|

시장보고서

상품코드

2073330

북미의 사료용 향료 및 감미료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Feed Flavors and Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

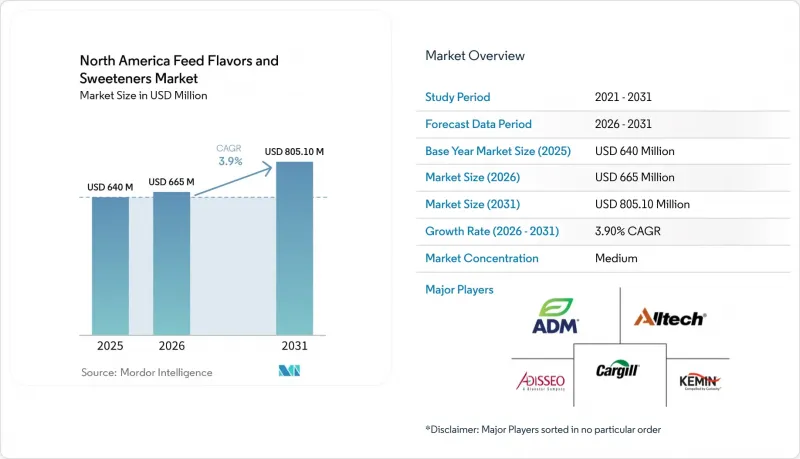

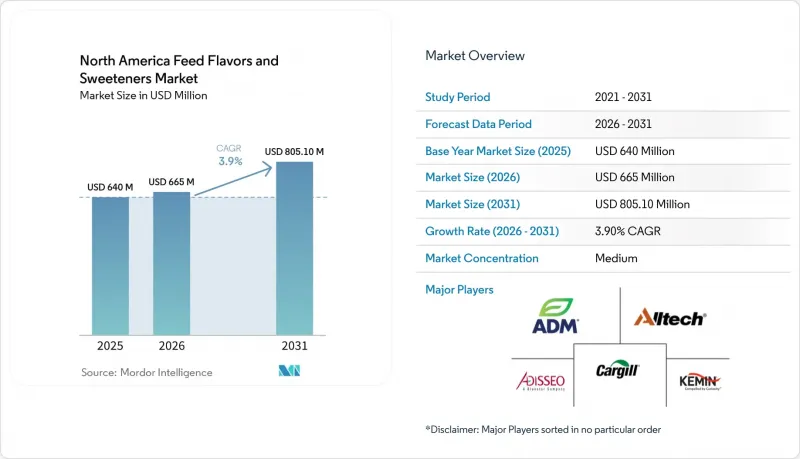

Mordor Intelligence에 의하면, 북미의 사료용 향료 및 감미료 시장은 2025년에 6억 4,000만 달러로 평가되었습니다. 2026년에는 6억 6,500만 달러에 이를 것으로 예상됩니다.

또한, 예측 기간 종료 시점에는 8억 510만 달러에 달할 것으로 추정되며, 2026년부터 2031년까지 연평균 성장률(CAGR) 3.9%로 성장할 것으로 전망됩니다.

본 보고서는 유형별(향미료 및 감미료), 가축별(돼지, 반추동물, 기타), 국가별(미국, 캐나다, 멕시코)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(메트릭 톤) 단위로 제시되어 있습니다.

북미의 사료용 향료 및 감미료 시장 동향 및 인사이트

사료 생산량 증가와 사료 공장 규모 확대

산업용 사료의 생산량은 북미의 사료용 향료 및 감미료 시장을 더욱 광범위하고 안정적인 수요 기반으로 이끌고 있습니다. “올텍 사료 조사"에 따르면, 멕시코의 혼합 사료 생산량은 2024년부터 2025년에 걸쳐 2% 증가했으며, 2020년 이후로는 7.7% 확대되어, 멕시코가 돼지 사료 제조 분야에서 실질적인 생산량 증가를 실현하고 있음을 보여줍니다. 또한, 캐나다는 429개의 상업용 사료 공장을 통해 탄탄한 기반을 마련하고 있으며, 연간 2,890만 메트르톤을 처리하고 있습니다. 이러한 규모 덕분에 공장 차원에서 체계적인 첨가제 조달이 가능해졌습니다. 농장에서 직접 사료를 배합하는 대신 상업적 시스템을 통해 사료가 유통되는 비중이 늘어남에 따라, 구매 결정은 더욱 일원화되고 기술적인 성격을 띠게 되고 있습니다. 이는 안정적인 공급 체계, 적용 지원, 그리고 다양한 가축 종에 걸쳐 일관된 공급을 제공할 수 있는 공급업체에게 유리하게 작용합니다. 또한, 제품이 제분 공장의 사양이나 실적 기록에 반영되면, 이미 확립된 프로그램을 대체하기가 어려워집니다. 이러한 운영 구조는 상업용 제분 공장이 대규모로 구매하며, 표준화된 사료 생산에 적합한 첨가물을 요구함에 따라 북미의 사료용 향료 및 감미료 시장의 성장을 지속적으로 뒷받침하고 있습니다.

항생제 감축 프로그램이 사료 섭취 촉진용 첨가제 수요를 끌어올렸습니다.

항생제 감축 프로그램으로 인해 시판 사료에서 향료 및 감미료의 기능적 역할이 커지고 있습니다. 항생제 및 성장 촉진제 사용이 줄어드는 가운데, 생산자들은 사료 섭취량과 일일 체중 증가량을 유지하기 위해 생후 초기 사료의 기호성을 높이는 데 점점 더 의존하고 있습니다. 이는 식욕 저하가 생산 성적이나 건강 상태에 즉각적인 영향을 미칠 수 있는 자돈이나 어린 반추동물의 사육 프로그램에서 특히 중요합니다. 현재, 향미료와 감미료는 단순한 선택적 기능 향상제가 아니라, 사료 섭취량을 유지하기 위한 필수적인 수단으로 인식되고 있습니다. 또한, 대규모 돼지를 대상으로 한 연구를 통해 식물 유래 첨가물 시스템이 돼지의 생산성을 유지하면서 항생제 의존도를 낮출 수 있음이 입증되었으며, 이에 따라 기호성 향상의 중요성이 더욱 부각되고 있습니다. 그 결과, 항생제의 적정 사용은 북미의 사료용 향료·감미료 시장의 주요 성장 동력이 되고 있습니다.

장기화되는 규제 심사 및 원료 승인 절차

규제 심사는 북미의 사료용 향료 및 감미료 시장에서 신제품 시장 확대 속도에 있어 여전히 큰 제약 요인으로 작용하고 있습니다. 동물용으로 개발된 새로운 향미 활성 물질이나 고강도 감미료의 경우, 21 CFR Part 573 및 관련 성분 정의 절차에 따라 승인 절차가 장기화되는 경우가 적지 않습니다. 규정을 준수하려면 제품이 시장에 출시되기 전에 이용 가능한 투자 자금의 상당 부분을 지출해야 하기 때문에 중소기업에 미치는 영향은 특히 큽니다. 이러한 상황은 풍부한 자금력과 전담 규제 대응 팀을 갖춘 대기업에 유리하게 작용하는 경향이 있습니다. 게다가, 인간용 식품 분야의 유사한 발전과 비교했을 때, 새로운 마스킹제나 감미 시스템의 도입이 지연되는 결과로 이어지고 있습니다. 북미의 사료용 향료 및 감미료 시장은 승인된 원료에 의존하고 있으며, 심사 기간이 길어짐에 따라 제품 포트폴리오의 혁신이 저해되고 있어, 이는 여전히 뚜렷한 제약 요인으로 작용하고 있습니다.

부문별 분석

2025년, 북미의 사료용 향료 및 감미료 시장에서 향료는 82.2%를 차지하며 지배적인 위치를 유지했습니다. 이러한 높은 시장 점유율은 반추동물 및 돼지 사료에서 불쾌한 냄새를 가리고 안정적인 사료 섭취를 보장하는 데 필수적이기 때문에 일상적으로 사용되고 있음을 반영하고 있습니다. 향료는 시판되는 사료 배합에 없어서는 안 될 요소이며, 그 수요는 가끔 있는 특수 용도가 아니라 일상적인 배합에서 비롯된 것입니다. 이러한 일관된 사용을 통해 북미의 사료용 향료 및 감미료 시장에서 향료는 표준 배합 사료와 프리미엄 배합 사료 모두에서 핵심 성분으로서의 입지를 확고히 하고 있습니다.

감미료 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 5.8%를 기록하며 향료 시장을 앞지를 것으로 전망됩니다. 이러한 성장 가속화는 특히 생후 초기 사료, 전환기용 사료, 그리고 쓴맛이 나는 생리활성 물질을 함유한 배합에서 사료 섭취량 증진이 극히 중요한 민감한 사료에 있어 감미료의 역할에 기인합니다. 또한, 감미료는 메탄 저감 성분이 함유된 젖소 사료나, 사료의 기호성이 생산 성적에 직접적인 영향을 미치는 자돈 사료에서도 그 중요성이 커지고 있습니다. 그 결과, 향료가 여전히 가장 큰 부문을 차지하고 있는 반면, 감미료는 북미의 사료용 향료 및 감미료 시장에서 주요 성장 동력으로 부상하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the north america feed flavors and sweeteners market was valued at USD 640 million in 2025, projected to be USD 665 million by 2026, and is estimated to reach USD 805.1 million by the end of the forecast period, growing at a CAGR of 3.9% from 2026 to 2031.

This report is Segmented by Type (Flavors and Sweeteners), by Livestock (Swine, Ruminants, and Others), and by Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Feed Flavors and Sweeteners Market Trends and Insights

Higher Compound Feed Throughput and Feed Mill Scale

Industrial feed output continues to drive the North American feed flavors and sweeteners market toward a wider, more stable demand base. According to the Alltech Feed Survey, Mexico's compound feed output increased by 2% from 2024 to 2025 and had expanded by 7.7% since 2020, indicating that the country is adding real volume to swine feed manufacturing. Additionally, Canada also provides a solid base through 429 commercial feed mills that process 28.9 million metric tons annually, and that scale supports organized additive procurement at the mill level. As more feed moves through commercial systems rather than on-farm mixing, purchasing decisions become more centralized and more technical. That favors suppliers that can offer stable delivery forms, application support, and consistent supply across multiple species. It also makes established programs harder to replace once a product is built into mill specifications and performance records. This operating structure continues to support growth in the North America feed flavors and sweeteners market because commercial mills buy at scale and seek additives that fit standardized feed production.

Antibiotic-Reduction Programs Increasing Demand for Intake-Support Additives

Antibiotic reduction programs are enhancing the functional role of flavors and sweeteners in commercial feed. With the reduction of antibiotic growth promoters, producers increasingly rely on improved feed acceptance in early-life diets to maintain intake and daily weight gain. This is particularly critical in nursery swine and young ruminant programs, where reduced appetite can quickly impact performance and health outcomes. Flavors and sweeteners are now viewed as essential tools for supporting feed intake rather than optional enhancements. Additionally, large-scale swine studies have demonstrated that plant-based additive systems can reduce antibiotic dependence while maintaining pig performance, further emphasizing the importance of palatability support. As a result, antibiotic stewardship has become a key driver for the North America feed flavors and sweeteners market.

Lengthy Regulatory Review and Ingredient Approval Pathways

Regulatory review continues to be a significant constraint on the pace at which new products can scale in the North America feed flavors and sweeteners market. Novel flavor actives and high-intensity sweeteners for animal use often face extended approval processes under 21 CFR Part 573 and related ingredient-definition procedures. Smaller companies are disproportionately affected, as regulatory compliance can consume a substantial portion of their available investment before commercial launch. This dynamic tends to favor larger companies with greater financial resources and dedicated regulatory teams. Additionally, it delays the introduction of newer masking and sweetening systems compared to similar advancements in human food. This remains a notable limitation, as the North America feed flavors and sweeteners market relies on approved ingredients, and prolonged review timelines hinder portfolio innovation.

Other drivers and restraints analyzed in the detailed report include:

- Premium Meat, and Dairy Requirements Lifting Palatability Standards

- Clean-Label and Natural Additive Adoption in Premium Feed

- Cost Inflation and ROI (Return on Investment) Scrutiny Among Feed Formulators and Integrators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flavors accounted for 82.2% of the North American feed flavors and sweeteners market in 2025, maintaining a dominant position. This significant share reflects their routine use across ruminant and swine feeds, where they are essential for masking undesirable odors and ensuring consistent feed intake. Flavors are an integral part of commercial feed formulations, with their demand driven by regular inclusion rather than occasional specialty use. This consistent utilization positions flavors as a core component of both standard compound feed and premium formulations in the North American feed flavors and sweeteners market.

Sweeteners are projected to grow at a CAGR of 5.8% from 2026 to 2031, outpacing flavors. This accelerated growth is attributed to their role in sensitive diets where stimulating feed intake is critical, particularly in early-life feeding, transition diets, and formulations containing bitter-tasting bioactives. Sweeteners are also gaining importance in dairy rations that incorporate methane-reduction ingredients and in nursery swine diets, where feed acceptance directly impacts performance. Consequently, while flavors remain the largest segment, sweeteners are emerging as the primary growth driver in the North American feed flavors and sweeteners market.

Complete Report Scope:

- By Type

- Flavors

- Sweeteners

- By Animal

- Swine

- Ruminants

- Dairy Cattle

- Beef Cattle

- Others

- Others

- By Country

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- Cargill, Incorporated

- ADM

- Kemin Industries Inc.

- Alltech

- Adisseo

- Prinova Group LLC

- AFB International

- DSM-Firmenich AG

- Kerry Group

- International Flavors & Fragrances Inc.

- Phytobiotics Futterzusatzstoffe GmbH

- Norel S.A.

- Novonesis

- Canadian Bio-Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Higher compound feed throughput and feed mill scale in the United States, Canada, and Mexico

- 4.2.2 Antibiotic-reduction programs increasing demand for intake-support additives

- 4.2.3 Premium meat, and dairy requirements lifting palatability standards

- 4.2.4 Clean-label and natural additive adoption in premium feed

- 4.2.5 Precision feeding and AI-based intake monitoring improving palatability ROI visibility

- 4.2.6 Taste-masking demand from alternative proteins, by-products, and methane-reduction rations

- 4.3 Market Restraints

- 4.3.1 Lengthy regulatory review and ingredient approval pathways

- 4.3.2 Cost inflation and ROI scrutiny among feed formulators and integrators

- 4.3.3 Ingredient transition uncertainty under evolving FDA and AAFCO frameworks

- 4.3.4 Citrus and molasses input volatility affecting flavor and sweetener economics

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 By Animal

- 5.2.1 Swine

- 5.2.2 Ruminants

- 5.2.2.1 Dairy Cattle

- 5.2.2.2 Beef Cattle

- 5.2.2.3 Others

- 5.2.3 Others

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

- 5.3.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 ADM

- 6.4.3 Kemin Industries Inc.

- 6.4.4 Alltech

- 6.4.5 Adisseo

- 6.4.6 Prinova Group LLC

- 6.4.7 AFB International

- 6.4.8 DSM-Firmenich AG

- 6.4.9 Kerry Group

- 6.4.10 International Flavors & Fragrances Inc.

- 6.4.11 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.12 Norel S.A.

- 6.4.13 Novonesis

- 6.4.14 Canadian Bio-Systems Inc.