|

시장보고서

상품코드

2073107

중동 및 아프리카의 그린 IT 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Middle East and Africa Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

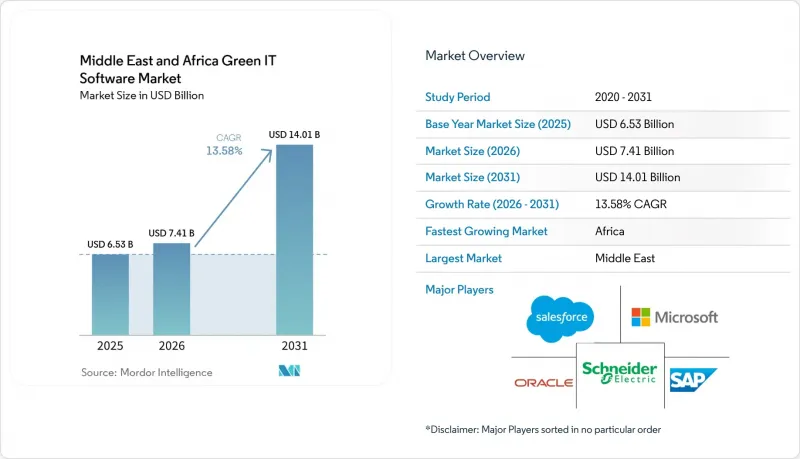

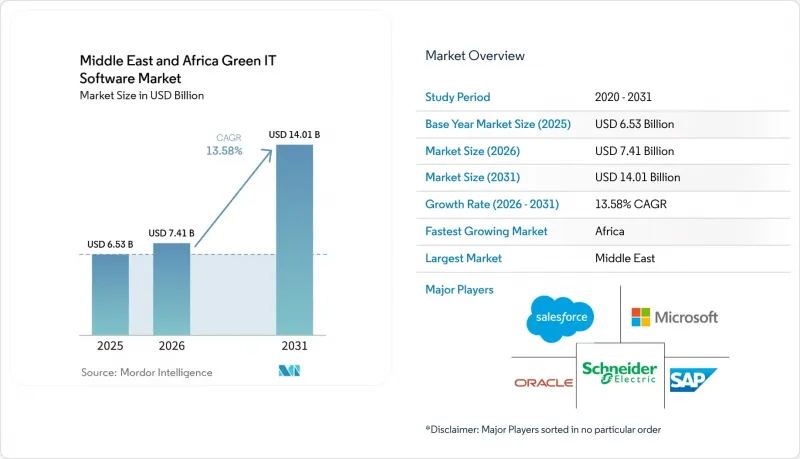

Mordor Intelligence에 의하면, 중동 및 아프리카 그린 IT 소프트웨어 시장 규모는 2025년 65억 3,000만 달러, 2026년 74억 1,000만 달러에서 2031년까지 140억 1,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 13.58%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 용도(탄소 회계 및 배출량 보고 등), 도입 형태(클라우드 기반 및 On-Premise형), 조직 규모(대기업 및 중소기업), 최종 사용자(제조업, 소매 및 전자상거래 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 아프리카 그린 IT 소프트웨어 시장 동향과 인사이트

지속가능성 보고 의무화와 감사 대응에 대한 압박

기후 변화 정보 공개 의무는 이미 중동 및 아프리카의 그린 IT 소프트웨어 시장 전반에서 단기적인 구매를 촉진하는 요인이 되고 있습니다. 이는 규정 준수 기한을 지키지 않을 경우 법적 및 업무상 직접적인 영향을 초래하게 되었기 때문입니다. UAE의 기후 변화 프레임워크와 이집트가 2026년 2월 비은행 금융기관을 대상으로 결정한 조치는 모두 기업들이 배출량 데이터를 정리하고, 검증을 지원하며, 공식 심사를 견딜 수 있는 기록을 작성할 수 있는 시스템의 도입을 촉진하고 있습니다. 이집트 금융 규제 당국은 자본금이 1억 이집트 파운드(204만 달러)를 초과하는 비은행 금융기관에 대해 스코프 1 및 스코프 2의 공시와 제3자 검증을 의무화하고, 2026년 6월까지 관련 규정을 준수할 것을 요구하고 있습니다. 공급업체에게 중요한 점은 구매자들이 더 이상 지속가능성 소프트웨어를 독립된 보고 계층으로 취급하지 않는다는 사실입니다. 왜냐하면 수작업에 의한 재처리를 최소화하면서도 감사, 재무, 거버넌스의 일상 업무에 통합할 수 있는 시스템을 원하는 경향이 강해지고 있기 때문입니다. 이에 따라 중동 및 아프리카(MEA) 지역의 그린 IT 소프트웨어 시장에서는 공시 워크플로우, 증거 추적, 그리고 변화하는 보고 의무를 단일 환경에서 처리할 수 있는 플랫폼에 대한 선호도가 높아지고 있습니다.

클라우드 네이티브형 ESG 및 에너지 분석의 도입 확대

2025년 중동 및 아프리카의 그린 IT 소프트웨어 시장에서 클라우드 기반 플랫폼은 71.33%의 점유율을 차지하고 있으며, 이러한 우위는 단순한 구독 경제의 범위를 넘어선 것입니다. 이 지역의 많은 구매자들은 공시 의무가 이미 도입된 후에 이 분야에 진출했기 때문에 장기간의 인프라 구축이 필요하지 않고 신속하게 가동을 시작하며 기존 기업 시스템과 연동할 수 있는 제공 모델을 선호했습니다. 이는 또한 중동 및 아프리카의 그린 IT 소프트웨어 시장이, 특히 공시 요건이 강화되기 시작한 후 지속가능성 팀이 설립된 사례에서 초기 도입 단계에서 여전히 SaaS(Software-as-a-Service)형 도구를 선호하는 이유를 설명해 줍니다. 클라우드 네이티브 환경에서는 분산된 사업 거점 전체에서 이용 데이터를 수집하여 경영진이나 외부 심사 담당자를 위한 정형화된 보고서로 변환할 수 있기 때문에 에너지 분석에 대한 제2 수요층이 부상하고 있습니다. 구매자층이 확대됨에 따라, 사내 지속가능성 데이터 처리 체계가 아직 구축 중인 단계라 하더라도, 클라우드 도구는 조달부터 운영 개시까지의 과정을 신속하게 진행할 수 있기 때문에 그 매력은 앞으로도 계속 유지될 것입니다.

레거시 IT 환경에서의 지속가능성 데이터 품질 저하

중동 및 아프리카의 그린 IT 소프트웨어 시장에서 가장 큰 걸림돌은 대개 소프트웨어에 대한 수요 자체가 아니라, 새로운 도구를 활용하기 위해 필요한 데이터의 품질이 낮다는 점에 있습니다. 많은 기존 ERP, 시설 관리 및 운영 시스템은 자산 단위의 전력 사용량을 파악하거나, 신뢰할 수 있는 배출량 산정에 필요한 메타데이터를 정리하는 것을 염두에 두고 구축되지 않았기 때문에 각 팀은 수작업이나 파편화된 파일에 의존할 수밖에 없는 상황에 처해 있습니다. 이 문제는 지속가능성, 재무, IT, 운영 부서가 각각 데이터 체인의 일부를 관리하는 분야에서 특히 중요하며, 책임 소재가 불분명하기 때문에 소프트웨어 예산이 승인된 후에도 도입이 지연될 가능성이 있습니다. 그 결과, 중동 및 아프리카의 그린 IT 소프트웨어 시장에서는 특히 첫 도입 시에 조달부터 본격적인 운영 개시까지의 과정에서 여전히 큰 실행상의 격차가 존재하고 있습니다. 구매자가 데이터 정비 상태가 규정 준수를 통해 얻는 이점을 얼마나 신속하게 실현할 수 있는지를 좌우한다는 사실을 인식하게 될수록, 더 우수한 템플릿, 커넥터, 거버넌스 워크플로우 및 도입 지원을 제공할 수 있는 벤더일수록 관심을 보이는 고객을 실제 성공 사례로 이끌 가능성이 높아집니다.

부문별 분석

2025년 구성 비율에서 소프트웨어는 68.29%를 차지하며, 중동 및 아프리카의 그린 IT 소프트웨어 시장에서 확고한 선두 자리를 유지하고 있습니다. 이러한 경쟁력은 광범위한 시스템 교체를 강요하지 않고, 기존 ERP 및 보고 환경 위에 구축할 수 있는 ESG, 탄소 회계, 에너지 분석 플랫폼을 구매자들이 선호하고 있음을 반영합니다. 많은 기업이 여전히 도입 초기 단계에 있기 때문에 기존 워크플로우에 통합 가능한 소프트웨어 모듈의 매력은 여전히 크며, 특히 가치 실현까지 걸리는 시간을 단축해야 하는 재무, IT, 지속가능성 부서에서 이러한 경향이 두드러집니다. 또한, 소프트웨어 부문은 대부분의 조직이 정보 공개나 데이터 관리의 필요성을 계기로 이 분야에 진출한다는 점에서도 혜택을 보고 있습니다. 이러한 요구 사항은 일반적으로 하드웨어나 인프라에 대한 투자가 아닌, 플랫폼을 통해 해결되기 때문입니다.

이 서비스 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 15.12%를 나타낼 것으로 예측되며, 중동 및 아프리카의 그린 IT 소프트웨어 시장에서 가장 빠르게 성장하는 부문이 될 것입니다. 이러한 성장은 데이터가 레거시 ERP, 클라우드, 시설 시스템 등 서로 다른 형식과 소유권 규칙을 가진 시스템에 분산되어 있을 때, 구매자가 필요로 하는 도입, 통합, 지원 및 유지보수 업무에서 비롯됩니다. DXC는 이집트의 센터 오브 엑설런스, 사우디아라비아의 SAP 아카데미, 그리고 300명 이상의 SAP 전문가 채용을 통해 해당 지역 전체에서 SAP 역량을 강화했습니다. 이는 소프트웨어 수요와 함께, 인증된 도입 역량에 대한 수요도 증가하고 있음을 보여줍니다. 새로운 수치를 산출하지 않더라도, 중동 및 아프리카의 그린 IT 소프트웨어 시장 내 서비스 규모는 기업이 감사에 대응할 수 있는 보고서를 작성하기 전에 데이터 계보, 거버넌스 절차 및 보증 방법을 문서화해야 할 필요성에 의해 분명히 뒷받침되고 있습니다. 또한, 이러한 경향은 복잡하고 여러 사업체를 포함하는 도입의 경우 표준 기능만으로는 불충분하기 때문에 많은 구매자가 여전히 실질적인 지원을 필요로 하고 있음을 보여줍니다.

2025년에는 ESG 보고 및 공시가 용도 매출의 35.23%를 차지하며, 중동 및 아프리카의 그린 IT 소프트웨어 시장에서 가장 큰 용도 분야가 되었습니다. 이 결과는 현재의 규제 상황과 일치합니다. 이는 해당 지역의 단기적 의무 중 상당수가 직접적인 배출 감축 목표보다는 우선적으로 정보 공개 준비, 증거 처리 및 보고 체계에 중점을 두고 있기 때문입니다. 따라서 구매 담당자들은 계속해서 지표를 통합하고, 출력을 표준화하며, 사내외 보고 주기를 지원할 수 있는 플랫폼을 중심으로 도입을 추진하고 있습니다. 이에 따라, 특히 상장 기업, 규제 대상 기관 및 여러 국가에 걸친 보고 요구 사항이 있는 기업에서 공시 도구가 조기 도입의 핵심적인 위치를 계속 차지하고 있습니다.

탄소 회계 및 배출량 보고 시장은 2031년까지 연평균 성장률(CAGR) 14.09%를 나타낼 것으로 예측되며, 이는 중동 및 아프리카의 그린 IT 소프트웨어 시장이 기본적인 규정 준수를 넘어 보다 적극적인 측정 및 계획 단계로 전환되고 있음을 보여줍니다. SAP의 “2026 지속가능성 컨트롤 타워” 업데이트에서는 규제 대응 및 데이터 매핑에 대한 AI 지원이 강화되었습니다. 이는 배출량 정보를 보다 실용적인 운영 데이터 세트로 변환할 수 있는 도구에 대한 구매자 수요와 부합합니다. 또한, 기업들이 탄소 배출량 시각화를 전력 비용 관리, 냉각 효율, 인프라 성능과 연계함에 따라 에너지 모니터링 및 최적화의 중요성도 커지고 있습니다. 수출업체와 공급업체들이 검증된 업스트림 데이터에 대한 요구가 높아지는 상황에 직면함에 따라, 공급망의 지속가능성 관리에 대한 관심도 커지고 있습니다. 한편, 폐기물 및 물 관련 응용 분야는 이 지역의 많은 지역에서 여전히 초기 단계에 머물러 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the middle east and Africa Green IT Software Market size is projected to expand from USD 6.53 billion in 2025 and USD 7.41 billion in 2026 to USD 14.01 billion by 2031, registering a CAGR of 13.58% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Application (Carbon Accounting and Emissions Reporting, and More), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), End User (Manufacturing, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Middle East and Africa Green IT Software Market Trends and Insights

Mandatory Sustainability Reporting and Audit Readiness Pressure

Mandatory climate disclosure has already become a near-term buying trigger across the Middle East and Africa Green IT Software Market because compliance deadlines now carry direct legal and operational consequences. The UAE climate framework and Egypt's February 2026 decision for non-banking financial institutions both pushed enterprises toward systems that can organize emissions data, support verification, and produce records that withstand formal review. Egypt's Financial Regulatory Authority required Scope 1 and Scope 2 disclosures, along with third-party verification, for non-banking financial institutions with capital above EGP 100 million (USD 2.04 million), with compliance due by June 2026. What matters for vendors is that buyers are no longer treating sustainability software as a separate reporting layer, because they increasingly want systems that can fit into audit, finance, and governance routines with less manual rework. This is why the MEA Green Information Technology software market is seeing a stronger preference for platforms that can handle disclosure workflows, evidence trails, and changing reporting obligations in one environment.

Rising Cloud-Native ESG and Energy Analytics Adoption

Cloud-based platforms held 71.33% of the 2025 Middle East and Africa Green IT Software Market, and that lead reflects more than simple subscription economics. Many regional buyers entered the category after mandatory reporting requirements had already been introduced, so they favored delivery models that could go live quickly and connect with existing enterprise systems without a lengthy infrastructure build. This also explains why the Middle East and Africa Green IT Software Market continues to lean toward software-as-a-service tools for first deployments, especially where sustainability teams were created after disclosure requirements had already started to tighten. A second layer of demand is emerging for energy analytics, as cloud-native environments can collect usage data across dispersed operations and turn it into repeatable reports for management teams and external reviewers. As the buyer base widens, the appeal of cloud tools is likely to remain strong because they give organizations a faster path from procurement to operational use, even when internal sustainability data processes are still being built.

Limited Sustainability Data Quality across Legacy IT Estates

The biggest brake on the Middle East and Africa Green IT Software Market is often not software demand, but the poor condition of the data that new tools are expected to use. Many legacy ERP, facilities, and operations systems were never built to capture electricity use at the asset level or to organize the metadata needed for credible emissions calculations, leaving teams to rely on manual work and fragmented files. That problem is especially important in sectors where sustainability, finance, IT, and operations each control parts of the data chain, because unclear ownership can slow implementation even after software budgets are approved. As a result, the Middle East and Africa Green IT Software Market still carries a meaningful execution gap between procurement and full operational use, particularly in first-time deployments. Vendors that can provide better templates, connectors, governance workflows, and onboarding support are more likely to convert interest into successful use, as buyers increasingly recognize that data readiness determines how quickly compliance benefits can be realized.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Carbon Accounting and Workload Optimization

- Multinational Supplier Traceability Requirements

- Shortage of Skilled ESG and Carbon Data Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 68.29% of the 2025 component mix, keeping it firmly in the leading position in the Middle East and Africa Green IT Software Market. That lead reflects buyer preference for ESG, carbon accounting, and energy analytics platforms that can sit on top of existing ERP and reporting environments, rather than forcing a broad system replacement. Many enterprises are still in an early deployment phase, so the appeal of software modules that can be integrated into existing workflows remains strong, especially for finance, IT, and sustainability teams that need faster time-to-value. The software segment also benefits from the fact that most organizations first enter this category through disclosure or data management needs, which are usually addressed through platforms rather than hardware or infrastructure spending.

Services are projected to grow at a 15.12% CAGR from 2026 to 2031, making them the fastest-rising component category in the Middle East and Africa Green IT Software Market. This growth comes from implementation, integration, support, and maintenance work that buyers need when data sits across legacy ERP, cloud, and facility systems with different formats and ownership rules. DXC expanded SAP capabilities across the region through a center of excellence in Egypt, a SAP academy in Saudi Arabia, and the recruitment of more than 300 SAP professionals, which illustrates how demand for certified delivery capacity is rising alongside software demand. Even without calculating new values, the Middle East and Africa Green IT Software Market size for services is clearly supported by the need to document data lineage, governance routines, and assurance methods before enterprises can claim audit-ready reporting. The pattern also shows that many buyers still need hands-on support because out-of-the-box functionality alone is not enough for complex, multi-entity deployments.

ESG reporting and disclosure accounted for 35.23% of application revenue in 2025, making it the largest application area across the Middle East and Africa Green IT Software Market. That result is consistent with the current regulatory landscape, since most near-term obligations in the region have focused first on disclosure readiness, evidence handling, and reporting structure rather than on direct emissions-reduction targets. Buyers, therefore, continue to start with platforms that can centralize metrics, standardize outputs, and support internal and external reporting cycles. This keeps disclosure tools at the center of early adoption, particularly among listed firms, regulated institutions, and enterprises with multi-country reporting needs.

Carbon accounting and emissions reporting are forecast to grow at a 14.09% CAGR through 2031, indicating that the Middle East and Africa Green IT Software Market is moving from basic compliance toward more active measurement and planning. SAP's 2026 Sustainability Control Tower updates strengthened AI support for regulatory readiness and data mapping, which aligns with buyer demand for tools that can turn emissions information into a more usable operational dataset. Energy monitoring and optimization are also becoming more important as enterprises link carbon visibility with electricity cost control, cooling efficiency, and infrastructure performance. Supply chain sustainability management is attracting stronger interest as exporters and suppliers face growing requests for verified upstream data, while waste and water applications are still at an earlier stage across much of the region.

Complete Report Scope:

- By Component

- Software

- Services

- Implementation and Integration Services

- Support and Maintenance Services

- By Application

- Carbon Accounting and Emissions Reporting

- Energy Monitoring and Optimization

- Environmental, Social, and Governance (ESG) Reporting and Disclosure

- Supply Chain Sustainability Management

- Green IT Asset and Data Center Optimization

- Other Applications

- By Deployment Mode

- Cloud-Based

- On-Premises

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End User

- Information Technology and Telecom

- Banking, Financial Services, and Insurance

- Manufacturing

- Government and Public Sector

- Energy and Utilities

- Healthcare and Life Sciences

- Retail and E-Commerce

- Other End Users

- By Geography

- Middle East

- Gulf Cooperation Council (GCC)

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- SAP SE

- Microsoft Corporation

- IBM Corporation

- Schneider Electric SE

- Oracle Corporation

- Salesforce, Inc.

- Wolters Kluwer N.V.

- Sphera Solutions, Inc.

- Cority Software Inc.

- Enablon North America Corp.

- Benchmark Gensuite, LLC

- Intelex Technologies ULC

- Diligent Corporation

- Workiva Inc.

- FigBytes Inc.

- Envirosuite Limited

- ESG Book GmbH

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Plan A Solutions GmbH

- Normative AB

- Sweep SAS

- Eniscope Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory Sustainability Reporting and Audit Readiness Pressure

- 4.2.2 Rising Cloud-Native ESG and Energy Analytics Adoption

- 4.2.3 AI-Enabled Carbon Accounting and Workload Optimization

- 4.2.4 Multinational Supplier Traceability Requirements

- 4.2.5 Energy Cost Volatility and IT Efficiency Mandates

- 4.2.6 Digital Sovereignty and Local Data Hosting Buildouts

- 4.3 Market Restraints

- 4.3.1 Limited Sustainability Data Quality Across Legacy IT Estates

- 4.3.2 Shortage of Skilled ESG and Carbon Data Specialists

- 4.3.3 Integration Complexity Across ERP, Cloud, and IoT Stacks

- 4.3.4 Budget Prioritization Versus Core Revenue Software

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Technology Outlook

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Support and Maintenance Services

- 5.2 By Application

- 5.2.1 Carbon Accounting and Emissions Reporting

- 5.2.2 Energy Monitoring and Optimization

- 5.2.3 Environmental, Social, and Governance (ESG) Reporting and Disclosure

- 5.2.4 Supply Chain Sustainability Management

- 5.2.5 Green IT Asset and Data Center Optimization

- 5.2.6 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End User

- 5.5.1 Information Technology and Telecom

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Manufacturing

- 5.5.4 Government and Public Sector

- 5.5.5 Energy and Utilities

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Retail and E-Commerce

- 5.5.8 Other End Users

- 5.6 By Geography

- 5.6.1 Middle East

- 5.6.1.1 Gulf Cooperation Council (GCC)

- 5.6.1.2 Turkey

- 5.6.1.3 Rest of Middle East

- 5.6.2 Africa

- 5.6.2.1 South Africa

- 5.6.2.2 Nigeria

- 5.6.2.3 Rest of Africa

- 5.6.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Microsoft Corporation

- 6.4.3 IBM Corporation

- 6.4.4 Schneider Electric SE

- 6.4.5 Oracle Corporation

- 6.4.6 Salesforce, Inc.

- 6.4.7 Wolters Kluwer N.V.

- 6.4.8 Sphera Solutions, Inc.

- 6.4.9 Cority Software Inc.

- 6.4.10 Enablon North America Corp.

- 6.4.11 Benchmark Gensuite, LLC

- 6.4.12 Intelex Technologies ULC

- 6.4.13 Diligent Corporation

- 6.4.14 Workiva Inc.

- 6.4.15 FigBytes Inc.

- 6.4.16 Envirosuite Limited

- 6.4.17 ESG Book GmbH

- 6.4.18 Persefoni AI, Inc.

- 6.4.19 Watershed Technology, Inc.

- 6.4.20 Plan A Solutions GmbH

- 6.4.21 Normative AB

- 6.4.22 Sweep SAS

- 6.4.23 Eniscope Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment