|

시장보고서

상품코드

2073171

남미의 그린 IT 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

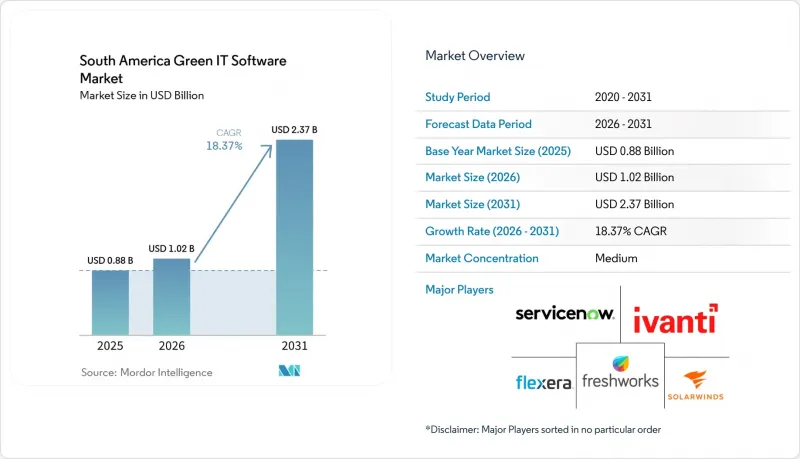

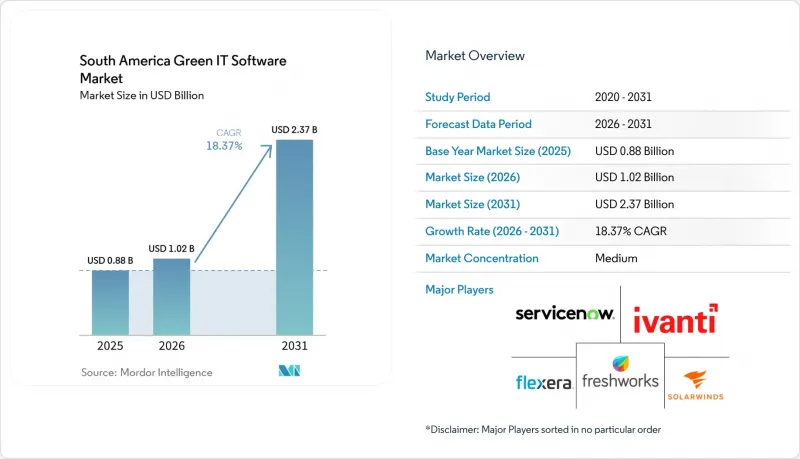

Mordor Intelligence에 의하면, 남미 그린 IT 소프트웨어 시장 규모는 2025년에 8억 8,000만 달러로 평가되었고 2026년 10억 2,000만 달러에서 2031년까지 23억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 18.37%를 나타낼 전망입니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 기업 규모(대기업 및 중소기업), 솔루션 유형(탄소 관리·산정 소프트웨어 등), 최종 사용자(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 에너지 및 유틸리티 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미 그린 IT 소프트웨어 시장 동향과 인사이트

강화되는 탄소 보고 및 ESG 규정 준수 요건

컴플라이언스는 남미의 그린 IT 소프트웨어 시장에서 여전히 가장 뚜렷한 단기 구매 동인으로 작용하고 있습니다. 기업들은 더 이상 대시보드만을 원하는 것이 아니라, 추적 가능한 데이터 수집, 재현 가능한 계산, 그리고 체계적인 보고서 작성 워크플로우를 지원하는 플랫폼을 필요로 하고 있습니다. 이러한 변화는 특히 대기업에 있어 가장 중요한데, 대기업에서는 지속가능성, 재무, 법무 및 IT 각 팀이 서로 흩어진 스프레드시트나 일회성 컨설팅 업무가 아닌, 공유 시스템을 필요로 하고 있습니다. 또한, 이러한 변화는 많은 도입 과정에서 탄소 관리 및 회계 소프트웨어가 여전히 가장 먼저 구매되는 대상인 이유를 설명하는 요인 중 하나이기도 합니다. 기업이 보고의 핵심이 되는 시스템을 도입하면, 다음 단계로 데이터 관리, 목표 추적, 워크플로우 관리를 위한 관련 모듈을 추가하는 경우가 많습니다. 이러한 양상 덕분에 남미의 그린 IT 소프트웨어 시장에는 단기적인 프로젝트 주기가 가져다주는 것보다 더 지속 가능한 수익 기반이 구축되고 있습니다.

에너지 효율이 높은 IT 운영에 대한 기업의 관심이 높아지고 있습니다.

남미의 그린 IT 소프트웨어 시장에서 에너지 효율은 단순한 부수적인 이점이 아니라 운영상의 우선 과제로 자리 잡고 있습니다. 디지털 워크로드 증가에 따라 IT 팀은 전력 소비량을 늘리지 않으면서 가동률을 모니터링하고, 유휴 용량을 파악하며, 성능을 향상시켜야 하는 과제에 직면해 있습니다. 이에 따라 소프트웨어 선정 업무가 지속가능성 팀에서 인프라, 운영, 플랫폼 엔지니어링 각 그룹으로 확대되고 있어, 구매자프로파일도 변화하고 있습니다. 또한, 에너지 최적화가 운영 비용, 가동 시간 계획, 자산 수명에 측정 가능한 효과를 가져온다는 점을 입증할 수 있다면, 그 가치 제안도 더욱 설득력을 갖게 될 것입니다. 이로 인해 아직 직접적인 보고 의무가 없는 기업에게도 그린 IT 소프트웨어는 중요한 요소가 됩니다. 장기적으로는 이러한 폭넓은 유용성 덕분에 남미의 그린 IT 소프트웨어 시장이 규정 준수를 중시하는 고객과 효율성을 중시하는 고객 모두에게서 도입이 더욱 확대될 것으로 기대됩니다.

레거시 IT 환경에서의 고도화된 통합의 복잡성

통합의 어려움은 남미의 그린 IT 소프트웨어 시장에서 도입을 가속화하는 데 있어 여전히 주요 장애물 중 하나입니다. 많은 기업에서는 표준화된 탄소 배출량 및 에너지 보고 도구에 데이터를 제공하도록 설계되지 않은 구식 ERP, 조달, 물류, 시설 관리, 서비스 관리 시스템을 운영하고 있습니다. 따라서 소프트웨어가 신뢰할 수 있는 결과를 생성할 수 있게 되기 전에, 구매 담당자는 다양한 형식, 소유자, 품질 수준에 걸친 데이터를 매핑해야 하기 때문에 도입 주기가 길어지게 됩니다. 또한, 벤더 선정 시에는 도입 지원, 미리 구축된 커넥터, 그리고 현지 파트너의 역량이 더욱 중요해집니다. 전 세계 플랫폼들은 대규모 지역 조직 전반에 걸친 운영 데이터의 파편화 정도를 과소평가할 경우, 추진력을 잃을 가능성이 있습니다. 따라서 남미의 그린 IT 소프트웨어 시장에서는 제품의 폭이 넓은 것뿐만 아니라 통합을 위한 준비 태세도 중요한 요소가 되는 경우가 많습니다.

부문별 분석

2025년, 남미의 그린 IT 소프트웨어 시장에서 소프트웨어가 76.14%의 점유율을 차지했습니다. 이는 구매자들이 여전히 시간이 지나도 구성 및 확장이 가능한 플랫폼을 선호하고 있음을 보여줍니다. 이러한 상황은 실질적인 요구를 반영한 것으로, 기업들은 배출량 데이터, 워크플로우 규칙, 보고서 템플릿, 감사 추적을 단일하고 반복 가능한 환경 내에서 관리할 수 있는 도구를 원하고 있습니다. 또한, 정보 공개에 대한 기대와 내부 거버넌스에 대한 요구가 정적인 보고 절차로는 따라잡을 수 없을 정도로 급속히 변화하고 있기 때문에 소프트웨어 계층은 시장의 방향성과도 부합하고 있습니다. 구매자는 요구 사항이 변경될 때마다 운영 모델을 재구축할 필요 없이 카테고리 업데이트, 계산 로직 조정, 새로운 모듈 추가가 가능하다는 점을 중요하게 생각합니다. 이에 따라 이 소프트웨어는 규모 확대, 지속성 및 내부 소유권을 지원함으로써 남미의 그린 IT 소프트웨어 시장에서 구조적인 우위를 점하고 있습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 18.43%를 나타낼 것으로 예측되며, 이는 소프트웨어 주도 시장에서도 도입 작업이 여전히 필수적임을 보여줍니다. 기업들은 레거시 시스템의 연동, 과거 기록의 정리, 책임의 명확화, 그리고 정기적인 보고 주기를 위한 거버넌스 규칙 수립에 있어 여전히 지원이 필요합니다. 또한, 많은 조직에서는 내부 성숙도가 높아짐에 따라 템플릿이나 관리 기법을 적용할 수 있도록 지원하는 것이 필요해지기 때문에 도입 후에도 자문 서비스와 관리형 서비스의 중요성은 더욱 커집니다. 그린 IT 소프트웨어 업계가 초기 도입 단계에서 더 광범위한 업무 기능에 걸친 지속적인 최적화 단계로 전환됨에 따라, 서비스 계층의 중요성은 더욱 커질 것으로 보입니다. 그렇긴 하지만, 가장 유망한 서비스 기회는 플랫폼 도입을 대체하는 것이 아니라 이를 보완하는 형태로 나타날 가능성이 높으며, 이로 인해 남미 그린 IT 소프트웨어 시장의 비즈니스 모델에서 소프트웨어가 계속해서 중심적인 위치를 차지하게 될 것입니다.

2025년, 남미의 그린 IT 소프트웨어 시장 규모 중 클라우드 기반 솔루션이 64.17%를 차지했습니다. 이는 확장 가능한 서비스 제공과 지속적인 제품 업데이트의 매력이 반영된 결과입니다. 이 모델은 장기간에 걸친 사내 업그레이드 프로젝트를 진행하지 않고도 새로운 보고서 템플릿, 워크플로 기능, 분석 기능의 출시를 원하는 기업에 적합합니다. 또한, 기술 환경의 표준화를 추진함으로써, 지역이나 기능을 초월하여 도입할 수 있는 구독형 소프트웨어를 선호하는 기업의 요구에도 부응하고 있습니다. 남미의 그린 IT 소프트웨어 시장에서 많은 구매자들이 먼저 보고서 작성이나 데이터 관리와 같은 이용 사례부터 도입을 시작한 뒤, 이후 플랫폼을 운영 분야로 확대해 나갑니다는 사실 또한 클라우드 도입을 뒷받침하고 있습니다. 이러한 순서를 통해 초기 부담이 줄어들고, 가치를 실현하기까지 걸리는 시간이 단축됩니다.

하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 18.52%로 확대될 것으로 예상되며, 이는 제어와 유연성이 종종 공존해야 한다는 점을 여실히 보여주고 있습니다. 기밀성이 높은 운영 데이터를 다루는 기업들은 여전히 클라우드 기반의 분석 및 보고서 작성 속도를 원하지만, 특정 레코드나 커넥터에 대해서는 관리된 사내 환경 내에 보관하는 것을 선호하는 경우가 있습니다. 이러한 구조는 모든 시스템을 한꺼번에 교체하는 것이 아니라 단계적으로 현대화를 추진하고 있는 기업에게도 매력적입니다. HPE의 “GreenLake Intelligence”의 출시는 운영 가시성과 지속가능성에 중점을 둔 최적화를 결합한, 하이브리드 IT 관리로의 광범위한 추세를 반영하고 있습니다. On-Premise 배포는 제한된 고객층을 대상으로 계속될 전망이지만, 남미의 그린 IT 소프트웨어 시장은 업데이트 속도, 감사 가능성, 데이터 관리의 균형이 잘 잡힌 아키텍처로 분명히 전환되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the south america green IT software market size was valued at USD 0.88 billion in 2025 and estimated to grow from USD 1.02 billion in 2026 to reach USD 2.37 billion by 2031, at a CAGR of 18.37% during the forecast period (2026-2031).

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and More), End User (IT and Telecom, BFSI, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Green IT Software Market Trends and Insights

Growing Carbon Reporting and ESG Compliance Requirements

Compliance remains the clearest near-term buying trigger for the South America green IT software market. Enterprises are no longer looking only for dashboards; they now need platforms that support traceable data capture, repeatable calculations, and structured reporting workflows. This change matters most for larger companies, where sustainability, finance, legal, and IT teams now need shared systems rather than disconnected spreadsheets and one-off consulting exercises. It also helps explain why carbon management and accounting software continues to act as the first purchase in many deployment journeys. Once an enterprise implements a reporting core, it often adds adjacent modules for data management, target tracking, and workflow controls in the next stage. This pattern is giving the South America green IT software market a more durable revenue base than a short project cycle would provide.

Rising Enterprise Focus on Energy-Efficient IT Operations

Energy efficiency is becoming an operating priority rather than a side benefit in the South America green IT software market. As digital workloads grow, IT teams are under pressure to monitor utilization, identify idle capacity, and improve performance without increasing power consumption. That is changing the buyer profile, because software selection is moving beyond sustainability teams and into infrastructure, operations, and platform engineering groups. The value case is also easier to defend when energy optimization can show measurable effects on operating costs, uptime planning, and asset life. This makes green IT software relevant even for firms that are not yet under direct reporting pressure. Over time, that broader utility should help the South America green IT software market deepen adoption across both compliance-led and efficiency-led accounts.

High Integration Complexity Across Legacy IT Environments

Integration difficulty is still one of the main barriers to faster adoption in the South America green IT software market. Many enterprises run old ERP, procurement, logistics, facilities, and service management systems that were never designed to feed standardized carbon or energy reporting tools. That creates long deployment cycles because buyers must map data across different formats, owners, and quality levels before the software can produce trusted outputs. It also raises the importance of implementation support, prebuilt connectors, and local partner capability during vendor selection. Global platforms can lose momentum when they underestimate the extent of operational data fragmentation across large regional organizations. For this reason, integration readiness often matters as much as product breadth in the South America green IT software market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cloud and Virtualized Infrastructure Management

- Wider Adoption of AI-Based IT Asset and Workload Optimization

- Budget Constraints Among Small and Mid-Sized Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 76.14% of South America's green IT software market share in 2025, which shows that buyers still prefer platforms they can configure and expand over time. That position reflects a practical need, as enterprises want tools that can manage emissions data, workflow rules, reporting templates, and audit trails within a single, repeatable environment. The software layer also aligns with the market's direction, as disclosure expectations and internal governance needs are changing faster than static reporting processes can keep pace. Buyers value the ability to update categories, adjust calculation logic, and add new modules without rebuilding the operating model each time requirements change. This gives software a structural advantage in the South America green IT software market because it supports scale, continuity, and internal ownership.

Services are projected to grow at a 18.43% CAGR through 2031, indicating that implementation work remains essential even in a software-led market. Enterprises still need support to connect legacy systems, clean historical records, define ownership, and set governance rules for recurring reporting cycles. Advisory and managed services also become more relevant after deployment, because many organizations need help adapting templates and controls as internal maturity improves. The service layer is likely to rise in importance as the green IT software industry moves from first purchase to ongoing optimization across broader business functions. Even so, the strongest service opportunities are likely to sit beside platform rollouts rather than replace them, which keeps software at the center of the commercial model for the South America green IT software market.

Cloud-based solutions accounted for 64.17% share of the South America green IT software market size in 2025, reflecting the appeal of scalable delivery and continuous product updates. This model works well for enterprises that want new reporting templates, workflow features, and analytics releases without lengthy internal upgrade projects. It also meets the needs of companies standardizing their technology estates and preferring subscription-based software that can be deployed across regions and functions. In the South America green IT software market, cloud deployment is also helped by the fact that many buyers begin with reporting and data management use cases before extending the platform into operations. That sequence reduces the initial burden and accelerates time-to-value.

Hybrid deployment is expected to expand at a 18.52% CAGR through 2031, underscoring that control and flexibility must often coexist. Companies handling sensitive operating data still want cloud-based analytics and reporting speed, but they may prefer to retain selected records or connectors within controlled internal environments. This structure also appeals to enterprises that are modernizing in stages rather than replacing all systems at once. HPE's GreenLake Intelligence launch reflects the wider push toward hybrid IT management that combines operational visibility with sustainability-focused optimization. On-premise deployments are likely to persist in a narrower set of accounts, yet the South America green IT software market is clearly moving toward architectures that balance update speed, auditability, and data control.

Complete Report Scope:

- By offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End User

- IT and Telecom

- BFSI

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare

- Construction and Infrastructure

- Other End-User Industries

- By Geography

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

List of Companies Covered in this Report:

- ServiceNow, Inc.

- SolarWinds Corporation

- Freshworks Inc.

- Ivanti Software, Inc.

- Flexera Software LLC

- Dynatrace, Inc.

- Progress Software Corporation

- Open Text Corporation

- New Relic, Inc.

- Workiva Inc.

- ScienceLogic, Inc.

- Schneider Electric SE

- N-able, Inc.

- IBM Corporation

- IFS AB

- BMC Software, Inc.

- NinjaOne, LLC

- Dakota Software Corporation

- EcoVadis SAS

- Salesforce Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Enterprise Focus on Energy-Efficient IT Operations

- 4.2.2 Growing Carbon Reporting and ESG Compliance Requirements

- 4.2.3 Expansion of Cloud and Virtualized Infrastructure Management

- 4.2.4 Increasing Data Center Power Optimization Initiatives

- 4.2.5 Public Sector Digital Sustainability Programs

- 4.2.6 Wider Adoption of AI-Based IT Asset and Workload Optimization

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity Across Legacy IT Environments

- 4.3.2 Budget Constraints Among Small and Mid-Sized Enterprises

- 4.3.3 Limited Standardization in Sustainability Measurement

- 4.3.4 Data Security and Data Residency Concerns

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of New Entrants

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End User

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

- 5.6 By Geography

- 5.6.1 Brazil

- 5.6.2 Argentina

- 5.6.3 Chile

- 5.6.4 Colombia

- 5.6.5 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ServiceNow, Inc.

- 6.4.2 SolarWinds Corporation

- 6.4.3 Freshworks Inc.

- 6.4.4 Ivanti Software, Inc.

- 6.4.5 Flexera Software LLC

- 6.4.6 Dynatrace, Inc.

- 6.4.7 Progress Software Corporation

- 6.4.8 Open Text Corporation

- 6.4.9 New Relic, Inc.

- 6.4.10 Workiva Inc.

- 6.4.11 ScienceLogic, Inc.

- 6.4.12 Schneider Electric SE

- 6.4.13 N-able, Inc.

- 6.4.14 IBM Corporation

- 6.4.15 IFS AB

- 6.4.16 BMC Software, Inc.

- 6.4.17 NinjaOne, LLC

- 6.4.18 Dakota Software Corporation

- 6.4.19 EcoVadis SAS

- 6.4.20 Salesforce Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment