|

시장보고서

상품코드

2073212

아시아태평양의 그린 IT 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

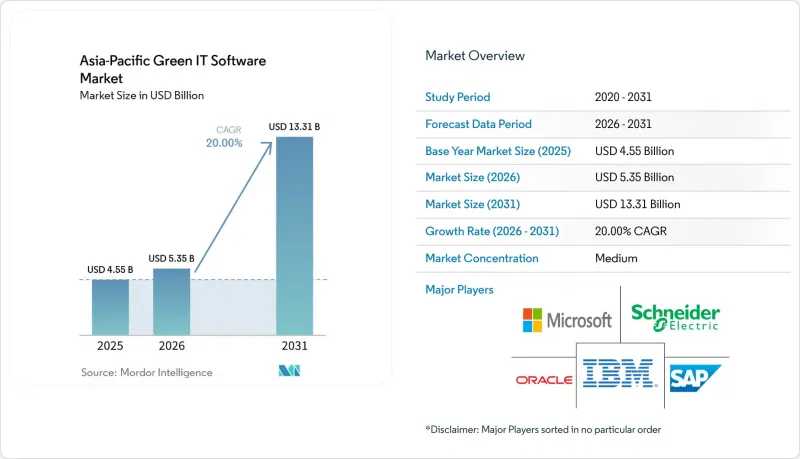

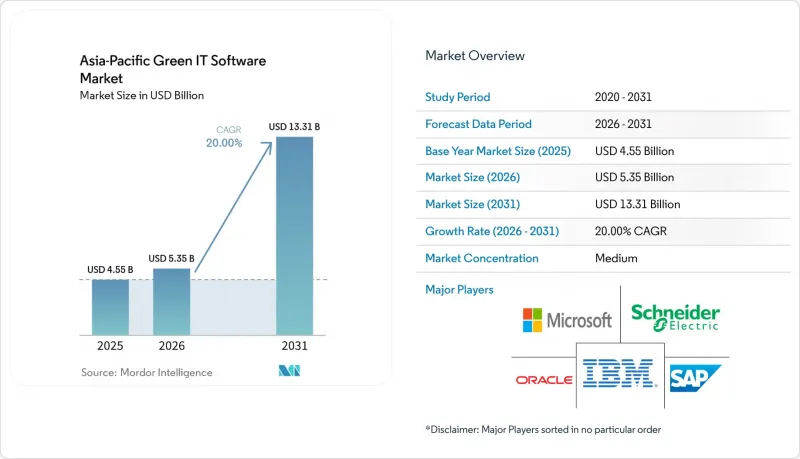

Mordor Intelligence에 의하면, 아시아태평양 그린 IT 소프트웨어 시장 규모는 2025년 45억 5,000만 달러에서 2026년에는 53억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 20.00%로 성장을 지속하여, 2031년에는 133억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드 기반, 하이브리드 등), 기업 규모(대기업 및 중소기업), 솔루션 유형(탄소 관리·산정 소프트웨어 등), 최종 사용자 산업 분야(정보기술·통신 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

아시아태평양의 그린 IT 소프트웨어 시장 동향 및 분석

아시아태평양의 ESG 공시 의무

공개 의무화 규제로 인해 아시아태평양의 그린 IT 소프트웨어 시장에서 현재 가장 강력한 수요 기반이 형성되고 있습니다. 이는 규정 준수 기한이 임박함에 따라, 기업이 플랫폼에 대한 투자를 미루기보다는 보고 절차를 공식적으로 확립해야 하기 때문입니다. 중국은 2026년에 A주 상장 기업을 대상으로 한 최초의 의무 보고 주기로 전환함에 따라, 많은 대기업들에게 정보 공시 준비가 단기적인 경영상의 최우선 과제가 되었습니다. 일본에서도 2026년 2월 26일 금융청이 SSBJ에 부합하는 공시 기준을 확정함에 따라 규제 추진이 진전되었으며, 대형 상장 기업에 대해 보고 의무와 관련된 보다 명확한 일정이 제시되었습니다. 싱가포르와 호주에서는 이미 기후 변화 보고 제도의 도입이 더욱 진전되어, 규정 준수 수준이 높아지고 준비 기간이 단축되는 등 지역 전체에서 나타나는 추세를 더욱 강화하는 결과를 낳았습니다. 이러한 일련의 움직임이 중요한 이유는 소프트웨어 선정이 제출 마감일이 다가올 무렵에 이루어지게 되었기 때문입니다. 이로 인해 기성 템플릿을 갖추고, 도입 지원이 충실하며, 감사 추적이 확립된 벤더가 유리해집니다. 또한, 각 규제가 발효될 때마다 첫 구매자나 재구매자에 의한 집중적인 구매 물결이 일어나기 때문에 아시아태평양의 그린 IT 소프트웨어 시장의 상업적 규모 확대를 가속화하는 결과로 이어집니다.

AI를 활용한 지속가능성 데이터 수집의 자동화

AI는 여러 프레임워크에 걸쳐 정보를 수집, 분류, 매핑하는 데 필요한 수작업을 줄여줌으로써 아시아태평양의 그린 IT 소프트웨어 시장의 가치 제안을 향상시키고 있습니다. SAP는 2026년 5월, 기존 지속가능성 워크플로우 내에서 규제 준수 및 공급망 탄소 인텔리전스를 지원하기 위한 도구를 포함한 새로운 지속가능성 AI 에이전트를 발표했습니다. IBM도 2026년에 Envizi의 기능을 활용하여 실용적인 배출량 산정 도구를 확충하고, 인증된 배출 계수를 기존의 스프레드시트나 기업 프로세스에 반영할 수 있게 했습니다. Workiva는 2026년, 아시아태평양에서의 사업 확장을 한층 더 강화했습니다. 이는 보다 광범위한 지역 확장을 지원할 수 있는 보고서 작성 자동화에 대한 기업 수요가 증가하고 있음을 반영합니다. 자동화가 진행됨에 따라 기업들은 추가적인 노력을 최소화하면서 새로운 프레임워크를 도입할 수 있게 되었으며, 그 결과 데이터 수집, 공시 내용 검토, 거버넌스 관리를 단일 환경에서 통합한 플랫폼에 대한 구매 우선순위가 변화하고 있습니다. 이러한 변화에 따라 아시아태평양의 그린 IT 소프트웨어 시장은 제한된 범위의 규정 준수 사례에 그치지 않고, 보다 광범위한 업무 분야로의 도입으로 전환되고 있습니다.

아시아태평양의 보고 체계와 분류 체계의 파편화

규제의 파편화는 여전히 아시아태평양의 그린 IT 소프트웨어 시장 성장 속도를 제한하고 있습니다. 이는 국경을 넘어 사업을 전개하는 기업이 종종 서로 다른 일정, 보증 요건 및 보고 기준에 직면하기 때문입니다. OECD는 2025년, 해당 지역에서 지속가능성 관련 정보 공개에 대한 관심이 높아지고 있음을 강조했으나, 각국의 접근 방식은 여전히 범위와 중점 사항 면에서 차이가 있습니다. 일본의 공시 절차는 SSBJ에 부합하는 기준에 따라 진행되는 반면, 싱가포르는 현지 규제 절차를 통해 독자적인 보고 및 보증 체계를 적용하고 있습니다. 이 때문에 조달 단계에서 망설임이 생깁니다. 구매자들은 수년에 걸친 도입을 결정하기 전에, 해당 플랫폼이 여러 규칙집에 동시에 부합할 수 있다는 증거를 요구하고 있기 때문입니다. 공급업체 네트워크가 여러 시장에 걸쳐 있으며, 전환 활동, 중요도 또는 보증 범위에 대해 서로 다른 정의를 사용하고 있는 경우, 이 문제는 더욱 복잡해집니다. 수요가 견조하더라도, 새로운 시스템을 도입할 때마다 추가적인 매핑, 맞춤 설정, 법적 검토가 필요하기 때문에 아시아태평양의 그린 IT 소프트웨어 시장의 성장 효율성은 떨어지게 됩니다.

부문별 분석

2025년에는 소프트웨어가 시장의 63.47%를 차지하고 있으며, 이는 구독형 플랫폼이 아시아태평양의 그린 IT 소프트웨어 시장의 주요 수익 기반으로서 계속해서 자리 잡고 있음을 보여줍니다. 구매자가 이 소프트웨어를 선호한 이유는 구독 모델을 통해 더 신속한 업데이트, 더 명확한 감사 추적, 그리고 반복되는 보고 주기에 대한 더 나은 관리가 가능하기 때문입니다. 또한, 공개 프레임워크의 변경 빈도가 높아짐에 따라 정적인 프로젝트 기반의 작업은 시간이 지남에 따라 실용성을 잃어가고 있으며, 플랫폼에 대한 수요도 증가하고 있습니다. 고객이 데이터 수집, 계산, 검토 및 최종 결과물 공개를 통합적으로 수행할 수 있는 환경을 원할 경우, 소프트웨어 공급업체는 그 혜택을 누리게 됩니다. 따라서 아시아태평양의 ESG 및 지속가능성 소프트웨어 업계에서 이 분야는 일회성 자문 업무보다는 운영상의 보고 요구 사항과 더욱 밀접하게 연계되고 있습니다.

서비스 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 22.96%로 확대될 것으로 예상되며, 이는 새로 공시 대상이 된 관할 구역 내 최초 공시 기업들의 단기적인 수요를 반영한 것입니다. 많은 기업들은 플랫폼을 안심하고 이용할 수 있게 되기 전에, 격차 평가, 데이터 준비 현황 확인, 공시 체계 해석, 그리고 첫 번째 공시 주기 준비와 관련해 여전히 지원이 필요합니다. 따라서, 도입 및 관리형 지원 기능을 갖춘 소프트웨어 공급업체는 새로운 보고 단계의 첫 12-24개월 동안 더 유리한 입장에 있습니다. 시간이 지남에 따라 사내 팀이 프로세스에 익숙해지고 거버넌스 절차가 안정화됨에 따라, 고객은 대개 셀프 서비스 방식의 이용으로 전환하게 됩니다. 이는 소프트웨어가 아시아태평양의 그린 IT 소프트웨어 시장의 장기적인 기반이 되는 한편, 서비스가 초기 도입을 가속화할 수 있음을 의미합니다.

2025년, 아시아태평양의 그린 IT 소프트웨어 시장 점유율 중 클라우드 기반 도입이 61.94%를 차지했으며, 보고 규정이 급속히 변화하는 가운데 구매자들이 여전히 유연한 제공 방식을 선호하고 있음이 입증되었습니다. 클라우드 시스템을 통해 기업은 사내 업그레이드 일정에 따른 장기간의 대기 시간 없이 템플릿 업데이트, 변경 사항 관리, 새로운 계산 로직 도입이 가능해집니다. 아시아태평양의 그린 IT 소프트웨어 시장에서 이는 중요한 의미를 지닙니다. 이는 여러 국가의 보고 시스템이 동시에 개발되고 있기 때문입니다. 또한, 일부 다국적 기업들은 기밀 데이터 수집을 현장 업무와 가까운 곳에서 유지하면서 클라우드상에서 통합적인 분석을 수행하고자 하기 때문에 하이브리드 도입도 더욱 확산되고 있습니다. 이러한 경향은 도입 결정이 더 이상 단일한 기술적 선호에 기반하지 않고, 거버넌스상의 필요에 따라 이루어지고 있음을 보여줍니다.

On-Premise 배포는 2026년부터 2031년까지 연평균 성장률(CAGR) 21.59%로 확대될 것으로 예측되며, 이는 더 엄격한 데이터 관리 요건을 가진 기관들 사이에서 견고한 틈새 시장을 유지할 것임을 시사합니다. 금융 기관, 정부 산하 기업 및 방위 관련 제조업체는 대부분의 경우 데이터 저장, 전송 및 시스템 접근에 대해 보다 강력한 관리가 필요합니다. 이러한 경우, On-Premise나 사설 환경이 선택되는 이유는 편의성보다는 규제 및 정책적 제약 때문인 경우가 많습니다. 따라서 클라우드가 여전히 더 큰 수익 기반을 차지하고 있기는 하지만, 이 부문의 성장 요인은 클라우드와는 다릅니다. 아시아태평양의 그린 IT 소프트웨어 시장은 데이터 주권에 따라 더욱 세분화되고 있으며, 벤더가 대형 다국적 기업과 규제가 엄격한 국내 기관 모두에 서비스를 제공하고자 한다면 유연한 아키텍처가 필요합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the asia-Pacific green IT software market size is expected to grow from USD 4.55 billion in 2025 to USD 5.35 billion in 2026 and is forecast to reach USD 13.31 billion by 2031 at 20.00% CAGR over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, Hybrid, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and More), End-User Industry (Information Technology and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Green IT Software Market Trends and Insights

ESG Disclosure Mandates Across Asia-Pacific

Mandatory disclosure rules are creating the strongest current demand base for the Asia-Pacific green IT software market because compliance deadlines now require companies to formalize reporting processes instead of delaying platform investment. China moved toward its first mandatory reporting cycle for A-share listed companies in 2026, which made disclosure readiness a near-term operating priority for a large corporate base. Japan also advanced the regulatory path when the Financial Services Agency finalized SSBJ-aligned disclosure standards on February 26, 2026, giving large listed companies a clearer timetable for reporting obligations. Singapore and Australia were already further along in climate reporting rollout, which reinforced a wider regional pattern of rising compliance depth and shorter preparation windows. This sequence matters because software selection now happens closer to the filing deadline, which favors vendors with ready-built templates, stronger implementation support, and established audit trails. It also supports faster commercial scale for the Asia-Pacific green IT software market because each regulatory activation creates another concentrated wave of first-time and repeat buyers.

AI-Enabled Automation of Sustainability Data Capture

AI is improving the value case for the Asia-Pacific green IT software market because it reduces the manual effort needed to gather, classify, and map information across multiple frameworks. SAP announced new sustainability AI agents in May 2026, including tools intended to support regulatory readiness and supply chain carbon intelligence inside existing sustainability workflows. IBM also expanded practical emissions accounting tools in 2026 with Envizi capabilities that brought recognized emissions factors into existing spreadsheets and enterprise processes. Workiva continued to strengthen its Asia-Pacific commercial presence in 2026, which reflects growing enterprise demand for reporting automation that can support broader regional expansion. As automation improves, companies can add new frameworks with less extra labor, and that changes buying priorities toward platforms that combine data ingestion, disclosure review, and governance controls in one environment. This shift helps the Asia-Pacific green IT software market move beyond narrow compliance use cases and toward broader operating adoption.

Fragmented Asia-Pacific Reporting Frameworks and Taxonomies

Fragmented rules still limit the pace of the Asia-Pacific green IT software market because companies operating across borders often face different timelines, assurance needs, and reporting definitions. The OECD highlighted the region's widening focus on sustainability-related disclosure in 2025, but country approaches still differ in scope and emphasis. Japan's disclosure path is moving under SSBJ-aligned standards, while Singapore applies its own reporting and assurance structure through local regulatory channels. This creates hesitation during procurement because buyers want proof that a platform can adjust to several rulebooks at once before they commit to a multi-year rollout. The problem becomes more difficult when supplier networks span several markets and use different definitions for transition activity, materiality, or assurance depth. Even when demand stays strong, the Asia-Pacific green IT software market grows less efficiently when every new rollout needs extra mapping, customization, and legal review.

Other drivers and restraints analyzed in the detailed report include:

- Scope 3 Reporting Pressure on Supplier Networks

- Cloud Migration Lowering Software Carbon Intensity

- High Integration Effort With Legacy Enterprise Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 63.47% of the market in 2025, which shows that recurring platforms remain the main commercial base for the Asia-Pacific green IT software market. Buyers favored software because subscription models give them faster updates, clearer audit trails, and better control over repeat reporting cycles. Platform demand also rose because disclosure frameworks now change more frequently, which makes static project-based work less practical over time. Software providers benefit when customers want one environment for data capture, calculation, review, and final disclosure output. This part of the Asia-Pacific ESG and sustainability software industry has therefore become more closely tied to operational reporting needs than to one-time advisory engagement.

Services are projected to expand at a 22.96% CAGR from 2026 to 2031, which reflects the near-term needs of first-time filers across newly covered jurisdictions. Many companies still need help with gap assessments, data readiness checks, framework interpretation, and first-cycle disclosure preparation before they can use a platform with confidence. That is why software vendors with implementation and managed support capabilities are better placed during the first 12 to 24 months of a new reporting phase. Over time, customers usually move toward more self-service use as internal teams gain process familiarity and governance routines become stable. This means services can accelerate initial adoption even while software remains the long-run anchor of the Asia-Pacific green IT software market.

Cloud-based deployment accounted for 61.94% of the Asia-Pacific green IT software market share in 2025, confirming that buyers still prefer flexible delivery when reporting rules change quickly. Cloud systems help enterprises receive template updates, control changes, and new calculation logic without waiting for lengthy internal upgrade schedules. This matters in the Asia-Pacific green IT software market because several national reporting systems are being developed simultaneously. Hybrid deployment is also gaining ground because some multinationals want centralized analytics in the cloud while keeping sensitive data collection closer to site operations. That pattern shows that deployment decisions are increasingly based on governance needs rather than on a single technology preference.

On-premise deployment is projected to expand at a 21.59% CAGR from 2026 to 2031, indicating a durable niche among institutions with stricter data control requirements. Financial institutions, state-linked firms, and defense-adjacent manufacturers often need stronger control over storage, transfer, and system access. In these cases, the preference for on-premise or private environments is shaped less by convenience and more by regulatory and policy constraints. This segment therefore grows for a different reason than cloud, even though cloud still holds the larger revenue base. The Asia-Pacific green IT software market is becoming more segmented by data sovereignty, which means vendors need flexible architecture if they want to serve both large multinational buyers and tightly regulated domestic institutions.

Complete Report Scope:

- By offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End-User Industry

- Information Technology and Telecommunications

- Banking, Financial Services, and Insurance (BFSI)

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare

- Construction and Infrastructure

- Other End-User Industries

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Schneider Electric SE

- Oracle Corporation

- Salesforce, Inc.

- Workiva Inc.

- Wolters Kluwer N.V.

- Sphera Solutions, Inc.

- EcoVadis SAS

- Diligent Corporation

- Persefoni AI Inc.

- Greenly SAS

- Enablon, a Wolters Kluwer Company

- Benchmark Digital Partners LLC

- Cority Software Inc.

- Intelex Technologies ULC

- Siemens AG

- Cisco Systems, Inc.

- Accenture PLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ESG Disclosure Mandates Across Asia-Pacific

- 4.2.2 Cloud Migration Lowering Software Carbon Intensity

- 4.2.3 Data Center Power Efficiency and Cooling Optimization Priorities

- 4.2.4 Scope 3 Reporting Pressure on Supplier Networks

- 4.2.5 AI-Enabled Automation of Sustainability Data Capture

- 4.2.6 Green Procurement Linked to Enterprise Cost and Reputation Goals

- 4.3 Market Restraints

- 4.3.1 Fragmented Asia-Pacific Reporting Frameworks and Taxonomies

- 4.3.2 High Integration Effort With Legacy Enterprise Systems

- 4.3.3 Data Quality Gaps Across Supplier and Operational Systems

- 4.3.4 Shortage of Sustainability Analytics Talent

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End-User Industry

- 5.5.1 Information Technology and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance (BFSI)

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

- 5.6 By Country

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 India

- 5.6.4 South Korea

- 5.6.5 Australia

- 5.6.6 Singapore

- 5.6.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 Schneider Electric SE

- 6.4.5 Oracle Corporation

- 6.4.6 Salesforce, Inc.

- 6.4.7 Workiva Inc.

- 6.4.8 Wolters Kluwer N.V.

- 6.4.9 Sphera Solutions, Inc.

- 6.4.10 EcoVadis SAS

- 6.4.11 Diligent Corporation

- 6.4.12 Persefoni AI Inc.

- 6.4.13 Greenly SAS

- 6.4.14 Enablon, a Wolters Kluwer Company

- 6.4.15 Benchmark Digital Partners LLC

- 6.4.16 Cority Software Inc.

- 6.4.17 Intelex Technologies ULC

- 6.4.18 Siemens AG

- 6.4.19 Cisco Systems, Inc.

- 6.4.20 Accenture PLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment