|

시장보고서

상품코드

2073601

베트남의 특수 비료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vietnam Specialty Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

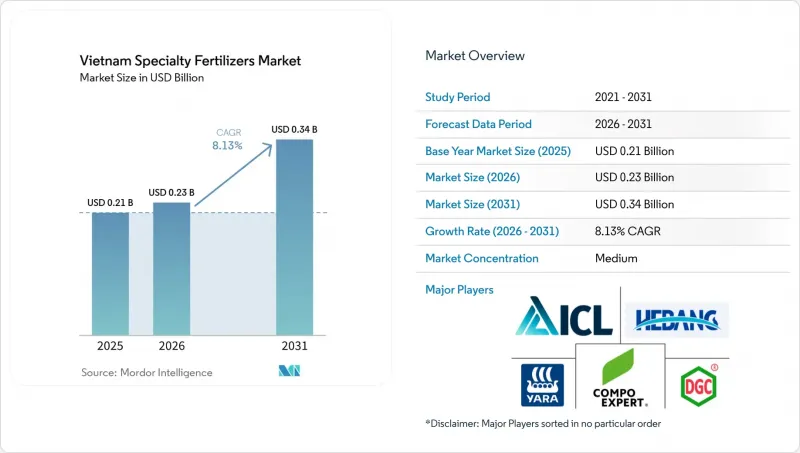

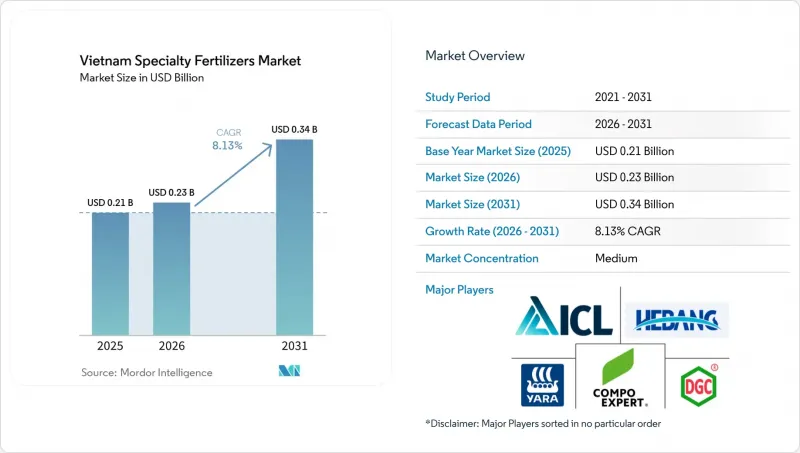

Mordor Intelligence에 의하면, 베트남 특수 비료 시장 규모는 2025년에 2억 1,000만 달러로 평가되었고 2026년 2억 3,000만 달러에서 2031년까지 3억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.13%를 나타낼 전망입니다.

본 보고서는 특수 비료의 유형(CRF, 액체 비료, SRF, 수용성 비료), 시비 방법(시비 관개, 엽면 시비, 토양 시비), 작물의 유형(밭작물, 원예작물, 잔디 및 관상용 작물)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

베트남 특수 비료 시장 동향과 인사이트

정밀 농업의 도입이 효율적인 투입 자재에 대한 수요를 촉진하고 있습니다.

2024년에는 5만 헥타르의 논에서 드론을 이용한 비료 살포가 실시되었으며, 디지털 토양 지도를 활용한 가변 비료 살포율을 통해 양분 비용을 최대 25% 절감했습니다. 특수 액체 비료는 균일하게 용해되기 때문에 호퍼 막힘을 방지할 수 있으며, 이를 통해 드론이 분진이 적은 자재에만 한정된다는 제약이 해소되었습니다. 야라 인터내셔널은 펩시코와 제휴하여 1,200헥타르 규모의 계약 감자 농장에서 2024년에 수확량을 15% 늘리고, 질소 유출을 30% 줄였습니다. 정부는 2030년까지 100만 헥타르의 논을 “습건 교대 관개”로 전환할 계획이며, 이 시스템에서는 관개 일정에 맞춘 서방형 질소 비료가 필요합니다. 토양 매핑 프로그램은 이미 250만 헥타르를 포괄하고 있으며, 농업 관련 기업에 고품질 복합 비료의 효과를 입증하는 영양 결핍 데이터를 제공합니다. 대부분의 농장 면적이 1헥타르 미만이며, 자본 집약적 기술 도입에 있어 협동조합 모델에 의존하고 있기 때문에 도입은 단계적으로 확대될 전망입니다.

정부의 부가가치세(VAT) 인하로 국내 생산자의 이익률이 개선되었습니다.

2025년 7월부터 기존의 10% 부가가치세가 5%로 인하됨에 따라, 수입품의 입고 비용 측면에서 가졌던 경쟁 우위가 약 5퍼센트 포인트 축소되면서 현지 기업들은 전문 분야에 대한 투자에 집중할 수 있게 되었습니다. 국내 비료 생산 능력은 800만 메트르톤 정도인 반면, 수요는 1,100만 메트르톤을 초과하고 있어 수입은 계속될 전망이지만, 국내 제조업체들은 현재 가격 책정 여지가 확대되고 있습니다. 페트로베트남 카마우사는 2025년 설비 투자액의 15%를 폴리머 코팅 NPK에 할당하고, 80만 메트르톤 규모의 요소 생산 기반을 활용하여 밸류체인의 업스트림 부문으로의 진출을 모색하고 있습니다. 경영진은 2027년까지 특수 제품의 생산량이 10-15% 증가할 것으로 전망하고 있습니다. 단기 일정은 즉각적인 세금 부담 경감을 반영한 것이지만, 새로운 라인의 설계 및 시운전에는 최대 2년이 소요됩니다.

변동이 심한 천연가스 원료 비용

암모니아 가격은 2022년 톤당 700달러 이상에서 2024년에는 톤당 300-400달러까지 하락하며, 요소의 이익률이 세계 가스 가격 변동에 얼마나 민감한지를 여실히 보여주었습니다. 페트로베트남 카마우사는 해상 가스전에 의존하고 있지만, 그 생산량은 2020년 이후 매년 3-5%씩 감소하고 있어 이를 보완하기 위해 수입에 의존할 수밖에 없는 상황입니다. 원자재 비용이 급등하면, 생산자는 비용에 민감한 농가에게 가격 인상을 전가할 수 없는 경우, 수익성을 확보하기 어려운 특수 제품의 설비 현대화에 대한 투자를 주저하게 됩니다. 중국산 수입 가격이 1메트릭톤당 314달러 전후로 형성되고 있는 것은 국내 공급업체들이 주시해야 할 가격 상한선입니다. 단기적인 일정은 가격 충격 발생 시 당면한 압박을 여실히 드러내고 있지만, 헤지나 제품 구성 변경을 통해 그 타격을 완화하는 것은 가능합니다.

부문별 분석

2025년, 베트남의 고기능성 비료 시장에서 액체 비료는 49.2%의 점유율을 차지했습니다. 이는 비료와 관개를 통해 150-200ppm 농도의 영양분이 공급되는 온실 채소 재배가 주도한 결과입니다. 달랏의 수경 재배 농가들은 고급 샐러드용 잎채소의 대부분을 공급하고 있으며, 상당한 절수 효과를 보고하고 있습니다. 이로 인해 액체 비료가 표준적인 시비 방법으로 자리 잡았습니다. 콜드체인 인프라가 제한적이기 때문에 도시 외곽 지역으로의 유통은 제한되고 있습니다. 빈디엔사가 조만간 출시할 예정인 수용성 과립 비료는 상온에서 보관할 수 있으며, 커피와 후추 농장을 대상으로 한 대체 제품이 될 것입니다.

방출 조절 비료 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 4.3%로 성장할 것으로 전망됩니다. 페트로베트남 카마우사의 잉여 요소를 활용하여 질소 방출 기간을 연장하는 폴리머 코팅 제품이 개발되었으며, 이는 커피와 용과 재배 주기에 적합합니다. 바이오차·폴리우레탄 코팅은 침출을 줄여주며, 점점 더 엄격해지는 유기물 함유 기준에도 부합합니다. 수용성 제품은 시장 점유율 면에서는 액체 제품에 뒤처지고 있지만, 점적 관개 시스템을 통해 노동력이 대폭 절감되는 커피나 후추 농장에서는 보급이 확대되고 있습니다. 서방형 유황 코팅 과립은 호우로 인해 영양분의 방출이 불균일해질 가능성이 있기 때문에 보급 속도는 비교적 완만합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 개 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO가 직면하는 중요 전략적 과제

JHS 26.07.09According to Mordor Intelligence, the vietnam specialty fertilizers market size was valued at USD 0.21 billion in 2025 and estimated to grow from USD 0.23 billion in 2026 to reach USD 0.34 billion by 2031, at a CAGR of 8.13% during the forecast period (2026-2031).

This report is Segmented by Specialty Type (CRF, Liquid Fertilizer, SRF, and Water-Soluble), Application Mode (Fertigation, Foliar, and Soil) and Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Vietnam Specialty Fertilizers Market Trends and Insights

Precision-Farming Adoption Boosts Demand for Efficient Inputs

Drone application covered 50,000 hectares of rice in 2024, reducing nutrient costs by up to 25% through variable-rate dosing that relies on digital soil maps. Specialty liquids dissolve evenly and avoid the hopper clogging that restricts drones to low-dust materials. Yara International partnered with PepsiCo on 1,200 hectares of contract potato farms, raising yields 15% and cutting nitrogen runoff 30% in 2024. The government plans to shift 1 million hectares of rice to alternate wetting and drying irrigation by 2030, a system that requires slow-release nitrogen to match water schedules. Soil-mapping programs already cover 2.5 million hectares, equipping agribusinesses with deficiency data that validate premium blends. Adoption will scale in phases because most farms remain below one hectare and depend on cooperative models for capital-intensive technology.

Government VAT Cut Improves Domestic Producer Margins

From July 2025, a 5% VAT replaced the prior 10% rate, shrinking the landed-cost advantage of imports by roughly five percentage points and freeing up local firms to pursue specialty investments. National fertilizer capacity stands near 8 million metric tons compared with demand above 11 million metric tons, so imports will still flow, yet domestic manufacturers now enjoy higher pricing headroom. PetroVietnam Ca Mau earmarked 15% of 2025 capital expenditure for polymer-coated NPK, leveraging its 800,000 metric tons urea base to climb the value chain. Management expects specialty output to rise 10-15% by 2027. The near-term timeline reflects immediate tax savings, while engineering and commissioning of new lines require up to two years.

Volatile Natural-Gas Feedstock Costs

Ammonia prices fell from over USD 700 per metric ton in 2022 to USD 300-400 per metric ton in 2024, underscoring the sensitivity of urea margins to global gas swings. PetroVietnam Ca Mau relies on offshore gas fields whose output has slipped 3-5% each year since 2020, forcing supplemental imports. When feedstock costs spike, producers hesitate to fund specialty upgrades that could turn uneconomic if pricing cannot be passed along to cost-conscious farmers. Imports priced near USD 314 per metric ton from China set a ceiling that domestic suppliers must watch. The short-term timeline highlights immediate pressure during price shocks, although hedging and product-mix shifts can soften the blow.

Other drivers and restraints analyzed in the detailed report include:

- High-Value Crop Export Expansion in Coffee and Pepper

- Rapid Growth of Greenhouse Vegetable Acreage

- Farmer Price Sensitivity Toward Premium Inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid fertilizers accounted for 49.2% of the Vietnam specialty fertilizers market share in 2025, anchored by greenhouse vegetables, where fertigation delivers nutrients at 150-200 parts per million. Hydroponic growers in Da Lat supply a large share of premium salad greens and report considerable water savings, cementing liquids as the default feed. Limited cold chain infrastructure narrows distribution outside urban zones. Binh Dien's upcoming launch of water-soluble granules offers an alternative that can be stored at ambient temperatures and targets coffee and pepper farms.

Controlled-release fertilizers are anticipated to grow at a CAGR of 4.3% from 2026 to 2031. PetroVietnam Ca Mau's surplus urea enables polymer-coated lines that extend nitrogen release, aligning with coffee and dragon-fruit cycles. Biochar-polyurethane coatings reduce leaching and meet rising organic content rules. Water-soluble products trail liquids in market share but are gaining traction across coffee and pepper farms, where drip systems significantly cut labor. Slow-release sulfur-coated granules grow more slowly because heavy rainfall can trigger uneven nutrient pulses.

Complete Report Scope:

- Speciality Type

- CRF

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Liquid Fertilizer

- SRF

- Water Soluble

- CRF

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

List of Companies Covered in this Report:

- PVFCCo (PetroVietnam - Vietnam Oil and Gas Group)

- PetroVietnam Ca Mau Fertilizer - DCM

- Baconco (Hebang Biotechnology Co. Ltd.)

- Binh Dien Fertilizer

- Yara International ASA

- Duc Giang Chemicals Group

- Kingenta Ecological Engineering

- Vietnam National Chemical Group

- Song Gianh Corporation

- Grupa Azoty S.A. (Compo Expert)

- Haifa Group

- Nutrien Ltd.

- ICL Group Ltd.

- Hebei Sanyuanjiuqi Fertilizer Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-farming adoption boosts demand for efficient inputs

- 4.6.2 Government VAT change (5 %) improves domestic producer margins

- 4.6.3 High-value crop export expansion

- 4.6.4 Rapid growth of greenhouse vegetable acreage

- 4.6.5 Surplus urea capacity enables coated-urea value-added lines

- 4.6.6 Dutch manure-granulate imports accelerate organic blends

- 4.7 Market Restraints

- 4.7.1 Volatile natural-gas feedstock costs

- 4.7.2 Farmer price-sensitivity toward premium inputs

- 4.7.3 Proliferation of counterfeit / sub-standard products

- 4.7.4 Limited cold-chain for microbial and liquid specialties

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 PVFCCo (PetroVietnam - Vietnam Oil and Gas Group)

- 6.4.2 PetroVietnam Ca Mau Fertilizer - DCM

- 6.4.3 Baconco (Hebang Biotechnology Co. Ltd.)

- 6.4.4 Binh Dien Fertilizer

- 6.4.5 Yara International ASA

- 6.4.6 Duc Giang Chemicals Group

- 6.4.7 Kingenta Ecological Engineering

- 6.4.8 Vietnam National Chemical Group

- 6.4.9 Song Gianh Corporation

- 6.4.10 Grupa Azoty S.A. (Compo Expert)

- 6.4.11 Haifa Group

- 6.4.12 Nutrien Ltd.

- 6.4.13 ICL Group Ltd.

- 6.4.14 Hebei Sanyuanjiuqi Fertilizer Co. Ltd.