|

시장보고서

상품코드

1684861

자동차용 연료전지 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2024-2032년)Automotive Fuel Cell Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

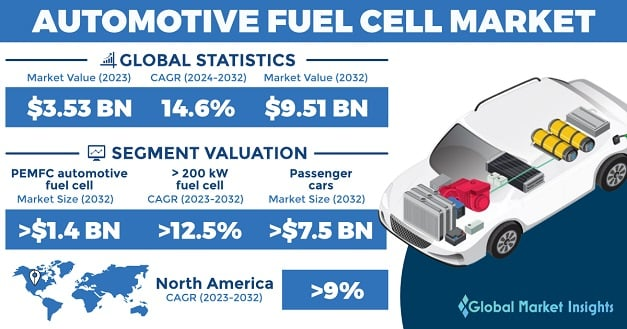

세계의 자동차용 연료전지 시장 규모는 2023년에 35억 3,000만 달러로 평가되었고 2024년부터 2032년까지 연평균 복합 성장률(CAGR) 14.6%를 나타낼 것으로 예측되고 있습니다.

연료전지는 수소와 산소의 반응에 의해 발전하는 전기화학 장치로서 기능하여 자동차, 버스, 트럭 등의 전기자동차에 전력을 공급합니다. 애노드에 수소를 도입하고 캐소드에 공기 중의 산소를 공급함으로써이 기술은 제로 방출 운송을 촉진합니다. 보다 깨끗하고 지속 가능한 모빌리티 솔루션으로의 전환은 정부, 자동차 제조업체 및 에너지 부문의 많은 투자와 함께 시장 확대의 원동력이 되었습니다. 친환경 운송 솔루션 추진, 수소 인프라 개선, 연료전지 기술 발전은 다양한 차량 부문에서 제품 채택을 가속화하고 있습니다. 연료전지 자동차를 우대하는 정책적 틀은 재정적 인센티브와 전략적 파트너십과 함께 업계의 긍정적인 궤도에 더욱 기여하고 있습니다.

고체 고분자형 연료전지(PEMFC)는 2032년까지 14억 달러 이상에 달할 것으로 예상됩니다. 규제 프레임 워크가보다 깨끗한 에너지 솔루션을 계속 추진하고 있기 때문에 운송 기관에 연료전지 도입이 꾸준히 증가하고 있습니다. 기술의 진보와 인프라의 확충이 중시됨에 따라 제품의 보급이 강화될 것으로 예상됩니다. 자동차 제조업체, 연료전지 개발업체, 에너지 공급업체는 수소 공급망 강화에 공동으로 노력하고 있으며 시장의 잠재력을 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2023 |

| 예측 연도 | 2024-2032년 |

| 시작 금액 | 35억 3,000만 달러 |

| 예측 금액 | 95억 1,000만 달러 |

| CAGR | 14.6% |

정격 출력이 200kW를 초과하는 연료전지 시스템은 2032년까지 연평균 복합 성장률(CAGR)이 12.5%를 초과할 것으로 전망됩니다. 대형 트럭, 버스, 산업용 차량에서는 이산화탄소 배출량을 삭감하면서 장거리 운송을 지원할 수 있기 때문에 이러한 대용량 시스템의 채용이 진행되고 있습니다. 상용차 부문의 대규모 용도는 업계의 성장 기회를 창출하고 있습니다. 연료전지의 효율 향상과 운영 비용 절감에 대한 노력이 경쟁 구도를 형성하고 있습니다. 정부 보조금, 세제 우대 조치 및 환경 규제도 투자 결정에 영향을 미치고, 함대 운영자에게 수소 기반 이동성으로의 전환을 촉구합니다.

연료전지 기술을 이용한 승용차는 제로 방출 차량에 대한 소비자의 관심 증가와 다양한 모빌리티 솔루션의 가용성으로 인해 2032년까지 75억 달러 이상을 창출할 것으로 예상됩니다. 연료전지 차량의 선택의 확대와 수소 보급 네트워크의 개선이 보급을 뒷받침하고 있습니다. 소비자는 지속 가능한 교통 수단에 대한 관심을 높이고 있으며, 피어 투 피어의 카셰어링 플랫폼 및 첨단 안전 기술과 같은 혁신이 자동차 분야에 연료전지 통합을 가속화하고 있습니다.

북미의 자동차용 연료전지 시장은 2032년까지 연평균 복합 성장률(CAGR) 9.0% 이상을 나타낼 것으로 예측됩니다. 정부의 강력한 지원, 수소 기반 솔루션 투자 증가, 도시 교통 용도 확대 등 업계의 성장을 강화하고 있습니다. 에너지·캐리어로서의 수소에 대한 관심은 산업 프로세스나 발전의 분야에서 높아지고 있습니다. 효율, 수명, 비용 효율성 향상을 목표로 하는 연구개발의 지속적인 노력이 지역 전체 채용을 더욱 촉진할 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

- 시장의 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

제2장 주요 요약

제3장 자동차용 연료전지 산업 인사이트

- 생태계 분석

- 벤더 매트릭스

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- FCEV 채용 증가

- 기술적 제품의 진보

- 수소 인프라 개발

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 벤치마킹

- 혁신과 지속가능성의 정세

- 경쟁 구도(2022년)

- 전략 대시보드

제5장 자동차용 연료전지 시장 : 유형별

- 주요 유형별 동향

- PEMFC

- PAFC&AFC

- 기타

제6장 자동차용 연료전지 시장 : 출력별

- 주요 출력 동향

- 100 kW 미만

- 100-200 kW

- 200 kW 이상

제7장 자동차용 연료전지 시장 : 용도별

- 주요 용도 동향

- 승용차

- 상용차

- 기타

제8장 자동차용 연료전지 시장 :지역별

- 주요 지역 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 오스트리아

- 아시아태평양

- 일본

- 한국

- 중국

- 인도

- 필리핀

- 베트남

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 라틴아메리카

- 브라질

- 페루

- 멕시코

제9장 기업 프로파일

- Acumentrics

- Altergy

- Ballard Power Systems

- FuelCell Energy, Inc

- Toshiba Energy Systems &Solutions Corporation

- Plug Power Inc.

- Cummins Inc.

- Panasonic Holdings Corporation

- Bloom Energy

- Convion Ltd

- Hyster-Yale Group, Inc.

- Advent Technologies

- BorgWarner Inc.

- Daimler Truck AG

- Ceres

- Hyundai Motor Company

- ITM Power PLC

- Nedstack Fuel Cell Technology BV

- NUVERA FUEL CELLS, LLC

- TW Horizon Fuel Cell Technologies

- Fuji Electric Co., Ltd

The Global Automotive Fuel Cell Market was valued at USD 3.53 billion in 2023 and is projected to expand at a CAGR of 14.6% between 2024 and 2032. Fuel cells serve as electrochemical devices that generate electricity through the reaction of hydrogen and oxygen, providing power for electric vehicles such as cars, buses, and trucks. With hydrogen introduced at the anode and oxygen from the air supplied to the cathode, the technology facilitates zero-emission transportation. A shift toward cleaner and more sustainable mobility solutions, combined with substantial investments from governments, automakers, and the energy sector, continues to drive market expansion. The growing push for green transportation solutions, improvements in hydrogen infrastructure, and advancements in fuel cell technology are accelerating product adoption across various vehicle segments. Policy frameworks favoring fuel cell vehicles, along with financial incentives and strategic partnerships, are further contributing to the industry's positive trajectory.

Proton Exchange Membrane Fuel Cells (PEMFCs) are expected to surpass USD 1.4 billion by 2032 due to their superior efficiency, rapid refueling, and environmentally friendly operation. As regulatory frameworks continue to promote cleaner energy solutions, fuel cell deployment in transportation is steadily increasing. The emphasis on technological advancements and infrastructure expansion is expected to strengthen product penetration. Automakers, fuel cell developers, and energy providers are working together to enhance hydrogen supply networks, reinforcing market potential.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $3.53 Billion |

| Forecast Value | $9.51 Billion |

| CAGR | 14.6% |

Fuel cell systems with power ratings above 200 kW are set to witness a CAGR of over 12.5% through 2032. The adoption of these higher-capacity systems in heavy-duty trucks, buses, and industrial vehicles is gaining traction due to their ability to support long-haul transport while reducing carbon footprints. Large-scale applications in the commercial vehicle sector are creating opportunities for industry growth. Efforts to enhance fuel cell efficiency and reduce operating costs are shaping the competitive landscape. Government grants, tax incentives, and environmental mandates are also influencing investment decisions, encouraging fleet operators to transition to hydrogen-based mobility.

Passenger cars using fuel cell technology are expected to generate over USD 7.5 billion by 2032, fueled by increased consumer interest in zero-emission vehicles and the availability of diverse mobility solutions. Expanding fuel cell vehicle options and improved hydrogen refueling networks are supporting widespread adoption. Consumers are increasingly inclined toward sustainable transportation, and innovations such as peer-to-peer car-sharing platforms and advanced safety technologies are accelerating the integration of fuel cells into the automotive sector.

North America automotive fuel cell market is forecasted to expand at a CAGR exceeding 9.0% through 2032. Robust government support, rising investments in hydrogen-based solutions, and expanding urban transit applications are strengthening industry growth. Interest in hydrogen as an energy carrier is surging across industrial processes and power generation. Ongoing research and development efforts aimed at enhancing efficiency, longevity, and cost-effectiveness are expected to further drive adoption across the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Unpaid sources

Chapter 2 Executive Summary

- 2.1 Automotive fuel cell industry 3600 synopsis, 2019 - 2032

- 2.1.1 Business trends

- 2.1.2 Type trends

- 2.1.3 Power output trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Automotive Fuel Cell Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Vendor matrix

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing adoption of FCEVs

- 3.3.1.2 Technological product advancements

- 3.3.1.3 Development of hydrogen Infrastructure

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Initial high cost

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Benchmarking

- 4.1 Innovation & sustainability landscape

- 4.2 Competitive landscape, 2022

- 4.2.1 Strategic dashboard

Chapter 5 Automotive Fuel Cell Market, By Type

- 5.1 Key type trends

- 5.2 PEMFC

- 5.3 PAFC & AFC

- 5.4 Others

Chapter 6 Automotive Fuel Cell Market, By Power Output

- 6.1 Key power output trends

- 6.2 < 100 kW

- 6.3 100 – 200 kW

- 6.4 > 200 kW

Chapter 7 Automotive Fuel Cell Market, By Application

- 7.1 Key application trends

- 7.2 Passenger cars

- 7.3 Commercial vehicles

- 7.4 Others

Chapter 8 Automotive Fuel Cell Market, By Region

- 8.1 Key regional trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 South Korea

- 8.4.3 China

- 8.4.4 India

- 8.4.5 Philippines

- 8.4.6 Vietnam

- 8.5 Middle East & Africa

- 8.5.1 South Africa

- 8.5.2 Saudi Arabia

- 8.5.3 UAE

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Peru

- 8.6.3 Mexico

Chapter 9 Company Profiles

- 9.1 Acumentrics

- 9.2 Altergy

- 9.3 Ballard Power Systems

- 9.4 FuelCell Energy, Inc

- 9.5 Toshiba Energy Systems & Solutions Corporation

- 9.6 Plug Power Inc.

- 9.7 Cummins Inc.

- 9.8 Panasonic Holdings Corporation

- 9.9 Bloom Energy

- 9.10 Convion Ltd

- 9.11 Hyster-Yale Group, Inc.

- 9.12 Advent Technologies

- 9.13 BorgWarner Inc.

- 9.14 Daimler Truck AG

- 9.15 Ceres

- 9.16 Hyundai Motor Company

- 9.17 ITM Power PLC

- 9.18 Nedstack Fuel Cell Technology BV

- 9.19 NUVERA FUEL CELLS, LLC

- 9.20 TW Horizon Fuel Cell Technologies

- 9.21 Fuji Electric Co., Ltd