|

시장보고서

상품코드

2073293

의료 분야 급여 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Payroll Software In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

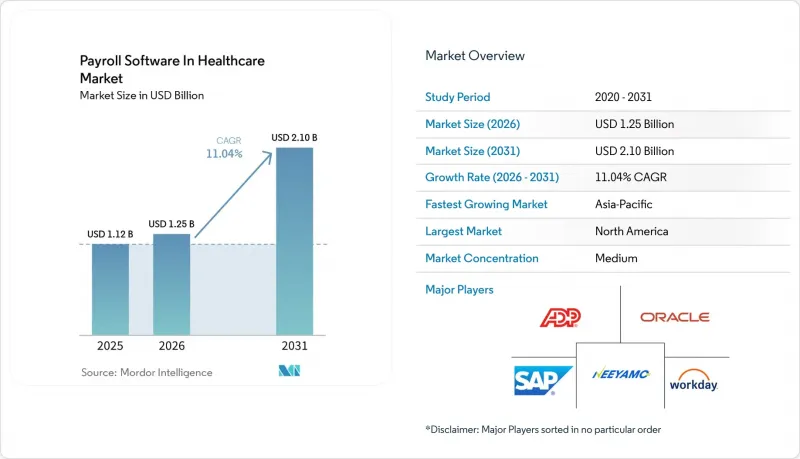

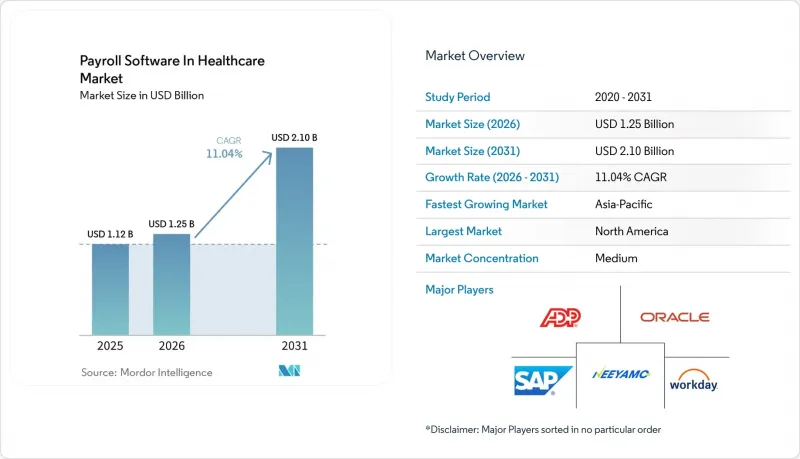

Mordor Intelligence에 의하면, 의료 분야 급여 소프트웨어 시장 규모는 2025년 11억 2,000만 달러로 평가되었습니다. 2026년 12억 5,000만 달러에서 2031년까지 21억 달러로 확대될 것으로 예측되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 11.04%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 용도(급여 계산, 근태 관리, 규정 준수 및 세무 관리, 복리후생 관리, 기타 용도), 배포 방식(클라우드 및 On-Premise), 최종 사용자(병원, 장기 요양·노인 요양 시설 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료 분야 급여 소프트웨어 시장 동향 및 인사이트

여러 관할 구역에 걸쳐 있는 의료 분야 급여 규정 준수 문제가 복잡해지고 있습니다.

2026년에 시행된 미네소타주 및 메릴랜드주의 유급 휴가 의무화에 따라, 고용주는 보험료 원천징수, 개별 적립 장부 관리, 분기별 신고서 제출이 의무화되었으나, 이러한 업무는 수작업 워크플로우로는 감당하기 어려운 규모에 이르렀습니다. SECURE Act 2.0에서는 연소득 14만 5,000달러를 초과하는 직원에 대한 손실 보전 기여금이 추가됨에 따라, 연도 중반에 코드 변경이 불가피하게 되었습니다. “Symmetry Tax Engine Premium"는 현재 7,000개 이상의 세무 관할 구역을 4밀리초 미만의 지연 시간으로 처리하고 있으며, 인공지능이 인간 감사 담당자보다 더 신속하게 중복되는 규정을 분석할 수 있음을 입증하고 있습니다. 2026년 ADP 조사에 따르면, 아시아태평양 기업의 71%가 규정 위반으로 인한 벌금을 납부하고 있는 것으로 나타나, 그 재정적 위험의 심각성이 부각되고 있습니다. 여러 주에 걸쳐 운영되는 병원 체인의 경우, 감사 및 추징세 위험이 이미 낮은 수익률을 더욱 압박하고 있어, 규정 준수 프로세스의 자동화가 주요 구매 기준으로 자리 잡고 있습니다.

병원에서의 클라우드 기반 급여 계산 솔루션으로의 전환이 가속화되고 있습니다.

미국 보건사회복지부는 2025년, 유지 관리 비용 절감과 재해 복구 능력 향상을 이유로 급여 계산 시스템을 클라우드 플랫폼으로 이전했습니다. ChristianaCare도 시스템 전환 후 급여 처리 시간을 30% 단축했습니다. 2024년에 발생한 Change Healthcare의 데이터 유출 사건에서는 1억 9,270만 건의 기록이 유출되었으며, 이에 따라 보안에 대한 기대가 높아지면서 규제 당국은 암호화 의무화와 데이터 유출 발생 후 72시간 이내의 통지 의무를 제안하기에 이르렀습니다. 2025년에는 Workday와 Salesforce에서 정보 유출 사고가 발생하여 700개 이상의 조직이 피해를 입었습니다. 이는 최고 수준의 벤더조차도 취약점을 안고 있음을 보여줍니다. 이러한 사건에도 불구하고, 클라우드 도입은 연평균 성장률(CAGR) 14.02%로 성장할 전망입니다. 이는 외래수술센터(ASC)나 지방 진료소들이 On-Premise형 시스템에는 없는 자본 부담이 적은 모델이나 지속적인 기능 업데이트를 선호하기 때문입니다.

클라우드 급여 계산 시스템 도입을 가로막는 데이터 보안 및 환자 개인정보 보호에 대한 우려

급여 파일에는 휴가 정보 및 복리후생 선택 내용이 포함되어 있으므로, HIPAA(의료보험 이동성 및 책임에 관한 법률)에 따라 보호 대상인 건강 정보(PHI)에 해당합니다. 2025년에 제안된 개정안에서는 저장 시 및 전송 중인 데이터의 암호화, 다단계 인증, 그리고 72시간 이내의 정보 유출 통보가 의무화되어 있습니다. 2025년 Workday와 Salesforce에서 발생한 정보 유출 사고는 집단 소송으로 이어졌으며, 일부 병원은 On-Premise 백업으로 되돌아갈 수밖에 없게 되었습니다. IBM의 추산에 따르면, 의료 업계에서 발생하는 정보 유출로 인한 평균 피해액은 742만 달러로, 벌금 및 신용 감시 비용을 포함하면 업계 전체 평균의 3배에 달할 전망입니다. 현재 보안 담당자들은 연 1회의 침투 테스트와 5,000만 달러 이상의 사이버 보험 가입을 요구하고 있으며, 이로 인해 조달 절차가 최대 9개월까지 지연되어 소규모 클라우드 스타트업 기업들이 불리한 입장에 처해 있습니다.

부문별 분석

아시아태평양 기관의 71%가 매년 보고하는 제재를 피하기 위해 의료 시스템이 세무 신고 업무를 외부에 위탁하게 되면서, 의료 분야 급여 소프트웨어 시장에서 서비스가 차지하는 비중이 증가하고 있습니다. 대규모 통합 의료 제공 네트워크는 노동조합 규정에 광범위하게 대응할 수 있는 영구 라이선스를 선호하기 때문에 소프트웨어는 2025년 매출의 66.41%를 계속 차지했습니다. 그러나 ADP의 공동 고용 모델은 원천징수 오류에 대한 책임을 전가할 수 있기 때문에 전담 급여 계산 담당 직원이 없는 외래 진료 센터들의 관심을 끌고 있습니다. SECURE Act 2.0에 따른 로스 IRA의 추가 납입 의무와 각 주의 유급 휴가 보험료 인상으로 인해, 2026년에는 신고 절차가 복잡해지면서 급여 계산 대행 서비스에 대한 문의가 급증했습니다. Paychex가 Paycor를 41억 달러에 인수한 것은 소프트웨어 및 서비스가 하나의 지붕 아래 통합되고 있음을 보여줍니다.

하이브리드형 서비스 제공으로 인해 부문 간의 경계가 모호해지고 있습니다. 현재 각 벤더사는 세무 신고 서비스와 결합된 소프트웨어 구독 상품을 판매하고 있어, 의료 분야 급여 소프트웨어 시장 점유율을 산출하는 것이 복잡해지고 있습니다. 중규모 병원들은 설정 관리보다 예측 가능한 가격 책정을 우선시하고 있으며, 이것이 아웃소싱 시장의 두 자릿수 성장을 이끌고 있습니다. 2주마다 5만 건의 급여 명세서를 처리하는 여러 주에 걸쳐 운영되는 시스템에서는 여전히 기존의 On-Premise형 제품군이 주류를 이루고 있지만, 이러한 제공업체들조차 벌금 보상을 보장하는 서비스 확장의 시범 운영을 진행하고 있습니다. 예측 기간 동안 소프트웨어가 절대액 기준으로는 최대 점유율을 유지하더라도, 서비스 수익은 라이선스 수익을 상회할 것으로 전망됩니다.

2025년 매출 중 급여 계산 처리가 45.89%를 차지했으나, 규정 준수 및 세무 관리 부문은 연평균 성장률(CAGR) 12.98%로 가장 빠른 성장세를 보일 것으로 전망됩니다. 병원들은 벌금이나 시정 조치에 소요되는 시간을 감당할 수 없기 때문에 실시간 규정 준수 알림에 대해 30%에서 40%의 할증료를 지불하고 있습니다. Symmetry Tax Engine Premium은 7,000개 관할 구역에 걸쳐 4밀리초 미만의 규칙 처리 성능을 입증하며, 과거의 비용 센터를 전략적 기능으로 탈바꿈시켰습니다. 2026년 메디케어 의사 보수 일정에 따른 작업 상대 가치 단위(WRVU)의 2.5% 변경으로 인해 주기 도중 업데이트가 불가피하게 되었으며, 규정 준수를 스트리밍 피드가 아닌 정적 테이블로 처리하는 시스템에 부하가 가해졌습니다.

근태 관리는 일정 관리와 급여 계산을 연결하는 중요한 역할을 계속해서 수행하고 있으며, 생체 인증 스캐너와 모바일 지오펜싱을 도입함으로써 대리 출퇴근 기록을 억제하고 있습니다. 복리후생 관리에서는 가입 절차와 보험료 대조가 자동화되어, 급여 계산 주기 외의 조정 업무가 줄어들었습니다. 급여 압류 처리나 조합비 송금은 여전히 틈새 분야이지만, 이러한 요소들이 구매자들을 결제 전반을 다루는 플랫폼으로 이끌고 있습니다. 의료 분야 급여 소프트웨어 시장에서 규정 준수 모듈의 규모가 확대되고 있습니다. 이는 오류가 감사나 추징세, 나아가 임상의의 신용 훼손으로까지 비화되어, 소프트웨어 라이선스 비용을 훨씬 상회하는 손실을 초래하기 때문입니다. 컴플라이언스 갱신을 연간 단위가 아닌 매주 수익화할 수 있는 공급업체가, 이처럼 증가하는 지출을 확보하게 될 것입니다.

지역별 분석

2025년 북미는 의료 분야 급여 소프트웨어 시장 매출의 37.54%를 계속 차지했습니다. 이는 주 및 지방 세제가 전문적인 규정 준수 엔진을 필요로 하기 때문입니다. 캘리포니아주만 해도 9가지 유형의 장애 보험 요율과 58개의 카운티 세금이 설정되어 있으며, 이 모든 항목이 각 급여 명세서에 반영되어야 합니다. 2026년 메디케어 의사 보수 일정 및 진료비 갱신으로 인해 의사의 보수를 실시간으로 재조정해야 할 필요가 생겼으며, 매일 밤 진행되는 일괄 갱신만으로는 더 이상 충분하지 않다는 사실이 밝혀졌습니다. 캐나다 서스캐처원주에서 발생한 비용의 급증은 전환 비용이라는 장벽을 여실히 보여주고 있습니다. 2024년 멕시코의 사회보장 개혁으로 인해 민간 병원 체인들은 전자 신고 기능을 통합한 클라우드 기반 급여 계산 시스템으로의 전환을 강요받게 되었습니다.

유럽에서는 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))과 향후 도입될 유럽 건강 데이터 공간(EHDS)이 적용되고 있으며, 두 규정 모두 지역 내 데이터 보관을 의무화하고 있습니다. 영국, 독일, 프랑스의 국민건강보험 서비스에서는 근로시간 지침의 제한을 준수하기 위해 근태 관리의 디지털화가 추진되고 있습니다. Zalaris와 같은 벤더들은 이러한 요구 사항을 충족하기 위해 자국에 설치된 데이터센터를 활용하고 있습니다. 한편, 아시아태평양에서는 노동력 부족과 정부 주도의 디지털화를 배경으로 2031년까지 연평균 12.54%의 성장이 예상됩니다. 인도의 “통합 결제 인터페이스(UPI)" 덕분에 급여를 즉시 지급할 수 있게 되었습니다. 일본에서는 월간 초과근무 시간 상한이 의무화되어 있으며, 호주의 ‘원터치 급여 계산 제도"에서는 급여 계산 시마다 세무서에 실시간으로 데이터가 전송됩니다.

아프리카와 중동에서는 “사우디 비전 2030" 및 아랍에미리트(UAE)의 의료 확대 계획에 따라 클라우드 인프라에 대한 투자가 진행되고 있지만, 계약 수주는 아랍어 현지화 및 현지 데이터센터를 제공하는 벤더들에게 쏠리고 있습니다. 남미와 아프리카는 도입 초기 단계에 머물러 있지만, 브라질의 “eSocial"이니셔티브와 남아프리카공화국의 PAYE(원천징수) 제도의 현대화가 미래 성장을 위한 기반을 마련하고 있습니다. 이러한 지역별 특성이 복합적으로 작용함에 따라, 각 벤더사는 세무 엔진의 지원 범위를 확대하는 동시에 현지화 기능을 추가함으로써, 의료 분야 급여 소프트웨어 잠재 고객 기반을 확대하도록 촉진받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the payroll software in healthcare market size is projected to expand from USD 1.12 billion in 2025 and USD 1.25 billion in 2026 to USD 2.10 billion by 2031, registering a CAGR of 11.04% between 2026 to 2031.

This report is Segmented by Component (Software, and Services), Application (Payroll Processing, Time and Attendance Tracking, Compliance and Tax Management, Benefits Administration, and Other Applications), Deployment Mode (Cloud, and On-Premises), End User (Hospitals, Long-term Care and Aged Care Facilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Payroll Software In Healthcare Market Trends and Insights

Rising Complexity of Multi-Jurisdiction Healthcare Payroll Compliance

Paid-leave mandates in Minnesota and Maryland that took effect in 2026 oblige employers to withhold premiums, maintain separate accrual ledgers, and file quarterly returns, tasks that manual workflows cannot scale. The SECURE Act 2.0 adds Roth catch-up deferrals for employees earning above USD 145,000, forcing mid-year code changes. Symmetry Tax Engine Premium now processes more than 7,000 tax jurisdictions with sub-four-millisecond latency, proving that artificial intelligence can parse overlapping rules faster than human auditors. A 2026 ADP survey showed 71% of Asia-Pacific organizations paid non-compliance penalties, underlining the financial stakes. For multistate hospital chains, the risk of audits and back-tax assessments erodes already-tight margins, making compliance automation a primary purchasing criterion.

Accelerating Shift Toward Cloud-Based Payroll Solutions in Hospitals

The U.S. Department of Health and Human Services migrated payroll to a cloud platform in 2025, citing lower maintenance overhead and better disaster recovery. ChristianaCare cut payroll-processing time by 30% after its own migration. Security expectations rose after the 2024 Change Healthcare breach, which compromised 192.7 million records, prompting regulators to propose mandatory encryption and 72-hour breach notification windows. Workday and Salesforce experienced a 2025 breach that affected more than 700 organizations, demonstrating that even tier-one vendors remain vulnerable. Despite these incidents, cloud deployments are set to grow at a 14.02% CAGR because ambulatory surgery centers and rural clinics prefer capital-light models and continuous feature updates that on-premises systems lack.

Data Security and Patient Privacy Concerns Hindering Cloud Payroll Adoption

Because payroll files contain leave data and benefit elections, they qualify as protected health information under HIPAA. Proposed 2025 amendments require encryption at rest and in transit, multi-factor authentication, and breach notification in under 72 hours. The 2025 breach at Workday and Salesforce triggered class-action lawsuits and forced some hospitals to revert to on-premises backups. IBM pegged the average healthcare breach at USD 7.42 million, triple the cross-industry mean, due to fines and credit-monitoring expenses. Security officers now demand annual penetration tests and cyber-insurance policies above USD 50 million, delaying procurements by up to nine months and putting small cloud startups at a disadvantage.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Integrated Workforce Management to Reduce Administrative Costs

- Growing Demand for Real-Time Analytics for Staffing Optimization

- High Switching Costs From Legacy HRIS in Large Health Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services accounted for a rising slice of the payroll software in healthcare market as health systems outsource tax filing to avoid penalties that 71% of Asia-Pacific organizations report each year. Software still generated 66.41% of 2025 revenue because large integrated delivery networks favor perpetual licenses that can handle union rules at scale. However, ADP's co-employment model transfers liability for withholding errors, attracting ambulatory centers that lack dedicated payroll staff. The SECURE Act 2.0 Roth catch-up mandate and new state paid-leave premiums increased filing complexity in 2026, spurring a surge in managed-payroll inquiries. Paychex's USD 4.1 billion purchase of Paycor underscores the convergence of software and services under one roof.

Hybrid offerings blur segment boundaries. Vendors now sell software subscriptions bundled with tax-filing services, complicating the attribution of payroll software in healthcare market share. Mid-sized hospitals prefer predictable pricing over configuration control, driving double-digit growth in outsourcing. Legacy on-premises suites still dominate among multistate systems processing 50,000 paychecks every two weeks, but even these providers are piloting service extensions that guarantee penalty reimbursement. Over the forecast horizon, service revenues are set to outpace license revenues even if software retains the largest absolute pool.

While payroll processing captured 45.89% of 2025 revenue, compliance and tax management is on course for the fastest expansion at a 12.98% CAGR. Hospitals cannot afford fines or remediation time, so they pay a 30% to 40% premium for real-time compliance feeds. Symmetry Tax Engine Premium demonstrates the value of sub-four-millisecond rule processing across 7,000 jurisdictions, turning an erstwhile cost center into a strategic feature. The 2026 Medicare Physician Fee Schedule's 2.5% work-relative-value-unit change forced mid-cycle updates, stressing systems that treat compliance as static tables instead of streaming feeds.

Time and attendance remains the connective tissue between scheduling and payroll, adding biometric scanners and mobile geofencing to curb buddy punching. Benefits administration automates enrollment and premium reconciliation, reducing off-cycle adjustments. Garnishment processing and union-dues remittance remain niche, yet they push buyers toward platforms that handle the full payments spectrum. The payroll software in healthcare market size for compliance modules grows because errors escalate to audits, back taxes, and damaged credit for clinicians, dwarfing software fees. Vendors able to monetize compliance updates weekly rather than annually will capture the incremental spend.

Complete Report Scope:

- By Component

- Software

- Services

- By Application

- Payroll Processing

- Time and Attendance Tracking

- Compliance and Tax Management

- Benefits Administration

- Other Applications

- By Deployment Mode

- Cloud

- On-Premises

- By End User

- Hospitals

- Clinics and Outpatient Centers

- Ambulatory and Diagnostic Centers

- Long-Term Care and Aged Care Facilities

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America retained 37.54% of payroll software in healthcare market revenue in 2025 because state and local tax regimes demand specialized compliance engines. California alone posts nine disability-insurance rates and 58 county levies, all of which must be reflected in each paycheck. The 2026 Medicare Physician Fee Schedule and practice-expense updates forced real-time physician-compensation recalibration, revealing that nightly batch updates no longer suffice. Canada's Saskatchewan cost blowout illustrates the switching-cost hurdle. Mexico's 2024 social-security reform pushed private hospital chains toward cloud payroll that integrates electronic filing.

Europe is governed by the General Data Protection Regulation and the forthcoming European Health Data Space, both of which compel in-region data residency. National health services in the United Kingdom, Germany, and France digitalize timekeeping to enforce Working Time Directive limits. Vendors such as Zalaris use sovereign data centers to navigate these requirements. Meanwhile, Asia-Pacific is forecast to grow at 12.54% through 2031, buoyed by workforce shortages and government digitalization. India's Unified Payments Interface enables instant salary disbursement; Japan enforces monthly overtime caps, and Australia's single-touch payroll regime submits every run to the tax office in real time.

The Middle East and Africa invest in cloud infrastructure under Saudi Vision 2030 and United Arab Emirates health-care expansion plans, though contract awards skew to vendors offering Arabic localization and local data centers. South America and Africa remain earlier in the adoption curve, but Brazil's eSocial initiative and South Africa's PAYE modernization lay groundwork for future growth. Together, these regional nuances encourage vendors to broaden tax-engine coverage while adding localization features that extend the payroll software in healthcare market addressable base.

- Automatic Data Processing, Inc.

- Ceridian HCM Holding Inc.

- Paychex, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paycor HCM, Inc.

- Ultimate Kronos Group LLC

- Intuit Inc.

- SAP SE

- Oracle Corporation

- Workday, Inc.

- BambooHR LLC

- Gusto, Inc.

- Sage Group plc

- TriNet Zenefits LLC

- Patriot Software Company

- Xero Limited

- Neeyamo Inc.

- Zalaris ASA

- Deel Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Complexity of Multi-Jurisdiction Healthcare Payroll Compliance

- 4.2.2 Accelerating Shift Toward Cloud-Based Payroll Solutions in Hospitals

- 4.2.3 Increasing Adoption of Integrated Workforce Management to Reduce Administrative Costs

- 4.2.4 Growing Demand for Real-Time Analytics for Staffing Optimization

- 4.2.5 Expansion of Value-Based Care Models Requiring Granular Labor Cost Allocation

- 4.2.6 Surge in Healthcare Gig Workforce Driving Need for Flexible Payroll Engines

- 4.3 Market Restraints

- 4.3.1 Data Security and Patient Privacy Concerns Hindering Cloud Payroll Adoption

- 4.3.2 High Switching Costs From Legacy HRIS in Large Health Systems

- 4.3.3 Shortage of Healthcare-Specific Payroll Tax Professionals

- 4.3.4 Fragmented Shift Differentials and Union Rules Complicating Standardization

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Application

- 5.2.1 Payroll Processing

- 5.2.2 Time and Attendance Tracking

- 5.2.3 Compliance and Tax Management

- 5.2.4 Benefits Administration

- 5.2.5 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premises

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Clinics and Outpatient Centers

- 5.4.3 Ambulatory and Diagnostic Centers

- 5.4.4 Long-Term Care and Aged Care Facilities

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Ceridian HCM Holding Inc.

- 6.4.3 Paychex, Inc.

- 6.4.4 Paycom Software, Inc.

- 6.4.5 Paylocity Holding Corporation

- 6.4.6 Paycor HCM, Inc.

- 6.4.7 Ultimate Kronos Group LLC

- 6.4.8 Intuit Inc.

- 6.4.9 SAP SE

- 6.4.10 Oracle Corporation

- 6.4.11 Workday, Inc.

- 6.4.12 BambooHR LLC

- 6.4.13 Gusto, Inc.

- 6.4.14 Sage Group plc

- 6.4.15 TriNet Zenefits LLC

- 6.4.16 Patriot Software Company

- 6.4.17 Xero Limited

- 6.4.18 Neeyamo Inc.

- 6.4.19 Zalaris ASA

- 6.4.20 Deel Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment