|

시장보고서

상품코드

2061443

바이오시밀러 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Biosimilars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

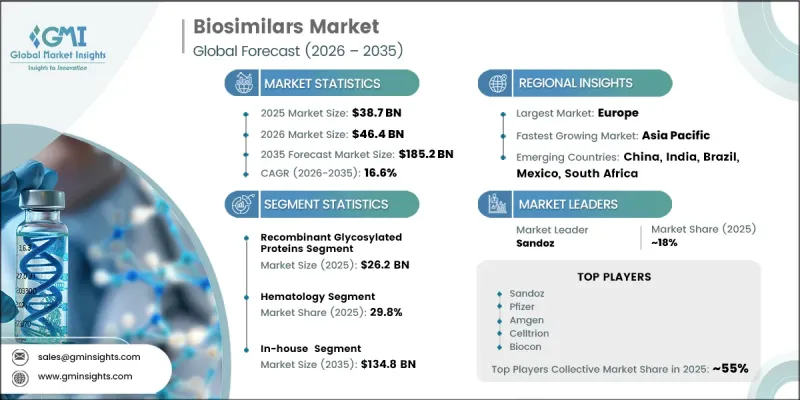

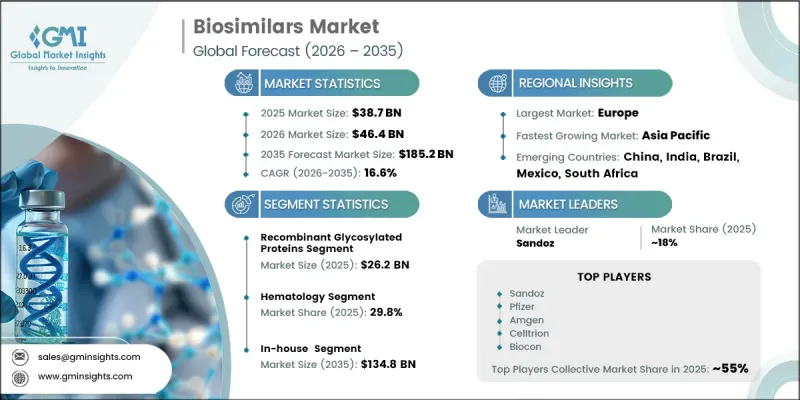

세계의 바이오시밀러 시장은 2025년에 387억 달러로 평가되고 CAGR 16.6%로 성장하며, 2035년까지 1,852억 달러에 달할 것으로 추정되고 있습니다.

이러한 강력한 시장 성장은 합리적인 가격의 생물제제에 대한 수요 증가와 전 세계에서 만성질환 및 복합 질환의 유병률 증가에 힘입어 이루어지고 있습니다. 생물제제를 통한 치료가 필요한 만성질환의 발생률 증가는 의료 시스템 전반에 걸쳐 바이오시밀러의 도입을 현저히 가속화하고 있습니다. 바이오시밀러란, 안전성, 유효성, 품질 면에서 이미 승인된 참조 생물제제와 엄격하게 일치하도록 개발되어, 비용 대비 효과가 더 높은 치료 옵션을 제공하는 생물제제입니다. 이러한 치료법은 환자들이 첨단 생물학적 치료를 더 쉽게 받을 수 있도록 하고, 만성질환 관리에 따르는 경제적 부담을 줄이는 데 있으며, 점점 더 중요한 역할을 하고 있습니다. 선발 생물제제와의 치료적 동등성 및 바이오시밀러성을 입증하기 위해서는 광범위한 임상 평가, 분석 연구 및 규제 당국의 평가가 필요합니다. 의료 종사자와 환자들 사이에서 인식이 높아지고, 유리한 보험 지급 체계, 제품 승인 증가, 그리고 여러 치료 분야에서 바이오시밀러 요법의 광범위한 수용이 예측 기간 중 시장의 급속한 확장에 더욱 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 387억 달러 |

| 예측액 | 1,852억 달러 |

| CAGR | 16.6% |

재조합 당화 단백질 부문은 2025년에 262억 달러에 달했습니다. 이 부문은 만성 및 중증 질환 치료에 사용되는 첨단 생물제제에 대한 수요가 증가함에 따라 업계 내에서 계속해서 큰 점유율을 차지하고 있습니다. 재조합 당화 단백질은 치료 효과에 필요한 정확한 단백질 개발과 필수적인 분자 수정을 가능하게 하는 첨단 재조합 DNA 기술을 이용하여 제조됩니다. 다양한 질환 관리 분야에서 이러한 생물제제의 사용이 확대됨에 따라 해당 부문의 지속적인 성장이 지원되고 있습니다. 생물제제 개발에 대한 투자 증가와 비용 대비 효과가 높은 대체 치료법에 대한 수요 증가도 이 부문의 성장을 지원하고 있습니다.

2025년 기준으로, 혈액학 부문은 29.8%의 점유율을 차지했습니다. 혈액학 분야의 시장 성장은 주로 혈액 관련 질환의 유병률 증가와 합리적인 가격의 생물학적 치료 솔루션에 대한 수요 증가에 힘입어 이루어지고 있습니다. 바이오시밀러는 임상 결과, 안전 기준 및 치료 효과에 대한 신뢰도가 높아짐에 따라 혈액 질환 관리 분야에서 점차 더 널리 채택되고 있습니다. 의료 종사자들 사이에서 바이오시밀러 치료가 가져다주는 경제적·임상적 이점에 대한 인식이 높아지고 있는 점도, 혈액학 치료 현장에서의 활용 확대를 더욱 지원하고 있습니다. 생물제제 치료의 대체 수단에 대한 접근성 확대 또한 이 부문의 지속적인 시장 성장에 기여하고 있습니다.

북미 바이오시밀러 시장은 2025년에 29.9%의 시장 점유율을 차지하며, 2026-2035년 연평균 성장률(CAGR) 16.5%로 성장할 것으로 전망됩니다. 해당 지역에서는 의료비 지출 증가, 저비용 생물제제 치료에 대한 선호도 상승, 그리고 주요 생물제제의 특허 만료가 잇따르고 있는 것을 배경으로, 바이오시밀러의 도입이 계속해서 견고한 추세를 보이고 있습니다. 북미는 효율적인 승인 절차를 지원하고, 의료진과 환자의 바이오시밀러 사용에 대한 신뢰를 높이는 잘 정비된 규제 환경의 혜택을 누리고 있습니다. 치료비 절감을 위한 의료 시스템에 대한 압박이 커지는 데다, 유리한 환급 정책과 처방약 리스트 최적화 전략이 맞물리면서, 해당 지역 전체에서 여러 치료 분야에서 바이오시밀러의 도입이 가속화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035년

제6장 시장 추산·예측 : 용도별, 2022-2035년

제7장 시장 추산·예측 : 제조 유형별, 2022-2035년

제8장 시장 추산·예측 : 기술별, 2022-2035년

제9장 시장 추산·예측 : 유통 채널별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.06.24The Global Biosimilars Market was valued at USD 38.7 billion in 2025 and is estimated to grow at a CAGR of 16.6% to reach USD 185.2 billion by 2035.

Strong market growth is driven by the rising demand for affordable biologic therapies and the increasing prevalence of chronic and complex medical conditions worldwide. The growing incidence of long-term diseases requiring biologic treatment solutions is significantly accelerating biosimilar adoption across healthcare systems. Biosimilars are biologic medicines developed to closely match approved reference biologics in terms of safety, effectiveness, and quality while offering more cost-efficient treatment alternatives. These therapies are playing an increasingly important role in improving patient access to advanced biologic treatments and reducing the financial burden associated with long-term disease management. Extensive clinical assessments, analytical studies, and regulatory evaluations are required to establish therapeutic equivalence and biosimilarity with originator biologics. Expanding awareness among healthcare professionals and patients, favorable reimbursement frameworks, increasing product approvals, and broader acceptance of biosimilar therapies across multiple therapeutic areas are further contributing to rapid market expansion throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $38.7 Billion |

| Forecast Value | $185.2 Billion |

| CAGR | 16.6% |

The Recombinant Glycosylated Proteins segment reached USD 26.2 billion in 2025. This segment continues to hold a substantial share of the industry due to increasing demand for advanced biologic therapies utilized in the treatment of chronic and severe medical conditions. Recombinant glycosylated proteins are manufactured using advanced recombinant DNA technologies that enable accurate protein development and essential molecular modifications required for therapeutic effectiveness. Growing adoption of these biologic therapies across various disease management applications is supporting continued segment expansion. Increasing investments in biologic drug development and rising demand for cost-effective therapeutic alternatives are also strengthening growth within this category.

The hematology segment accounted for a share of 29.8% in 2025. Market growth within hematology applications is primarily driven by the increasing prevalence of blood-related disorders and rising demand for affordable biologic treatment solutions. Biosimilars are being increasingly adopted for the management of hematologic conditions due to growing confidence in their clinical performance, safety standards, and therapeutic effectiveness. Rising awareness among healthcare providers regarding the economic and clinical benefits associated with biosimilar therapies is further supporting broader utilization across hematology treatment settings. Expanding access to biologic treatment alternatives is also contributing to the segment's sustained market growth.

North America Biosimilars Market held 29.9% share in 2025 and is expected to grow at a CAGR of 16.5% during 2026-2035. The region continues to experience strong biosimilar adoption supported by increasing healthcare expenditures, growing preference for lower-cost biologic treatment options, and ongoing patent expirations for several major biologic products. North America benefits from a highly structured regulatory environment that supports efficient approval pathways and strengthens confidence in biosimilar utilization among healthcare professionals and patients. Growing pressure on healthcare systems to reduce treatment costs, along with favorable reimbursement policies and formulary optimization strategies, is accelerating biosimilar adoption across multiple therapeutic applications throughout the region.

Key companies operating in the Global Biosimilars Market include Biocon, Sandoz, Bio-Thera Solutions, Pfizer, Dr. Reddy's Laboratories, Amgen, Teva Pharmaceuticals, Fresenius Kabi, Coherus Biosciences, Apobiologix, Biocad, Intas Pharma, Celltrion, Zydus Cadila, and Samsung Bioepis. Companies operating in the biosimilars market are adopting multiple strategic initiatives to strengthen their competitive position and expand global market presence. Leading industry participants are investing heavily in research and development activities to accelerate biosimilar product launches and improve manufacturing capabilities. Strategic partnerships, licensing agreements, and collaborations with biotechnology firms are enabling companies to expand product portfolios and enhance market reach across various therapeutic areas. Organizations are also focusing on strengthening regulatory compliance and obtaining approvals across international markets to improve commercialization opportunities. Increasing investments in advanced manufacturing technologies, supply chain optimization, and biologics production facilities are further supporting long-term growth strategies. In addition, companies are prioritizing physician education programs, patient awareness initiatives, and competitive pricing strategies to increase biosimilar acceptance and strengthen their foothold within the global biosimilars industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 Manufacturing type trends

- 2.2.5 Technology trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising chronic disease burden

- 3.2.1.2 Increasing biologics patent expirations

- 3.2.1.3 Higher clinician and patient acceptance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited market penetration in some regions

- 3.2.2.2 High development and manufacturing costs

- 3.2.3 Market opportunities

- 3.2.3.1 Advancement in AI-driven bioprocessing

- 3.2.3.2 Adoption of streamlined regulatory pathways

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technology

- 3.5.2 Emerging technologies

- 3.6 Reimbursement landscape

- 3.6.1 U.S.

- 3.6.2 Canada

- 3.6.3 Europe

- 3.6.4 Australia

- 3.6.5 New Zealand

- 3.7 Biosimilar Litigation landscape

- 3.8 Future market trends (Driven by primary research)

- 3.9 Impact of AI and generative AI on the market (Driven by primary research)

- 3.10 Biosimilars factor analysis

- 3.10.1 Access

- 3.10.2 Regulations

- 3.10.3 Payer assessment and access

- 3.10.4 Physician acceptance

- 3.10.5 Patient acceptance

- 3.11 Biosimilar product pipeline analysis

- 3.12 Biosimilars approval scenario, 2022 - 2025

- 3.13 Biologics patent expiry scenario

- 3.14 International policies on use of biosimilar drugs

- 3.14.1 Interchangeability, switching and subsitution

- 3.14.2 Supply side policies

- 3.14.3 Prescribing incentives

- 3.15 Porter's analysis

- 3.16 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 ($ Mn)

- 5.1 Key trends

- 5.2 Recombinant non-glycosylated proteins

- 5.2.1 Human growth hormone

- 5.2.2 Granulocyte colony-stimulating factor (filgrastim)

- 5.2.3 Insulin

- 5.2.4 Interferon

- 5.2.4.1 Alfa

- 5.2.4.2 Beta

- 5.3 Recombinant glycosylated proteins

- 5.3.1 Monoclonal antibodies

- 5.3.1.1 Infliximab

- 5.3.1.2 Rituximab

- 5.3.1.3 Adalimumab

- 5.3.1.4 Trastuzumab

- 5.3.1.5 Bevacizumab

- 5.3.2 Erythropoietin

- 5.3.2.1 Alfa

- 5.3.2.2 Beta

- 5.3.3 Follitropin

- 5.3.3.1 Alfa

- 5.3.3.2 Beta

- 5.3.4 Fusion proteins

- 5.3.1 Monoclonal antibodies

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hematology

- 6.2.1 Neutropenia

- 6.2.2 Anemia

- 6.2.3 Other hematology applications

- 6.3 Oncology

- 6.3.1 Lung cancer

- 6.3.2 Brain cancer

- 6.3.3 Breast cancer

- 6.3.4 Cervical cancer

- 6.3.5 Colorectal cancer

- 6.3.6 Leukemia

- 6.3.7 Other Oncology applications

- 6.4 Autoimmune disease

- 6.4.1 Arthritis

- 6.4.1.1 Rheumatoid arthritis

- 6.4.1.2 Psoriatic arthritis

- 6.4.1.3 Juvenile arthritis

- 6.4.1.4 Ankylosing spondylitis

- 6.4.1.5 Other arthritis

- 6.4.2 Inflammatory bowel disease (IBD)

- 6.4.2.1 Ulcerative colitis

- 6.4.2.2 Crohn's disease

- 6.4.2.3 Other IBD

- 6.4.3 Psoriasis

- 6.4.4 Other autoimmune diseases

- 6.4.1 Arthritis

- 6.5 Ophthalmology

- 6.6 Growth hormone deficiency

- 6.7 Diabetes

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By Manufacturing Type, 2022-2035 ($ Mn)

- 7.1 Key trends

- 7.2 Contract research and manufacturing services

- 7.3 In-house

Chapter 8 Market Estimates and Forecast, By Technology, 2022-2035 ($ Mn)

- 8.1 Key trends

- 8.2 Recombinant DNA technology

- 8.3 Mammalian cell culture systems

- 8.4 Other technologies

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Specialty pharmacies

- 9.4 Other distribution channels

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Biocon

- 11.2 Sandoz

- 11.3 Bio-Thera Solutions

- 11.4 Pfizer

- 11.5 Dr. Reddy’s Laboratories

- 11.6 Amgen

- 11.7 Teva Pharmaceuticals

- 11.8 Fresenius Kabi

- 11.9 Coherus Biosciences

- 11.10 Apobiologix

- 11.11 Biocad

- 11.12 Intas Pharma

- 11.13 Celltrion

- 11.14 Zydus Cadila

- 11.15 Samsung Bioepis