|

시장보고서

상품코드

2073331

아프리카의 사료용 향료 및 감미료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Africa Feed Flavors and Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

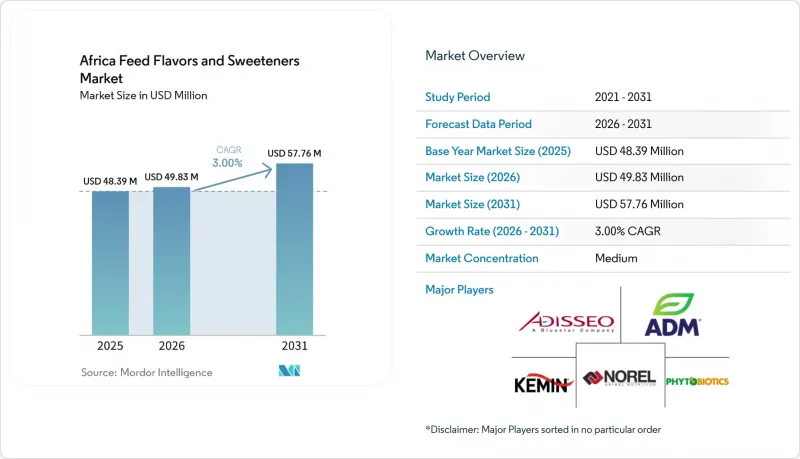

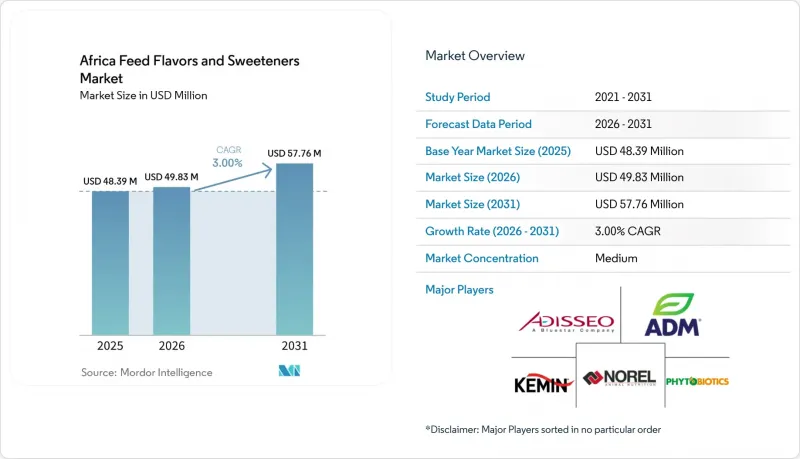

Mordor Intelligence에 의하면, 아프리카의 사료용 향료 및 감미료 시장은 2025년에 4,839만 달러로 평가되었습니다. 2026년 4,983만 달러에서 2031년까지 5,776만 달러로 성장하여 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 3.0%를 나타낼 것으로 예측됩니다.

본 보고서는 부가물(향료 및 감미료), 대상 동물(수산물 양식, 가금류, 반추동물, 돼지, 기타 동물) 및 지역(이집트, 케냐, 남아프리카공화국 및 아프리카의 기타 지역)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

아프리카의 사료용 향료 및 감미료 시장 동향 및 인사이트

가금류 및 유우용 가축 사료의 산업화

아프리카의 가축 사료 생산, 특히 가금류 및 유우용 가축을 위한 사료 생산이 산업화됨에 따라, 기호성 및 사료 섭취량 관리의 중요성이 커지고 있습니다. 미국 농무부(USDA) 해외농업국(FAS)의 2025년 자료에 따르면, 케냐의 혼합사료 총 생산량 중 가금용 사료가 약 41%를 차지했으며, 유우용 사료가 39%의 근소한 차이로 뒤를 이었습니다. 이는 케냐의 조직화된 사료 산업에서 시판되는 배합 사료가 지배적인 위치를 차지하고 있음을 보여줍니다. 사료 제조업체들이 가금류 및 유우용 가축을 위한 표준화된 배합 사료를 점점 더 많이 채택함에 따라, 향료 및 감미료에 대한 수요가 증가하고 있습니다. 이러한 첨가물은 사료의 기호성을 확보하고, 안정적인 섭취를 촉진하며, 펠릿화 및 가공된 사료의 효능을 높이기 위해 필수적입니다. 이러한 시판 사료 제조 동향은 아프리카 전역에서 사료용 향료 및 감미료 시장을 확대시키고 있습니다.

사료 섭취량과 사료 전환율의 최적화에 초점

아프리카의 축산 농가들이 생산 비용을 관리하기 위해 사료 섭취량과 사료 전환 효율을 우선시하는 가운데, 사료용 향료 및 감미료 시장은 급속한 성장을 이루고 있습니다. 미국 농무부 해외농업국은 2025년까지 케냐의 닭고기 생산 총비용 중 사료비가 무려 82%를 차지할 가능성이 있다고 지적하며, 농장의 수익성을 결정하는 데 있어 사료의 성능이 매우 중요한 역할을 하고 있음을 부각시켰습니다. 이러한 상황을 감안하여, 시판되는 배합 사료에 사료용 향료 및 감미료를 첨가하는 추세가 강해지고 있습니다. 이러한 첨가물은 기호성을 높일 뿐만 아니라, 특히 가공 사료나 펠렛 사료의 경우 안정적인 사료 섭취를 촉진합니다. 생산자들이 영양 이용률 향상과 생산 경제성 강화로 이어지는 해결책을 모색하고 있는 만큼, 아프리카 상업 축산 부문의 사료용 향료 및 감미료 수요는 앞으로 더욱 확대될 전망입니다.

비용 중심의 배합 경제성

아프리카의 사료용 향료 및 감미료 시장은 비용 측면을 고려하여 축산 농가들이 사료 배합 시 필수 영양 성분을 특수 첨가물보다 우선시하기 때문에 여러 과제에 직면해 있습니다. 미국 농무부 해외농업국(USDA FAS)에 따르면, 이집트의 옥수수 소비량은 가금류 부문의 회복에 힘입어 2025/26 마케팅 연도에 1,580만 메트르톤에 달했습니다. 상업적 축산에서는 대량의 사료용 곡물이 필요하기 때문에 사료 예산의 대부분은 주요 에너지원이 되는 원료에 배정됩니다. 이러한 추세로 인해 비필수 첨가물에 할당되는 자금이 제한되고 있으며, 특히 사료 비용 절감과 경쟁력 있는 생산 경제성 유지를 목표로 하는 생산자들 사이에서는 사료용 향료나 감미료의 사용이 제한적인 상황입니다.

부문별 분석

2025년 아프리카의 사료용 향료 및 감미료 시장에서 향료 시장 점유율은 94.0%로 가장 높은 비중을 차지하며, 이는 해당 지역 축산 부문에서 기호성 향상 솔루션에 대한 강력한 수요를 반영했습니다. 시장 역학은 반추동물 생산 시스템이 주류를 이루고 있다는 점에 좌우되며, 이 시스템에서는 사료나 배합의 변동과 관계없이 사료의 수용성과 안정적인 섭취량을 확보하는 데 있어 사료용 향미제가 매우 중요한 역할을 하고 있습니다. 상업용 사료 제조업체들은 제품의 일관성을 높이고 가축의 생산성을 향상시키기 위해 배합 사료에 향미제를 첨가하는 비율을 점점 더 늘리고 있습니다. 수요는 특히 체계화된 사료 유통 채널에서 두드러지며, 가축의 생산성에 있어 배합 정확도와 섭취량 관리가 얼마나 중요한지가 강조되고 있습니다.

아프리카의 사료용 향료 및 감미료 시장에서 감미료 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 3.0%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망되며, 사료 생산자들이 더욱 폭넓은 기호성 향상 전략을 모색함에 따라, 이미 성숙기에 접어든 향료 분야를 능가하는 성장이 예상됩니다. 이러한 급증은 축산 생산의 상업화가 진행되고 있는 점과, 특히 생산에 어려움이 있는 단계에서 사료 섭취량의 최적화에 대한 인식이 높아진 데 힘입은 것입니다. 감미료는 어린 동물의 영양 관리 및 특수 사료 분야에서 틈새 시장을 개척하고 있으며, 사료의 기호성을 높이는 역할을 통해 생산 효율 향상에 기여하고 있습니다. 그 보급은 향료에 비해 뒤처져 있지만(이는 주로 아프리카의 많은 축산 시스템이 여전히 기본적인 영양 요구를 중시하기 때문입니다), 사료 제조의 점진적인 현대화가 시장으로의 더 깊은 진출의 길을 열어주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 CEO에 대한 주요 전략적 질문

KTH 26.07.08According to Mordor Intelligence, the africa feed flavors and sweeteners market was valued at USD 48.39 million in 2025 and is projected to grow from USD 49.83 million in 2026 to USD 57.76 million by 2031 at a CAGR of 3.0% from 2026 to 2031.

This report is Segmented by Sub-Additive (Flavors and Sweeteners), by Animal (Aquaculture, Poultry, Ruminants, Swine, and Other Animals), and by Geography (Egypt, Kenya, South Africa, and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Africa Feed Flavors and Sweeteners Market Trends and Insights

Industrialization of Poultry and Dairy Feed

As Africa's livestock feed production industrializes, particularly in poultry and dairy, the importance of palatability and feed intake management is rising. According to the United States Department of Agriculture (USDA) Foreign Agricultural Service (FAS) in 2025, poultry feed made up roughly 41% of Kenya's total compound feed output, with dairy feed close behind at 39%. This underscores the dominance of commercially formulated feed in Kenya's organized feed industry. With feed manufacturers increasingly adopting standardized compound feed for poultry and dairy, there's a growing demand for flavoring and sweetening additives. These additives are crucial for ensuring feed acceptance, promoting consistent intake, and enhancing the efficacy of pelleted and processed rations. This trend towards commercial feed manufacturing is expanding the market for feed flavors and sweeteners throughout Africa.

Feed Intake and Conversion Ratio Optimization Focus

As livestock producers in Africa prioritize feed intake and conversion efficiency to manage production costs, the market for feed flavors and sweeteners is witnessing a surge. The United States Department of Agriculture Foreign Agricultural Service highlights that by 2025, feed costs in Kenya could constitute a staggering 82% of the total expenses in chicken meat production, underscoring the pivotal role of feed performance in determining farm profitability. In light of this, there is a growing trend of integrating feed flavors and sweeteners into commercial formulations. These additives not only boost palatability but also promote steady feed consumption, especially in processed and pelleted diets. With producers on the lookout for solutions that enhance nutrient utilization and bolster production economics, the demand for feed flavors and sweeteners is poised for growth in Africa's commercial livestock sector.

Cost-Sensitive Inclusion Economics

The feed flavors and sweeteners market in Africa encounters challenges as livestock producers prioritize essential nutritional components over specialty additives in feed formulations due to cost considerations. According to the United States Department of Agriculture Foreign Agricultural Service (USDA FAS), Egypt's corn consumption reached 15.8 million metric tons in the 2025/26 marketing year, driven by a recovery in the poultry sector. With commercial livestock production requiring substantial feed grain inputs, a significant portion of feed budgets is allocated to core energy ingredients. This focus restricts the financial resources available for non-essential additives, limiting the adoption of feed flavors and sweeteners, particularly among producers aiming to control feed costs and sustain competitive production economics.

Other drivers and restraints analyzed in the detailed report include:

- Replacement of Antibiotic-Led Performance Tools

- Natural and Phytogenic Palatability Demand

- Substitute Additives and Flavor Masking Workarounds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Africa feed flavors and sweeteners market share for flavors accounted for the largest 94.0% in 2025, reflecting the strong preference for palatability enhancement solutions in the region's livestock sector. The market dynamics are shaped by the prevalence of ruminant production systems, where feed flavors play a pivotal role in ensuring feed acceptance and consistent intake, regardless of forage and ration variations. Commercial feed manufacturers are increasingly infusing flavoring solutions into their compound feeds, aiming to boost product consistency and enhance animal performance. Demand is particularly pronounced in organized feed channels, emphasizing the significance of formulation precision and intake management for livestock productivity.

The Africa feed flavors and sweeteners market size for sweeteners is projected to grow at the fastest CAGR of 3.0% from 2026 to 2031, outpacing the more mature flavor segment as feed producers explore broader palatability strategies. The surge is bolstered by the rising commercialization of livestock production and heightened awareness regarding feed intake optimization, especially during challenging production phases. Sweeteners are carving a niche in young animal nutrition and specialized feed applications, where their role in enhancing feed acceptance can drive production efficiency. While their uptake lags behind flavors-primarily because many African livestock systems still emphasize fundamental nutritional needs-the gradual modernization of feed manufacturing is paving the way for deeper market penetration.

Complete Report Scope:

- By Sub-Additive

- Flavors

- Sweeteners

- By Animal

- Aquaculture

- Fish

- Shrimp

- Other Aquaculture Species

- Poultry

- Broiler

- Layer

- Other Poultry Birds

- Ruminants

- Beef Cattle

- Dairy Cattle

- Other Ruminants

- Swine

- Other Animals

- Aquaculture

- By Geography

- Egypt

- Kenya

- South Africa

- Rest of Africa

List of Companies Covered in this Report:

- Adisseo France SAS (China National BlueStar (Group) Co., Ltd.)

- Archer Daniels Midland Company

- Kemin Industries, Inc.

- Norel, S.A.

- Phytobiotics Futterzusatzstoffe GmbH

- Lucta, S.A.

- Alltech, Inc.

- Innovad NV/SA (Innovad Group)

- Palital Feed Additives B.V. (Arvesta NV)

- Nutreco N.V. (SHV Holdings N.V.)

- dsm-firmenich AG

- Evonik Industries AG

- Cargill, Incorporated

- International Flavors and Fragrances Inc.

- Guilin Layn Natural Ingredients Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 Kenya

- 4.3.3 South Africa

- 4.3.4 Rest of Africa

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Industrialization of poultry and dairy feed

- 4.5.2 Feed intake and conversion ratio optimization focus

- 4.5.3 Replacement of antibiotic-led performance tools

- 4.5.4 Natural and phytogenic palatability demand

- 4.5.5 Heat-stress intake stabilization needs

- 4.5.6 African Continental Free Trade Area (AfCFTA)-led formal feed trade integration

- 4.6 Market Restraints

- 4.6.1 Cost-sensitive inclusion economics

- 4.6.2 Substitute additives and flavor masking workarounds

- 4.6.3 FX-driven import cost inflation

- 4.6.4 Local sweetener and molasses supply unreliability

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Sub-Additive

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 By Animal

- 5.2.1 Aquaculture

- 5.2.1.1 Fish

- 5.2.1.2 Shrimp

- 5.2.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 Broiler

- 5.2.2.2 Layer

- 5.2.2.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 Beef Cattle

- 5.2.3.2 Dairy Cattle

- 5.2.3.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 By Geography

- 5.3.1 Egypt

- 5.3.2 Kenya

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Adisseo France SAS (China National BlueStar (Group) Co., Ltd.)

- 6.4.2 Archer Daniels Midland Company

- 6.4.3 Kemin Industries, Inc.

- 6.4.4 Norel, S.A.

- 6.4.5 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.6 Lucta, S.A.

- 6.4.7 Alltech, Inc.

- 6.4.8 Innovad NV/SA (Innovad Group)

- 6.4.9 Palital Feed Additives B.V. (Arvesta NV)

- 6.4.10 Nutreco N.V. (SHV Holdings N.V.)

- 6.4.11 dsm-firmenich AG

- 6.4.12 Evonik Industries AG

- 6.4.13 Cargill, Incorporated

- 6.4.14 International Flavors and Fragrances Inc.

- 6.4.15 Guilin Layn Natural Ingredients Corp.