|

시장보고서

상품코드

2073389

독일의 하이퍼스케일 데이터센터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2031년)Germany Hyperscale Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

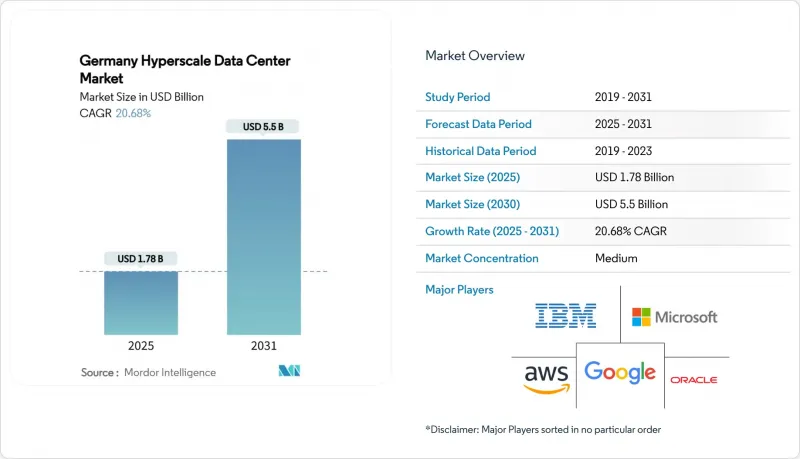

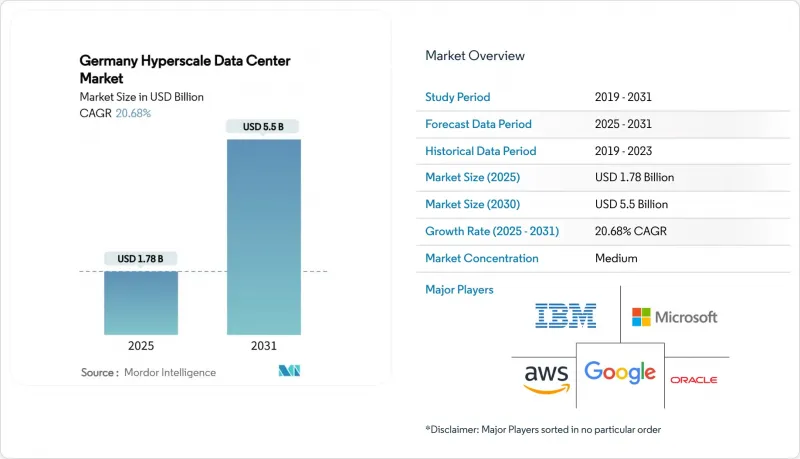

Mordor Intelligence에 의하면, 독일의 하이퍼스케일 데이터센터 시장 규모는 2025년에 17억 8,151만 달러로 평가되었고, 2031년까지 연평균 복합 성장률(CAGR) 20.68%로 55억 328만 달러에 이를 것으로 예측됩니다.

한편, IT 설비 용량은 2025년 2,451.07 MW에서 2031년까지 3,942.78 MW로 연평균 성장률(CAGR) 8.24%를 기록하며 확대될 전망입니다.

본 보고서는 데이터센터의 유형(하이퍼스케일·자체 구축, 하이퍼스케일·코로케이션), 구성 요소(IT 인프라, 전력 인프라 등), 티어 기준(Tier III, Tier IV), 최종 사용자 산업(클라우드 및 IT 서비스, 통신 등), 데이터센터 규모(대규모, 초대규모, 메가), 그리고 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 규모(MW)로 제시되어 있습니다.

독일의 하이퍼스케일 데이터센터 시장 동향 및 인사이트

GPU를 중심으로 한 AI/ML 랙 밀도의 급증(50 kW 이상)

현재 대부분의 AI 훈련 클러스터에서 랙당 전력 소비량이 50 kW를 초과하고 있어, NVIDIA H100 도입 시 공랭식 냉각은 현실적으로 불가능해졌습니다. 마이크로소프트의 32억 유로(37억 3,000만 달러) 규모의 프로그램은 스토리지 중심의 구축 방식에서 직접 투 칩(Direct-to-Chip) 냉각이나 액침 냉각이 필요한 연산 최적화 홀로 전환되고 있음을 여실히 보여주고 있습니다. 각 사업자들은 배전 시스템을 415V 3상 토폴로지로 개조하고 있는 반면, UPS 공급업체들은 GPU의 버스트 부하를 관리하기 위한 고속 응답 모듈을 도입하고 있습니다. Northern Data의 19,000대의 H100 GPU 도입은 AI 전용 시설에 수반되는 설비 투자(Capex)의 프리미엄을 여실히 보여주고 있습니다. 프리미엄 가격대와 밀도 향상은 매출총이익률의 잠재적 확대를 가져오지만, 독일의 하이퍼스케일 데이터센터 시장 전체에 걸쳐 엔지니어링의 복잡성을 가중시키고 있습니다.

소버린 클라우드의 규정 준수(GDPR(EU 개인정보보호규정), BSI C5) 체계가 점차 정비되고 있습니다.

독일의 디지털 주권 의제에 따라, 공공 부문의 워크로드에 대해 BSI C5 인증 및 데이터 거주성 보증이 의무화되어 있습니다. Google Cloud를 기반으로 하는 T-Systems의 “Sovereign Cloud"는 규정 준수를 위한 설비 투자가 어떻게 경쟁 우위로 작용하는지를 보여주고 있습니다. NIS-2의 시행에 따라 사이버 복원력에 관한 의무가 수천 개의 사업자로 확대되었으며, 운영상의 점검 항목이 더욱 엄격해졌습니다. 인증 획득에 따른 부하로 인해 프로젝트 일정이 길어지기는 하지만, 규정 준수를 충족하는 사이트는 더 높은 수익률을 확보할 수 있기 때문에 독일의 하이퍼스케일 데이터센터 시장에서 규정 준수가 수요를 견인하는 요인으로 자리 잡아가고 있습니다.

증발 냉각 시 물 사용량의 상한

EU의 지속가능성 규정에 따라 물 사용량 공개가 의무화됨에 따라, 대규모 시설의 경우 하루 500만 갤런에 달하는 일일 소비량이 주목받고 있습니다. DENEFF의 조사에 따르면, 사업자의 56%가 열 재이용에 대한 수요가 낮다고 인식하고 있어, 물과 열 효율의 시너지 효과가 제한되고 있습니다. 도시 지역의 물 사용 상한선으로 인해 허용 취수량이 더욱 엄격해짐에 따라, 사업자들은 초기 비용이 많이 들고 운영상의 장벽도 높은 폐쇄형 루프 단열식 또는 액체 냉각 시스템으로의 전환을 강요받고 있으며, 이것이 독일의 하이퍼스케일 데이터센터 시장에서 주요 과제로 대두되고 있습니다.

부문별 분석

2024년에는 하이퍼스케일 코로케이션이 매출의 52%를 차지했으며, 이는 턴키 방식을 통해 장애 복원력을 추구하는 기업들의 경향이 정착되고 있음을 반영하고 있습니다. 그러나 독일의 하이퍼스케일 데이터센터 시장에서는 현재 주요 클라우드 기업들이 AI 및 주권 워크로드를 위한 아키텍처 통제권을 요구하는 가운데, 하이퍼스케일러들의 자체 건설이 연평균 성장률(CAGR) 12.8%를 나타낼 것으로 전망됩니다. AWS, 마이크로소프트, Oracle이 맞춤형 캠퍼스에 수십억 규모의 예산을 투자함에 따라, 가속화되는 프로젝트 파이프라인이 독일의 하이퍼스케일 데이터센터 시장을 견인하고 있습니다.

당사의 자체 건설 시설에는 직접-투-칩 냉각, 400G 패브릭, 그리고 코로케이션 시설에서는 사전 설치되는 경우가 드문 맞춤형 전원 경로가 통합되어 있습니다. 이에 대해 콜로케이션 분야의 기존 사업자들은 맞춤형 모듈, 주권 클라우드 엔클레이브, 그리고 유연한 토지 보유 방식을 통해 대응하고 있습니다. 이 두 가지 성장 궤적 덕분에 수요 변동이 완화되면서, 독일의 하이퍼스케일 데이터센터 업계 전반에 걸쳐 서비스 메뉴가 확대되고 있습니다.

IT 인프라는 2024년 매출의 41.2%를 차지하며, GPU 서버 클러스터가 스토리지 중심의 랙을 대체함에 따라 연평균 성장률(CAGR) 14.6%로 해당 부문의 성장을 주도했습니다. 트레이닝 워크로드가 설비 투자(CAPEX)의 대부분을 차지하는 가운데, 독일의 하이퍼스케일 데이터센터 시장에서 서버 노드 시장 규모는 칠러나 발전기를 웃돌고 있습니다.

전기 기기 역시 이에 뒤이어 있습니다. 415 V 버스웨이, 고속 전송 개폐 장치, 리튬 이온 UPS 유닛은 랙 밀도가 높아짐에 따라 수요가 증가하고 있습니다. 기계 설비에 대한 투자는 액체 루프나 리어 도어식 열교환기로 점차 전환되고 있지만, 저밀도 홀에서는 여전히 기존의 냉수 플랜트가 주를 이루고 있습니다. 부품 구성표(BOM)의 발전에 따라 독일의 하이퍼스케일 데이터센터 시장에서 프로젝트의 평균 가치가 상승하는 한편, 공급업체의 전문화도 더욱 심화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 하이퍼스케일 데이터센터 인공지능(AI) 도입(하위 부문은 데이터 최신 상황에 의해 변경되는 경우가 있습니다)

제6장 규제 및 컴플라이언스 프레임워크

제7장 데이터센터 주요 통계

제8장 시장 규모 및 성장 예측

제9장 경쟁 구도

제10장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the germany hyperscale data center market size stands at USD 1,781.51 million in 2025 and is projected to reach USD 5,503.28 million by 2031 at a 20.68% CAGR, while installed IT capacity is set to expand from 2,451.07 MW in 2025 to 3,942.78 MW by 2031 at an 8.24% CAGR.

This report is Segmented by Data Center Type (Hyperscale Self-Build, Hyperscale Colocation), Component (IT Infrastructure, Electrical Infrastructure, and More), Tier Standard (Tier III, Tier IV), End-User Industry (Cloud and IT Services, Telecom, and More), Data Center Size (Large, Massive, Mega), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (MW).

Germany Hyperscale Data Center Market Trends and Insights

Surging GPU-centric AI/ML rack densities ( Greater than 50 kW)

Rack power envelopes now exceed 50 kW in most AI training clusters, rendering air cooling impractical for NVIDIA H100 deployments. Microsoft's EUR 3.2 billion (USD 3.73 billion) programme underscores the pivot from storage-heavy builds to compute-optimized halls that demand direct-to-chip or immersion cooling. Operators are retrofitting distribution to 415 V three-phase topologies, while UPS vendors introduce fast-response modules to manage GPU burst loads. Northern Data's roll-out of 19,000 H100 GPUs exemplifies the capex premium attached to AI-ready halls Premium price points and density gains widen gross-margin potential but raise engineering complexity across the Germany hyperscale data center market.

Sovereign-cloud compliance (GDPR, BSI C5) builds

Germany's digital-sovereignty agenda makes BSI C5 attestation and data-residency guarantees compulsory for public-sector workloads. T-Systems' Sovereign Cloud powered by Google Cloud shows how compliance capital spend turns into a competitive moat NIS-2 implementation expands cyber-resilience obligations to thousands of operators, tightening operational checkpoints. Certification overheads lengthen project schedules but let compliant sites command higher yields, cementing compliance as a demand driver within the Germany hyperscale data center market.

Water-use caps on evaporative cooling

EU sustainability rules now compel water-use disclosure, spotlighting daily consumption that can hit 5 million gallons at large sites DENEFF's survey shows 56% of operators see weak demand for heat-reuse, limiting synergy between water and thermal efficiency. Urban water caps tighten allowable draw, pushing operators toward closed-loop adiabatic or liquid systems that cost more upfront and lift the operational hurdle in the Germany hyperscale data center market.

Other drivers and restraints analyzed in the detailed report include:

- Real-time payment and CBDC latency mandates

- 5G edge-core consolidation around metro hubs

- GPU/optics supply-chain shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hyperscale colocation controlled 52% revenue in 2024, reflecting entrenched enterprise preference for turnkey resilience. However, the Germany hyperscale data center market now sees hyperscaler self-builds expanding at 12.8% CAGR as cloud majors seek architectural control for AI and sovereignty workloads. The accelerating pipeline lifts the Germany hyperscale data center market as AWS, Microsoft, and Oracle commit multibillion budgets to bespoke campuses.

Self-builds embed direct-to-chip cooling, 400 G fabric and custom power paths that colocation shells seldom pre-install. Colocation incumbents respond with build-to-suit modules, sovereign-cloud enclaves and flexible land banks. This two-track growth cushions demand volatility and broadens service menus across the Germany hyperscale data center industry.

IT infrastructure delivered 41.2% of 2024 revenue, leading segment growth at 14.6% CAGR as GPU server clusters displace storage-centric racks. The Germany hyperscale data center market size for server nodes outpaces chillers and generators as training workloads dominate capex.

Electrical gear follows closely: 415 V busways, fast-transfer switchgear and lithium-ion UPS units rise in tandem with rack density. Mechanical spend migrates toward liquid loops and rear-door exchangers, though legacy chilled-water plants still underpin lower-density halls. The evolving bill-of-materials lifts average project value in the Germany hyperscale data center market while deepening vendor specialization.

Complete Report Scope:

- By Data Center Type

- Hyperscale Self-Build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Unit

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning

- Design and Engineering

- Fire Detection and Physical Security

- DCIM/BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT Services

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End User

- By Data Center Size

- Large (Less than equal to 25 MW)

- Massive (Greater than 25 MW and less than equal to 60 MW)

- Mega (Greater than 60 MW)

- By Geography

- Frankfurt / Rhein-Main

- Berlin / Brandenburg

- Munich / Bavaria

- Hamburg / North

- NRW (Dusseldorf-Cologne)

List of Companies Covered in this Report:

- Amazon Web Services

- Microsoft Corporation

- Alphabet Inc. (Google)

- Meta Platforms Inc.

- Oracle Corporation

- International Business Machines Corp.

- Alibaba Group Holding Ltd.

- Tencent Holdings Ltd.

- Baidu Inc.

- Digital Realty (Interxion)

- Equinix Inc.

- NTT Global Data Centers (e-Shelter)

- CyrusOne Inc.

- Vantage Data Centers

- Quality Technology Services (QTS)

- STACK Infrastructure

- Iron Mountain Data Centers

- Maincubes One GmbH

- Hetzner Online GmbH

- OVHcloud

- Data4 Group

- GDS Holdings Ltd.

- CoreWeave Inc.

- Flexential Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging GPU-centric AI/ML rack densities (>50 kW)

- 4.2.2 Sovereign-cloud compliance (GDPR, BSI C5) builds

- 4.2.3 Real-time payment and CBDC latency mandates

- 4.2.4 5G edge-core consolidation around metro hubs

- 4.2.5 GenAI inference clusters needing liquid cooling

- 4.2.6 Availability-based renewable PPAs for capacity hedge

- 4.3 Market Restraints

- 4.3.1 Water-use caps on evaporative cooling

- 4.3.2 GPU/optics supply-chain shortages

- 4.3.3 Heat-reuse mandate increasing CapEx (draft law)

- 4.3.4 Grid-connection curtailment greater than 30 MW in Tier-2 cities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

5 ARTIFICIAL INTELLIGENCE (AI) INCLUSION IN HYPERSCALE DATA CENTER (Sub-segments are subject to change depending on Data Recency)

- 5.1 AI Workload Impact: Rise of GPU-Packed Racks and High Thermal Load Management

- 5.2 Rapid Shift toward 400G and 800G Ethernet - Local OEM Integration and Compatibility Demands

- 5.3 Innovations in Liquid Cooling: Immersion and Cold Plate Trends

- 5.4 AI-Based Data Center Management (DCIM) Adoption - Role of Cloud Providers

6 REGULATORY AND COMPLIANCE FRAMEWORK

7 KEY DATA CENTER STATISTICS

- 7.1 Existing Hyperscale Data Center Facilities in Germany (in MW) (Hyperscale Self build VS Colocation)

- 7.2 List of Upcoming Hyperscale Data Center in Germany

- 7.3 List of Hyperscale Data Center Operators in Germany

- 7.4 Analysis on Data Center CAPEX in Germany

8 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 8.1 By Data Center Type

- 8.1.1 Hyperscale Self-Build

- 8.1.2 Hyperscale Colocation

- 8.2 By Component

- 8.2.1 IT Infrastructure

- 8.2.1.1 Server Infrastructure

- 8.2.1.2 Storage Infrastructure

- 8.2.1.3 Network Infrastructure

- 8.2.2 Electrical Infrastructure

- 8.2.2.1 Power Distribution Unit

- 8.2.2.2 Transfer Switches and Switchgears

- 8.2.2.3 UPS Systems

- 8.2.2.4 Generators

- 8.2.2.5 Other Electrical Infrastructure

- 8.2.3 Mechanical Infrastructure

- 8.2.3.1 Cooling Systems

- 8.2.3.2 Racks

- 8.2.3.3 Other Mechanical Infrastructure

- 8.2.4 General Construction

- 8.2.4.1 Core and Shell Development

- 8.2.4.2 Installation and Commissioning

- 8.2.4.3 Design and Engineering

- 8.2.4.4 Fire Detection and Physical Security

- 8.2.4.5 DCIM/BMS Solutions

- 8.2.1 IT Infrastructure

- 8.3 By Tier Standard

- 8.3.1 Tier III

- 8.3.2 Tier IV

- 8.4 By End-User Industry

- 8.4.1 Cloud and IT Services

- 8.4.2 Telecom

- 8.4.3 Media and Entertainment

- 8.4.4 Government

- 8.4.5 BFSI

- 8.4.6 Manufacturing

- 8.4.7 E-Commerce

- 8.4.8 Other End User

- 8.5 By Data Center Size

- 8.5.1 Large (Less than equal to 25 MW)

- 8.5.2 Massive (Greater than 25 MW and less than equal to 60 MW)

- 8.5.3 Mega (Greater than 60 MW)

- 8.6 By Geography

- 8.6.1 Frankfurt / Rhein-Main

- 8.6.2 Berlin / Brandenburg

- 8.6.3 Munich / Bavaria

- 8.6.4 Hamburg / North

- 8.6.5 NRW (Dusseldorf-Cologne)

9 COMPETITIVE LANDSCAPE

- 9.1 Market Share Analysis

- 9.2 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 9.2.1 Amazon Web Services

- 9.2.2 Microsoft Corporation

- 9.2.3 Alphabet Inc. (Google)

- 9.2.4 Meta Platforms Inc.

- 9.2.5 Oracle Corporation

- 9.2.6 International Business Machines Corp.

- 9.2.7 Alibaba Group Holding Ltd.

- 9.2.8 Tencent Holdings Ltd.

- 9.2.9 Baidu Inc.

- 9.2.10 Digital Realty (Interxion)

- 9.2.11 Equinix Inc.

- 9.2.12 NTT Global Data Centers (e-Shelter)

- 9.2.13 CyrusOne Inc.

- 9.2.14 Vantage Data Centers

- 9.2.15 Quality Technology Services (QTS)

- 9.2.16 STACK Infrastructure

- 9.2.17 Iron Mountain Data Centers

- 9.2.18 Maincubes One GmbH

- 9.2.19 Hetzner Online GmbH

- 9.2.20 OVHcloud

- 9.2.21 Data4 Group

- 9.2.22 GDS Holdings Ltd.

- 9.2.23 CoreWeave Inc.

- 9.2.24 Flexential Corp.

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-Space and Unmet-Need Assessment