|

시장보고서

상품코드

2073614

남미의 특수 비료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

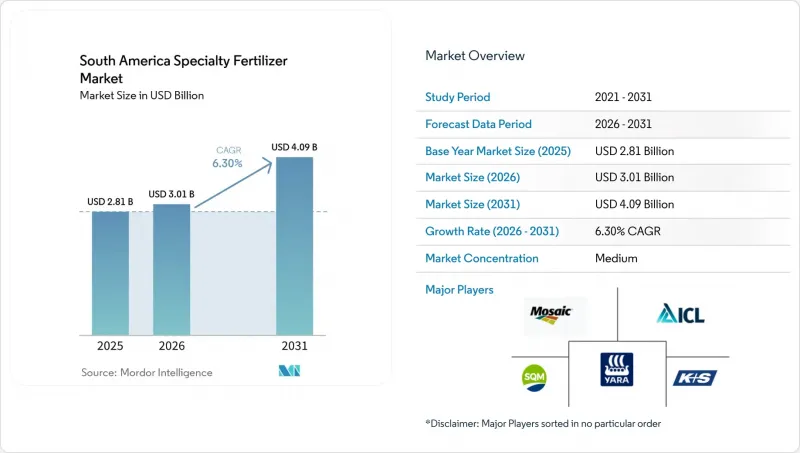

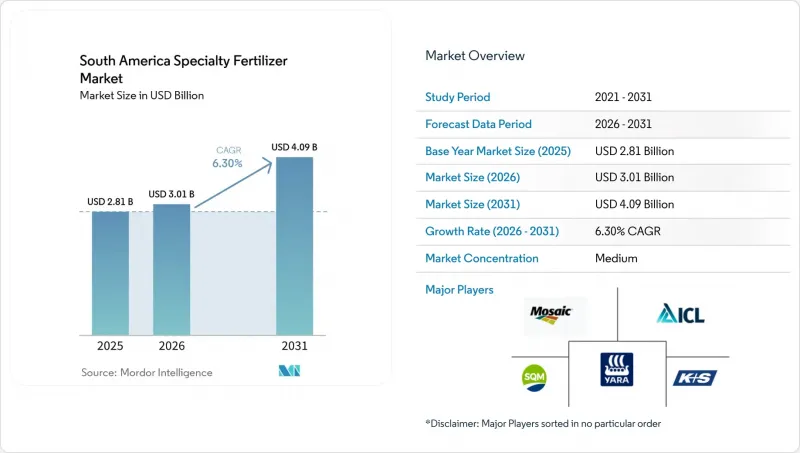

Mordor Intelligence에 의하면, 남미 특수 비료 시장 규모는 2025년에 28억 1,000만 달러로 평가되었고 2026년 30억 1,000만 달러에서 2031년까지 40억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.30%를 나타낼 전망입니다.

본 보고서는 특수 비료의 유형(CRF, 액체 비료, SRF, 수용성 비료), 시용 방법(비료 관개, 엽면 시비, 토양 시비), 작물의 유형(밭작물, 원예작물, 잔디 및 관상용 작물), 그리고 국가(아르헨티나, 브라질, 기타 남미 국가)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

남미 특수 비료 시장 동향과 인사이트

점적 관개 면적의 급증

브라질의 관개 면적은 2019년부터 2024년까지 12% 확대되어 820만 헥타르에 달했습니다. 그중에서도 점적 관개 시스템 시장 점유율이 가장 빠르게 증가하고 있습니다. 점적 관개 기술에서는 완전히 수용성인 비료가 필요하기 때문에 에미터의 막힘을 방지하고 작물 수요에 맞추어 영양분을 공급하기 위해서는 특수 비료가 필수적입니다. 아르헨티나에서는 주로 멘도사의 포도밭과 북부의 감귤류 과수원에서 180만 헥타르가 추가되면서, 액체 및 수용성 비료의 도입이 더욱 확대되었습니다. 지역 농업 기계 제조업체들은 연간 15-20%의 매출 성장을 기록하고 있으며, 정밀 관개와 비료 기술 혁신 간의 선순환이 강화되고 있습니다. 수확량 데이터에 따르면, 수용성 NPK와 미량 원소 킬레이트를 조합한 비료 시비 및 관개를 통해 8-10%의 수확량 증가가 확인되었으며, 상품 가격 변동이 심한 상황에서도 투자의 유효성이 입증되었습니다. 현지 농업 서비스 제공업체들은 현재 관개 키트와 비료 시비 조언을 세트로 제공함으로써 농가들의 학습 곡선을 가속화하고 있습니다. 파라과이와 우루과이에서 점적 관개가 보급됨에 따라 수용성 복합비료에 대한 국경을 초월한 수요가 증가하고 있으며, 남미의 특수 비료 시장의 잠재 고객 기반이 확대되고 있습니다.

고효율 비료에 대한 정부의 세제 혜택

브라질에서는 2024년 세제 개혁에 따라 서서히 방출되는 비료 및 지연형 비료에 대한 PIS/COFINS 세율이 9.25%에서 3.65%로 인하되어 소매 가격이 약 6% 하락했습니다. 아르헨티나도 이에 발맞추어 폴리머 코팅 요소 및 생장 촉진제 첨가제의 수입 관세를 인하하여, ISO 14001 인증에 따른 환급 조치와 일치시켰습니다. 초기 시장 데이터에 따르면, 출시 후 불과 6개월 만에 방출 조절 비료의 출하량이 23% 증가했습니다. 이 정책은 환경 보전과 수익성 간의 연계성을 강화하여, 고부가가치 원예 분야에 그치지 않고 광대한 농지에서 대두, 옥수수, 면화 시장으로의 진출을 가속화하고 있습니다. 현지 블렌딩 업체들은 전환 기간 동안의 재고 크레딧을 활용하여 제품 포트폴리오를 급속히 코팅 제품으로 전환했습니다. 2026년에 세제상의 우대 조치가 종료됨에 따라, 각 제조업체는 이미 입증된 수확량 증가와 헥타르당 인건비 절감을 바탕으로 수요의 지속성을 기대하고 있습니다. 인접 국가 정부들도 브라질의 모델을 주시하고 있으며, 남미의 특수 비료 시장 경제 전반에 걸쳐 더 광범위한 인센티브의 물결이 밀려올 조짐이 보입니다.

범용 비료에 드는 높은 초기 비용

특수 비료는 기존의 NPK 비료에 비해 25-40% 더 비싸게 판매되고 있어, 농업 경영체의 77%를 차지하는 브라질의 390만 소규모 농가에게 장벽이 되고 있습니다. 농산물 가격이 하락하면 생산자들은 더 저렴한 대량 비료로 다시 돌아서게 됩니다. 아르헨티나에서는 많은 농업 자재가 달러로 거래되기 때문에 페소 약세가 가격 격차를 더욱 확대시키고 있습니다. 유통업체들은 계절별 신용 대출 상품이나 곡물 물물교환 프로그램을 통해 대응하고 있지만, 상환 위험으로 인해 금리는 여전히 높은 수준을 유지하고 있습니다. 비용 분담에 대한 인센티브가 없기 때문에 노동력이 풍부하고 수확량 증가 여지가 제한적인 지역에서는 도입이 더딘 실정입니다. 정부의 바우처 제도는 여전히 시범적인 규모에 그치고 있어, 단기적인 구제 효과는 제한적입니다. 그 결과, 가격에 대한 민감도로 인해 향후 2년간 남미의 특수 비료 시장 연평균 성장률(CAGR) 전망치는 약 1.8% 하락할 것으로 예측됩니다.

부문별 분석

2025년, 남미의 특수 비료 시장에서 액체 비료는 36.6%라는 압도적인 점유율을 차지했습니다. 이는 감귤류, 커피, 사탕수수 농장에서 사용되는 비료 관개(퍼티게이션) 및 엽면 살포 장치와의 통합이 뒷받침한 결과입니다. 빠른 흡수, 균일한 혼합, 그리고 작물 보호제와의 탱크 혼합 적합성이 이 제품의 보급을 뒷받침하고 있습니다. 방출 조절 비료는 시장 점유율이 낮지만, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.4%를 나타낼 것으로 전망됩니다. 이는 브라질의 감세 조치와 질산염에 대한 강제적인 상한 규제로 인해, 고효율 대안이 비용 면에서 경쟁력을 높이고 있음을 반영한 것입니다.

또한, 결정화를 지연시키는 최근의 기술 혁신 덕분에 살포 횟수 감소, 노동력 절감, 저장 안정성 향상과 같은 운영상의 이점도 액체 비료의 도입을 뒷받침하고 있습니다. 한편, 폴리머 코팅 입상 비료는 한 번만 시비해도 되는 편리함이 높은 초기 비용을 상쇄해 주는 광활한 곡물 밭에서 호조를 보이고 있습니다. 유황 코팅 요소는 면화와 옥수수 재배에서 보급이 확대되고 있으며, 폴리머·유황 하이브리드 제품은 비용 효율을 중시하는 대두 재배 지역에서 활용되고 있습니다. 서방형 유기·무기 복합 비료는 유기농 인증을 취득한 생산자들 사이에서 틈새 시장을 차지하고 있습니다. 전반적으로, 제품 포트폴리오의 다각화를 통해 공급업체들은 기상 상황, 가격 변동, 정책 변화에 대한 위험을 헤지할 수 있게 되었으며, 각 전문 분야에서 견실한 수익을 유지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 개 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO가 직면하는 중요 전략적 과제

JHS 26.07.09According to Mordor Intelligence, the south america specialty fertilizer market size was valued at USD 2.81 billion in 2025 and estimated to grow from USD 3.01 billion in 2026 to reach USD 4.09 billion by 2031, at a CAGR of 6.30% during the forecast period (2026-2031).

This report is Segmented by Speciality Type (CRF, Liquid Fertilizer, SRF, and Water Soluble), by Application Mode (Fertigation, Foliar, and Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Country (Argentina, Brazil, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

South America Specialty Fertilizer Market Trends and Insights

Surge in Drip-Irrigated Acreage

Brazil's irrigated land expanded 12% between 2019 and 2024, reaching 8.2 million ha, with drip systems the fastest-growing share. Drip technology requires fully soluble inputs, making specialty fertilizers essential to prevent emitter clogging and to match nutrient pulses with crop demand. Argentina added 1.8 million ha, chiefly in Mendoza vineyards and northern citrus groves, reinforcing liquid and water-soluble uptake. Regional equipment manufacturers posted 15-20% annual sales growth, reinforcing the feedback loop between precision irrigation and fertilizer innovation. Yield data show 8-10% gains when fertigation combines soluble NPK with micronutrient chelates, validating investment even under volatile commodity prices. Local agronomic service providers now bundle irrigation kits with nutrition advisories, speeding farmer learning curves. As drip lines penetrate Paraguay and Uruguay, cross-border demand for soluble blends climbs, widening the addressable base of the South America specialty fertilizer market.

Government Tax Incentives on Enhanced-Efficiency Fertilizers

Brazil's 2024 reform cut PIS/COFINS on controlled-release and slow-release fertilizers from 9.25% to 3.65%, trimming retail prices about 6%. Argentina matched with lower import duties on polymer-coated urea and biostimulant additives, aligning with ISO 14001 certification rebates. Early market data show controlled-release tonnage up 23% just six months after rollout. The policy tightens the link between environmental stewardship and profitability, accelerating market penetration beyond high-value horticulture into broadacre soybean, corn, and cotton. Local blenders rapidly shifted portfolios toward coated products, leveraging transitional inventory credits. As fiscal benefits sunset in 2026, manufacturers expect demand stickiness given demonstrable yield boosts and lower labor costs per hectare. Neighboring governments monitor the Brazilian model, foreshadowing a broader incentive wave across South America specialty fertilizer market economies.

High Upfront Cost versus Commodity Fertilizers

Specialty fertilizers sell at 25-40% premiums to conventional NPK, a hurdle for Brazil's 3.9 million smallholders who comprise 77% of farm units. When crop prices soften, growers revert to cheaper bulk nutrients. Peso depreciation in Argentina magnifies price gaps because many inputs are dollar-denominated. Distributors counter with seasonal credit plans and grain-barter programs, but repayment risk keeps interest rates high. Without cost-sharing incentives, adoption lags in zones where labor is abundant and yield ceilings are lower. Government voucher schemes remain pilot-scale, limiting near-term relief. Consequently, price sensitivity chops an estimated 1.8% from the South America specialty fertilizer market CAGR forecast over the next two years.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Soybean and Corn Double-Cropping Intensity

- Tightening Water-Quality Regulations on Nitrate Leaching

- Limited Distribution Infrastructure in Interior Brazil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid fertilizers held a dominant 36.6% share of the South America specialty fertilizer market in 2025, boosted by integration with fertigation and foliar equipment used in citrus, coffee, and sugarcane plantations. Rapid absorption, uniform mixing, and compatibility with crop-protection tank mixes underpin adoption. Controlled-release fertilizers, though smaller, are forecast to deliver a 7.4% CAGR during 2026-2031, reflecting Brazil's tax cuts and mandatory nitrate caps that make enhanced-efficiency options cost-competitive.

Operational gains also favor liquids, such as fewer passes, reduced labor, and better shelf stability after recent innovations that slow crystallization. Conversely, polymer-coated granules thrive in broadacre grains where single-application convenience offsets higher upfront cost. Sulfur-coated urea finds traction in cotton and corn, while polymer-sulfur hybrids serve cost-sensitive soy areas. Slow-release organo-mineral blends occupy a niche among organic-certified growers. Overall, product portfolio diversification allows suppliers to hedge against weather, price swings, and policy shifts, sustaining revenue robustness across specialty categories.

Complete Report Scope:

- Specialty Type

- Controlled-Release Fertilizer (CRF)

- Polymer-Coated

- Polymer-Sulfur-Coated

- Others

- Liquid Fertilizer

- Slow-Release Fertilizer (SRF)

- Water-Soluble Fertilizer

- Controlled-Release Fertilizer (CRF)

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

- Country

- Argentina

- Brazil

- Rest of South America

List of Companies Covered in this Report:

- EuroChem Group

- SQM S.A.

- The Mosaic Company

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Yara International ASA

- Grupa Azoty S.A. (Compo Expert GmbH)

- Haifa Group

- TIMAC Agro Brasil (Groupe Roullier)

- Nutrien

- Compass Minerals International Inc.

- Koch Agronomic Services LLC (Koch Industries)

- Valagro (Syngenta Group)

- AgroLiquid

- Omex Agrifluids Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Surge in drip-irrigated acreage

- 4.6.2 Government tax incentives on enhanced-efficiency fertilizers

- 4.6.3 Increasing soybean and corn double-cropping intensity

- 4.6.4 Tightening water-quality regulations on nitrate leaching

- 4.6.5 Biostimulant-fertilizer premix integration

- 4.6.6 Blockchain-based traceability premiums

- 4.7 Market Restraints

- 4.7.1 High upfront cost vs. commodity fertilizers

- 4.7.2 Limited distribution infrastructure in interior Brazil

- 4.7.3 Lack of crop-specific field trial data for tropical soils

- 4.7.4 Currency-exchange volatility impacting import costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Specialty Type

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.1.1.1 Polymer-Coated

- 5.1.1.2 Polymer-Sulfur-Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 Slow-Release Fertilizer (SRF)

- 5.1.4 Water-Soluble Fertilizer

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 EuroChem Group

- 6.4.2 SQM S.A.

- 6.4.3 The Mosaic Company

- 6.4.4 ICL Group Ltd.

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Yara International ASA

- 6.4.7 Grupa Azoty S.A. (Compo Expert GmbH)

- 6.4.8 Haifa Group

- 6.4.9 TIMAC Agro Brasil (Groupe Roullier)

- 6.4.10 Nutrien

- 6.4.11 Compass Minerals International Inc.

- 6.4.12 Koch Agronomic Services LLC (Koch Industries)

- 6.4.13 Valagro (Syngenta Group)

- 6.4.14 AgroLiquid

- 6.4.15 Omex Agrifluids Ltd.