|

시장보고서

상품코드

2038697

항공 연료 첨가제 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Aviation Fuel Additives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

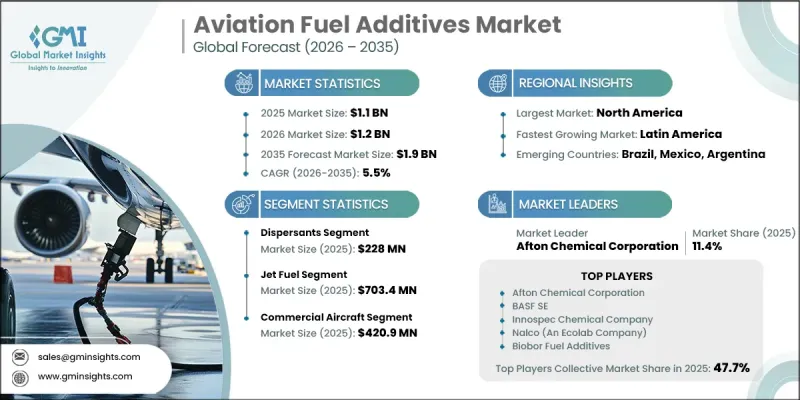

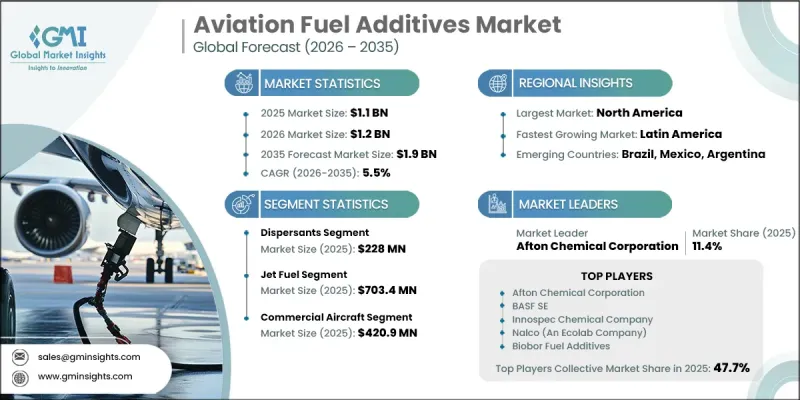

세계의 항공 연료 첨가제 시장은 2025년에 11억 달러로 평가되었고, CAGR 5.5%로 성장할 전망이며, 2035년까지 19억 달러에 이를 것으로 예측됩니다.

항공업계가 복잡한 연료 시스템 전반에 걸쳐 운항 안전, 연료 효율성 및 장기적인 신뢰성을 우선시하는 가운데, 항공 연료 첨가제 산업은 지속적으로 성장하고 있습니다. 이러한 특수 화학 제제는 성능을 향상시키고, 안정성을 유지하며, 연료의 수명 주기 동안 안전한 취급을 보장하기 위해 항공 연료에 통제된 양으로 혼합됩니다. 그 기능적 역할은 산화 최소화, 오염 억제, 부식 위험 감소, 연료 이동 중 정전기 거동 관리 등에 이르기까지 다양합니다. 항공 산업 전반에 걸친 엄격한 규정 준수 요건은 이러한 첨가제의 일관된 사용을 강화하여 항공기 시스템과의 호환성을 보장하고 다양한 환경 조건에서도 연료의 품질을 유지하도록 하고 있습니다. 정제, 저장, 유통, 그리고 최종 항공기 급유에 이르기까지 첨가제는 장기 보관과 온도 및 기압 변동에 노출된 상황에서도 품질 유지를 돕고 있습니다. 또한, 시장에서는 혼합 연료 및 대체 항공 연료와 같이 진화하는 연료 구성에 대응하기 위해 설계된 첨가제 배합의 혁신도 볼 수 있습니다. 주입 및 분사 시스템의 기술적 진보로 인해 정확도와 효율성이 향상되어 첨가제 적용을 더 잘 제어할 수 있으며, 동시에 연료의 종합적인 성능과 시스템과의 호환성을 향상시킬 수 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 11억 달러 |

| 예측 시장 규모 | 19억 달러 |

| CAGR | 5.5% |

2025년 분산제 부문은 2억 2,800만 달러를 차지했으며, 연료의 청정성과 운영 안정성을 유지하는 데 필수적인 역할을 하고 있음을 보여줍니다. 분산제 및 산화방지제 배합에 대한 의존도가 높아짐에 따라 장기 저장 및 운송 사이클에서 침전물 형성을 방지하고 연료 품질을 유지하는 것이 중요하다는 사실이 부각되고 있습니다. 저온 성능을 관리하기 위해 설계된 첨가제는 특히 온도 변동이 연료의 거동에 영향을 미치는 가혹한 비행 조건에서 안정적인 연료 흐름을 유지하고 운영 위험을 최소화하기 위해 여전히 필수적입니다.

제트 연료 부문은 2025년 7억 3,400만 달러를 차지했으며, 항공 생태계에서 제트 연료가 차지하는 지배적인 역할을 강조하고 있습니다. 열 안정성을 보장하고, 오염을 억제하며, 장시간 비행 기간 동안 신뢰할 수 있는 연료 성능을 유지하기 위해서는 첨가제의 지속적인 통합이 필요합니다. 연료 유통 네트워크의 복잡성과 연료 구성의 진화는 다양한 항공 시스템 전반에 걸쳐 일관성을 유지하면서 변화하는 운영 및 기술 요구사항에 적응할 수 있는 첨단 첨가제 솔루션의 필요성을 더욱 강조하고 있습니다.

북미의 항공 연료 첨가제 시장은 활발한 항공 활동과 잘 구축된 급유 인프라를 바탕으로 2025년 3억 8,470만 달러로 평가되었고, 2035년까지 6억 6,100만 달러로 성장할 것으로 예측됩니다. 이 지역에서는 지속적인 비행 운항과 함께 대규모 저장 및 유통 시스템 전체에서 연료의 품질을 유지해야 하기 때문에 강한 수요를 보이고 있습니다. 엄격한 품질 기준과 운영 효율성에 대한 요구는 성능 향상 첨가제의 지속적인 채택을 촉진하고 있습니다. 또한, 광범위한 항공 네트워크, 시간의 경과에 따른 성능 저하, 오염, 성능 변동으로부터 연료 시스템을 보호해야 할 필요성도 수요의 지속을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 첨가제 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 연료 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

AJY 26.06.11The Global Aviation Fuel Additives Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 1.9 billion by 2035.

The aviation fuel additives industry continues to gain momentum as the aviation sector prioritizes operational safety, fuel efficiency, and long-term reliability across complex fuel systems. These specialized chemical formulations are blended into aviation fuels in controlled quantities to enhance performance, maintain stability, and ensure safe handling throughout the fuel lifecycle. Their functional role extends to minimizing oxidation, limiting contamination, reducing corrosion risks, and managing electrostatic behavior during fuel movement. Strict compliance requirements across the aviation sector reinforce the consistent use of these additives, ensuring compatibility with aircraft systems and maintaining fuel integrity under varying environmental conditions. From refining and storage to distribution and final aircraft fueling, additives support quality preservation even during prolonged storage and exposure to fluctuating temperatures and pressure levels. The market is also witnessing innovation in additive formulations designed to align with evolving fuel compositions, including blended and alternative aviation fuels. Technological advancements in dosing and injection systems are improving accuracy and efficiency, allowing better control over additive application while enhancing overall fuel performance and system compatibility.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $1.9 Billion |

| CAGR | 5.5% |

The dispersants segment accounted for USD 228 million in 2025, reflecting their essential role in maintaining fuel cleanliness and operational stability. Increasing reliance on dispersants and antioxidant formulations highlights their importance in preventing deposit formation and preserving fuel quality during extended storage and transportation cycles. Additives designed to manage low-temperature performance remain critical for maintaining consistent fuel flow and minimizing operational risks, particularly in demanding flight conditions where temperature variations can affect fuel behavior.

The jet fuel segment captured USD 703.4 million in 2025, underscoring its dominant role within the aviation ecosystem. Continuous additive integration is required to ensure thermal stability, control contamination, and support reliable fuel performance across extended flight durations. The growing complexity of fuel distribution networks and the evolution of fuel compositions further emphasize the need for advanced additive solutions that can adapt to changing operational and technical requirements while maintaining consistency across diverse aviation systems.

North America Aviation Fuel Additives Market is anticipated to grow from USD 384.7 million in 2025 to USD 661 million by 2035, driven by high aviation activity levels and a well-established fueling infrastructure. The region demonstrates strong demand due to continuous flight operations and the need to maintain fuel integrity across large-scale storage and distribution systems. Strict quality standards and operational efficiency requirements encourage ongoing adoption of performance-enhancing additives. Sustained demand is further supported by extensive aviation networks and the need to protect fuel systems from degradation, contamination, and performance inconsistencies over time.

Key companies operating in the Global Aviation Fuel Additives Market include Afton Chemical Corporation, BASF SE, Chevron Corporation, Innospec Chemical Company, LANXESS Deutschland GmbH, Nalco an Ecolab Company, Dorf-Ketal Chemicals India Pvt., Ltd., Meridian Fuels, Biobor Fuel Additives, and A S Harrison & Co. Companies in the Aviation Fuel Additives Market are focusing on advancing formulation technologies to improve performance, compatibility, and environmental compliance. Strategic investments in research and development are enabling the creation of additives that align with next-generation fuel requirements and evolving aviation standards. Market participants are strengthening their supply chains and expanding global distribution networks to ensure consistent product availability. Collaboration with fuel producers and aviation stakeholders is enhancing product integration across the value chain. Firms are also prioritizing precision dosing technologies and digital monitoring solutions to improve application efficiency. Sustainability initiatives, product diversification, and long-term partnerships are further supporting competitive positioning and market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Additive Type

- 2.2.3 Fuel Type

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing commercial and military flight operations

- 3.2.1.2 Need for fuel quality consistency

- 3.2.1.3 Extended fuel storage and transport durations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited additive compatibility with fuels

- 3.2.2.2 Complex fuel logistics and handling requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of sustainable aviation fuels

- 3.2.3.2 Advancements in additive formulation technologies

- 3.2.3.3 Improved fuel system protection requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By additive type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Additive Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dispersants

- 5.3 Antioxidants

- 5.4 Anti-icing

- 5.5 Corrosion inhibitors

- 5.6 Antiknock

- 5.7 Metal deactivators

- 5.8 Others (fuel stabilizers, combustion improvers)

Chapter 6 Market Estimates and Forecast, By Fuel Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Aviation gasoline

- 6.3 Jet fuel

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Commercial aircraft

- 7.3 Passenger aircraft

- 7.4 Cargo aircraft

- 7.5 Military aircraft

- 7.6 Others (private jets, helicopters)

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Afton Chemical Corporation

- 9.2 Chevron Corporation

- 9.3 BASF SE

- 9.4 Biobor Fuel Additives

- 9.5 Dorf-Ketal Chemicals India Pvt., Ltd.

- 9.6 Innospec Chemical Company

- 9.7 Meridian Fuels

- 9.8 Nalco an Ecolab Company

- 9.9 LANXESS Deutschland GmbH

- 9.10 A S Harrison & Co