|

시장보고서

상품코드

1665287

우주 라스트 마일 배송 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Space Last-Mile Delivery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

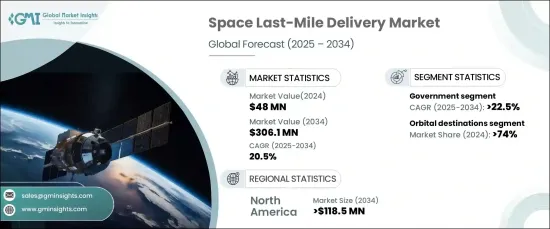

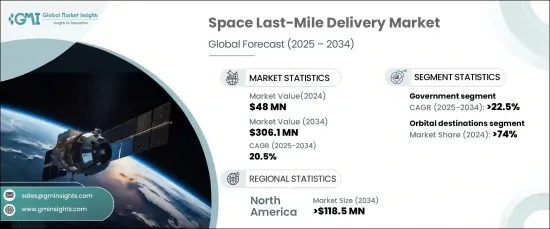

세계의 우주 라스트 마일 배송 시장은 2024년에는 4,800만 달러로 평가되었고, 2025년부터 2034년까지 CAGR은 20.5%로 예측되어 눈부신 성장을 이룰 전망입니다. 이 성장의 원동력이 되는 것은 최첨단 궤도상 물류 솔루션과 정밀한 위성 배치에 대한 수요 증가입니다. 궤도 운송기 및 첨단 추진 시스템의 혁신은 보다 효율적인 페이로드 배치 및 재배치를 가능하게 하여 위성 네트워크, 우주 탐사 및 상업 운영을 그 어느 때보다 효과적으로 만듭니다. 우주의 상업화가 진행되고 재사용 가능한 기술이 진보함에 따라 이러한 서비스는 보다 비용 효율적이 되어 보다 폭넓은 산업을 이용할 수 있게 되었습니다.

우주 라스트 마일 배송 시장은 주로 궤도 목적지와 행성 또는 지표 목적지의 두 가지 범주로 나뉩니다. 궤도 목적지 부문은 2024년에는 74%의 압도적인 시장 점유율을 차지했으며, 향후 수년간은 강력한 성장이 예상됩니다. 세계의 광대역 커버리지, 지구관측, 통신 서비스를 위한 위성 별자리의 전개 확대는 궤도 전달 솔루션 수요를 크게 밀어 올리고 있습니다. 각 조직은 위성의 성능을 최적화하기 위해 정확한 궤도 배치를 달성하는 데 중점을 두고 있으며, 우주 임무의 진화하는 요구를 충족시키기 위해 라스트 마일 배송 시스템과 궤도 변환 기술에 대한 의존도를 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 4,800만 달러 |

| 예측 금액 | 3억610만 달러 |

| CAGR | 20.5% |

최종 사용자의 관점에서 시장은 상업 부문과 정부 부문으로 구분됩니다. 2034년 CAGR은 22.5%로 예측되어 정부 부문이 가장 높은 성장이 예상되고 있습니다. 세계 각국의 정부는 모니터링, 커뮤니케이션, 미사일 감지에 중요한 방위 위성을 배포하기 위해 라스트 마일 배송 인프라에 대한 투자를 강화하고 있습니다. 정확한 궤도 측위의 필요성으로 궤도상 수송기나 궤도상 서비스 기능에 대한 관심이 높아져 국가 안보가 강화되고 위성 네트워크의 효율이 최적화됩니다.

북미는 우주 라스트 마일 배송 시장을 선도하며 2034년까지 1억 1,850만 달러에 이를 것으로 예상됩니다. 미국은 우주 탐사와 상업화에 있어서의 기술적 전문 지식에 의해 이 성장의 최전선에 있습니다. 지구관측과 통신을 위한 위성 별자리의 배치가 가속화됨에 따라 선진적 궤도상 물류 시스템 수요가 더욱 높아지고 있습니다. 각 회사는 임무의 유연성을 높이고 비용을 절감하며 우주 운영을 보다 효율적이고 합리적으로 만드는 재사용 가능한 수송기 및 자율 수송 기술 개발에 주력하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

- 시장 범위 및 정의

- 기본 추정 및 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 자료

- 유료 정보원

- 공적 정보원

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 변혁

- 장래의 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향 요인

- 성장 촉진요인

- 위성 배치수 증가

- 상업 우주 벤처의 대두 및 우주 개발에 대한 민간 분야 관여 확대

- 라이드 쉐어링 및 2차 페이로드 발사 증가

- 지속가능성 및 공간 파편의 완화에 대한 관심 증가

- 정부투자 및 우주개발계획 증가

- 산업의 잠재적 리스크 및 과제

- 높은 개발 및 운용 비용

- 기술적 한계 및 신뢰성

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정 및 예측 : 목적지별(2021-2034년)

- 주요 동향

- 궤도 목적지

- 저궤도(LEO)

- 중궤도(MEO)

- 정지궤도(GEO)

- 지구 고주회 궤도(GEO 이원)

- 행성 및 지표의 목적지

- 월면

- 화성 표면

- 소행성 표면

제6장 시장 추정 및 예측 : 페이로드별(2021-2034년)

- 주요 동향

- 과학 기기

- 인프라 컴포넌트

- 우주 정거장 모듈

- 위성 부품

- 소모품

- 추진제 및 연료

- 기타

제7장 시장 추정 및 예측 : 배송 기술별(2021-2034년)

- 주요 동향

- 자율 시스템

- 유인 배송

- 하이브리드 시스템

제8장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 상업

- 정부

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AAC Clyde Space

- Aliena

- Astro Digital

- D-Orbit

- Exotrail

- Impulse Space

- Momentus Space

- Orbit Fab

- Rocket Lab

- SEOPS(Space Exploration and Orbital Solutions)

- Spaceflight Industries

- SpaceLink

- TransAstra

The Global Space Last-Mile Delivery Market was valued at USD 48 million in 2024 and is set to experience impressive growth, with a projected compound annual growth rate (CAGR) of 20.5% from 2025 to 2034. This growth is being driven by an increasing demand for cutting-edge in-orbit logistics solutions and precise satellite deployment. Innovations in orbital transfer vehicles and advanced propulsion systems enable more efficient payload placement and repositioning, making satellite networks, space exploration, and commercial operations more effective than ever. With the growing commercialization of space and advancements in reusable technologies, these services are becoming more cost-effective and accessible to a broader range of industries.

The space last-mile delivery market is primarily divided into two categories: orbital targets and planetary or surface destinations. The orbital destinations segment held a dominant 74% market share in 2024 and is expected to see robust growth in the coming years. The expanding deployment of satellite constellations for global broadband coverage, Earth observation, and communication services is significantly boosting the demand for orbital delivery solutions. Organizations are placing greater emphasis on achieving precise orbital placement to optimize satellite performance, driving increased reliance on last-mile delivery systems and orbital transfer technologies to meet the evolving needs of space missions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48 million |

| Forecast Value | $306.1 million |

| CAGR | 20.5% |

In terms of end users, the market is segmented into commercial and government sectors. The government segment is expected to experience the highest growth, with a projected CAGR of 22.5% through 2034. Governments worldwide are ramping up investments in last-mile delivery infrastructure to deploy critical defense satellites for surveillance, communications, and missile detection. The need for exact orbital positioning is fueling greater interest in orbital transfer vehicles and in-orbit servicing capabilities, which in turn enhances national security and optimizes satellite network efficiency.

North America is anticipated to lead the space last-mile delivery market, reaching USD 118.5 million by 2034. The United States is at the forefront of this growth, driven by its technological expertise in space exploration and commercialization. The escalating deployment of satellite constellations for Earth observation and communication is further intensifying the demand for advanced in-orbit logistics systems. Companies are focusing on developing reusable transfer vehicles and autonomous delivery technologies, which enhance mission flexibility and reduce costs, making space operations more efficient and affordable.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing number of satellite deployment

- 3.6.1.2 Rise of commercial space ventures and the growing private sector involvement in space exploration

- 3.6.1.3 Increasing ride-sharing and secondary payload launches

- 3.6.1.4 Growing focus on sustainability and mitigating space debris

- 3.6.1.5 Increasing governmental investments and space programs

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and operational costs

- 3.6.2.2 Technological limitations and reliability

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Destination, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Orbital destinations

- 5.2.1 Low earth orbit (LEO)

- 5.2.2 Medium earth orbit (MEO)

- 5.2.3 Geostationary orbit (GEO)

- 5.2.4 High earth orbit (Beyond GEO)

- 5.3 Planetary/surface destinations

- 5.3.1 Lunar surface

- 5.3.2 Martian surface

- 5.3.3 Asteroids surface

Chapter 6 Market Estimates & Forecast, By Delivery Payload, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Scientific equipment

- 6.3 Infrastructure components

- 6.3.1 Space station modules

- 6.3.2 Satellite components

- 6.4 Consumables

- 6.5 Propellants/fuel

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Delivery Technology, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Autonomous systems

- 7.3 Manned delivery

- 7.4 Hybrid systems

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AAC Clyde Space

- 10.2 Aliena

- 10.3 Astro Digital

- 10.4 D-Orbit

- 10.5 Exotrail

- 10.6 Impulse Space

- 10.7 Momentus Space

- 10.8 Orbit Fab

- 10.9 Rocket Lab

- 10.10 SEOPS (Space Exploration and Orbital Solutions)

- 10.11 Spaceflight Industries

- 10.12 SpaceLink

- 10.13 TransAstra