|

시장보고서

상품코드

2073172

독일의 그린 IT 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

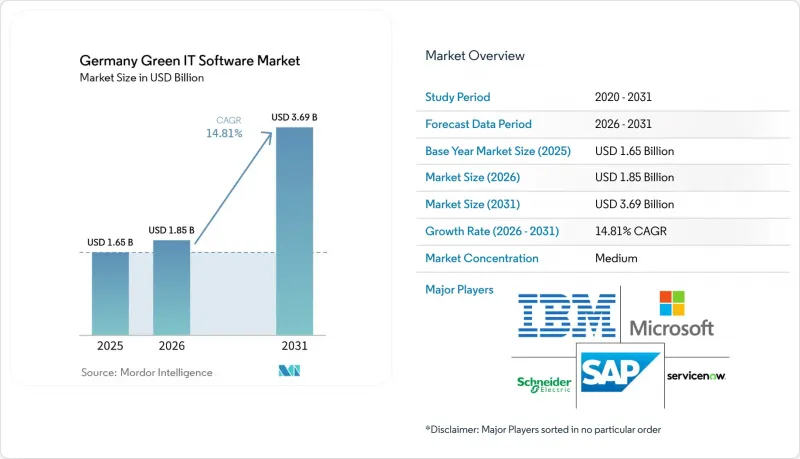

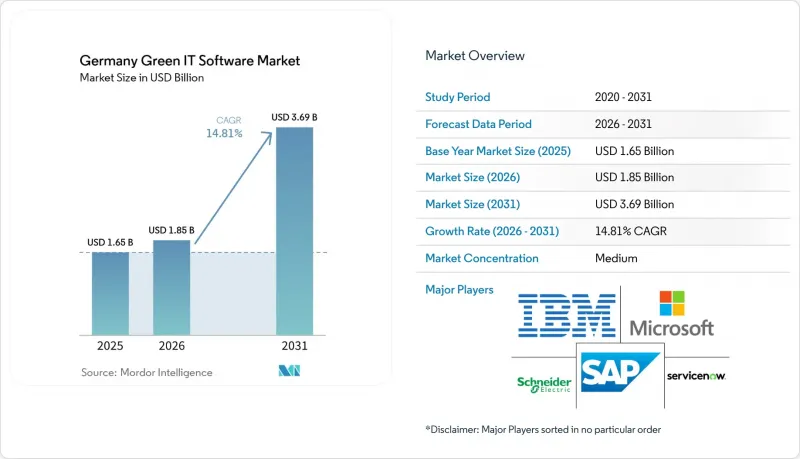

Mordor Intelligence에 의하면, 독일 그린 IT 소프트웨어 시장은 2025년 16억 5,000만 달러에서 2026년에는 18억 5,000만 달러로 확대되어 2031년까지 36억 9,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 14.81%로 성장할 전망입니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 기업 규모(대기업 및 중소기업), 솔루션 유형(탄소 관리·산정 소프트웨어, ESG 보고·컴플라이언스 소프트웨어 등), 최종 사용자(IT 및 통신 업계 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일 그린 IT 소프트웨어 시장 동향과 인사이트

기업의 지속가능성 보고에 따른 규제적 압력

독일의 CSRD(기업 지속가능성 보고 지침) 국내 법제화 과정은 2026년에 대기업을 대상으로 한 첫 번째 주요 보고 물결이 다가옴에 따라, 독일의 그린 IT 소프트웨어 시장을 보다 체계적인 구매 주기로 이끌고 있습니다. 첫 번째 대상 그룹에는 직원 수 1,000명 이상의 독일 기업 약 240곳이 포함되어 있으며, 이후 보고 의무는 단계적으로 확대되어 2028년까지 약 15,000곳에 달할 전망입니다. 초기 ESRS 프레임워크에서는 82개 공시 항목에 걸쳐 최대 1,100개의 데이터 포인트가 요구되었으나, 2025년 12월에 승인된 EU 옴니버스 I 패키지에 따라 위임 규정의 개정을 통해 해당 요건이 약 400-500개의 데이터 포인트로 축소될 전망입니다. 이러한 조정이 소프트웨어 수요를 감소시키는 것은 아닙니다. 기업들은 여전히 감사 가능한 데이터 흐름을 필요로 하며, 최종 아키텍처가 명확해짐에 따라 이에 적응할 수 있는 도구를 찾고 있기 때문입니다. 또한, 공급업체로부터 데이터를 수집함으로써 직접 보고를 하지 않는 중견 기업들도 조달 활동에 참여하는 사례가 늘고 있습니다. 이는 1차 고객들이 여전히 해당 기업들로부터 검증된 스코프 3 데이터를 확보해야 하기 때문입니다. SAP의 '2026년 지속가능성 컨트롤 타워' 업데이트에서는 기존 벤더들이 ESRS 지표의 적용 범위를 확대하고, AI를 활용한 감사 대응 기능을 도입함으로써 이러한 규정 준수 주도형 수요를 확보하려는 움직임을 보이고 있습니다.

독일 기업의 ESG 보고 부담 증가

독일의 그린 IT 소프트웨어 시장은 독일 기업들이 단일 보고 프레임워크뿐만 아니라 여러 보고 프레임워크를 동시에 지원하고 있다는 사실에 힘입어 성장하고 있습니다. 대형 금융기관들은 은행 규제에 따른 ESG 리스크 공시 의무에 직면해 있는 한편, 제조업체들은 EU 택소노미 준수 및 공급망 실사 요건에도 대응해야 합니다. 이러한 중복으로 인해 단일 목적의 도구의 유용성은 떨어지고 있으며, 구매자들은 보고, 데이터 거버넌스, 감사 준비를 단일 운영 계층에서 관리할 수 있는 플랫폼으로 눈을 돌리고 있습니다. Plan A사는 독일어 지원 워크플로우, 현지 규제 동향 추적, CSRD 및 ESRS 변경 사항에 대한 실시간 업데이트를 강점으로 입지를 다져왔으며, 2024년 이후 DACH 지역 기업 1,500곳 이상에 서비스를 제공하면서 수익성을 유지하고 있다고 밝혔습니다. SAP는 2026년 5월, 실적 최적화 에이전트를 포함한 새로운 지속가능성 AI 에이전트가 2026년 말까지 일반에 공개될 예정이며, 이를 통해 시나리오 시뮬레이션에 소요되는 시간을 1일에서 20분으로 단축할 수 있다고 발표했습니다. 보고 업무의 부담이 커지는 가운데, 구매자들은 단편적인 도구에 대한 수용도가 낮아지고 있으며, CSRD, EU 택소노미, GRI 및 은행 관련 공시 요건을 종합적으로 지원할 수 있는 통합 플랫폼에 대한 관심을 높이고 있습니다.

기존 ERP 및 ITSM 스택과의 통합에 따른 복잡성

레거시 아키텍처는 독일의 그린 IT 소프트웨어 시장 전체에서 여전히 도입 속도를 현저히 저해하는 요인으로 작용하고 있습니다. 많은 독일 기업들은 여전히 SAP ECC나 SAP IS-U, 혹은 대폭 맞춤화된 산업별 환경을 운영하고 있기 때문에 그린 IT 플랫폼은 신뢰할 수 있는 결과를 도출하기 전에 데이터 추출, 매핑, 대조와 같은 까다로운 작업에 직면하는 경우가 많습니다. 감사에 대응할 수 있는 지속가능성 보고서의 경우, 자산, 조달, 운용, 재무 데이터의 일관성이 기존 시스템 환경이 지원하는 수준보다 훨씬 더 높은 수준으로 요구되기 때문에 이 문제는 더욱 심각해지고 있습니다. 미텔슈탄트 기업들의 경우, 주요 핵심 시스템의 전환이 이미 진행 중이기 때문에 이와 병행하여 소프트웨어를 도입하기 위한 사내 자원이 제한적이라는 추가적인 부담이 발생하고 있습니다. FairEnergie GmbH가 2026년 6월에 SAP IS-U를 SAP S/4HANA Utilities를 기반으로 하는 클라우드 기반 플랫폼으로 교체하기로 결정한 것은 이 유틸리티 회사가 이미 2027년까지 이어질 근본적인 변혁 프로그램에 사내 자원을 투입하고 있음을 보여줍니다. 따라서 SAP나 ServiceNow용 기성 커넥터를 제공할 수 있는 벤더는 도입 기간을 단축하고, 구매자가 부담해야 하는 맞춤형 통합 작업의 양을 줄일 수 있으므로 경쟁 우위를 점하고 있습니다.

부문별 분석

2025년 독일의 그린 IT 소프트웨어 시장에서 소프트웨어는 시장 점유율의 76.14%를 차지하며, 이 부문에서 매출 1위를 기록한 카테고리가 되었습니다. 이 직책은 SAP와 Microsoft를 중심으로 한 IT 환경 내에서 이미 도입이 진행되고 있던 탄소 관리, ESG 보고, 탈탄소화 계획 도구를 위한 엔터프라이즈 라이선싱과 밀접한 관련이 있었습니다. 독일 기업들은 독립형 도구를 도입하기보다는 기존 플랫폼 계약을 확장하는 것을 선호하는 경향이 있습니다. 이는 공급업체 수를 줄이고, 보안 심사 기간을 단축하며, 조달을 기존에 알려진 상업적 구조 내에서 진행할 수 있기 때문입니다. 이러한 추세는 지속가능성 기능을 보다 광범위한 ERP나 클라우드 계약 내의 기능 확장으로 판매할 수 있게 해주기 때문에 기존 공급업체들이 고객 기반을 굳건히 지키는 데 도움이 되고 있습니다. 또한, 이는 독일의 그린 IT 소프트웨어 시장에서 소프트웨어 매출이 완전히 새로운 플랫폼으로의 교체 주기가 아니라, 우선 이미 도입된 시스템을 활용하는 것을 중심으로 확대되어 왔음을 의미합니다.

서비스 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 14.93%를 나타낼 것으로 예측되며, 시장 규모는 여전히 작지만 제공 서비스 구성 중 가장 빠르게 성장하는 분야가 될 전망입니다. 이러한 성장은 단순한 업무상의 현실을 반영하고 있습니다. 즉, 거버넌스 체계, 중요성 평가, 이해관계자의 워크플로우, 데이터 시정 조치 등이 소프트웨어를 중심으로 설계되어야 하는 한, 소프트웨어만으로는 감사에 대응할 수 있는 ESRS 출력을 생성할 수 없습니다. 또한, 대규모 조직의 경우 보고의 신뢰성을 확보하기 전에, 지속가능성 지표를 재무 주체, 사업 거점 및 공급업체와의 관계에 연계할 수 있도록 지원하는 것도 필요합니다. 2026년 말까지 일반에 공개될 것으로 예상되는 새로운 지속가능성 AI 에이전트는 일상적인 서비스 업무를 줄여주는 한편, 이러한 도구의 설정 및 관리를 담당하는 파트너 기업에게는 추가적인 도입 작업이 발생할 가능성이 있습니다. 또한, 데이터 구조를 ISO 14001 방식의 관리 프로세스에 부합하도록 구성한 공급업체는 제조업의 구매 담당자가 기존의 환경 관리 관행에 따라 소프트웨어 공급업체를 선정할 때 더 유리한 입지를 확보할 가능성이 높을 것입니다.

2025년 독일의 그린 IT 소프트웨어 시장에서 클라우드 기반 도입 비중은 64.17%를 차지했으나, 하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 15.02%로 성장할 것으로 전망됩니다. 클라우드를 통한 제공은 신속한 배포, 손쉬운 기능 업데이트, 그리고 CSRD 및 ESRS 요건 변경에 대한 신속한 대응을 가능하게 하므로, 여전히 매력적인 선택지로 남아 있습니다. 한편, 많은 구매자들이 기밀성이 높은 공급업체 정보, 배출량 데이터, 운영 데이터의 저장 위치에 대해 여전히 보다 강력한 관리를 필요로 하고 있기 때문에 시장이 단순한 퍼블릭 클라우드 모델로 전환되고 있는 것은 아닙니다. 조사에 따르면, 독일 기업의 73%가 하이브리드 IT 아키텍처를 채택하고 있으며, 이는 혼합 환경이 일시적인 현상이 아니라 이미 표준이 되었다는 견해를 뒷받침하고 있습니다. 데이터 주권, NIS-2 및 BSI C5 요건과 관련된 요구 사항으로 인해, 하이브리드 도입은 로컬 제어권을 완전히 포기하지 않으면서도 소프트웨어의 신속성을 추구하는 조직에게 현실적인 중간 대안이 되고 있습니다.

하이브리드 차량에 대한 수요는 중견 시장 구매자들의 행동에 의해서도 뒷받침되고 있습니다. 독일의 중소기업들은 보고, 대시보드 또는 대외 협업에는 계속해서 퍼블릭 클라우드 계층을 활용하는 한편, 지속가능성을 고려한 워크로드를 독일 또는 EU 내 호스팅 환경으로 리쇼어링하는 경향이 강해지고 있습니다. 이 방식은 스코프 3 데이터 수집에 효과적입니다. 왜냐하면 공급업체 정보에는 상업적 기밀성이 수반되는 경우가 많기 때문에 기업들은 이를 완전히 개방된 아키텍처에 노출시키기를 꺼리기 때문입니다. On-Premise 구축은 KRITIS 관련 기업, 방위 관련 공급망, 그리고 완전한 클라우드 전환이 여전히 제한을 받고 있는 규제 대상 금융 환경에서 여전히 중요한 역할을 수행하고 있습니다. 따라서 독일의 그린 IT 소프트웨어 시장에서는 단일 호스팅 모델만을 추진하는 벤더보다, 명확한 거버넌스 하에서 여러 환경 간에 데이터를 이동할 수 있는 벤더가 더 높이 평가받고 있습니다. 앞으로는 호스팅 규모뿐만 아니라 상호 운용성, 인증 지원, 원활한 통합과 같은 요소들이 도입 결정에 있어 더욱 중요해질 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the germany green IT software market is expected to grow from USD 1.65 billion in 2025 to USD 1.85 billion in 2026, and reach USD 3.69 billion by 2031, growing at a CAGR of 14.81% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, and More), and End User (IT and Telecom, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Green IT Software Market Trends and Insights

Regulatory Pressure from Corporate Sustainability Reporting

Germany's CSRD transposition path is moving the Germany green IT software market toward a more structured buying cycle, as the first major reporting wave reaches large companies in 2026. The initial group covers around 240 German enterprises with more than 1,000 employees, and the obligation then extends, in later waves, to a much broader base, reaching around 15,000 companies by 2028. The original ESRS framework carried up to 1,100 data points across 82 disclosures, and the EU Omnibus I package approved in December 2025 is reducing that requirement to an estimated 400-500 data points through a delegated revision. That adjustment is not lowering software demand, because companies still need auditable data flows and now want tools that can adapt as the final reporting architecture becomes clearer. Supplier data collection is also drawing many mid-market firms into procurement even when they do not file directly, because first-wave customers still need verified Scope 3 inputs from them. SAP's 2026 Sustainability Control Tower updates show how incumbent vendors are trying to capture this compliance-led demand by expanding ESRS metric coverage and introducing AI-based audit-readiness features.

Rising ESG Reporting Burden across German Enterprises

The German green IT software market is also supported by the fact that Germany enterprises are dealing with multiple reporting frameworks simultaneously, not just one. Large financial institutions face ESG risk disclosures under banking rules, while manufacturers must also handle EU Taxonomy alignment and supply chain due diligence requirements. That overlap is diminishing the usefulness of single-purpose tools and pushing buyers toward platforms that can manage reporting, data governance, and audit preparation from a single operating layer. Plan A built its position on German-language workflows, local regulatory tracking, and live updates for CSRD and ESRS changes, and the company said it has served more than 1,500 DACH enterprises while remaining profitable since 2024. SAP said in May 2026 that new sustainability AI agents, including a Footprint Optimization Agent, would be generally available by the end of 2026 and could reduce scenario simulation time from 1 day to 20 minutes. As reporting fatigue rises, buyers are showing less tolerance for fragmented tools and more interest in integrated platforms that can support CSRD, EU Taxonomy, GRI, and banking-related disclosure needs together.

Integration Complexity with Legacy ERP And ITSM Stacks

Legacy architecture remains a meaningful drag on deployment speed across the Germany green IT software market. Many German enterprises still run SAP ECC, SAP IS-U, or heavily customized sector-specific environments, so green IT platforms often face difficult extraction, mapping, and reconciliation work before they can produce reliable outputs. This problem is becoming sharper because audit-ready sustainability reporting requires asset, procurement, operational, and finance data to align at a much deeper level than many existing system landscapes were built to support. Mittelstand companies are facing an added burden because major core-system migrations are already underway, which reduces internal capacity for parallel software onboarding. FairEnergie GmbH's June 2026 decision to replace SAP IS-U with a cloud-based platform built on SAP S/4HANA Utilities shows how utility companies are already using internal resources on foundational change programs that run well into 2027. Vendors that can offer prebuilt connectors to SAP and ServiceNow therefore have an advantage, as they can shorten implementation timelines and reduce the amount of custom integration work buyers must fund.

Other drivers and restraints analyzed in the detailed report include:

- Energy Cost Pressure Accelerating Software-Led Optimization

- Data Center Decarbonization Programs Across Large IT Users

- Fragmented Sustainability Data Across Business Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 76.14% of the Germany green IT software market share in 2025, making it the leading revenue category in this segment. That position was tied to enterprise licensing for carbon management, ESG reporting, and decarbonization planning tools that were already being added inside SAP- and Microsoft-centered IT estates. German enterprises have often preferred to extend existing platform agreements rather than introduce standalone tools, because that reduces vendor count, shortens security reviews, and keeps procurement inside known commercial structures. This pattern has helped incumbent vendors defend their base, since sustainability functionality can be sold as a feature expansion within broader ERP or cloud contracts. It also means the German green IT software market has seen software revenue build first around installed-system leverage rather than around entirely new platform replacement cycles.

Services are projected to grow at a 14.93% CAGR from 2026 to 2031, making them the faster-moving part of the offering mix even though they remain on a smaller base. That growth reflects a simple operational reality: software alone does not create audit-ready ESRS output when governance structures, materiality assessments, stakeholder workflows, and data remediation still need to be designed around it. Large organizations also need support to map sustainability metrics to financial entities, operational sites, and supplier relationships before reporting can be trusted. New sustainability AI agents, which are expected to become generally available by the end of 2026, may reduce routine service work while creating additional implementation work for partners who configure and govern those tools. Vendors that align their data structures with ISO 14001-style management processes are also likely to stay better positioned when manufacturing buyers screen software providers against existing environmental management practices.

Cloud-based deployment held 64.17% of the Germany green IT software market in 2025, while hybrid deployment is projected to grow at a 15.02% CAGR through 2031. Cloud delivery has remained attractive because it allows faster rollout, easier feature updates, and quicker adjustment when CSRD and ESRS requirements change. At the same time, the market is not moving toward a simple public cloud model, since many buyers still need stronger control over where sensitive supplier, emissions, and operational data is stored. Surveys show that 73% of German enterprises operate hybrid IT architectures, which supports the view that mixed environments are already standard rather than transitional. Requirements tied to data sovereignty, NIS-2, and BSI C5 preferences have therefore made hybrid deployment a practical middle path for organizations that want software speed without fully giving up local control.

Hybrid demand is also being reinforced by buyer behavior in the mid-market. German SMEs are increasingly reshoring sustainability-sensitive workloads to German or EU-hosted environments while still using public cloud layers for reporting, dashboards, or external collaboration. That pattern works well for Scope 3 data collection, because supplier information often carries commercial sensitivity that companies do not want to place into a fully open architecture. On-premise deployment still keeps a role in KRITIS-related enterprises, defense-linked supply chains, and regulated financial settings where full cloud migration remains constrained. For this reason, the Germany green IT software market is rewarding vendors that can move data across several environments with clear governance rather than vendors that push one hosting model only. Over time, interoperability, certification readiness, and smooth integration are likely to matter more in deployment decisions than hosting scale alone

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management Accounting Software

- ESG Reporting Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy Resource Optimization Software

- By End User

- IT Telecom

- BFSI

- Manufacturing

- Energy Utilities

- Retail E-Commerce

- Government

- Healthcare

- Construction Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- SAP SE

- IBM Corporation

- Microsoft Corporation

- ServiceNow, Inc.

- Schneider Electric SE

- Siemens AG

- SAP SE

- Salesforce, Inc.

- Oracle Corporation

- ENGIE SA

- Enablon SA

- Wolters Kluwer N.V.

- Persefoni AI, Inc.

- Plan A

- Sweep SAS

- Envizi (IBM)

- Greenly SAS

- Quentic GmbH

- Sphera Solutions, Inc.

- Diligent Corporation

- Benchmark Gensuite, Inc.

- Dakota Software Corporation

- Microsoft Cloud for Sustainability

- EcoVadis SAS

- Salesforce Net Zero Cloud

- Sustainability Strategy and Roadmap Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ESG Reporting Burden Across German Enterprises

- 4.2.2 Energy Cost Pressure Accelerating Software-Led Optimization

- 4.2.3 Data Center Decarbonization Programs Across Large IT Users

- 4.2.4 IT Asset Lifecycle Tracking for Scope 3 Reduction

- 4.2.5 Regulatory Pressure From Corporate Sustainability Reporting

- 4.2.6 AI-Based Energy Orchestration In Hybrid Workloads

- 4.3 Market Restraints

- 4.3.1 Integration Complexity With Legacy ERP and ITSM Stacks

- 4.3.2 Budget Competition With Core Security and Cloud Programs

- 4.3.3 Fragmented Sustainability Data Across Business Units

- 4.3.4 Limited Internal Carbon Accounting Maturity In Mid-Market Firms

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of New Entrants

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management Accounting Software

- 5.4.2 ESG Reporting Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy Resource Optimization Software

- 5.5 By End User

- 5.5.1 IT Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy Utilities

- 5.5.5 Retail E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare

- 5.5.8 Construction Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 ServiceNow, Inc.

- 6.4.5 Schneider Electric SE

- 6.4.6 Siemens AG

- 6.4.7 SAP SE

- 6.4.8 Salesforce, Inc.

- 6.4.9 Oracle Corporation

- 6.4.10 ENGIE SA

- 6.4.11 Enablon SA

- 6.4.12 Wolters Kluwer N.V.

- 6.4.13 Persefoni AI, Inc.

- 6.4.14 Plan A

- 6.4.15 Sweep SAS

- 6.4.16 Envizi (IBM)

- 6.4.17 Greenly SAS

- 6.4.18 Quentic GmbH

- 6.4.19 Sphera Solutions, Inc.

- 6.4.20 Diligent Corporation

- 6.4.21 Benchmark Gensuite, Inc.

- 6.4.22 Dakota Software Corporation

- 6.4.23 Microsoft Cloud for Sustainability

- 6.4.24 EcoVadis SAS

- 6.4.25 Salesforce Net Zero Cloud

- 6.4.26 Sustainability Strategy and Roadmap Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment