|

시장보고서

상품코드

2073622

상용 항공기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Commercial Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

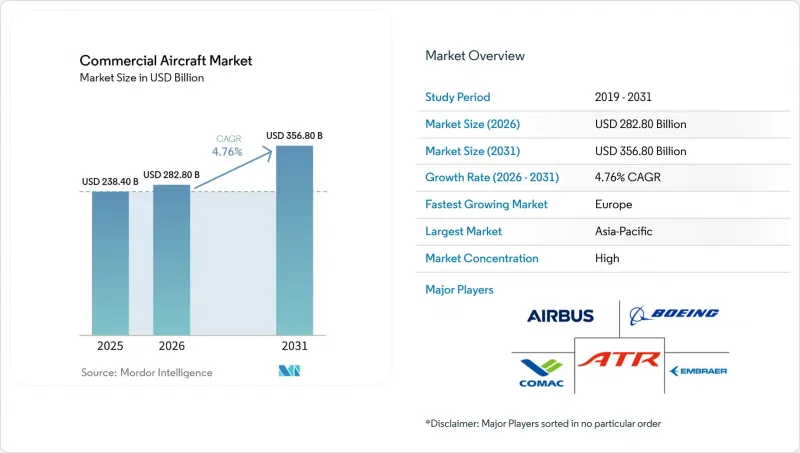

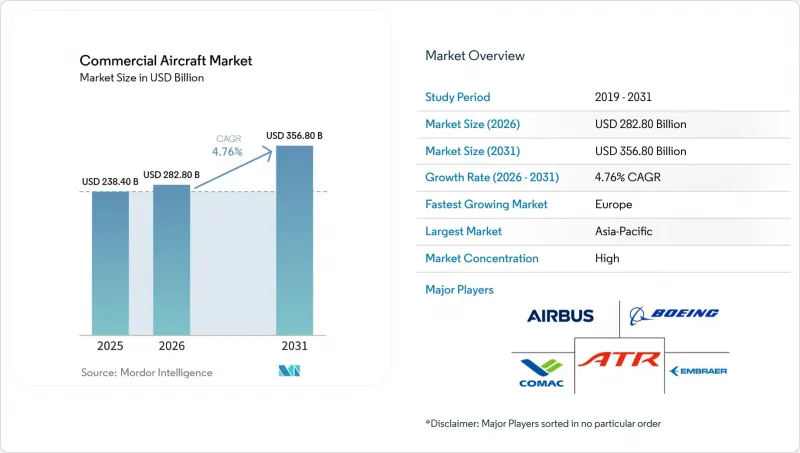

Mordor Intelligence에 의하면, 상용 항공기 시장 규모는 2025년 2,384억 달러에서 2026년에는 2,828억 달러로 확대되어 2026년부터 2031년까지 CAGR 4.76%로 성장을 지속하여, 2031년에는 3,568억 달러에 이를 것으로 예측됩니다.

본 보고서는 항공기 유형(나로우드, 와이드바디, 리저널 제트), 용도(여객기 및 화물기), 추진 방식(터보팬 및 터보프로프), 구성 요소(기체 구조, 항공 엔진, 아비오닉스 및 비행 제어, 객실 내장재 및 기내 엔터테인먼트·통신(IFEC) 등), 그리고 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 상용 항공기 시장 동향과 인사이트

연비 효율이 뛰어난 단일 통로 제트기를 중심으로 한 기단 현대화 움직임

A320neo와 B737 MAX 모델은 좌석당 연료 소비량을 약 20% 줄여 운항 효율을 대폭 향상시키기 때문에 각 항공사들은 취항한 지 20년이 지난 협폭기들의 퇴역을 가속화하고 있습니다. 델타항공은 2025년 4월, 노후화된 MD-88을 대체하기 위해 B737 MAX 여객기 100대를 발주했습니다. MD-88의 유지비가 신조 항공기의 리스 비용을 초과했기 때문입니다. 에어버스는 7,000대 이상의 미인도 주문량 덕분에 생산 계획의 가시성이 확보되었습니다는 점을 근거로, 2027년까지 A320 계열의 월간 생산 대수를 75대로 늘릴 계획입니다. 엔진 제조업체들도 마찬가지로 혜택을 보고 있습니다. CFM의 LEAP 및 프랫 앤 휘트니의 기어드 터보팬은 이러한 기체들과 연계된 수십 년에 걸친 서비스 계약을 체결했습니다. 이러한 전환으로 인해 지역 제트기 시장의 틈새 시장이 위축되면서, 항공사들은 76석 규모의 엠브라에르 E175에서 좌석당 비용이 더 낮은 150석 규모의 협폭기종으로 기종을 변경해야 하는 상황에 직면해 있습니다.

신흥 시장에서 COVID-19 이후 여객 수요 회복의 가속화

2023년 말까지 아시아태평양 전역에서 국경이 재개되고, 억눌려 있던 수요가 풀리면서 2025년 지역별 여객 킬로미터(RPK)는 전년 대비 5% 증가했습니다. 중국 항공사는 2024년, 단일 계약으로 A320neo 계열 항공기 292대를 발주했습니다. 이는 고속철도가 포화 상태에 이른 가운데, 국내 여행이 그 공급 능력을 흡수할 수 있다는 자신감을 보여주는 것입니다. 인도의 인디고는 2024년에 1억 1,300만 명의 승객을 수송할 예정이며, 2030년까지 600대 규모의 항공기 편대를 구축하는 것을 목표로 하고 있습니다. 여기에는 델리와 유럽의 도시들을 직항편으로 연결하는 A321XLR도 포함됩니다. 두바이와 도하 등 중동의 허브 공항들은 도착 시 비자 제도가 환승을 촉진함에 따라 제6자유권에 따른 여객 수송을 회복하여, 2028년까지 연평균 성장률(CAGR) 5.4%로 성장을 지속하고, 있습니다. 거시적인 위험 요인은 여전히 남아 있지만, 수요의 급증은 신형 기종의 투자 회수 기간을 단축함으로써 상용 항공기 시장을 지탱하고 있습니다.

엔진 주조 및 복합재료 공급망의 병목 현상

분말 금속이 혼입된 것으로 인해 플랫 앤 휘트니사의 기어드 터보팬 디스크에 대한 검사가 실시되었으며, 정점 시기에는 약 600대의 A320neo가 운항 중단되었고, 2024년에는 협폭기 리스료가 15% 상승했습니다. 인력 부족으로 인해 스피릿 에어로시스템즈사의 기체 납품이 지연되면서, 보잉사와 에어버스사 양사 모두에 영향을 미쳤습니다. 게다가 자동차 및 풍력 발전 업계도 직면하고 있는 과제인 탄소섬유용 수지 부족이 복합재 주익의 생산을 방해했습니다. 이러한 지연으로 인해, 에어버스가 내세웠던 ‘월 75대 생산되는 협폭기"라는 목표는 2027년 하반기로 미루게 되었습니다. 이러한 납품 지연의 결과로 미처리 주문이 발생했습니다. 2024년에 각 항공사는 2,100대의 협폭기체를 발주했으나, 실제로 인도된 대수는 1,350대에 그쳤습니다.

부문별 분석

협폭기체는 상용 항공기 시장에서 가장 큰 점유율을 차지하고 있으며, 2025년 인도 대수의 78.69%를 차지하고 있습니다. 또한, 2031년까지 연평균 성장률(CAGR) 5.98%를 기록하며 그 우위를 확대할 것으로 예측됩니다. 생산 라인은 이러한 수요에 부응하도록 조정되어 있습니다. 에어버스는 2025년에 A320 시리즈 650대를 인도할 예정이며, 2027년까지월75대 생산을 목표로 하고 있습니다. 한편, 보잉은 기체 생산 지연이 해소되는 대로 2026년 말까지 B737 MAX를월38대씩 생산할 계획입니다. 와이드바디 항공기는 장거리 노선이라는 틈새 시장을 채우고 있지만, 항공사가 종합적인 D-체크를 통해 B787이나 A350의 수명을 연장할 수 있기 때문에 교체 수요는 4%에 그치는 등 저조한 수준을 보이고 있습니다. 지역 제트기 수요는 여전히 저조합니다. 미국의 스코프 조항에 따라 좌석 수가 76석으로 제한되어 있어, 100석 미만의 기체 도입이 제약을 받고 있습니다.

지방 공항으로의 진출이 협폭기 동향을 가속화하고 있습니다. 라이언에어, 위즈에어, 인디고 등 3사는 총 1,000대 이상의 A320neo 및 B737 MAX를 발주하여 향후 10년간 생산 라인의 안정성을 확보하고 있습니다. 와이드 바디 기종의 수주 상황은 더욱 불규칙합니다. 에미레이트 항공이 두 업체(OEM)로부터 200대 이상을 구매한 것은 거의 10년 치 생산량에 해당합니다. 각 항공사들이 에어버스 A220으로의 전환을 추진하는 가운데, 지역 제트기는 어려움을 겪고 있습니다. A220은 협폭기(narrow-body)로 분류되지만, 지역 제트기 수준의 운항 비용을 실현함으로써 상용 항공기 시장에서 협폭기의 우위를 더욱 공고히 하고 있습니다.

2025년에는 여객 서비스가 부문 매출의 95.55%를 차지해, 2031년까지 연평균 성장률(CAGR) 5.55%로 증가할 것으로 전망됩니다. B787이나 A350의 화물칸에는 20-30톤의 화물이 실리며, 대부분의 경우 운항 비용의 15%를 충당하고 있어, 여객 수요가 부진할 때에도 노선의 수익성을 유지하고 있습니다. 페덱스나 UPS와 같은 통합 물류 기업에 대한 화물기 수요는 여전히 이어지고 있지만, 현재는 많은 전자상거래 소포가 정기 여객기 내에서 운송되고 있습니다.

개조 프로그램을 통해 트윈 아일 항공기의 수명이 연장되고 있습니다. 보잉은 2024년에 B767-300 화물기 28대를 인도했는데, 이 중 대부분은 여객기를 화물기로 개조한 기체이며, 이를 통해 노후화된 기체의 수익 기간이 15년 연장됩니다. 신조 B777F와 향후 출시될 A350F 모델은 가격이 2억 달러를 초과하기 때문에 수익성이 높은 노선에서만 주문을 받고 있습니다. 2027년부터 전용 화물기에 대해 EU의 탄소세가 부과될 전망인 만큼, 환경 정책이 화물 사업의 수익성에 영향을 미칠 가능성이 있습니다.

지역별 분석

아시아태평양은 2025년 상용 항공기 시장 점유율의 32.75%를 차지하며 세계 최대의 점유율을 기록했습니다. 그러나 공항 인프라의 제약과 조종사 부족으로 인해 Tier 1 허브 공항 이외의 지역에서는 운항 횟수 증가가 제한될 것으로 보이며, 이에 따라 성장 속도는 둔화될 전망입니다. 중국동방항공과 중국국제항공은 2024년까지 총 292대의 A320neo 계열 항공기를 발주했습니다. 이는 첨단 항공전자 장비 및 반도체 수입을 제한하는 서방의 수출 규제로 인해 COMAC의 C919가 국내에 15대만 인도된 상황에서도, 단일 통로 항공기에 대한 수요가 지속되고 있음을 보여줍니다. 인디고는 현재 350대의 항공기를 운항하고 있으며, 2030년까지 600대로 늘릴 계획입니다. A321XLR의 항속 거리를 활용해 델리-런던 및 뭄바이-파리 간 직항편을 취항시키고, 직항편을 이용하기 위해 15% 더 높은 운임을 지불하는 것을 마다하지 않는 프리미엄층 승객을 유치할 방침입니다.

유럽은 지역별로는 가장 빠른 성장세를 보일 것으로 예상되며, 2031년까지 연평균 성장률(CAGR) 5.81%를 나타낼 것으로 전망됩니다. 이는 동유럽과 이베리아 반도 수요에 힘입은 것으로, 라이언에어와 위즈에어는 기존 항공사들이 간과하기 쉬운 지방 공항의 슬롯을 활용하고 있습니다. 라이언에어는 2025년 8월 월간 승객 수 2,100만 명을 기록했으며, 브라티슬라바와 예레반에 거점을 개설했습니다. 이 항공사는 197석 규모의 B737 MAX 8-200 기종을 운항하고 있으며, 이를 통해 이용 가능한 좌석 킬로미터당 단위 비용을 0.025유로로 억제하여, 네트워크 내 경쟁사보다 40% 낮은 수준을 달성하고 있습니다. 위즈에어는 2025년 여름, 밀라노-티라나 노선 및 로마-부쿠레슈티 노선에 A321neo를 투입해 평균 탑승률 85%를 달성함으로써, 이탈리아 LCC 운항 능력의 60.6%를 차지하며 알리탈리아 항공의 파산으로 인해 생긴 공백을 메웠습니다.

북미는 미국의 협폭기 교체 주기와 캐나다의 지역 노선망 확충에 힘입어, 2025년 상용 항공기 시장에서 여전히 큰 점유율을 유지했습니다. 그러나 항공기 노후화와 허브 공항의 수용 능력 포화로 인해 향후 성장세는 둔화될 것으로 예측됩니다. 델타항공의 B737 MAX 100대 구매와 유나이티드항공의 A321neo 110대 발주는 각 신형 항공기가 15년이 지난 구형 항공기에 비해 연간 150만 달러의 연료비 절감 효과를 가져온다는 점을 여실히 보여주고 있습니다. 멕시코의 볼라리스와 비바에어로바스는 2020년 이후, 기존 항공사들이 완전히 회복하지 못한 미국 지방 도시로의 국경을 넘는 노선망을 확대하며, 팬데믹으로 인한 운항 감축으로 발생한 잉여 운항 능력을 흡수하고 있습니다. 중동은 허브로서의 지역적 우위를 활용하고 있습니다. 에미레이트 항공과 카타르 항공은 계속해서 와이드바디 항공기를 증강하고 있는 반면, 리야드 에어는 “비전 2030”의 일환으로 보잉 787-9 기종 72대를 도입하여, 2030년까지 승객 수 3,000만 명을 목표로 하고 있습니다. 남미와 아프리카에서는 터보프롭기 및 협폭기 운항을 단계적으로 확대되고 있습니다. LATAM과 GOL은 총 320대의 항공기를 운용하고 있으며, 에티오피아 항공은 아프리카 내 노선망을 확대되고 있습니다. 그러나 환율 변동과 인프라 부족으로 인해 두 지역 모두 성장률이 한 자릿수 중반에 머물고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.09According to Mordor Intelligence, the commercial aircraft market size is expected to grow from USD 238.4 billion in 2025 to USD 282.8 billion in 2026 and is forecasted to reach USD 356.8 billion by 2031 at a 4.76% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Narrowbody, Widebody, and Regional Jets), Application (Passenger and Freighter), Propulsion Type (Turbofan and Turboprop), Component (Airframe Structures, Aero-Engines, Avionics and Flight Control, Cabin Interior and IFEC, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Commercial Aircraft Market Trends and Insights

Fleet-Modernization Push for Fuel-Efficient Single-Aisle Jets

Airlines are retiring 20-year-old narrowbody aircraft at an accelerated pace, as the A320neo and B737 MAX models offer approximately 20% lower fuel consumption per seat, significantly enhancing operating efficiency. Delta ordered 100 B737 MAX jets in April 2025 to replace its aging MD-88s, whose maintenance costs had exceeded lease rates for new aircraft. Airbus plans to increase A320-family output to 75 units per month by 2027, citing a backlog exceeding 7,000 frames that ensures line visibility. Engine makers reap parallel gains: CFM's LEAP and Pratt & Whitney's geared turbofan secure multi-decade service contracts tied to these airframes. The shift crowds regional-jet niches, pushing operators to up-gauge from 76-seat Embraer E175s to 150-seat narrowbodies that offer lower per-seat costs.

Accelerating Post-COVID Passenger-Traffic Rebound in Emerging Markets

International borders reopened across Asia-Pacific by late 2023, unleashing pent-up demand that lifted regional revenue passenger kilometers (RPKs) by 5% year over year in 2025. Chinese airlines booked 292 A320neo-family jets in a single transaction in 2024, signaling confidence that domestic travel can absorb capacity as high-speed rail reaches saturation. India's IndiGo flew 113 million passengers in 2024 and targets a 600-strong fleet by 2030, including A321XLRs that open nonstop Delhi-to-European city pairs. Middle Eastern hubs such as Dubai and Doha regained sixth-freedom traffic, posting a 5.4% CAGR through 2028, as visa-on-arrival schemes stimulate transfers. While macro risks persist, the demand surge underpins the commercial aircraft market by shortening payback periods on new jets.

Engine-Casting and Composite Supply-Chain Bottlenecks

Powder-metal contamination led to inspections of Pratt & Whitney geared-turbofan disks, resulting in the grounding of approximately 600 A320neos at their peak, and causing narrowbody lease rates to increase by 15% in 2024. Due to workforce shortages, Spirit AeroSystems experienced delays in fuselage deliveries, affecting both Boeing and Airbus. Additionally, a shortage of carbon-fiber resin, a challenge also faced by the automotive and wind energy sectors, hindered the production of composite wings. This setback has pushed Airbus's target of producing 75 narrowbody aircraft per month to late 2027. As a result of these delivery shortfalls, a backlog has formed: while airlines placed orders for 2,100 narrowbody aircraft in 2024, they only took delivery of 1,350.

Other drivers and restraints analyzed in the detailed report include:

- Low-Cost-Carrier Route Expansion into Secondary Airports

- Sustainable-Aviation-Fuel Blending Mandates Influencing OEM Roadmaps

- Airline Profit Cyclicality and High Financing Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Narrowbodies accounted for the largest commercial aircraft market share, representing 78.69% of 2025 deliveries, and are expected to extend their lead at a 5.98% CAGR through 2031. Production lines are calibrated to meet this demand: Airbus delivered 650 A320-family units in 2025 and targets a monthly output of 75 by 2027, while Boeing plans to produce 38 B737 MAX units per month by late 2026, once fuselage delays are resolved. Widebodies fill long-haul niches but face slower 4% replacement demand because airlines can prolong the lifecycles of B787s or A350s through comprehensive D-checks. Regional-jet volumes remain modest; US scope clauses cap seats at 76, constraining expansion of sub-100-seat fleets.

Secondary-airport penetration accelerates the narrowbody trend. Ryanair, Wizz Air, and IndiGo collectively hold orders for more than 1,000 A320neos and B737 MAXs, ensuring line stability for the rest of the decade. Widebody order books are lumpier; Emirates' dual-OEM purchase of 200-plus frames equals nearly a decade of output. Regional jets struggle as airlines upscale to Airbus A220s, which qualify as narrowbodies yet offer regional-jet trip costs, further cementing narrowbody supremacy within the commercial aircraft market.

Passenger services accounted for 95.55% of sectoral revenue in 2025 and are expected to increase at a 5.55% CAGR through 2031. Belly holds on B787s, and A350s haul 20-30 tonnes of freight, often covering 15% of trip cost, which protects route economics when passenger loads soften. Freighter demand persists for integrators like FedEx and UPS, yet many e-commerce parcels now ride inside scheduled passenger aircraft.

Conversion programs extend twin-aisle life. Boeing delivered 28 B767-300 Freighters in 2024, mostly passenger-to-freighter retrofits that add 15 years of revenue for older airframes. New-build B777F and future A350F models attract orders only on high-yield lanes because price tags exceed USD 200 million. Environmental policy may tilt cargo economics as EU carbon taxes loom for dedicated freighters starting in 2027.

Complete Report Scope:

- By Aircraft Type

- Narrowbody

- Widebody

- Regional Jets

- By Application

- Passenger

- Freighter

- By Propulsion Type

- Turbofan

- Turboprop

- By Component

- Airframe Structures

- Aero-Engines

- Avionics and Flight Control

- Cabin Interior and IFEC

- Other Components

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

The Asia-Pacific region commanded 32.75% of the 2025 commercial aircraft market share, the largest share globally. Yet, its growth pace will moderate as airport infrastructure limitations and pilot shortages curb frequency additions beyond Tier-1 hubs. China Eastern and Air China collectively ordered 292 A320neo-family jets in 2024, underscoring sustained single-aisle demand even as COMAC's C919 remains confined to 15 domestic deliveries due to Western export controls that restrict advanced avionics and semiconductor imports. IndiGo operates 350 aircraft and plans to reach 600 by 2030, leveraging the A321XLR's range to launch nonstop flights from Delhi to London and Mumbai to Paris, capturing premium travelers willing to pay 15% more for direct service.

Europe will post the fastest regional expansion, advancing at a 5.81% CAGR through 2031, driven by demand in Eastern Europe and the Iberian Peninsula, where Ryanair and Wizz Air capitalize on secondary-airport slots that legacy carriers often overlook. Ryanair set a monthly record with 21 million passengers in August 2025 and opened bases in Bratislava and Yerevan, operating 197-seat B737 MAX 8-200s that reduce unit costs to EUR 0.025 per available seat-kilometer, 40% below those of its network competitors. Wizz Air captured 60.6% of Italy's low-cost capacity in summer 2025 by fielding A321neos on Milan-Tirana and Rome-Bucharest flights that average 85% load factors, filling the vacuum left by Alitalia's collapse.

North America retained a sizable position in the 2025 commercial aircraft market, fueled by US narrowbody replacement cycles and Canada's regional build-out. However, future growth is tempered by mature fleets and hub capacity saturation. Delta's 100-unit B737 MAX purchase and United's 110 A321neo commitment highlight the USD 1.5 million annual fuel-cost advantage each new jet offers over 15-year-old predecessors. Mexico's Volaris and VivaAerobus expand their cross-border networks to US secondary cities that legacy carriers never fully restored after 2020, absorbing capacity displaced by pandemic cuts. The Middle East capitalizes on its hub geography; Emirates and Qatar Airways continue to add widebodies, while Riyadh Air targets 30 million passengers by 2030 with 72 Boeing 787-9s under Vision 2030. South America and Africa add turboprops and narrowbodies incrementally; LATAM and GOL field 320 aircraft combined, while Ethiopian Airlines expands intra-African links. However, currency volatility and infrastructure gaps confine both regions to mid-single-digit growth trajectories.

- Airbus SE

- The Boeing Company

- Embraer S.A.

- Avions de Transport Regional GIE

- Commercial Aircraft Corporation of China, Ltd. (COMAC)

- De Havilland Aircraft of Canada Limited

- United Aircraft Corporation

- Mitsubishi Heavy Industries, Ltd.

- GE Aerospace

- Rolls-Royce Holdings plc

- Safran S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fleet-modernization push for fuel-efficient single-aisle jets

- 4.2.2 Accelerating post-COVID passenger-traffic rebound in emerging markets

- 4.2.3 Low-cost-carrier (LCC) route expansion into secondary airports

- 4.2.4 Sustainable-aviation-fuel (SAF) blending mandates influencing OEM roadmaps

- 4.2.5 Bundled "power-by-the-hour" service contracts tied to OEM airframes

- 4.2.6 Urban air-mobility (UAM) corridor funding spurring demand for high-cycle turboprops

- 4.3 Market Restraints

- 4.3.1 Engine-casting and composite supply-chain bottlenecks

- 4.3.2 Airline profit cyclicality and high financing costs

- 4.3.3 Certification delays from next-gen software compliance rules

- 4.3.4 Export-control tensions restricting deliveries to sanctioned nations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.1.3 Regional Jets

- 5.2 By Application

- 5.2.1 Passenger

- 5.2.2 Freighter

- 5.3 By Propulsion Type

- 5.3.1 Turbofan

- 5.3.2 Turboprop

- 5.4 By Component

- 5.4.1 Airframe Structures

- 5.4.2 Aero-Engines

- 5.4.3 Avionics and Flight Control

- 5.4.4 Cabin Interior and IFEC

- 5.4.5 Other Components

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Singapore

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Qatar

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 The Boeing Company

- 6.4.3 Embraer S.A.

- 6.4.4 Avions de Transport Regional GIE

- 6.4.5 Commercial Aircraft Corporation of China, Ltd. (COMAC)

- 6.4.6 De Havilland Aircraft of Canada Limited

- 6.4.7 United Aircraft Corporation

- 6.4.8 Mitsubishi Heavy Industries, Ltd.

- 6.4.9 GE Aerospace

- 6.4.10 Rolls-Royce Holdings plc

- 6.4.11 Safran S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment