.4.17 Sophos Ltd.

- 6.4.18 WatchGuard Technologies, Inc.

- 6.4.19 Belkin International, Inc.

- 6.4.20 Cradlepoint, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment