|

시장보고서

상품코드

2073174

페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Paperless Enterprise and Digital Process Sustainability Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

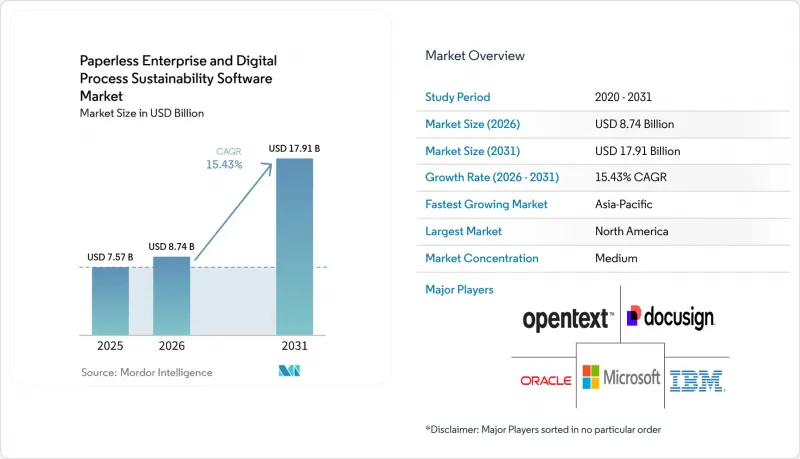

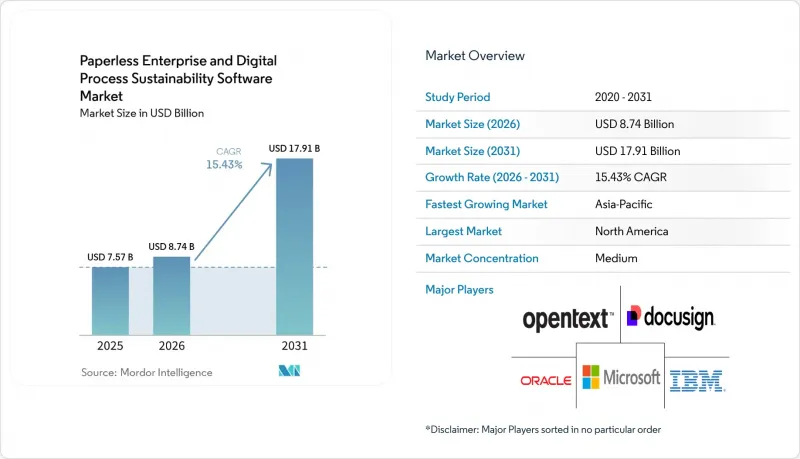

Mordor Intelligence에 의하면, 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장 규모는 2025년 75억 7,000만 달러, 2026년 87억 4,000만 달러에서 2031년까지 179억 1,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 15.43%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 모델(클라우드, On-Premise, 하이브리드), 조직 규모(대기업 및 중소기업), 용도(문서 관리 등), 최종 사용자 산업(제조업, 교육 기관 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장 동향과 인사이트

페이퍼리스 업무 방식에 따른 규정 준수 및 감사 대응에 대한 수요 증가

페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장이 확대되고 있는 이유는 규정 준수가 더 이상 선택적인 소프트웨어 업그레이드로 간주되지 않기 때문입니다. 독일은 2025년 7월 14일 GoBD 지침을 개정하여, 비즈니스 거래에서 규정 준수에 부합하는 전자 기록 관리 및 디지털 아카이브에 관한 요건을 강화했습니다. 또한, 일본도 “전자장부 관리법”에 따라 공식적인 전자 장부 관리 규정 준수를 추진하고 있으며, 이에 따라 디지털 저장 및 검색 요건이 기업의 업무 흐름 결정에 핵심 요소로 자리 잡고 있습니다. 이는 구매자가 단순히 종이 문서를 디지털 폴더로 대체하는 데 그치지 않고, 감사에 견딜 수 있는 거버넌스가 확립된 프로세스 계층을 구축하고 있음을 의미합니다. 이러한 기반이 마련되면, 동일한 시스템을 통해 재무, 조달, 업무 전반에 걸쳐 보다 신속한 검색, 보다 강력한 버전 관리, 그리고 보다 명확한 증거 추적이 가능해집니다. 법적 요건과 업무상 요건이 서로를 보완하게 됨에 따라, 이러한 조합은 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장의 회복력을 높이고 있습니다.

AI를 활용한 문서 캡처 및 워크플로우 자동화

AI를 활용한 캡처 기술은 기업 구매 담당자들이 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장을 평가하는 방식을 변화시키고 있습니다. 이러한 변화는 더 이상 광학 문자 인식(OCR)에 그치지 않습니다. 이는 구매 담당자들이 현재 거버넌스가 적용된 워크플로 환경 내에서 데이터 추출, 라우팅 및 검증이 이루어지기를 기대하고 있기 때문입니다. LF AI and Data Foundation은 2026년 6월 9일에 “DocLang 사양 워킹그룹”를 출범시켜, AI 네이티브 문서를 위한 개방형 표준 제정을 목표로 하고 있습니다. 이러한 움직임이 중요한 이유는 기업 내의 모든 이용 사례에서 AI 시스템을 위한 문서 데이터의 준비 및 처리를 보다 일관성 있게 만들기 위함입니다. 또한, 경쟁의 초점은 단순한 캡처에서 오케스트레이션, 분석, 거버넌스로 옮겨가고 있습니다. 그 결과, 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서는 AI를 독립적인 기능으로 제공하는 것이 아니라, 실제 워크플로우에 지능을 직접 통합할 수 있는 벤더가 높이 평가받고 있습니다.

레거시 시스템이 여전히 뿌리 깊게 자리 잡고 있는 기업에서 나타나는 변경 관리에 대한 저항

변경 관리는 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서 여전히 가장 뚜렷한 제약 요인 중 하나입니다. 특히, 레거시 프로세스가 깊게 뿌리내린 기업에서는 이러한 경향이 두드러집니다. 많은 기업에서는 처리 속도가 느리더라도, 직원들이 익숙해져 있는 기존의 ERP 연동 루틴 내에서 여전히 문서를 많이 사용하는 워크플로를 운영하고 있습니다. 이 때문에 전환에 많은 노력이 필요할 뿐만 아니라, 팀이 생산성이나 규정 준수에 단기적인 차질이 생길 것을 우려하는 경우가 많아 저항이 발생합니다. 이 문제는 플랫폼을 구매·도입했음에도 불구하고, 그 워크플로우 기능 중 극히 일부만 실제로 활용되고 있는 상황에서 도입 후에 종종 드러나는 경우가 많습니다. 그런 경우, 기업은 시스템이 프로세스에 주는 가치를 실감하기도 전에 시스템의 비용만 먼저 눈에 들어오게 됩니다. 따라서 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장공급업체들은 소프트웨어에 도입 지원 프로그램, 워크플로우 재설계 지원, 그리고 측정 가능한 활용 목표를 결합함으로써 꾸준히 입지를 다져가고 있습니다.

부문별 분석

2025년에는 소프트웨어가 매출의 63.47%를 차지했으며, 라이선싱 및 플랫폼 수익이 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서 계속해서 핵심적인 위치를 차지했습니다. 이러한 상황은 문서 관리, 워크플로 로직, 기록 처리 및 보고서 기능이 여전히 핵심을 이루는 소프트웨어 계층에서 비롯된다는 사실을 반영하고 있습니다. 그럼에도 불구하고 서비스 부문은 2031년까지 연평균 성장률(CAGR) 16.01%를 나타낼 것으로 예측되며, 이는 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장 전체의 성장률을 상회하는 수치입니다. 서비스 부문의 더욱 빠른 성장은 많은 구매자들이 현재 도입 지원 이상의 것을 필요로 하고 있음을 보여줍니다. 이들에게는 통합 작업, 거버넌스 설계, 워크플로우 매핑, 그리고 시스템 가동 후의 지속적인 최적화가 요구됩니다. 이 부문에서는 소프트웨어가 여전히 수익의 주축을 이루고 있지만, 도입이 점점 더 복잡해짐에 따라 서비스의 중요성이 커지고 있습니다.

AI 지원 플랫폼에서는 기존의 문서 저장소보다 더 체계적인 데이터 구조, 더 강력한 통제, 그리고 더 엄격한 프로세스 설계가 요구되기 때문에 소프트웨어 및 서비스 간의 균형이 변화하고 있습니다. 기업이 자동화를 대규모로 안정적으로 운영할 수 있게 되려면, ERP, CRM, 미들웨어, 레거시 문서 환경에 걸친 지원이 필요한 경우가 적지 않습니다. 이로 인해 초기 라이선스 판매 후에도 공급업체와 파트너에게는 지속적인 업무가 발생합니다. Newgen사는 2026년 5월에 “Enterprise Orchestration Layer”를 발표했는데, 이는 각 벤더들이 고립된 자동화에서 벗어나 기업 프로세스 전반에 걸친 지속적이고 거버넌스가 적용된 실행으로 전환하려 하고 있음을 보여줍니다. ABBYY 역시 제품 포지셔닝과 지능형 문서 처리 분야에서 지속적으로 인정받으며, 거버넌스가 반영된 문서 AI를 강조하고 있으며, 이를 통해 정확성, 감사 가능성, 운영의 일관성 등의 가치가 더욱 공고해졌습니다. 이는 ‘페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장’이라는 산업이 소프트웨어 그 자체에서 멀어진 것이 아니라, 소프트웨어를 실제로 작동하는 운영 모델로 전환하는 서비스 계층을 더욱 중시하고 있음을 의미합니다.

2025년에는 클라우드 기반 솔루션 도입이 매출의 68.91%를 차지하며, 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서 가장 큰 점유율을 기록했습니다. 또한, 2031년까지 연평균 성장률(CAGR) 17.42%를 나타낼 것으로 예측되며, 클라우드의 성장률은 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장 전체의 성장률을 확실히 상회하고 있습니다. 현재, 클라우드 도입의 근거는 인프라 비용 절감에만 그치지 않습니다. 구매자들은 클라우드 도입을 AI 지원, 신속한 업데이트, 그리고 더 확장성 있는 워크플로우 실행과 연결 짓는 경향이 점점 더 강해지고 있기 때문입니다. 이는 문서량이 많은 환경에서 추출, 라우팅, 검색, 분류가 더 이상 정적 컴퓨팅의 가정에 의존할 수 없게 되었음을 의미합니다. 또한 클라우드 플랫폼은 On-Premise형 모델보다 채널 확대, 마켓플레이스 주도형 구매, 번들형 판매를 보다 용이하게 지원합니다. 이러한 요인들로 인해, 특히 기업이 워크플로우 관리와 사용자 액세스 모두를 현대화하고자 할 때, 클라우드는 새로운 도입 결정에 있어 계속해서 최전선에 자리 잡고 있습니다.

이와 유사한 경향은 벤더들이 컨텐츠 도구를 보다 광범위한 클라우드 생태계와 연동시키고 있다는 점에서도 확인할 수 있습니다. Laserfiche는 2026년 6월 AWS 마켓플레이스에서 서비스를 시작함으로써, 많은 IT 팀에게 이미 친숙한 클라우드 채널을 통해 규제 대상 기업 구매자들이 직접 조달할 수 있는 기회를 확대했습니다. 한편, 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서는 On-Premise 및 하이브리드 모델이 여전히 중요한 위치를 차지하고 있습니다. 이는 일부 구매자가 여전히 모든 컨텐츠와 프로세스 데이터를 퍼블릭 클라우드 환경에 배치할 수 없기 때문입니다. UiPath는 2026년 5월, On-Premise 배포용 에이전트형 AI 기능을 출시했습니다. 이는 보다 강력한 주권 관리가 필요한 공공 부문 및 규제 대상 이용 사례에 명확히 초점을 맞춘 것입니다. 따라서 기술적 성과와 마찬가지로 정책 리스크가 중요한 부문에서는 하이브리드 방식이 일시적인 타협안이라기보다는 실용적인 운영 모델로 자리매김하고 있습니다. 이러한 상황에서 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서 클라우드의 점유율은 여전히 압도적이지만, 실제 구매자의 행동에 있어서는 혼합 아키텍처가 여전히 중요한 역할을 하고 있습니다.

지역별 분석

2025년, 북미는 매출의 35.43%를 차지하며, 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서 가장 규모가 큰 지역 점유율을 기록했습니다. 이러한 우위는 성숙한 기업 소프트웨어의 도입, 견고한 클라우드 인프라, 그리고 대기업에서 오랫동안 이어져 온 워크플로우 자동화에 대한 선호에서 비롯된 것입니다. 또한, 해당 지역에서는 문서 시스템을 보다 광범위한 생산성 향상, 자동화 및 분석 플랫폼과 연동하는 데 거부감이 없는 구매자층이 존재한다는 점도 긍정적인 요인으로 작용하고 있습니다. Automation Anywhere사의 보고서에 따르면, 4분기 소프트웨어 수주의 61%가 AI 기반 솔루션 도입에 기인한 것이었습니다. 이는 해당 지역의 기업 수요가 단순한 업무 자동화의 범위를 넘어 점차 확대되고 있음을 보여줍니다. 실제로 북미는 규모, 통합에 대한 의지, 클라우드 활용 숙련도가 가장 조화를 이루고 있는 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장의 한 축으로 자리 잡고 있습니다.

유럽은 여전히 2위 지역을 유지하고 있으며, 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서 유럽이 차지하는 역할은 규제에 의해 크게 좌우되고 있습니다. 지침(EU) 2026/470은 2026년 3월 18일에 발효되었으며, 해당 지속가능성 공시에 대해 통일된 디지털 데이터 형식과 XBRL 태깅을 의무화하고 있습니다. 또한, 독일은 2025년 7월에 GoBD 지침을 개정하여, 적절한 디지털 아카이브 및 전자 기록 관리의 규정 준수상 중요성을 더욱 강조했습니다. 이러한 조치들로 인해 유럽은 임의적인 현대화 예산이 아닌, 공식적인 의무에 의해 수요가 주도되는 지역으로서 가장 뚜렷한 사례가 되고 있습니다. 이러한 환경은 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장에서 강력한 현지화, 감사 관리, 워크플로우 거버넌스를 제공할 수 있는 공급업체를 뒷받침하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 16.81%를 나타낼 것으로 예측되며, 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장 규모 전망에서 가장 빠르게 성장하는 지역 부문으로 꼽히고 있습니다. 이 지역은 주요 경제권 전반에서 동시에 고조되고 있는 디지털화의 흐름, 특히 부기, 세무, 기록 관리에 관한 규제가 강화되고 있는 국가들로부터 그 혜택을 누리고 있습니다. 일본은 그 대표적인 예이며, “전자장부법”에 따라, 기업 내 디지털 자료의 보관 및 검색에 관한 규정 준수가 계속해서 중요시되고 있습니다. 남미, 중동 및 아프리카는 여전히 초기 단계에 있는 지역이지만, 데이터 현지화, 클라우드 접근성, 규제에 기반한 디지털화 프로그램이 개선됨에 따라 그 중요성이 커지고 있습니다. 이를 통해 페이퍼리스 기업 및 디지털 프로세스 지속가능성 소프트웨어 시장은 북미와 유럽 같은 성숙한 중심지를 넘어 더 광범위한 성장 기반을 확보하게 될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the paperless enterprise and digital process sustainability software market size is projected to expand from USD 7.57 billion in 2025 and USD 8.74 billion in 2026 to USD 17.91 billion by 2031, registering a CAGR of 15.43% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Document Management, and More), End-User Industry (Manufacturing, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Paperless Enterprise and Digital Process Sustainability Software Market Trends and Insights

Rising Demand for Paperless Compliance and Audit Readiness

The paperless enterprise and digital process sustainability software market is moving forward because compliance is no longer treated as a discretionary software upgrade. Germany updated its GoBD guidance on July 14, 2025, and the rule tightened expectations around compliant electronic recordkeeping and digital archiving for business transactions. Japan has also been pushing formal electronic bookkeeping compliance under the Electronic Bookkeeping Act, which keeps digital storage and retrieval requirements at the center of enterprise workflow decisions. This means buyers are not just replacing paper files with digital folders, they are building governed process layers that can stand up in an audit. Once that foundation is in place, the same systems also support faster retrieval, stronger version control, and cleaner evidence trails across finance, procurement, and operations. That combination is making the paperless enterprise and digital process sustainability software market more resilient, because legal needs and operational needs are now reinforcing each other.

AI-Enabled Document Capture and Workflow Automation

AI-enabled capture is changing how the paperless enterprise and digital process sustainability software market is evaluated by enterprise buyers. The shift is no longer limited to optical character recognition, because buyers now expect extraction, routing, and validation to happen inside a governed workflow environment. The LF AI and Data Foundation launched the DocLang Specification Working Group on June 9, 2026, with the aim of creating an open standard for AI-native documents. That move matters because it supports more consistent preparation and handling of document data for AI systems across enterprise use cases. It also shifts competitive pressure away from simple capture and toward orchestration, analytics, and governance. As a result, the paperless enterprise and digital process sustainability software market is rewarding vendors that can embed intelligence directly in production workflows instead of offering AI as an isolated feature.

Change Management Resistance in Legacy-Heavy Enterprises

Change management remains one of the clearest limits on the paperless enterprise and digital process sustainability software market, especially where legacy processes are deeply embedded. Many enterprises still run document-heavy workflows inside established ERP-linked routines that employees know well, even if those routines are slow. That creates resistance not only because migration takes effort, but also because teams often fear short-term disruption to productivity and compliance. The problem often appears after deployment, when a platform is purchased and implemented, but only a small share of its workflow capability is actually used. In those cases, the business sees the cost of the system before it sees the process value of the system. This is why vendors in the paperless enterprise and digital process sustainability software market are gaining ground when they pair software with adoption programs, workflow redesign support, and measurable usage targets.

Other drivers and restraints analyzed in the detailed report include:

- Remote and Hybrid Work Process Standardization

- Sustainability Reporting Pressure on Enterprise Process Digitization

- Data Residency and Sovereignty Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 63.47% of revenue in 2025, which kept license and platform income at the center of the paperless enterprise and digital process sustainability software market. That position reflects the fact that document control, workflow logic, records handling, and reporting functions still begin with a core software layer. Even so, services are projected to grow at a 16.01% CAGR through 2031, which is faster than the overall paperless enterprise and digital process sustainability software market. The faster expansion in services shows that many buyers now need more than installation support. They need integration work, governance design, workflow mapping, and continued optimization after the system goes live. In this segment, software remained the commercial anchor, but services became more important as the complexity of deployment increased.

The balance between software and services is changing because AI-capable platforms require cleaner data structures, stronger controls, and tighter process design than older document repositories did. Enterprises often need support across ERP, CRM, middleware, and legacy document environments before automation can run reliably at scale. That creates recurring work for vendors and partners even after the initial license has been sold. Newgen introduced its Enterprise Orchestration Layer in May 2026, which showed how vendors are trying to move from isolated automation into continuous, governed execution across enterprise processes. ABBYY also emphasized governed document AI through its product positioning and continued recognition in intelligent document processing, which reinforced the value of accuracy, auditability, and operational consistency. This means the Paperless Enterprise and Digital Process Sustainability Software Market industry is not shifting away from software, but it is placing more value on the service layer that turns software into a working operating model.

Cloud-based deployment held 68.91% of revenue in 2025, giving it the largest share of the paperless enterprise and digital process sustainability software market. It is also projected to grow at a 17.42% CAGR through 2031, which places cloud clearly ahead of the overall paperless enterprise and digital process sustainability software market size growth rate. The current case for cloud is broader than lower infrastructure cost, because buyers increasingly connect cloud adoption with AI readiness, faster updates, and more scalable workflow execution. That matters in document-heavy environments where extraction, routing, search, and classification can no longer depend on static compute assumptions. Cloud platforms also support channel expansion, marketplace-led buying, and bundle-based distribution more easily than on-premises models do. These factors are keeping cloud at the forefront of new deployment decisions, especially where enterprises want to modernize both workflow control and user access.

The same pattern is visible in how vendors are linking content tools with broader cloud ecosystems. Laserfiche launched on AWS Marketplace in June 2026, which expanded direct procurement access for regulated enterprise buyers through a cloud channel already familiar to many IT teams. At the same time, on-premises and hybrid models remain important in the paperless enterprise and digital process sustainability software market because some buyers still cannot place all content and process data in a public cloud environment. UiPath released agentic AI capabilities for on-premises deployment in May 2026, with clear attention to public sector and regulated use cases that require stronger sovereignty control. Hybrid deployment therefore remains less of a temporary compromise and more of a practical operating model in sectors where policy risk matters as much as technical performance. In that context, the paperless enterprise and digital process sustainability software market share of cloud remains dominant, but mixed architectures are still important to actual buyer behavior.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Model

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Document Management

- Workflow Automation

- E-Signature

- Electronic Forms

- Records Management

- Process Sustainability Tracking and Reporting

- By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare and Life Sciences

- Information Technology and Telecom

- Government and Public Sector

- Manufacturing

- Retail and E-Commerce

- Education

- Energy and Utilities

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 35.43% of revenue in 2025, giving it the largest regional position in the paperless enterprise and digital process sustainability software market. That lead came from mature enterprise software adoption, strong cloud infrastructure, and a long-standing preference for workflow automation in large organizations. The region also benefits from a buyer base that is comfortable linking document systems with broader productivity, automation, and analytics platforms. Automation Anywhere reported that 61% of its Q4 software bookings came from AI-driven deployments, which shows how enterprise demand in the region is moving beyond narrow task automation. In practical terms, North America remains the part of the paperless enterprise and digital process sustainability software market where scale, integration appetite, and cloud familiarity are most aligned.

Europe remained the second-largest geography, and its role in the paperless enterprise and digital process sustainability software market is shaped heavily by regulation. Directive (EU) 2026/470 entered into force on March 18, 2026, and it requires harmonized digital data formats and XBRL tagging for covered sustainability disclosures. Germany also updated its GoBD guidance in July 2025, which reinforced the compliance importance of proper digital archiving and electronic records management. Those measures make Europe the clearest example of a region where demand is often driven by formal obligations rather than optional modernization budgets. That environment supports vendors that can present strong localization, audit control, and workflow governance in the paperless enterprise and digital process sustainability software market.

Asia-Pacific is projected to grow at a 16.81% CAGR through 2031, which makes it the fastest-growing regional segment in the paperless enterprise and digital process sustainability software market size outlook. The region is benefiting from simultaneous digitization pressure across large economies, especially where bookkeeping, tax, and recordkeeping rules are tightening. Japan remains a clear example because the Electronic Bookkeeping Act continues to keep digital storage and retrieval compliance in focus for businesses. South America, the Middle East, and Africa remain earlier-stage areas, but they are becoming more relevant as data localization, cloud access, and regulatory digitization programs improve. This gives the paperless enterprise and digital process sustainability software market a wider growth base beyond its mature centers in North America and Europe.

- Microsoft Corporation

- OpenText Corporation

- Oracle Corporation

- IBM Corporation

- DocUSign, Inc.

- SAP SE

- Adobe Inc.

- Box, Inc.

- Hyland Software, Inc.

- Laserfiche

- M-Files Corporation

- DocuWare GmbH

- Nintex Global, Inc.

- Appian Corporation

- UiPath Inc.

- Automation Anywhere, Inc.

- ABBYY Development Inc.

- Newgen Software Technologies Limited

- Tungsten Automation Corporation

- Kofax, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Paperless Compliance and Audit Readiness

- 4.2.2 Remote and Hybrid Work Process Standardization

- 4.2.3 AI-Enabled Document Capture and Workflow Automation

- 4.2.4 Sustainability Reporting Pressure on Enterprise Process Digitization

- 4.2.5 Integration With Enterprise Systems and API-Led Orchestration

- 4.2.6 Underused Value From Archived Process Data and Process Mining

- 4.3 Market Restraints

- 4.3.1 Change Management Resistance in Legacy-Heavy Enterprises

- 4.3.2 Data Residency and Sovereignty Constraints

- 4.3.3 Workflow Fragmentation Across Mixed Application Stacks

- 4.3.4 Long Enterprise Sales Cycles for Regulated Buyers

- 4.4 Industry Value-Chain Analysis

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Document Management

- 5.4.2 Workflow Automation

- 5.4.3 E-Signature

- 5.4.4 Electronic Forms

- 5.4.5 Records Management

- 5.4.6 Process Sustainability Tracking and Reporting

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services, and Insurance (BFSI)

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Government and Public Sector

- 5.5.5 Manufacturing

- 5.5.6 Retail and E-Commerce

- 5.5.7 Education

- 5.5.8 Energy and Utilities

- 5.5.9 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 OpenText Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 IBM Corporation

- 6.4.5 DocuSign, Inc.

- 6.4.6 SAP SE

- 6.4.7 Adobe Inc.

- 6.4.8 Box, Inc.

- 6.4.9 Hyland Software, Inc.

- 6.4.10 Laserfiche

- 6.4.11 M-Files Corporation

- 6.4.12 DocuWare GmbH

- 6.4.13 Nintex Global, Inc.

- 6.4.14 Appian Corporation

- 6.4.15 UiPath Inc.

- 6.4.16 Automation Anywhere, Inc.

- 6.4.17 ABBYY Development Inc.

- 6.4.18 Newgen Software Technologies Limited

- 6.4.19 Tungsten Automation Corporation

- 6.4.20 Kofax, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment