|

시장보고서

상품코드

2073069

라우터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

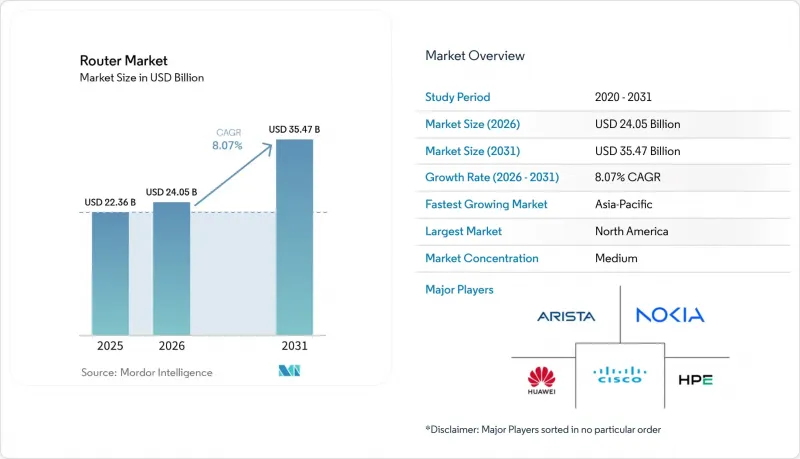

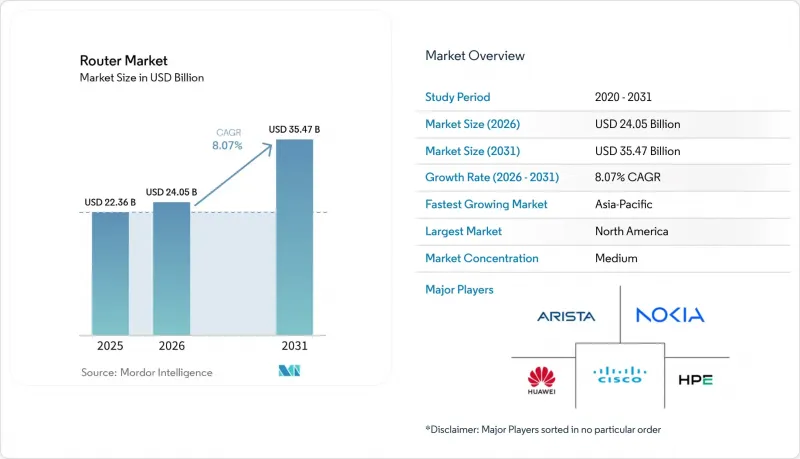

Mordor Intelligence에 의하면, 라우터 시장 규모는 2025년 223억 6,000만 달러, 2026년 240억 5,000만 달러에서 2031년까지 354억 7,000만 달러로 확대한다고 예측되고 있어 2026-2031년까지 연평균 복합 성장률(CAGR)은 8.07%를 나타낼 전망입니다.

본 보고서는 라우터 유형(유선 라우터, 무선 라우터, 셀룰러 라우터), 성능 수준(저 처리량, 기타), 최종 사용자(주택/소비자, IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 정부·국방, 제조, 운송 및 물류, 기타 최종 사용자), 유통 채널(온라인 마켓플레이스, 직접 판매, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 라우터 시장 동향과 인사이트

광대역 보급률의 상승과 고속 홈 네트워크에 대한 수요

2024년, OECD 회원국의 고정 광대역 회선 중 FTTP(Fiber-to-the-Premises) 계약 비중이 44.6%를 넘어섰으며, 멀티 기가비트 Wi-Fi의 성능에 대한 가구의 기대가 높아지고 있습니다. 또한, 통신 사업자들은 2030년까지 3억 5,000만 개의 고정 무선 접속 회선이 도입될 것으로 예측하고 있으며, 이 수치를 달성하기 위해서는 라스트 마일의 구리선을 우회할 수 있는 견고한 실외용 5G 라우터가 필요합니다. 2024년에는 영국 주택의 69% 이상에서 풀 파이버를 이용할 수 있게 되었으며, 서비스 제공업체들은 기가비트 요금제에 Wi-Fi 6E 트라이밴드 라우터를 번들로 제공하기 시작했습니다. 따라서 새로운 홈 게이트웨이에는 클라우드 게임이나 화상 회의 등 지연에 민감한 트래픽을 우선 처리하는 고급 QoS 엔진이 탑재되어 있습니다. 그 결과, 라우터 시장은 양극화되고 있습니다. 광섬유가 구축된 가정용 프리미엄 메쉬 시스템과, 서비스가 충분히 제공되지 않는 지역을 위한 셀룰러 게이트웨이로, 각각에 독자적인 공급망, 가격 책정, 지원 모델이 요구됩니다.

고급 엔터프라이즈 라우팅이 필요한 클라우드 서비스의 보급

하이브리드 클라우드와 멀티 클라우드의 도입으로 인해 기업들은 지사나 데이터센터의 라우팅 환경을 개편할 수밖에 없게 되었습니다. 이를 통해 SD-WAN 오버레이, 자동 페일오버, 용도 인식형 채널 선택 기능이 퍼블릭 클라우드와 프라이빗 클라우드 모두에서 원활하게 작동하게 됩니다. 시스코의 “Cloud OnRamp”는 수동 BGP 조정 없이도 AWS, Azure, Google Cloud에 대한 인텐트 기반 라우팅을 구현합니다. 아리스타의 “CloudEOS”는 On-Premise와 클라우드의 전체 패브릭에 걸쳐 일관된 세분화을 확대하여 DevOps 팀의 운영 부담을 줄여줍니다. Palo Alto Networks는 라우팅과 제로 트러스트 보안을 단일 어플라이언스에 통합하여 지사의 총 소유 비용(TCO)을 절감하는 동시에 도입을 가속화했습니다. 그 결과, 수요는 딥 패킷 검사 및 암호화 트래픽 분석 기능을 갖춘 라우터로 이동하고 있으며, 각 벤더들은 단순한 포트 수보다는 통합 소프트웨어를 통한 수익 창출에 주력하고 있습니다.

공급망 부족과 반도체 가격 변동

2024년 하반기에는 라우팅용 ASIC의 리드타임이 52주에 달하면서 기업의 교체 주기가 연기되었고, 이로 인해 이익률을 압박하는 긴급 납품 수수료가 상승했습니다. 브로드컴은 AI 관련 네트워크용 반도체 시장이 2027년까지 1,000억 달러를 넘어설 것으로 전망하고 있으며, 제한된 첨단 노드 생산 능력을 둘러싸고 하이퍼스케일러와 네트워크 장비 제조업체 간의 경쟁이 치열해지고 있습니다. 시스코는 희소 부품들을 고수익 소프트웨어 번들에 재배치한 탓에 2024 회계연도 하드웨어 매출이 감소했다고 밝혔습니다. 아리스타는 공급 부족에도 불구하고 전년 대비 20%의 성장률을 유지하기 위해, 수년에 걸친 웨이퍼 계약을 확보했습니다. 칩렛 기반 설계는 공급원의 다각화로 이어질 가능성이 있지만, 테스트의 복잡성을 증가시키고, 수요가 급증할 경우 소규모 공급업체가 할당량 변동에 따른 영향을 받기 쉬워질 우려가 있습니다.

부문별 분석

무선 라우터는 2025년에도 라우터 시장 점유율의 49.62%를 차지하며 여전히 주도적인 위치를 차지하고 있지만, 도시 지역의 광섬유 보급률이 포화 상태에 가까워짐에 따라 성장 둔화에 직면하고 있습니다. 5G 프라이빗 네트워크의 시범 운영이 본격적인 상용화로 전환됨에 따라, 셀룰러 플랫폼이 라우터 시장에서 점점 더 주목을 받고 있습니다. 셀룰러 라우터 시장은 2031년까지 연평균 성장률(CAGR) 11.24%를 나타낼 것으로 예측되며, 다른 어떤 부문보다 높은 성장률을 보일 것으로 전망됩니다. 이러한 기술들은 유선 연결이 현실적으로 어려운 창고 자동화, 광업 분야의 원격 측정, 스마트 시티의 조명 등을 뒷받침하는 핵심 요소로 자리 잡고 있습니다. GSM 협회의 집계에 따르면, 2024년에는 1,000개 이상의 상용 프라이빗 5G 네트워크가 존재할 것이며, 각 네트워크는 저지연 연결을 실현하기 위해 여러 대의 셀룰러 게이트웨이를 도입하고 있습니다.

각 벤더들이 eSIM 및 5G 모뎀을 엔터프라이즈급 무선 라우터에 탑재하여 유선 회선이 끊어졌을 때 자동 페일오버를 구현함에 따라 경쟁이 치열해지고 있습니다. Cradlepoint의 2025년 제품 라인업에는 텔레매틱스와 승객용 Wi-Fi 간에 대역폭을 분배하기 위한 네트워크 슬라이싱 기능이 추가되었습니다. Teltonika와 Digi International은 철도 및 해양 용도로 인증받은 견고한 장치를 출시하며, ‘셀룰러 퍼스트’ 도입에 따른 라우터 시장 규모를 확대했습니다. Telecom Infra Project의 이니셔티브를 통한 오픈 API에 대한 규제적 지원으로 인해 전환 비용이 절감됨에 따라, 라우터 업계의 경쟁사들 사이에서 소프트웨어가 진정한 차별화 요소로서 그 중요성이 커지고 있습니다.

하이퍼스케일러와 통신 사업자들은 100Gbps를 초과하는 라우터에 대한 두 자릿수 성장을 주도하고 있으며, 이 하위 부문은 2031년까지 연평균 성장률(CAGR) 11.67%를 나타낼 것으로 예측됩니다. Arista의 7800R4와 Juniper의 PTX10000 시리즈는 구매자들이 랙 유닛당 밀도와 서브 마이크로초 수준의 지연 시간을 얼마나 중요하게 여기는지를 여실히 보여주고 있습니다. 대조적으로, 중간 처리량의 라우터는 2025년에 라우터 시장 점유율의 39.18%를 차지하며, 비용과 기능 세트의 균형이 요구되는 캠퍼스 코어 및 지역 거점(PoP)을 지원하고 있습니다.

1 Gbps 이하의 저대역폭 라우터는 여전히 소규모 사무실용으로 대량 출하되고 있지만, AI 워크로드로 인한 동서 방향 트래픽의 급증에 따라 라우터 시장의 성장은 하이엔드 및 울트라 하이엔드 부문에 집중되고 있습니다. 시스코의 8000 시리즈는 실리콘 포토닉스를 통합하여 비트당 전력 소비를 줄였으며, 유럽의 대기 전력 규정을 준수합니다. 노키아의 코히런트 광학 접근 방식을 통해 통신 사업자는 라우팅과 전송을 통합하여 전력 예산과 랙 공간을 절약할 수 있습니다. 버스트 성향이 강한 AI 트래픽을 위해 패킷 버퍼링 및 혼잡 제어 알고리즘을 최적화한 벤더는 데이터센터 내에서 800GbE가 표준 사양으로 자리 잡음에 따라 압도적인 시장 점유율을 확보하게 될 것으로 보입니다.

지역별 분석

북미는 제로 트러스트 의무화 및 광대역 격차 해소를 위한 보조금 덕분에 기업과 ISP가 멀티 기가비트 게이트웨이로의 업그레이드를 지속함에 따라, 2025년 라우터 시장 매출의 34.68%를 차지했습니다. 연방 정부의 자금 지원에 힘입어, 서비스가 미흡한 카운티에서의 광섬유 인프라 구축이 가속화되면서, 소비자용 및 통신사 집선 계층에서의 라우터 수요가 촉진되고 있습니다. 한편, 북미의 데이터센터 사업자들은 인공지능(AI) 훈련 클러스터에 대응하기 위해 400 GbE 패브릭을 단계적으로 도입하고 있으며, 이에 따라 초고처리량 섀시의 수주가 더욱 확대되고 있습니다.

아시아태평양은 라우터 시장의 성장 동력이며, 2026년부터 2031년까지 연평균 성장률(CAGR) 10.36%를 나타낼 것으로 전망됩니다. 중국은 2024년까지 이미 395만 기의 5G 기지국을 구축했으며, 슬라이싱 지원 기능과 AI 기반 트래픽 스티어링이 필요한 5G-Advanced 기능의 시험 운영을 진행하고 있습니다. 인도의 “스마트 시티 미션”에서는 교통 관리, 영상 분석, 공공 요금 자동 계량을 위해 지자체용 엣지 라우터가 도입되면서, 해당 지역의 라우터 시장 규모가 확대되고 있습니다. 화웨이(Huawei)와 같은 신흥 기업들은 인구 밀도가 높은 대도시권의 엄격한 에너지 제한에 대응하기 위해 AI 기능을 강화하고 전력 효율이 뛰어난 라우터를 출시하고 있습니다.

유럽에서는 지속가능성이 중요시되고 있습니다. 유럽위원회의 “광대역 기기의 에너지 소비에 관한 행동 강령”와 “대기 전력 규제(2023/826)”에 따라 아이돌 모드 시의 최대 전력 소비량이 설정되었으며, 신형 모델에서는 전력 관리 회로의 재설계가 요구되고 있습니다. 독일, 프랑스, 스페인의 통신 사업자들은 현재 기업용 광섬유 계약에 더 효율적인 중간 처리량 장비를 묶어 제공하고 있으며, 데이터센터 운영자들은 탄소 예산에 맞추어 실리콘 포토닉 라우터를 도입하고 있습니다. 남미와 아프리카에서는 자본 집약적인 광섬유 설치 비용을 줄이기 위해 고정 무선 접속에 셀룰러 라우터를 널리 사용하고 있습니다. 국제전기통신연합(ITU)의 기록에 따르면, 2024년 개발도상국 시장의 고정 광대역 회선 수는 전년 대비 8% 증가했으며, 이는 이더넷 백홀과 LTE 또는 5G 업링크를 모두 지원하는 비용 효율적인 라우터에 대한 수요가 여전히 높다는 사실을 뒷받침하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the router market size is projected to expand from USD 22.36 billion in 2025 and USD 24.05 billion in 2026 to USD 35.47 billion by 2031, registering a CAGR of 8.07% between 2026 and 2031.

This report is Segmented by Router Type (Wired Routers, Wireless Routers, and Cellular Routers), Performance Tier (Low Throughput, and More), End User (Residential/Consumer, IT and Telecom, BFSI, Government and Defense, Manufacturing, Transportation and Logistics, and Other End Users), Sales Channel (Online Marketplaces, Direct Sales, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Router Market Trends and Insights

Rising Broadband Penetration And Demand For High-Speed Home Networking

Fiber-to-the-premises subscriptions exceeded 44.6% of fixed broadband lines across OECD economies in 2024, lifting household expectations for multi-gigabit Wi-Fi performance. Operators also forecast 350 million fixed-wireless access links by 2030, a figure that requires ruggedized outdoor 5G routers to bypass last-mile copper. Full-fiber availability surpassed 69% of U.K. premises in 2024, causing service providers to bundle Wi-Fi 6E tri-band routers with gigabit plans. New residential gateways therefore integrate advanced QoS engines that prioritize latency-sensitive traffic such as cloud gaming and video conferencing. The result is a bifurcated router market: premium mesh systems for fiber homes and cellular gateways for underserved regions, each demanding unique supply-chain, pricing, and support models.

Proliferation Of Cloud Services Requiring Advanced Enterprise Routing

Hybrid and multicloud adoption is forcing enterprises to refresh branch and data-center routing so that SD-WAN overlays, automated failover, and application-aware path selection work seamlessly across public and private clouds. Cisco's Cloud OnRamp delivers intent-based routing into AWS, Azure, and Google Cloud without manual BGP tuning. Arista's CloudEOS extends consistent segmentation across on-prem and cloud fabrics, reducing operational toil for DevOps teams. Palo Alto Networks has fused routing with zero-trust security in a single appliance that lowers branch TCO and speeds deployment. Demand is therefore shifting toward routers with deep packet inspection and encrypted-traffic analytics, prompting vendors to monetize integrated software far more than raw port counts.

Supply Chain Shortages And Semiconductor Price Volatility

Lead times for routing ASICs stretched to 52 weeks in late 2024, postponing enterprise refresh cycles and lifting expedite fees that eroded margins. Broadcom projected AI-related networking silicon to top USD 100 billion by 2027, pitting hyperscalers against network-equipment makers for limited advanced-node capacity. Cisco disclosed lower hardware revenue in fiscal 2024 as it diverted scarce parts to high-margin software bundles. Arista secured multi-year wafer contracts to sustain 20% YoY growth despite shortages. Chiplet-based designs may diversify supply but raise testing complexity and leave smaller vendors exposed to allocation shocks during demand spikes.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption Of Wi-Fi 6 And Wi-Fi 7 Standards

- Emergence Of Multi-Access Edge Computing Driving Micro-Edge Routers

- Intense Price Competition Commoditizing Consumer Routers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wireless routers, while still leading with 49.62% router market share in 2025, now face slowed growth as urban fiber penetration approaches saturation. Cellular platforms captured mounting attention in the router market as 5G private-network pilots became full commercial rollouts. Cellular routers are forecast to grow at an 11.24% CAGR through 2031, outpacing every other category. They anchor warehouse automation, mining telemetry, and smart-city lighting, where hard-wired links prove impractical. The GSM Association counted more than 1,000 commercial private-5G networks in 2024, each deploying multiple cellular gateways for low-latency connectivity.

Competition intensifies as vendors embed eSIMs and 5G modems into enterprise-grade wireless routers, delivering automatic failover when fixed lines drop. Cradlepoint's 2025 portfolio added network-slicing support to split bandwidth between telematics and passenger Wi-Fi. Teltonika and Digi International released rugged devices qualified for rail and maritime uses, broadening the addressable router market size for cellular-first deployments. Regulatory support for open APIs under Telecom Infra Project initiatives lowers switching costs, amplifying software as the true differentiator across router industry contenders.

Hyperscalers and telecom carriers are driving double-digit demand for routers exceeding 100 Gbps, a sub-segment expected to post an 11.67% CAGR to 2031. Arista's 7800R4 and Juniper's PTX10000 lines together illustrate the premium buyers place on density per rack unit and sub-microsecond latency. In contrast, mid-throughput routers held 39.18% router market share in 2025, underpinning campus cores and regional points of presence where balanced cost and feature sets suffice.

Low-throughput routers below 1 Gbps still ship in volume to small offices, yet the router market size growth story concentrates in high and ultra-high tiers as AI workloads spike east-west traffic. Cisco's 8000 series integrated silicon photonics to lower energy per bit, aligning with European idle-power rules. Nokia's coherent-optics approach allows carriers to collapse routing and transport, conserving power budgets and rack space. Vendors that optimize packet buffering and congestion algorithms for bursty AI traffic will capture an outsized share as 800 GbE becomes table stakes inside data centers.

Complete Report Scope:

- By Router Type

- Wired Routers

- Wireless Routers

- Cellular Routers

- By Performance Tier

- Low Throughput (<1 Gbps)

- Mid Throughput (1-10 Gbps)

- High Throughput (10-100 Gbps)

- Ultra-High (>100 Gbps)

- By End User

- Residential/Consumer

- IT and Telecom

- BFSI

- Government and Defense

- Manufacturing

- Transportation and Logistics

- Others End Users

- By Sales Channel

- Online Marketplaces

- Direct Sales

- Distributors/Value-Added Resellers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America retained 34.68% of 2025 revenue in the router market as zero-trust mandates and broadband-equity subsidies kept enterprises and ISPs upgrading to multi-gigabit gateways. Federal funding streams accelerate fiber builds in underserved counties, stimulating router demand across consumer and carrier aggregation layers. Meanwhile, data-center operators in the North America regionphase in 400 GbE fabrics to accommodate Artificial Intelligence training clusters, reinforcing orders for ultra-high-throughput chassis.

Asia-Pacific is the growth engine of the router market, forecast to log a 10.36% CAGR from 2026 to 2031. China had already erected 3.95 million 5G base stations by 2024 and is trialing 5G-Advanced features that demand edge routers with slicing awareness and AI-based traffic steering. India's Smart Cities Mission added municipal edge routers for traffic management, video analytics, and automated utility metering, broadening the regional router market size. Emerging players like Huawei are shipping AI-enhanced power-optimized routers to fit stringent energy caps in dense metros.

Europe emphasizes sustainability. The European Commission's Code of Conduct on Broadband Equipment Energy Consumption and Standby Regulation 2023/826 impose idle-power ceilings that trigger redesigned power-management circuits in new models. Carriers in Germany, France, and Spain now bundle more efficient mid-throughput devices into business fiber contracts, while data-center operators slot silicon-photonic routers to align with carbon budgets. South America and Africa rely heavily on cellular routers for fixed-wireless access, bypassing capital-intensive fiber builds. The International Telecommunication Union recorded 8% YoY growth in developing-market fixed broadband lines during 2024, affirming the continued need for cost-effective routers that straddle Ethernet backhaul and LTE or 5G uplinks.

- Cisco Systems Inc.

- Huawei Technologies Co Ltd.

- Nokia Corporation

- Hewlett Packard Enterprise Company

- Arista Networks Inc.

- TP-Link Technologies Co Ltd.

- Netgear Inc.

- D-Link Corporation

- Zyxel Communications Corp.

- Ubiquiti Inc.

- MikroTik SIA

- DrayTek Corp.

- Extreme Networks Inc.

- Cambium Networks Corp.

- Peplink International Ltd.

- Digi International Inc.

- Advantech Co Ltd.

- Teltonika Networks UAB

- Edgecore Networks Corporation

- Cradlepoint Inc.

- Sierra Wireless Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Broadband Penetration and Demand for High-Speed Home Networking

- 4.2.2 Proliferation of Cloud Services Requiring Advanced Enterprise Routing

- 4.2.3 Rapid Adoption of Wi-Fi 6 and Wi-Fi 7 Standards

- 4.2.4 Emergence of Multi-Access Edge Computing Driving Micro-Edge Routers

- 4.2.5 Regulatory Push for Open Standards (TIP, OpenWiFi) Encouraging Disaggregated Routers

- 4.2.6 Increasing Demand for Deterministic Networking in Industrial TSN Routers

- 4.3 Market Restraints

- 4.3.1 Supply Chain Shortages and Semiconductor Price Volatility

- 4.3.2 Intense Price Competition Commoditizing Consumer Routers

- 4.3.3 Growing Cybersecurity Certification Costs Under Zero-Trust Mandates

- 4.3.4 Sustainability Regulations Penalizing High Idle Power Consumption of Core Routers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Router Type

- 5.1.1 Wired Routers

- 5.1.2 Wireless Routers

- 5.1.3 Cellular Routers

- 5.2 By Performance Tier

- 5.2.1 Low Throughput (<1 Gbps)

- 5.2.2 Mid Throughput (1-10 Gbps)

- 5.2.3 High Throughput (10-100 Gbps)

- 5.2.4 Ultra-High (>100 Gbps)

- 5.3 By End User

- 5.3.1 Residential/Consumer

- 5.3.2 IT and Telecom

- 5.3.3 BFSI

- 5.3.4 Government and Defense

- 5.3.5 Manufacturing

- 5.3.6 Transportation and Logistics

- 5.3.7 Others End Users

- 5.4 By Sales Channel

- 5.4.1 Online Marketplaces

- 5.4.2 Direct Sales

- 5.4.3 Distributors/Value-Added Resellers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Huawei Technologies Co Ltd.

- 6.4.3 Nokia Corporation

- 6.4.4 Hewlett Packard Enterprise Company

- 6.4.5 Arista Networks Inc.

- 6.4.6 TP-Link Technologies Co Ltd.

- 6.4.7 Netgear Inc.

- 6.4.8 D-Link Corporation

- 6.4.9 Zyxel Communications Corp.

- 6.4.10 Ubiquiti Inc.

- 6.4.11 MikroTik SIA

- 6.4.12 DrayTek Corp.

- 6.4.13 Extreme Networks Inc.

- 6.4.14 Cambium Networks Corp.

- 6.4.15 Peplink International Ltd.

- 6.4.16 Digi International Inc.

- 6.4.17 Advantech Co Ltd.

- 6.4.18 Teltonika Networks UAB

- 6.4.19 Edgecore Networks Corporation

- 6.4.20 Cradlepoint Inc.

- 6.4.21 Sierra Wireless Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment