|

시장보고서

상품코드

2073245

육계 사료 첨가제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Broiler Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

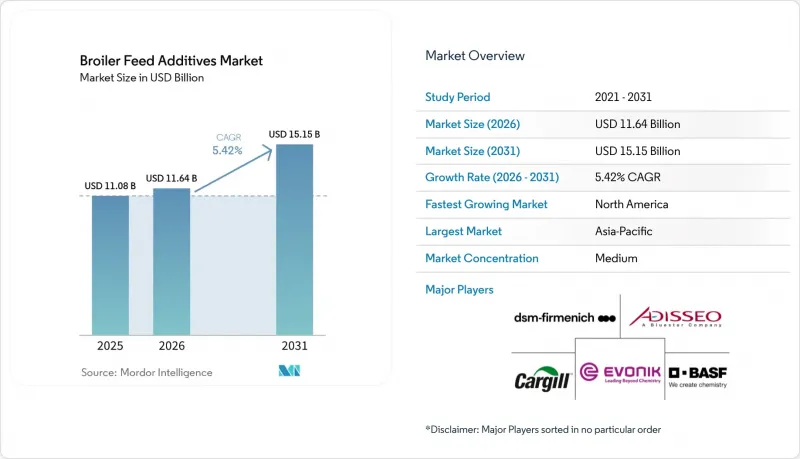

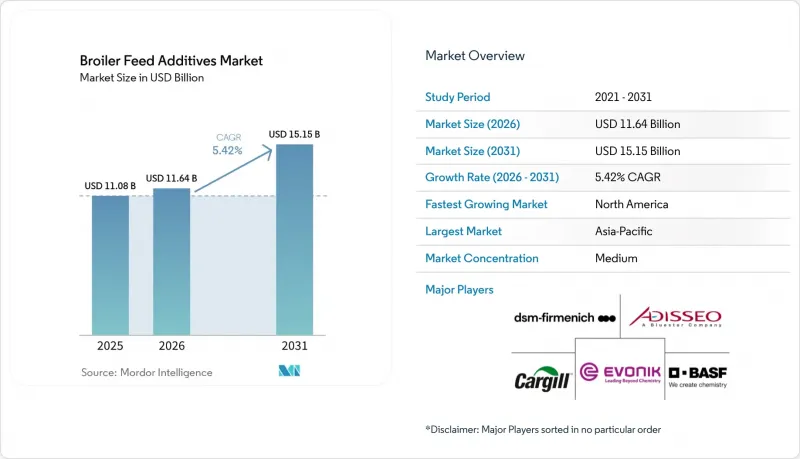

Mordor Intelligence에 의하면, 육계 사료 첨가제 시장 규모는 2025년 110억 8,000만 달러로 평가되었습니다. 2026년에는 116억 4,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.42%로 성장을 지속하여, 2031년까지 151억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 첨가제별(산미제, 항생제, 아미노산, 효소, 식물 유래 성분, 프로바이오틱스 등), 형태별(건조·액체), 육계 생산 단계별(스타터 사료, 그로워 사료, 피니셔 사료), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

세계의 육계 사료 첨가제 시장 동향 및 인사이트

항생제를 사용하지 않는 육계 사육 프로그램이 유바이오틱스 도입을 가속화

육계 사료 첨가제 시장에서는 항생제에 대한 규제가 강화됨에 따라, 더 많은 생산자들이 "항생제를 일절 사용하지 않는다" 프로그램이 지속됨에 따라 유비오틱의 도입이 가속화되고 있습니다. 미국 식품의약국(FDA)은 2026년 2월에 '업계 지침 273'을 발표하고, 식품 생산용 동물에 대해 사용 기간 제한이 설정되지 않았던 의학적으로 중요한 항생제에 대해, 의약품 신청자에게 사용 기간 제한을 추가하도록 의무화했습니다. 미국 가금류·계란 협회(USPOULTRY)가 2025년에 2024년까지의 데이터를 바탕으로 발표한 보고서는 육계 생산 과정에서 의학적으로 중요한 항생제의 사용이 지속적으로 감소하고 있음을 강조하고 있습니다. 이러한 추세는 상업적 양계 사업에서 항생제의 적정 사용이 확대되고 있음을 보여줍니다. 그 결과, 프로바이오틱스, 유기산, 식물 유래 성분, 사료용 효소 등의 대체제가 장내 환경 개선, 영양소 이용 효율 향상, 생산성 향상 측면에서 그 중요성이 커지고 있습니다. 기존 시스템과 항생제 사용 감축 시스템 모두에 대응할 수 있는 유연한 제품 라인업을 제공하는 공급업체는 시장 수요에 부응하는 데 있어 유리한 입장에 있습니다.

사료 비용 압박 하에서 사료 전환율 최적화

육계 생산에서 사료가 여전히 가장 큰 비용 요인인 만큼, 사료 전환율 개선에 대한 수요가 육계 사료 첨가제의 사용을 지속적으로 이끌고 있습니다. 에보닉 인더스트리즈(Evonik Industries AG)는 가금류 영양 프로그램이 영양소의 이용 효율과 군의 생산성 향상에 중점을 두고 있으며, 따라서 아미노산과 효소는 농장 차원의 투자 수익률(ROI)에 관한 의사결정과 밀접한 관련이 있다고 밝혔습니다. 『Frontiers in Animal Science』지에 게재된 2025년 연구에 따르면, 프로테아제, 피타제, 자일라나제의 조합을 통해 상업적 사육 조건 하에서 육계의 체중, 사료전환율, 회장 소화율 및 장 형태가 개선된 것으로 밝혀졌습니다. 이러한 연구 결과는 단일 제품의 최적화에서 벗어나, 제품군 전체에 걸쳐 측정 가능한 경제적 이익을 가져다주는 복합 첨가제 프로그램으로의 전환을 뒷받침합니다. 따라서 육계 사료 첨가제 시장은 배합률 상승뿐만 아니라, 공급업체의 가격 결정력을 높여주는 더욱 풍부한 제품 라인업으로부터도 혜택을 보고 있습니다.

농축 비타민 및 아미노산공급 기반이 조달 위험을 높입니다.

육계 사료 첨가제 시장은 몇 가지 주요 원자재가 제한된 생산 기반에 의존하고 있기 때문에 조달 위험에 노출되어 있습니다. 이는 특히 비타민과 아미노산의 경우에서 두드러지는데, 가격 변동이나 공급 차질로 인해 프리믹스의 수익성이 급격히 변동하여 배합을 재검토해야 할 가능성이 있습니다. 아디세오사는 2026년 5월 1일부터 "SmartLine"메티오닌의 전 세계 가격 인상을 발표하며, 그 이유로 원자재, 에너지, 제조 및 물류 비용의 지속적인 상승을 꼽았습니다. 생산자나 사료 배합 업체에게 있어 문제는 비용 상승뿐만 아니라, 확립된 배합 프로그램을 중단시킬 수 있는 공급 부족의 위험에도 있습니다. 이로 인해 수입 유효 성분에 크게 의존하고 있는 경우, 육계 사료 첨가제 시장에서 프리미엄 프로그램이 얼마나 신속하게 확대될 수 있는지에 실질적인 한계가 생기게 됩니다.

부문별 분석

아미노산은 가장 큰 비중을 차지하는 첨가제 유형으로, 2025년 육계 사료 첨가제 시장 점유율의 22.1%를 차지했습니다. 이러한 위상은 라이신, 메티오닌, 트레오닌, 트립토판이 상업적 육계 사육 프로그램에서 단백질 합성, 성장 성적 및 도체 품질에 있어 수행하는 기본적인 역할을 반영하고 있습니다. 메티오닌은 옥수수나 대두박을 주원료로 하는 많은 사료에서 제1제한 아미노산이기 때문에 여전히 특히 중요하며, 집약적인 육계 사육 시스템에서는 거의 보편적으로 사용되고 있습니다. 또한, 피타제, 탄수화물 분해 효소, 프로테아제 등의 효소 제품은 비용 압박 속에서 생산자가 사료 원료로부터 더 큰 가치를 창출하는 데 도움이 되기 때문에 육계 사료 첨가제 시장에서도 중요한 역할을 하고 있습니다. 비타민, 산미료, 미네랄, 항산화제 및 항생제는 지역별 규제, 사료 구성, 생산 모델에 따라 안정적인 역할을 하거나 부차적인 역할을 하고 있습니다.

프로바이오틱스는 육계 사료 첨가제 시장에서 가장 빠르게 성장하는 첨가제 부문이 될 것으로 예상되며, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.6%를 나타낼 것으로 전망됩니다. 이러한 성장은 항생제를 사용하지 않는 장 건강 유지 수단에 대한 수요가 증가하고, 상업용 가금류 영양 분야에서 균주 수준의 입지가 강화된 것을 반영하고 있습니다. 노보네시스(Novonesis)는 2025년, DSM-Firmenich AG가 보유한 Feed Enzyme Alliance의 지분을 16억 2,000만 달러(15억 유로)에 인수하는 절차를 완료함으로써, 효소 및 프로바이오틱스 응용 분야에서의 사업 확장을 강화했습니다. 또한 2026년에는 이 회사가 태국 라용에 위치한 생산 시설을 5,000만 달러에 인수하기로 합의함으로써, 아시아 수요 거점에 가까운 곳에서 공급 능력을 확대했습니다. 육계 사료 첨가제 업계에서 피토제닉, 프리바이오틱스, 효모 유래 성분, 미코톡신 해독제 및 색소는 규모는 작지만 여전히 중요한 카테고리로 자리 잡고 있습니다. 이는 대상 생산 시스템에서 장 건강, 스트레스 반응, 사료 안전성 및 제품 품질을 뒷받침하기 때문입니다.

지역별 분석

2025년, 아시아태평양은 육계 사료 첨가제 시장의 34.1%를 차지했으며, 2026년이 되어서도 여전히 가장 규모가 큰 지역 시장으로 자리매김했습니다. 올텍(Alltech)사의 『Agri-Food Outlook』에 따르면, 2025년 중국의 육계 사료 상업 생산량은 1억 100만 메트르톤에 달했으며, 인도는 2,030만 메트르톤, 인도네시아는 870만 메트르톤이었습니다. 아시아태평양의 육계 사료 첨가제 시장은 농장 내 혼합 방식에서 보다 일관성 있는 첨가제 프로그램을 채택한 상업적 사료 시스템으로의 전환이 진행되고 있는 데 힘입어 호조를 보이고 있습니다. 이러한 전환은 대규모 통합형 양계 사업 전반에 걸쳐 아미노산, 효소, 비타민, 프로바이오틱스에 대한 수요 증가를 뒷받침하고 있으며, 중규모 생산자들의 사업 체계 정비도 서서히 진행되고 있습니다. 2026년에 노보네시스사가 태국 라용에 위치한 생산 시설 인수를 합의한 점에서도, 이 지역에 대한 공급업체들의 관심이 높아지고 있음을 알 수 있습니다.

북미는 2026년부터 2031년까지 연평균 성장률(CAGR) 6.3%를 기록하며, 육계 사료 첨가제 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예측됩니다. 이 지역의 성장은 영양 프로그램의 고급화와 밀접한 관련이 있으며, 특히 통합형 생산자가 "항생제를 일절 사용하지 않는다" 또는 '항생제 사용 감축' 이러한 노력의 일환으로 사업을 전개하고 있는 경우에 특히 두드러집니다. 2026년 2월 미국 식품의약국(FDA)이 발표한 지침은 식용 동물에 대한 항생제의 적정 사용을 강화하는 데 기여하고 있으며, 이에 따라 유바이오틱스와 기능성 영양 보조제에 대한 수요는 계속해서 견조한 추세를 보일 것으로 예측됩니다. 2026년 1분기에 출범한 아처 다니엘스 미들랜드(ADM)와 올텍(Alltech)의 사료 합작 사업은 프리믹스 및 첨가제 솔루션의 지역 공급 플랫폼 규모를 확대했습니다. 육계 사료 첨가제 시장의 이 분야 성장은 사육 두수 증가보다는 마리당 첨가제 가치의 상승과 더욱 전문화된 고객 요구 사항에 기인한 것입니다.

남미의 경우, 브라질이 국내에서 막대한 가금류 생산량과 수출 체계를 모두 갖추고 있어, 육계 사료 첨가제 시장에서 계속해서 강력한 성장세를 보이고 있습니다. 브라질 동물성 단백질 협회(ABPA)에 따르면, 브라질은 2025년에 1,530만 메트르톤의 닭고기를 생산하고 530만 메트르톤(98억 달러 상당)을 수출했으며, 이는 브라질의 상업용 가금류 산업 체인의 규모를 여실히 보여주었습니다. 유럽 시장은 성숙기에 접어들었음에도 불구하고, 항생제계 성장촉진제의 장기적인 사용 금지, 동물 복지 관련 규제, 그리고 상세한 첨가물 승인 제도로 인해 기술적 요건이 여전히 높은 수준을 유지하고 있어, 혁신이 활발하게 이어지고 있습니다. 『Alltech Agri-Food Outlook』에 따르면, 2025년 독일의 육계 사료 생산량은 410만 메트르톤에 달했으며, 이는 규제가 엄격한 유럽 환경 속에서도 사료 수요의 기반이 견고함을 입증했습니다. 중동 및 아프리카는 절대적인 규모로는 작지만, 사우디아라비아, 튀르키예, 남아프리카공화국, 이집트, 나이지리아 등지에서 상업용 사료의 도입이 확대됨에 따라, 육계 사료 첨가제 시장은 낮은 수준에서 점차 성장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the broiler feed additives market size is projected to grow from USD 11.08 billion in 2025 to USD 11.64 billion in 2026 and is forecast to reach USD 15.15 billion by 2031 at 5.42% CAGR over 2026-2031.

This report is Segmented by Additive (Acidifiers, Antibiotics, Amino Acids, Enzymes, Phytogenics, Probiotics, and More), by Form (Dry and Liquid), by Broiler Production Phase (Starter Feed, Grower Feed, and Finisher Feed), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Broiler Feed Additives Market Trends and Insights

Antibiotic-Free Broiler Programs Accelerate Eubiotic Adoption

The broiler feed additives market is seeing faster adoption of eubiotics as antibiotic rules tighten and more producers maintain no-antibiotics-ever programs. The Food and Drug Administration (FDA) issued Guidance for Industry 273 in February 2026, requiring drug sponsors to add duration limits to medically important antibiotics that lacked them in food-producing animals. The report, published by the United States Poultry & Egg Association (USPOULTRY) in 2025 using data through 2024, emphasizes the ongoing decline in the use of medically important antibiotics in broiler production. This trend demonstrates advancements in antibiotic stewardship within commercial poultry operations. As a result, alternatives such as probiotics, organic acids, phytogenics, and feed enzymes are gaining significance for improving gut health, nutrient utilization, and production performance. Suppliers offering flexible portfolios that cater to both conventional and reduced-antibiotic systems are well-positioned to meet market demand.

Feed Conversion Ratio Optimization Under Feed-Cost Pressure

The use of feed additives for broilers continues to be driven by the need to improve feed conversion ratios, as feed remains the largest cost component in broiler production. Evonik Industries AG states that poultry nutrition programs center on improving nutrient use and flock performance, which keeps amino acids and enzymes closely tied to return-on-investment decisions at the farm level. A 2025 study in Frontiers in Animal Science found that a protease, phytase, and xylanase combination improved body weight, feed conversion ratio, ileal digestibility, and gut morphology in broilers under commercial conditions. This evidence supports a move away from single-product optimization toward stacked additive programs that deliver measurable economic gains across the flock. The broiler feed additives market, therefore, gains not only from higher inclusion rates but also from a richer product mix with better pricing power for suppliers.

Concentrated Vitamin and Amino-acid Supply Base Raises Sourcing Risk

The broiler feed additives market is exposed to sourcing risk because several core inputs depend on a narrow production base. This matters most for vitamins and amino acids, where price movements and supply disruptions can quickly shift premix economics and force reformulation. Adisseo announced a worldwide price increase for SmartLine methionine effective May 1, 2026, and linked it to sustained raw material, energy, manufacturing, and logistics cost increases. For producers and feed formulators, the problem is not only cost inflation but also the risk of supply gaps that interrupt established inclusion programs. This creates a practical ceiling on how quickly premium programs can scale in the broiler feed additives market when they rely heavily on imported active ingredients.

Other drivers and restraints analyzed in the detailed report include:

- Amino-Acid-Enabled Low-Protein Formulations Gain Traction

- Enteric Disease and Mycotoxin Control Raise Additive Intensity

- Regulatory Proof Burden Slows Novel Microbial and Phytogenic Launches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amino acids were the largest additive type, and accounted for 22.1% of the broiler feed additives market share in 2025. Their position reflects the basic role of lysine, methionine, threonine, and tryptophan in protein synthesis, growth performance, and carcass quality across commercial broiler feeding programs. Methionine remains especially important because it is the first-limiting amino acid in many corn and soybean meal diets, which keeps its use close to universal in intensive broiler systems. Enzymes also play a significant role in the broiler feed additives market, as phytase, carbohydrase, and protease products help producers extract greater value from feed ingredients under cost pressure. Vitamins, acidifiers, minerals, antioxidants, and antibiotics play stable or residual roles depending on local regulations, dietary structure, and production model.

Probiotics are projected to be the fastest-growing additive category in the broiler feed additives market, with a 6.6% CAGR over 2026-2031. This growth reflects stronger demand for non-antibiotic gut health tools and better strain-level positioning in commercial poultry nutrition. Novonesis completed the acquisition of DSM-Firmenich AG's share in the Feed Enzyme Alliance in 2025 for USD 1.62 billion (EUR 1.5 billion), thereby strengthening its reach across enzyme and probiotic applications. In 2026, the company also agreed to acquire a production facility in Rayong, Thailand, for USD 50 million, expanding supply capacity closer to Asian demand centers. Within the broiler feed additives industry, phytogenics, prebiotics, yeast derivatives, mycotoxin detoxifiers, and pigments remain smaller but important categories because they support gut health, stress response, feed safety, and product quality in targeted production systems.

Complete Report Scope:

- By Additive

- Acidifiers

- Lactic Acid

- Propionic Acid

- Fumaric Acid

- Other Acidifiers

- Antibiotics

- Tetracyclines

- Penicillins

- Tylosin

- Bacitracin

- Other Antibiotics

- Antioxidants

- Butylated Hydroxyanisole (BHA)

- Butylated Hydroxytoluene (BHT)

- Ethoxyquin

- Propyl Gallate

- Tocopherols

- Citric Acid

- Other Antioxidants

- Amino Acids

- Lysine

- Tryptophan

- Methionine

- Threonine

- Other Amino Acids

- Binders

- Natural Binders

- Synthetic Binders

- Enzymes

- Carbohydrases

- Phytases

- Other Enzymes

- Flavors & Sweeteners

- Flavors

- Sweeteners

- Minerals

- Macrominerals

- Microminerals

- Mycotoxin Detoxifiers

- Binders

- Biotransformers

- Phytogenics

- Herbs & Spices

- Essential Oil

- Other Phytogenics

- Pigments

- Carotenoids

- Curcumin & Spirulina

- Prebiotics

- Inulin

- Fructo Oligosaccharides

- Galacto Oligosaccharides

- Xylo Oligosaccharides

- Lactulose

- Mannan Oligosaccharides

- Other Prebiotics

- Probiotics

- Lactobacilli

- Bifidobacteria

- Streptococcus

- Pediococcus

- Enterococcus

- Other Probiotics

- Vitamins

- Vitamin A

- Vitamin B

- Vitamin C

- Vitamin E

- Other Vitamins

- Yeast

- Live Yeast

- Spent Yeast

- Torula Dried Yeast

- Selenium Yeast

- Whey Yeast

- Yeast Derivatives

- Acidifiers

- By Form

- Dry

- Liquid

- By Broiler Production Phase

- Starter Feed

- Grower Feed

- Finisher Feed

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Thailand

- Indonesia

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Turkey

- Iran

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific accounted for 34.1% of the broiler feed additives market in 2025 and remained the largest regional base entering 2026. As per Alltech's Agri-Food Outlook, China's total commercial broiler feed output reached 101.0 million metric tons in 2025, while India reached 20.3 million metric tons, and Indonesia's output was 8.7 million metric tons. The broiler feed additives market in Asia-Pacific benefits from the ongoing shift from on-farm mixing to more commercial feed systems that adopt more consistent additive programs. That shift supports greater demand for amino acids, enzymes, vitamins, and probiotics across large integrated poultry operations and is gradually formalizing mid-scale producers. Supplier interest in the region also remained visible when Novonesis agreed in 2026 to acquire a production facility in Rayong, Thailand.

North America is anticipated to be the fastest-growing region in the broiler feed additives market, with a 6.3% CAGR over 2026-2031. The region's growth is tied to premiumization in nutrition programs, especially where integrators operate under no-antibiotics-ever or reduced-antibiotic commitments. The Food and Drug Administration (FDA) guidance issued in February 2026 supported tighter antibiotic stewardship in food-producing animals, which is anticipated to keep demand favorable for eubiotics and functional nutrition tools. The Archer Daniels Midland Company and Alltech, Inc. feed joint venture launched in the first quarter of 2026 and added scale to the regional supply platform for premix and additive solutions. In this part of the broiler feed additives market, growth comes less from flock expansion and more from higher additive value per bird and more specialized customer requirements.

South America remains a strong growth geography for the broiler feed additives market, as Brazil combines large domestic poultry output with export discipline. According to the Brazilian Association of Animal Protein (ABPA), Brazil produced 15.3 million metric tons of chicken meat in 2025 and exported 5.3 million metric tons, valued at USD 9.8 billion, which shows the scale of the country's commercial poultry chain. Europe remains mature, but innovation remains active because its long-standing ban on antibiotic growth promoters, welfare rules, and detailed additive approvals keep technical requirements high. Germany's broiler feed production reached 4.1 million metric tons in 2025, according to the Alltech Agri-Food Outlook, which confirmed steady underlying feed demand in a regulated European setting. The Middle East and Africa are smaller in absolute size, but the broiler feed additives market there is expanding from a lower base as commercial feed adoption rises in countries such as Saudi Arabia, Turkey, South Africa, Egypt, and Nigeria.

- DSM-Firmenich AG

- Evonik Industries AG

- Bluestar Adisseo Company

- Cargill, Incorporated

- BASF SE

- Archer Daniels Midland Company

- Nutreco N.V. (SHV Holdings N.V.)

- Novus International, Inc. (Mitsui & Co., Ltd.)

- Kemin Industries, Inc.

- International Flavors & Fragrances Inc.

- Novonesis A/S

- Alltech, Inc.

- Elanco Animal Health Incorporated

- Phibro Animal Health Corporation

- Lesaffre

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Antibiotic-free broiler programs accelerate eubiotic adoption

- 4.2.2 Feed conversion ratio optimization under feed-cost pressure

- 4.2.3 Amino-acid-enabled low-protein formulations gain traction

- 4.2.4 Enteric disease and mycotoxin control raise additive intensity

- 4.2.5 Pelleting-stable precision additives widen commercial use

- 4.2.6 Carcass yield and footpad outcome optimization drive premium blends

- 4.3 Market Restraints

- 4.3.1 Inconsistent field response across diet matrices and flock conditions

- 4.3.2 Concentrated vitamin and amino-acid supply base raises sourcing risk

- 4.3.3 Regulatory proof burden slows novel microbial and phytogenic launches

- 4.3.4 Cost-sensitive producers retain legacy additive programs in some systems

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Additive

- 5.1.1 Acidifiers

- 5.1.1.1 Lactic Acid

- 5.1.1.2 Propionic Acid

- 5.1.1.3 Fumaric Acid

- 5.1.1.4 Other Acidifiers

- 5.1.2 Antibiotics

- 5.1.2.1 Tetracyclines

- 5.1.2.2 Penicillins

- 5.1.2.3 Tylosin

- 5.1.2.4 Bacitracin

- 5.1.2.5 Other Antibiotics

- 5.1.3 Antioxidants

- 5.1.3.1 Butylated Hydroxyanisole (BHA)

- 5.1.3.2 Butylated Hydroxytoluene (BHT)

- 5.1.3.3 Ethoxyquin

- 5.1.3.4 Propyl Gallate

- 5.1.3.5 Tocopherols

- 5.1.3.6 Citric Acid

- 5.1.3.7 Other Antioxidants

- 5.1.4 Amino Acids

- 5.1.4.1 Lysine

- 5.1.4.2 Tryptophan

- 5.1.4.3 Methionine

- 5.1.4.4 Threonine

- 5.1.4.5 Other Amino Acids

- 5.1.5 Binders

- 5.1.5.1 Natural Binders

- 5.1.5.2 Synthetic Binders

- 5.1.6 Enzymes

- 5.1.6.1 Carbohydrases

- 5.1.6.2 Phytases

- 5.1.6.3 Other Enzymes

- 5.1.7 Flavors & Sweeteners

- 5.1.7.1 Flavors

- 5.1.7.2 Sweeteners

- 5.1.8 Minerals

- 5.1.8.1 Macrominerals

- 5.1.8.2 Microminerals

- 5.1.9 Mycotoxin Detoxifiers

- 5.1.9.1 Binders

- 5.1.9.2 Biotransformers

- 5.1.10 Phytogenics

- 5.1.10.1 Herbs & Spices

- 5.1.10.2 Essential Oil

- 5.1.10.3 Other Phytogenics

- 5.1.11 Pigments

- 5.1.11.1 Carotenoids

- 5.1.11.2 Curcumin & Spirulina

- 5.1.12 Prebiotics

- 5.1.12.1 Inulin

- 5.1.12.2 Fructo Oligosaccharides

- 5.1.12.3 Galacto Oligosaccharides

- 5.1.12.4 Xylo Oligosaccharides

- 5.1.12.5 Lactulose

- 5.1.12.6 Mannan Oligosaccharides

- 5.1.12.7 Other Prebiotics

- 5.1.13 Probiotics

- 5.1.13.1 Lactobacilli

- 5.1.13.2 Bifidobacteria

- 5.1.13.3 Streptococcus

- 5.1.13.4 Pediococcus

- 5.1.13.5 Enterococcus

- 5.1.13.6 Other Probiotics

- 5.1.14 Vitamins

- 5.1.14.1 Vitamin A

- 5.1.14.2 Vitamin B

- 5.1.14.3 Vitamin C

- 5.1.14.4 Vitamin E

- 5.1.14.5 Other Vitamins

- 5.1.15 Yeast

- 5.1.15.1 Live Yeast

- 5.1.15.2 Spent Yeast

- 5.1.15.3 Torula Dried Yeast

- 5.1.15.4 Selenium Yeast

- 5.1.15.5 Whey Yeast

- 5.1.15.6 Yeast Derivatives

- 5.1.1 Acidifiers

- 5.2 By Form

- 5.2.1 Dry

- 5.2.2 Liquid

- 5.3 By Broiler Production Phase

- 5.3.1 Starter Feed

- 5.3.2 Grower Feed

- 5.3.3 Finisher Feed

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Thailand

- 5.4.4.5 Indonesia

- 5.4.4.6 Australia

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Turkey

- 5.4.5.3 Iran

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DSM-Firmenich AG

- 6.4.2 Evonik Industries AG

- 6.4.3 Bluestar Adisseo Company

- 6.4.4 Cargill, Incorporated

- 6.4.5 BASF SE

- 6.4.6 Archer Daniels Midland Company

- 6.4.7 Nutreco N.V. (SHV Holdings N.V.)

- 6.4.8 Novus International, Inc. (Mitsui & Co., Ltd.)

- 6.4.9 Kemin Industries, Inc.

- 6.4.10 International Flavors & Fragrances Inc.

- 6.4.11 Novonesis A/S

- 6.4.12 Alltech, Inc.

- 6.4.13 Elanco Animal Health Incorporated

- 6.4.14 Phibro Animal Health Corporation

- 6.4.15 Lesaffre