|

시장보고서

상품코드

2073280

인력 인텔리전스 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Workforce Intelligence Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

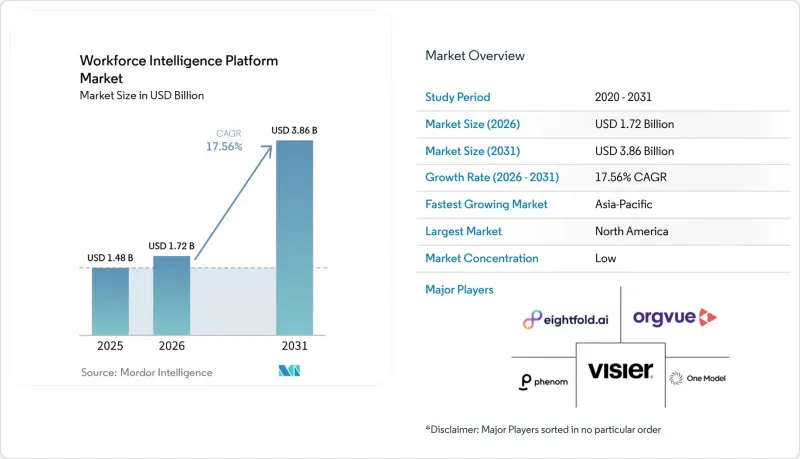

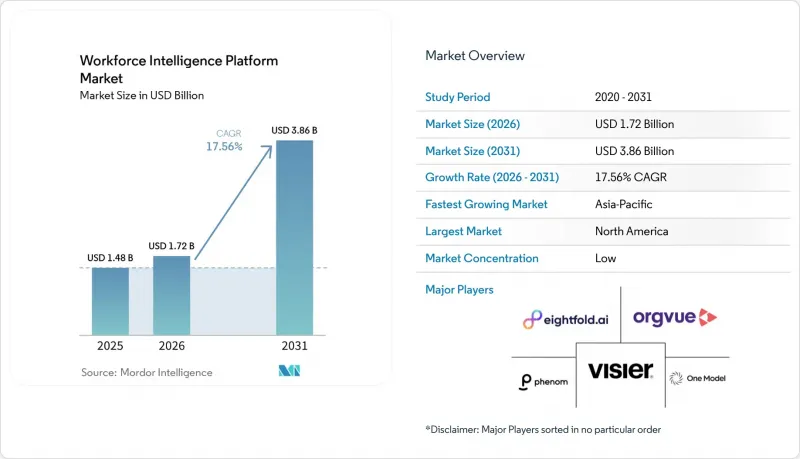

Mordor Intelligence에 의하면, 인력 인텔리전스 플랫폼 시장은 2025년에 14억 8,000만 달러로 평가되었습니다. 2026년 17억 2,000만 달러에서 2031년까지 38억 6,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 17.56%를 나타낼 전망입니다.

본 보고서는 도입 모델(클라우드 및 On-Premise), 기능(인력 분석·보고, 인재 이동성·기술 인텔리전스, 인력 계획·예측 등), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(IT 및 통신, BFSI 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 인력 인텔리전스 플랫폼 시장 동향 및 인사이트

핵심 인사 워크플로우에서 AI를 활용한 예측형 인재 계획

인력 인텔리전스 플랫폼 시장은 단순히 과거 실적을 요약하는 데 그치지 않고, 미래를 내다보는 계획 도구를 원하는 구매자들 수요에 따라 그 양상이 변화하고 있습니다. Betterworks가 2026년 4월에 실시한 ‘탤런트 인텔리전스 조사"에 따르면, 진정한 예측형 인사 체제로 운영되는 조직은 고작 16%에 불과하며, 대시보드 기반 보고 기능을 뛰어넘는 솔루션을 제공할 수 있는 벤더에게는 큰 비즈니스 기회가 되고 있습니다. 이 조사에서 응답자의 36%는 업무 데이터나 성과 데이터를 바탕으로 AI를 활용해 역량을 추론하는 기능을, 인재 관련 의사결정을 개선할 가능성이 가장 높은 단일 기능으로 꼽았으며, 다른 선택지보다 높은 순위에 배치했습니다. SAP SuccessFactors의 2026년 상반기 릴리스에서도 스킬 거버넌스가 핵심 데이터 분야로 자리매김하고 있으며, 이는 예측 기능이 선택 사항인 프리미엄 애드온이 아니라 플랫폼에서 기본적으로 기대되는 기능으로 자리 잡고 있음을 보여줍니다. 인력 인텔리전스 플랫폼 시장에서 이는 독립 벤더들에게 기준을 높이는 요인이 될 것입니다. 왜냐하면, 스위트 벤더들이 네이티브 기능을 확충해 나가는 가운데, 가격 경쟁력을 유지하기 위해서는 더 높은 모델 정확도, 더 광범위한 통합, 그리고 더 우수한 외부 데이터의 확충이 필요하기 때문입니다.

기술 기반 조직 프로그램에는 동적인 기술 그래프가 필요합니다.

인력 인텔리전스 플랫폼 시장은 정적인 직무 구조에서 기술 기반의 운영 모델로의 광범위한 전환으로 인한 혜택도 누리고 있습니다. “Skills-base"의 조사에 따르면, 검증된 역량 데이터를 대규모로 활용하고 있는 고성능 조직은 역량 라이브러리의 94.4%를 하드 스킬로 구성하고 있으며, 직원 평가의 커버리지 중앙값이 82%에 달할 전망입니다. 이는 기계의 지원을 통한 추론 없이는 스킬 데이터를 최신 상태로 유지하는 것이 얼마나 어려운지를 보여줍니다. 분산된 팀, 로컬 시스템, 변화하는 역할 구조 전반에 걸쳐 직원의 역량을 추론·업데이트·연동할 수 있는 플랫폼이 기업에 요구되고 있기 때문에 인력 인텔리전스 플랫폼 시장은 이러한 수요 격차로부터 혜택을 보고 있습니다. 또한 유럽에서는 인적 자본 보고와 관련된 공시 및 거버넌스 과정에서 체계적인 인재 개발에 관한 증거의 중요성이 점점 더 커지고 있어, 비즈니스 사례도 확대되고 있습니다.

직원 데이터의 개인정보 보호 및 알고리즘 편향성에 대한 면밀한 검토

인력 인텔리전스 플랫폼 시장은 직원 모니터링, 자동화된 의사 결정, 모델의 설명 가능성에 대한 엄격한 심사가 이루어지는 가운데 조달 과정에서 마찰을 겪고 있습니다. 2024년 8월부터 시행되고 있는 EU AI법은 직장 환경에서 생체 인식 데이터를 바탕으로 감정을 추론하는 AI 시스템을 금지하고 있으며, 금지 행위를 위반할 경우 최대 3,500만 유로(3,960만 달러) 또는 전 세계 연간 매출액의 7%에 해당하는 벌금이 부과됩니다. 해당 지침에서는 행동 모니터링 및 완전 자동화된 인사 결정과 관련된 인력 인텔리전스 시스템이 고위험 분류에 해당할 가능성이 있으며, 이로 인해 문서화, 인적 감독 및 직원 대상 투명성 관련 요건이 더욱 엄격해진다고 설명하고 있습니다. 편향에 대한 우려도 또 다른 과제로 대두되고 있습니다. 이는 과거 인사 기록을 바탕으로 학습된 모델이 급여, 승진, 업무 배분에서 오랫동안 지속되어 온 불평등을 재현할 가능성이 있기 때문입니다. 따라서 유럽 및 영국의 인력 인텔리전스 플랫폼 시장에서는 입증 책임이 더욱 무겁게 다가오고 있으며, 이러한 부담이 아키텍처 선택, 판매 주기 및 거버넌스 관리에 대한 구매자의 요구에 점점 더 큰 영향을 미치고 있습니다.

부문별 분석

2025년, 인력 인텔리전스 플랫폼 시장의 69.84%를 클라우드가 차지했으며, 이는 구매자들이 AI 기능, 커넥터, 규정 준수 업데이트에 대한 공통 릴리스 주기를 지원하는 멀티테넌트형 제공 모델을 선호하고 있음을 보여줍니다. 인력 인텔리전스 플랫폼 시장이 클라우드로 기울고 있는 배경에는 벤더가 고객의 On-Premise 업그레이드 프로젝트를 기다릴 필요 없이 이미 도입된 시스템 전체에서 모델을 업데이트할 수 있다는 점이 있습니다. 기업 환경에서 개인정보 보호 요건, 기술 분류 체계, 통합 기준이 끊임없이 변화하고 있는 가운데, 이러한 출시 속도는 점점 더 중요해지고 있습니다. 또한, 클라우드는 가장 빠르게 성장하고 있는 도입 모델이기도 하며, 클라우드 기반 인력 인텔리전스 플랫폼 시장 규모는 2031년까지 연평균 성장률(CAGR) 17.92%로 확대될 것으로 전망됩니다. 이러한 성장은 중소기업 수요에 더해, 아시아태평양의 “클라우드 우선"를 내세우는 조직들에 의해 뒷받침되고 있으며, 이러한 조직들은 기존의 On-Premise형 아키텍처를 도입 주기에 그대로 이어받지 않고, 이러한 플랫폼을 채택하고 있습니다.

On-Premise 배포는 인력 인텔리전스 플랫폼 업계에서 특히 정부 기관, 금융 서비스 기관 및 엄격한 주권 및 보안 규정을 준수하며 업무를 수행하는 대기업에서 여전히 명확한 역할을 담당하고 있습니다. 이러한 고객들은 미가공 인사 기록, 급여 파일 및 접근 제어 요구 사항이 여전히 기존의 내부 시스템에 연계되어 있기 때문에 완전한 전환을 미루는 경우가 많습니다. 각 벤더사는 기밀 데이터를 로컬 환경에 보관하면서 분석 및 AI 레이어를 클라우드로 이전해 확장성과 모델 성능을 확보하는 하이브리드 접근 방식을 통해 이러한 격차를 해소하고 있습니다. 따라서 ISO 27001 및 SOC 2 Type II 인증은 클라우드 공급업체에게 단순한 선택 사항이 아니라 표준적인 조달 기준이 되었습니다. 인력 인텔리전스 플랫폼 시장에서 도입 방식의 선택은 호스팅 선호도와 마찬가지로 거버넌스 체계 및 통합 준비 현황을 나타내는 지표가 되고 있습니다.

2025년, 인력 분석 및 보고 기능은 인력 인텔리전스 플랫폼 시장 점유율의 29.42%를 차지했습니다. 이는 복잡한 인사 환경 속에서 직원 수 대시보드, 이직률 추적, 그리고 관리자를 위한 셀프 서비스형 분석에 대한 수요가 여전히 높다는 점을 반영하고 있습니다. 이 부문은 기업들이 계획, 모빌리티, 성과 각 계층을 추가하기 전에 가장 먼저 도입하는 범주가 되는 경우가 많기 때문에 인력 인텔리전스 플랫폼 시장의 핵심으로 자리매김하고 있습니다. 많은 조직에서는 여전히 분산된 시스템 전반에 걸친 가시성 향상이 요구되고 있기 때문에 구매자가 향후 기능 확장을 계획하고 있는 경우에도 보고서 작성 도구는 여전히 실용적인 도입의 출발점으로 남아 있습니다. 한편, 인재 이동성 및 기술 인텔리전스는 2031년까지 연평균 성장률(CAGR) 20.18%로 확대될 것으로 예상되며, 인력 인텔리전스 플랫폼 시장에서 가장 빠르게 성장하는 기능 부문이 될 전망입니다. 이러한 급속한 성장은 고용주들이 과거 보고서에만 의존하는 것이 아니라, 직원의 역량을 실시간으로 파악하고 이를 바탕으로 조치를 취할 수 있는 도구를 점점 더 많이 찾고 있음을 보여줍니다.

Skills-base의 보고서에 따르면, 검증된 기술 데이터를 대규모로 적극적으로 활용하고 있는 조직에서는 직책당 평균 89개의 기술을 유지하고 있으며, 직원 평가의 커버리지 비율은 중앙값 기준 82%를 달성하고 있고, 기술 데이터의 갱신 주기는 중앙값 기준 6개월인 것으로 나타났습니다. 이러한 벤치마크는 인력 인텔리전스 플랫폼 업계가 정적인 프로파일 데이터베이스에서 보다 정교한 스킬 엔진으로 전환하고 있는 이유를 설명하는 데 도움이 됩니다. 또한, 고용주가 동일한 인력 모델 내에서 직원 수와 AI 에이전트를 모두 포함하는 시나리오를 필요로 하기 때문에 인력 계획 및 예측의 중요성도 커지고 있습니다. Eightfold AI가 2026년 5월에 출시한 ‘Workforce Readiness"는 CHRO(최고인사책임자)에게 직원들의 AI 도구 도입 현황과 생산성을 실시간으로 시각화해 주는 것으로, 각 벤더사가 기능성을 새로운 인텔리전스 분야로 확대하고 있음을 보여줍니다.

지역별 분석

2025년, 북미는 전 세계 인력 인텔리전스 플랫폼 시장 점유율의 40.74%를 차지하며, 지역별로는 가장 큰 기여도를 보였습니다. 이 지역에서 해당 시장이 가장 활발한 이유는 대기업들이 이미 성숙한 HR 기술 환경을 운영하고 있으며, 인재 관련 의사결정과 재무 실적을 연계하기 위한 관행이 더욱 확립되어 있기 때문입니다. 미국은 여전히 주요 수요 거점이며, 인적 자본 자원과 관련된 상장 기업의 공시 요건과, 인력 기술에 대한 투자에 대한 CHRO와 CFO의 강력한 공동 지원에 힘입고 있습니다. 캐나다는 두 번째 수요 거점으로 자리매김하고 있으며, 특히 밴쿠버는 Visier와 같은 기업들을 통해 인재 분석 분야의 혁신을 이끄는 중요한 거점으로 두각을 나타내고 있습니다. 인력 인텔리전스 플랫폼 시장에서 구매자의 성숙도, 공급업체의 진출 현황, 그리고 대규모 계약 범위라는 요소들이 복합적으로 작용하여 북미의 주도적 지위를 지속적으로 뒷받침하고 있습니다.

유럽에서는 인력 인텔리전스 플랫폼 시장에서 규정 준수를 더욱 중시하는 모델이 채택되고 있습니다. “기업 지속가능성 보고 지침(CSRD)"에 따라 직원 구성, 역량 개발, 임금 격차에 관한 체계적인 정보 공개의 필요성이 높아지고 있으며, 이러한 데이터 흐름을 공식적으로 관리할 수 있는 플랫폼에 대한 투자가 촉진되고 있습니다. 한편, 독일, 프랑스, 벨기에, 네덜란드에서는 근로자 대표 위원회와의 협의 의무로 인해 시스템 가동 전에 근로자 대표의 심사가 필요한 경우가 있어, 도입이 지연될 가능성이 있습니다. 에버셰즈 서덜랜드사의 2026년 고용 전망도 이 지역의 구매자들이 여전히 신중한 태도를 유지하고 있는 이유를 보여줍니다. 직장 환경에서 사용되는 AI 시스템은 EU AI법에 따라 고위험 의무가 부과될 가능성이 있기 때문입니다. 북유럽 국가들과 영국은 유럽 대륙의 일부 지역에 비해 기업의 인사 분석 실천이 더욱 성숙해 있으며, 데이터 거버넌스 프로세스도 확립되어 있어 비교적 변화가 빠른 하위 시장으로 자리매김하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 19.64%를 나타낼 것으로 예측되며, 인력 인텔리전스 플랫폼 시장에서 가장 빠르게 성장하는 지역으로 꼽히고 있습니다. 이러한 성장은 정부 주도의 AI 프로그램, 세계 역량 센터의 확대, 그리고 많은 조직이 기존의 HR 시스템을 계속 사용하는 대신 클라우드 기반 아키텍처로 직접 전환하고 있다는 사실에 힘입은 것입니다. 인도는 IT 서비스 및 금융 서비스 분야에서 생성형 AI가 이미 인력 계획, 이직 예측, 역량 추론에 활용되고 있는 급성장 시장으로서 두각을 나타내고 있습니다. 일본은 여전히 주요 지역 SaaS 시장인 반면, 호주의와 한국은 디지털화와 규정 준수 수요가 높은 성숙한 2차 시장으로 기능하고 있습니다. WTW는 또한 AI가 아시아태평양의 인사팀이 직무, 등급, 역량에 관한 통일된 ‘진실의 원천(single source of truth)"를 구축하는 데 도움을 주고 있으며, 이것이 동일한 운영 모델 내에서 급여 거버넌스와 사내 인사 이동 모두를 뒷받침하고 있다고 보고하고 있습니다. 남미, 중동 및 아프리카는 인력 인텔리전스 플랫폼 시장에서 여전히 초기 단계에 있는 지역이며, 해당 플랫폼의 도입은 다국적 기업의 자회사, 대형 금융기관, 정부 산하 고용주들에게 집중되어 있습니다. 브라질과 남아프리카공화국이 지역 내 수요를 뒷받침하고 있는 반면, 사우디아라비아와 아랍에미리트(UAE)는 노동력 현지화 의무로 인해 정책 목표에 따른 노동력 구성을 감사 가능한 방식으로 추적해야 하므로 특히 주목받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the workforce intelligence platform market was valued at USD 1.48 billion in 2025 and estimated to grow from USD 1.72 billion in 2026 to reach USD 3.86 billion by 2031, at a CAGR of 17.56% during the forecast period (2026-2031).

This report is Segmented by Deployment Model (Cloud, and On-Premises), Functionality (Workforce Analytics and Reporting, Talent Mobility and Skills Intelligence, Workforce Planning and Forecasting, and More), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Workforce Intelligence Platform Market Trends and Insights

AI-Enabled Predictive Workforce Planning in Core HR Workflows

The workforce intelligence platform market is being reshaped by buyer demand for planning tools that look ahead instead of only summarizing what has already happened. Betterworks' April 2026 Talent Intelligence Survey finds that only 16% of organizations operate with a truly predictive HR posture, which leaves a large opening for vendors that can move customers beyond dashboard-based reporting. The same survey shows that 36% of respondents identified AI-driven skills inference from work and performance data as the single capability most likely to improve workforce decision-making, ranking it ahead of other options. SAP SuccessFactors' 1H 2026 release also treats skills governance as a core data discipline, which indicates that predictive capabilities are becoming expected platform features rather than optional premium add-ons. For the workforce intelligence platform market, this raises the standard for standalone vendors, because they now need stronger model accuracy, broader integrations, and better external data enrichment to defend pricing as suite vendors expand their native functionality.

Skills-Based Organization Programs Need Dynamic Skills Graphs

The workforce intelligence platform market is also benefiting from the wider move away from static job architecture and toward skills-based operating models. Skills-base finds that high-functioning organizations using verified skills data at scale maintain skill libraries that are 94.4% hard skills and reach a median 82% workforce assessment coverage, which shows how difficult it is to keep skills data current without machine-assisted inference. The workforce intelligence platform market is gaining from this gap because enterprises need platforms that can infer, refresh, and connect employee capabilities across distributed teams, local systems, and changing role structures. The business case is also growing in Europe, where evidence on structured workforce development is becoming more relevant for disclosure and governance processes tied to human capital reporting.

Employee Data Privacy and Algorithmic Bias Scrutiny

The workforce intelligence platform market faces procurement friction where employee monitoring, automated decision-making, and model explainability sit under close review. The EU AI Act, in force since August 2024, prohibits AI systems that infer emotions from biometric data in workplace settings, with penalties reaching EUR 35 million (USD 39.6 million) or 7% of annual global turnover for prohibited-practice violations. The same guidance explains that workforce intelligence systems tied to behavioral monitoring or fully automated personnel decisions can fall under high-risk classification, which brings stricter requirements for documentation, human oversight, and employee transparency. Bias concerns add another layer because models trained on historical HR records can reproduce long-standing inequality in pay, promotion, and work allocation. The workforce intelligence platform market, therefore, has a higher burden of proof in Europe and the UK, and that burden is increasingly affecting architecture choices, sales cycles, and buyer demand for governance controls.

Other drivers and restraints analyzed in the detailed report include:

- Internal Talent Marketplaces Redirect Spend from External Hiring

- Rising Strategic Workforce Planning Needs Amid Labor and AI Disruption

- Fragmented HR, Payroll, and Collaboration Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud accounted for 69.84% of the workforce intelligence platform market in 2025, underscoring that buyers are prioritizing multi-tenant delivery models that support a common release cycle for AI features, connectors, and compliance updates. The workforce intelligence platform market has leaned toward the cloud because vendors can refresh models across the installed base without waiting for customers to run local upgrade projects. That release speed matters more as privacy requirements, skills taxonomies, and integration standards keep changing across enterprise environments. Cloud is also the fastest-growing deployment model, with the workforce intelligence platform market size for cloud projected to rise at a 17.92% CAGR through 2031. This growth is being supported by SME demand and by cloud-first organizations in Asia-Pacific that are adopting these platforms without carrying legacy on-premises architecture into the implementation cycle.

On-premises deployments still hold a defined role in the workforce intelligence platform industry, especially in government bodies, financial services institutions, and large enterprises working under strict sovereignty or security rules. These customers often delay full migration because raw HR records, payroll files, and access control requirements remain tied to older internal systems. Vendors are addressing that gap with hybrid approaches that keep sensitive data in local environments while shifting analytics and AI layers into the cloud for scale and model performance. ISO 27001 and SOC 2 Type II certifications have therefore become standard procurement signals rather than optional credentials for cloud vendors. In the workforce intelligence platform market, deployment choice now says as much about governance posture and integration readiness as it does about hosting preference.

Workforce analytics and reporting held 29.42% of the workforce intelligence platform market share in 2025, which reflects the continued demand for headcount dashboards, attrition tracking, and manager self-service analytics across complex HR environments. This segment remains the anchor of the workforce intelligence platform market because it is often the first category that enterprises adopt before adding planning, mobility, and performance layers. Many organizations still need better visibility across fragmented systems, so reporting tools remain a practical entry point even when buyers plan to expand functionality later. At the same time, talent mobility and skills intelligence is projected to advance at a 20.18% CAGR through 2031, making it the fastest-growing functional segment in the workforce intelligence platform market. That faster growth shows that employers increasingly want tools that can map and act on workforce capability in real time instead of relying only on historical reporting.

Skills-base reports that organizations actively using verified skills data at scale maintain an average of 89 skills per role, achieve a median 82% workforce assessment coverage, and refresh skills data on a median 6-month cycle. Those benchmarks help explain why the workforce intelligence platform industry is moving toward richer skills engines and away from static profile databases. Workforce planning and forecasting is also gaining weight because employers need scenarios that include both headcount and AI agents inside the same workforce model. Eightfold AI's May 2026 launch of Workforce Readiness, which gives CHROs real-time visibility into employee AI tool adoption and productivity, shows how vendors are expanding functionality into new intelligence categories.

Complete Report Scope:

- By Deployment Model

- Cloud

- On-premises

- By Functionality

- Workforce Analytics and Reporting

- Talent Mobility and Skills Intelligence

- Workforce Planning and Forecasting

- Employee Experience and Performance Intelligence

- Other Functionality Types

- By Organization Size

- Large Enterprises

- SMEs

- By End-User Industry

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-commerce

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 40.74% of global workforce intelligence platform market share in 2025, making it the largest regional contributor. The workforce intelligence platform market is strongest in this region because large enterprises already operate mature HR technology estates and have more established practices for linking workforce decisions with financial performance. The United States remains the main demand center, supported by public company disclosure expectations around human capital resources and by stronger CHRO-CFO co-sponsorship of workforce technology spending. Canada adds a secondary center of demand, with Vancouver standing out as an important base for people analytics innovation through companies such as Visier. In the workforce intelligence platform market, that combination of buyer maturity, vendor presence, and larger contract scope continues to support North America's leading position.

Europe operates under a more compliance-driven model in the workforce intelligence platform market. The Corporate Sustainability Reporting Directive has increased the need for structured disclosure on workforce composition, skills development, and pay equity, which supports investment in platforms that can formalize those data flows. At the same time, works council consultation obligations in Germany, France, Belgium, and the Netherlands can slow deployments because employee representatives may need to review systems before activation. Eversheds Sutherland's 2026 employment guidance also shows why buyers in this region remain cautious, since AI systems used in workplace settings can trigger high-risk obligations under the EU AI Act. The Nordics and the UK remain relatively faster-moving sub-markets because enterprise HR analytics practices are more mature and data governance processes are more established than in some parts of continental Europe.

Asia-Pacific is projected to expand at a 19.64% CAGR through 2031, which makes it the fastest-growing region in the workforce intelligence platform market. Growth is being supported by government-backed AI programs, the expansion of Global Capability Centers, and the fact that many organizations are moving directly into cloud-led architectures instead of carrying older HR stacks forward. India stands out as a high-velocity market where generative AI is already being applied to workforce planning, attrition prediction, and skills inference in IT services and financial services environments. Japan remains a major regional SaaS market, while Australia and South Korea function as mature secondary markets with strong digitization and compliance needs. WTW also reports that AI is helping Asia-Pacific HR teams build a unified source of truth for jobs, levels, and skills, which supports both pay governance and internal mobility within the same operating model. South America, the Middle East, and Africa remain earlier-stage regions for the workforce intelligence platform market, with adoption concentrated in multinational subsidiaries, large financial institutions, and government-linked employers. Brazil and South Africa anchor regional demand, while Saudi Arabia and the UAE stand out because workforce nationalization mandates require auditable tracking of workforce composition against policy targets.

- Visier, Inc.

- Eightfold AI, Inc.

- Phenom People, Inc.

- One Model, Inc.

- OrgVue Limited

- Gloat Ltd.

- Crunchr B.V.

- TechWolf NV

- 365Talents SAS

- Beamery Inc.

- SeekOut, Inc.

- Lightcast, Inc.

- Reejig Pty Ltd.

- Retrain.ai Ltd.

- Humanyze, Inc.

- ChartHop, Inc.

- Lattice, Inc.

- Culture Amp Pty Ltd

- Syndio Solutions, Inc.

- Perceptyx, Inc.

- Betterworks Systems, Inc.

- Aquire, Inc.

- Draup Inc.

- iMocha Technologies Private Limited

- ProFinda Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Enabled Predictive Workforce Planning Enters Core HR Workflows

- 4.2.2 Skills-Based Organization Programs Need Dynamic Skills Graphs

- 4.2.3 Internal Talent Marketplaces Redirect Spend From External Hiring

- 4.2.4 Rising Strategic Workforce Planning Needs Amid Labor and AI Disruption

- 4.2.5 CHRO-CFO Pressure for Workforce ROI and Capacity Visibility

- 4.2.6 HR-Finance-Payroll Integration Matures Into a Buying Trigger

- 4.3 Market Restraints

- 4.3.1 Employee Data Privacy and Algorithmic Bias Scrutiny

- 4.3.2 Fragmented HR, Payroll, and Collaboration Data

- 4.3.3 EU AI Act and Works Council Review Delays

- 4.3.4 Vendor Service Pullback Extends Time to Value

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premises

- 5.2 By Functionality

- 5.2.1 Workforce Analytics and Reporting

- 5.2.2 Talent Mobility and Skills Intelligence

- 5.2.3 Workforce Planning and Forecasting

- 5.2.4 Employee Experience and Performance Intelligence

- 5.2.5 Other Functionality Types

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 SMEs

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Visier, Inc.

- 6.4.2 Eightfold AI, Inc.

- 6.4.3 Phenom People, Inc.

- 6.4.4 One Model, Inc.

- 6.4.5 OrgVue Limited

- 6.4.6 Gloat Ltd.

- 6.4.7 Crunchr B.V.

- 6.4.8 TechWolf NV

- 6.4.9 365Talents SAS

- 6.4.10 Beamery Inc.

- 6.4.11 SeekOut, Inc.

- 6.4.12 Lightcast, Inc.

- 6.4.13 Reejig Pty Ltd.

- 6.4.14 Retrain.ai Ltd.

- 6.4.15 Humanyze, Inc.

- 6.4.16 ChartHop, Inc.

- 6.4.17 Lattice, Inc.

- 6.4.18 Culture Amp Pty Ltd

- 6.4.19 Syndio Solutions, Inc.

- 6.4.20 Perceptyx, Inc.

- 6.4.21 Betterworks Systems, Inc.

- 6.4.22 Aquire, Inc.

- 6.4.23 Draup Inc.

- 6.4.24 iMocha Technologies Private Limited

- 6.4.25 ProFinda Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment