|

시장보고서

상품코드

2073306

승계 계획 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Succession Planning Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

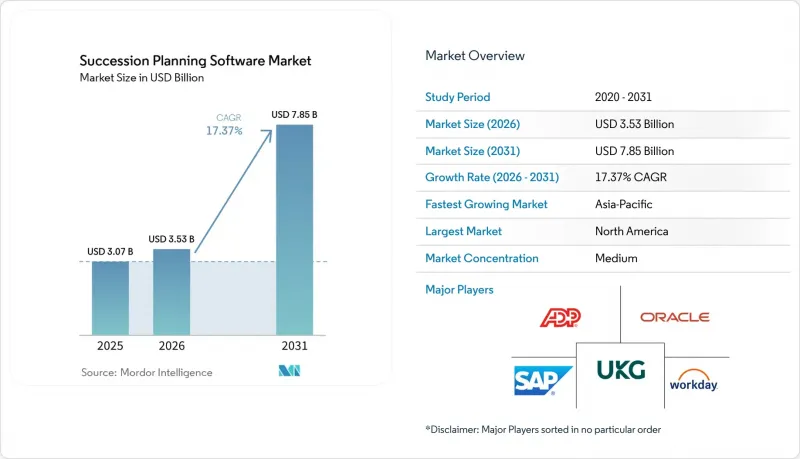

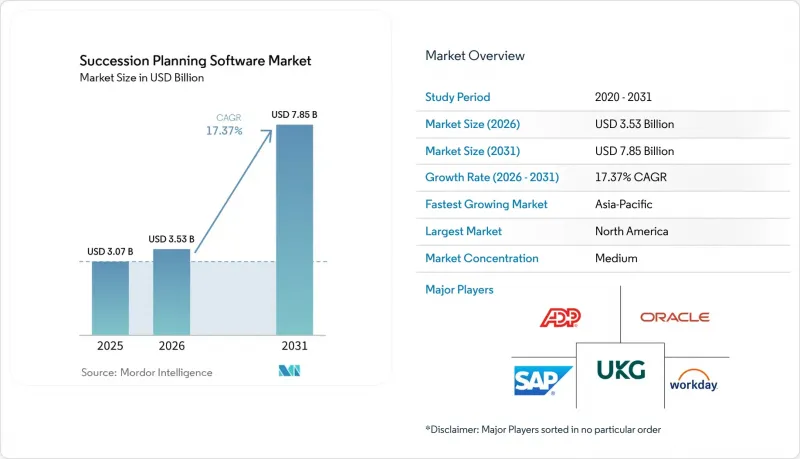

Mordor Intelligence에 의하면, 승계 계획 소프트웨어 시장 규모는 2025년에 30억 7,000만 달러로 평가되었습니다. 2026년 35억 3,000만 달러에서 2031년까지 78억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 17.37%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 모델(On-Premise 및 클라우드 기반), 조직 규모(중소기업(SME) 및 대기업), 최종 사용자 산업(은행 및 금융 서비스·보험(BFSI), 정보 기술·통신, 교육, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 승계 계획 소프트웨어 시장 동향 및 인사이트

AI를 활용한 인재 분석 도입 가속화

인공지능은 단편적인 평가를 지속적인 인재 인텔리전스로 전환함으로써 후계자 육성 프로그램을 혁신하고 있습니다. 최신 플랫폼은 성과 데이터, 역량 평가, 동료들의 피드백을 종합하여, 향후 몇 달 동안의 이직 위험을 파악할 수 있는 실시간 후계자 히트맵을 생성합니다. 이를 통해 주요 직책의 채용 소요 시간을 30% 단축하고, 사내 승진 비율을 18% 높였습니다. SAP는 2025년에 “Joule AI 코파일럿"를 도입하여, 관리자가 쉬운 말로 승계 계획 시나리오를 확인할 수 있도록 했습니다. 이는 대화형 분석이 의사결정 주기를 어떻게 가속화하는지를 보여줍니다. 이러한 기능은 틈새 분야의 기술 요건을 충족하는 외부 인재 채용이 어려운 의료 및 제조업 분야에서 특히 중요한 역할을 하고 있습니다.

기술 부족을 배경으로 높아지는 사내 전보 수요

노동 시장의 긴축으로 인해, 사내 이동은 단순한 인재 유지 전략에서 기업 전략으로 격상되었습니다. 호주 공무원 위원회(Australian Public Service Commission)의 보고서에 따르면, 2025년에는 88%의 기관이 심각한 기술 격차에 직면할 것으로 예상되며, 채용 공고가 구인사이트에 게시되기 전에 사내 인재를 발굴할 수 있는 도구에 대한 긴급 투자가 촉구되고 있습니다. 2026년 3월에 출시된 Fuel50의 “기술 성장 예측 모델(Skills Growth Predictive Model)"는 미래의 역량 요구 사항을 예측하고, 직원들이 몇년후를 내다보며 리더십을 발휘할 수 있도록 준비할 수 있는 맞춤형 학습 경로를 제안합니다. 사내 전보를 중시하는 조직에서는 재직 기간이 41% 더 길고, 직원 몰입도 점수가 25% 더 높은 것으로 나타났으며, 이러한 수치는 경력 경로를 자동화하는 후계자 육성 플랫폼의 비즈니스적 유효성을 입증하고 있습니다.

인재 프로파일과 관련된 데이터 개인정보 보호 및 보안 문제

후계자 육성 도구에는 GDPR(EU 개인정보보호규정) 및 캘리포니아주 소비자 개인정보 보호법(CCPA)에 따라 엄격한 동의 및 보존 규정이 적용되는 기밀성이 높은 고용 데이터가 저장되어 있습니다. 2024년, 규제 당국은 GDPR(EU 개인정보보호규정) 위반에 대해 21억 유로(23억 달러)의 벌금을 부과했습니다. 이에 따라 인사 담당 임원의 34%가 거버넌스 체제가 정비될 때까지 플랫폼 도입을 일시 중단하고 있습니다. 각 벤더사는 현재 역할 기반 접근 제어 및 의사 익명화와 같은 ‘프라이버시 바이 디자인" 기능을 탑재하고 있지만, 많은 중소기업은 여러 국가에 걸친 규정 준수 체제에 대응할 수 있는 법무 인력이 부족합니다.

부문별 분석

2025년, 승계 계획 소프트웨어 시장에서 소프트웨어가 66.45%의 점유율을 유지했으며, 플랫폼 라이선스가 여전히 수익의 핵심을 차지하고 있는 것으로 확인되었습니다. 그러나 도입 과정에서 발생하는 과제로 인해 AI 모델 설정 및 레거시 데이터 통합을 담당하는 자문 파트너와의 계약이 증가하고 있으며, 이러한 변화가 서비스 분야의 연평균 성장률(CAGR) 19.23%라는 예측을 뒷받침하고 있습니다. 다중 벤더 인재 관리 생태계에 직면한 기업들은 대개 전 세계의 시스템 통합사업자를 통해 도입을 진행하고 있으며, 현재는 기술적인 작업 외에도 변경 관리 워크숍도 패키지 형태로 제공되고 있습니다. 이러한 부가가치가 높은 패키지는 고객이 인재 워크플로우의 현대화를 추진하는 과정에서 공급업체가 고객의 유지율을 높이는 데 도움이 되고 있습니다.

매니지드 서비스는 사내에 분석 담당자가 없는 중견 기업에게 매력적인 옵션이며, 서비스 제공업체는 데이터의 일관성을 모니터링하고 분기별 리더십 파이프라인 보고서를 제공할 수 있게 됩니다. 승계 계획 소프트웨어 시장의 매니지드 서비스 시장 규모는 2031년까지 두 자릿수 성장률을 기록하며 확대될 것으로 예상되며, 이는 운영 예산에 맞춘 구독형 비즈니스 모델에 대한 수요를 반영한 것입니다. 틈새 시장 컨설팅 기업들은 도입 기간을 수개월에서 수주로 단축하는 고정 가격 플레이북을 제공함으로써 이에 대응하고 있으며, 이를 통해 진행 중인 실적 평가에 미치는 지장을 줄이고 있습니다. 이사회가 후계자 후보의 상황을 더 자주 파악할 것을 요구하는 가운데, 이러한 서비스 주도적인 추세는 앞으로도 지속될 전망입니다.

2025년 기준으로, 승계 계획 소프트웨어 시장 점유율의 60.21%를 On-Premise 도입이 차지했습니다. 이는 많은 대기업들이 여전히 구식 인사 관리 제품군 내에서 인사 관리 모듈을 운영하고 있기 때문입니다. 그러나 자동 갱신, 설비 투자 절감, 모바일 접속 등 하이브리드 근무 환경의 직원들이 선호하는 장점 덕분에 클라우드 구독 시장은 연평균 성장률(CAGR) 20.01%를 나타낼 것으로 전망됩니다. SOC 2 Type II 및 ISO 27001 인증을 획득한 공급업체는 과거 로컬 서버에서 운영할 수밖에 없었던 보안상의 우려를 해소하고 있습니다. 그 결과, 신규 구매자들이 영구 라이선스를 요구하는 경우는 거의 없어졌습니다.

클라우드 플랫폼용 승계 계획 소프트웨어 시장 규모는 2031년까지 On-Premise 방식의 매출액을 넘어설 것으로 예측됩니다. 이러한 반전은 신속한 도입을 우선시하는 중소기업에 의해 주도되고 있습니다. API를 활용한 통합을 통해 인사 담당자는 몇 달이 아닌 며칠 만에 승계 계획 대시보드를 채용, 교육, 보상 관리 시스템에 통합할 수 있게 됩니다. 규제가 엄격한 업계에서는 기밀성이 높은 개인 데이터를 On-Premise에 보관하면서 분석 워크로드를 클라우드로 이전하는 하이브리드 아키텍처가 여전히 과도기적인 모델로 남아 있습니다. 그러나 분석가들은 ‘클라우드 우선’을 내세운 조달 조건이 현재 대부분의 RFP(제안 요청서)에서 표준으로 자리 잡았다는 점에 의견을 같이하고 있습니다.

지역별 분석

북미는 서벤스-옥슬리법의 거버넌스 규정과 탄탄한 벤더 생태계의 뒷받침을 받아, 2025년에는 37.89%의 점유율로 승계 계획 소프트웨어 시장을 주도했습니다. 상장 기업들은 이사회 수준의 파이프라인 지표를 정기적으로 공개하고 있으며, 이에 따라 업종을 불문하고 플랫폼에 대한 지출이 정착되고 있습니다. 캐나다도 비슷한 추세를 보이고 있으며, 연방 정부의 정책에 따라 핵심 기능의 연속성 계획 수립이 요구되고 있습니다. 또한, 멕시코의 아웃소싱 거점은 다국적 기업 고객을 지원하기 위해 표준화된 인사 체계를 도입하고 있습니다. 이러한 기반을 바탕으로 지역 공급업체들은 높은 계약 갱신율을 유지하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 18.96%를 나타낼 것으로 예측되며, 승계 계획 소프트웨어 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 인도나 중국에서는 클라우드 인프라 비용이 지속적으로 하락함에 따라 디지털 HR 전환이 가속화되고 있습니다. 한편, 호주의 공공 기관들은 전국적인 기술 인력 부족 문제에 대처할 수 있는 방안을 적극적으로 모색하고 있습니다. 일본에서는 노동력의 고령화에 따라 지식 전수의 필요성이 커지고 있으며, 대형 복합 기업들은 수작업에 의존하던 멘토 제도를 분석을 기반으로 한 후계자 계획 대시보드로 대체하고 있습니다. 현지 급여 계산 시스템 및 노동법에 대한 대응은 여전히 시장 진출의 필수 조건으로 남아 있습니다. 데이터 소재지 보증을 확보한 공급업체는 보다 신속한 조달 주기를 실현할 수 있습니다.

유럽에서는 독일, 영국, 프랑스를 중심으로 꾸준한 도입이 진행되고 있으며, 특히 프랑스에서는 “기업 지속가능성 보고 지침(CSRD)"에 따라, 인재 계획이 ESG 공시의 중요한 요소로 자리 잡고 있습니다. 남미에서는 동향에 편차가 나타나고 있습니다. 브라질의 은행들은 꾸준히 투자를 진행하고 있지만, 다른 지역에서는 환율 변동으로 인해 프로젝트 승인이 지연될 가능성이 있습니다. 중동 및 아프리카, 특히 아랍에미리트(UAE)와 사우디아라비아에서는 정부의 경제 다각화 정책에 힘입어 틈새 수요가 나타나고 있습니다. 지역 데이터 보호 체계가 성숙해지기 전까지, 하이브리드형 호스팅 모델이 가교 역할을 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the succession planning software market size was valued at USD 3.07 billion in 2025 and estimated to grow from USD 3.53 billion in 2026 to reach USD 7.85 billion by 2031, at a CAGR of 17.37% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Model (On-Premises, and Cloud-Based), Organization Size (Small and Medium-Sized Enterprises [SMEs], and Large Enterprises), End-User Industry (Banking, Financial Services, and Insurance [BFSI], Information Technology and Telecom, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Succession Planning Software Market Trends and Insights

Accelerating Adoption of AI-Driven Talent Analytics

Artificial intelligence is transforming succession programs by converting episodic reviews into continuous talent intelligence. Modern platforms combine performance data, skills assessments, and peer feedback to create real-time succession heat maps that uncover flight risks months in advance, cutting time-to-fill for critical roles by 30% and boosting internal promotions by 18%. SAP embedded the Joule AI copilot in 2025 so managers can query succession scenarios in plain language, illustrating how conversational analytics hasten decision cycles. These capabilities carry particular weight in healthcare and manufacturing, where external hiring often struggles to match niche skill requirements.

Rising Demand for Internal Mobility Amid Skills Shortages

Tight labor markets have elevated internal mobility from a retention tactic to an enterprise strategy. The Australian Public Service Commission reported that 88% of agencies faced critical skills gaps in 2025, prompting urgent investment in tools that surface internal candidates before vacancies hit job boards. Fuel50's Skills Growth Predictive Model, launched in March 2026, forecasts future competency needs and recommends individual learning paths that prepare employees for leadership years in advance. Organizations emphasizing internal mobility record 41% longer tenure and 25% higher engagement scores, figures that strengthen the business case for succession platforms that automate career pathing.

Data Privacy and Security Concerns in Talent Profiles

Succession tools store sensitive employment data that triggers strict consent and retention rules under the GDPR and the California Consumer Privacy Act. Regulators issued EUR 2.1 billion (USD 2.3 billion) in GDPR fines during 2024, causing 34% of HR leaders to pause platform deployments until governance models mature. Vendors now embed privacy-by-design features such as role-based access controls and pseudonymization, yet many small enterprises lack the legal resources to navigate multi-country compliance regimes.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Compliance Pressures for Leadership Continuity Planning

- Growing Shift Toward Cloud-Native HR Tech Stacks

- Resistance to Change From Traditional HR Practices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software retained 66.45% of the succession planning software market in 2025, confirming that platform licenses still form the revenue core. Implementation challenges, however, are steering more contracts toward advisory partners that configure AI models and integrate legacy data, a shift that explains the 19.23% CAGR forecast for services. Enterprises facing multivendor human capital ecosystems often route deployments through global systems integrators, which now bundle change-management workshops alongside technical tasks. These value-added packages help vendors defend account stickiness as customers modernize talent workflows.

Managed services appeal to mid-market firms that lack in-house analytics staff, allowing providers to monitor data hygiene and deliver quarterly leadership pipeline reports. The succession planning software market size for managed offerings is projected to rise at double-digit rates through 2031, reflecting demand for subscription economics aligned with operating budgets. Niche consultancies have responded with fixed-price playbooks that compress launch timelines from months to weeks, thereby reducing disruption to ongoing performance reviews. This service-led momentum should continue as boards request more frequent bench-strength updates.

On-premises deployment accounted for 60.21% succession planning software market share in 2025 because many large enterprises still run talent modules inside older human capital suites. Yet cloud subscriptions are scaling at a 20.01% CAGR thanks to automatic updates, lower capital expense, and mobile access, benefits that resonate with hybrid workforces. Vendors that achieve SOC 2 Type II and ISO 27001 certifications now ease security objections that once anchored workloads on local servers. As a result, new buyers rarely request perpetual licenses.

The succession planning software market size for cloud platforms is expected to surpass on-premises revenue before 2031, a crossover driven by small and medium-sized enterprises prioritizing rapid implementation. API-enabled integration lets HR leaders stitch succession dashboards into recruiting, learning, and compensation systems in days rather than months. Hybrid architectures remain a transitional model in heavily regulated industries, keeping sensitive personal data on-site while pushing analytics workloads to the cloud. However, analysts agree that cloud-first procurement language is now standard in most RFPs.

Complete Report Scope:

- By Component

- Software

- Talent Identification and Assessment Software

- Succession Planning and Role Mapping Software

- Career Pathing and Development Planning Software

- Leadership Development and Readiness Software

- Workforce Analytics and Talent Intelligence Software

- Other Software

- Services

- Software

- By Deployment Model

- On-Premises

- Cloud-Based

- By Organization Size

- Small and Medium-Sized Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- Information Technology and Telecom

- Manufacturing

- Education

- Government

- Other End-User Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America led the succession planning software market with a 37.89% share in 2025, supported by Sarbanes-Oxley governance rules and a dense vendor ecosystem. Public corporations routinely disclose board-level pipeline metrics, which normalizes platform spending across industries. Canada mirrors the trend as federal policies demand continuity plans for critical functions, and Mexico's outsourcing hubs adopt standardized HR frameworks to serve multinational clients. This foundation gives regional suppliers strong renewal rates.

Asia-Pacific is projected to post an 18.96% CAGR, making it the fastest-growing territory within the succession planning software market. Digital HR transformation across India and China is accelerating because cloud infrastructure costs keep falling, while Australia's public agencies actively seek tools that address nationwide skill shortages. Japan's aging workforce intensifies knowledge-transfer needs, prompting large conglomerates to replace manual mentorship schemes with analytics-driven succession dashboards. Local payroll and labor-law integrations remain table stakes for market entry. Vendors that secure data-residency assurances win faster procurement cycles.

Europe maintains steady uptake anchored in Germany, the United Kingdom, and France, where the Corporate Sustainability Reporting Directive elevates workforce planning to ESG disclosures. South America shows mixed momentum: Brazil's banks invest steadily, but currency swings can slow project approvals elsewhere. The Middle East and Africa contribute niche demand driven by government diversification agendas, particularly in the United Arab Emirates and Saudi Arabia. Hybrid hosting models offer a bridge until regional data-protection frameworks mature.

- SAP SE

- Oracle Corporation

- Workday Inc.

- UKG Inc.

- Cornerstone OnDemand Inc.

- ADP Inc.

- Ceridian HCM Holding Inc.

- BambooHR LLC

- Gloat Ltd.

- Eightfold AI Inc.

- TalentGuard Inc.

- PeopleFluent Inc.

- SumTotal Systems LLC

- PageUp People Holdings Pty Ltd

- ClearCompany LLC

- Plum.io Inc.

- Lattice Holdings Inc.

- HiBob Ltd.

- Degreed Inc.

- Fuel50 Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Adoption of AI-Driven Talent Analytics

- 4.2.2 Rising Demand for Internal Mobility Amid Skills Shortages

- 4.2.3 Increasing Compliance Pressures for Leadership Continuity Planning

- 4.2.4 Growing Shift Toward Cloud-Native HR Tech Stacks

- 4.2.5 Expansion of Remote and Hybrid Work Models Requiring Digital Succession Processes

- 4.2.6 Integration of Succession Planning With Broader Talent Management Suites

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Security Concerns in Talent Profiles

- 4.3.2 Resistance to Change From Traditional HR Practices

- 4.3.3 Limited Skilled Administrators to Manage Advanced Platforms

- 4.3.4 Economic Uncertainty Causing HR Tech Spending Delays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Talent Identification and Assessment Software

- 5.1.1.2 Succession Planning and Role Mapping Software

- 5.1.1.3 Career Pathing and Development Planning Software

- 5.1.1.4 Leadership Development and Readiness Software

- 5.1.1.5 Workforce Analytics and Talent Intelligence Software

- 5.1.1.6 Other Software

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 On-Premises

- 5.2.2 Cloud-Based

- 5.3 By Organization Size

- 5.3.1 Small and Medium-Sized Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 Banking, Financial Services, and Insurance (BFSI)

- 5.4.2 Healthcare

- 5.4.3 Information Technology and Telecom

- 5.4.4 Manufacturing

- 5.4.5 Education

- 5.4.6 Government

- 5.4.7 Other End-User Industry

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Workday Inc.

- 6.4.4 UKG Inc.

- 6.4.5 Cornerstone OnDemand Inc.

- 6.4.6 ADP Inc.

- 6.4.7 Ceridian HCM Holding Inc.

- 6.4.8 BambooHR LLC

- 6.4.9 Gloat Ltd.

- 6.4.10 Eightfold AI Inc.

- 6.4.11 TalentGuard Inc.

- 6.4.12 PeopleFluent Inc.

- 6.4.13 SumTotal Systems LLC

- 6.4.14 PageUp People Holdings Pty Ltd

- 6.4.15 ClearCompany LLC

- 6.4.16 Plum.io Inc.

- 6.4.17 Lattice Holdings Inc.

- 6.4.18 HiBob Ltd.

- 6.4.19 Degreed Inc.

- 6.4.20 Fuel50 Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment