|

시장보고서

상품코드

1802916

폴리비닐부티랄 시장 예측(-2030년) : 용도별, 최종 용도 산업별, 제품 유형별, 수지 유형별, 두께별, 지역별Polyvinyl Butyral Market by Application, Thickness, Resin Type, Product Type, End-use Industry, and Region - Global Forecast to 2030 |

||||||

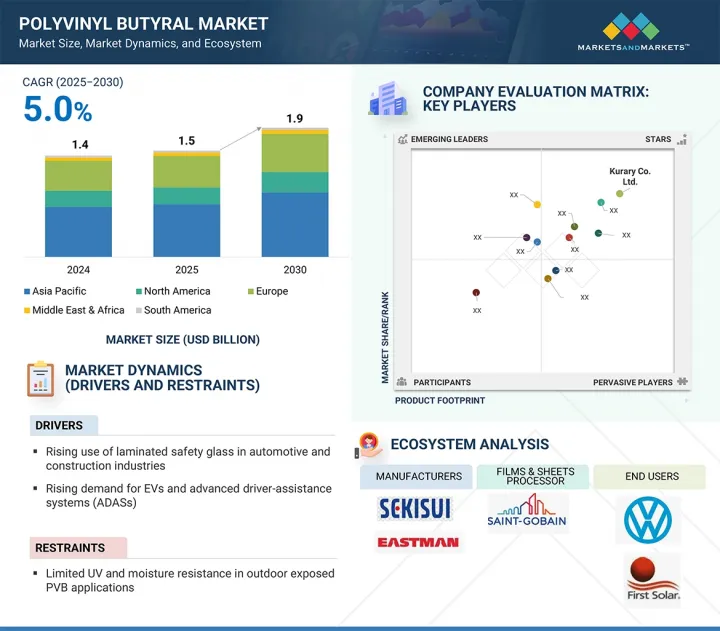

폴리비닐부티랄 시장 규모는 2025년 15억 달러에서 2030년에는 19억 달러로 성장하며, 예측 기간 중 CAGR은 5.0%를 기록할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러/10억 달러) 및 킬로톤 |

| 부문 | 용도별, 최종 용도 산업별, 제품 유형별, 수지 유형별, 두께별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

PVB 산업은 자동차, 건설, 재생에너지 등 주요 산업에서 많은 용도를 가지고 있으며, 괄목할 만한 성장세를 보이고 있습니다. 이러한 성장의 주요 원동력은 접합 안전유리에서 PVB의 사용 확대입니다. PVB는 충격시 유리를 이어주는 중간막 역할을 하여 안전성을 높이고 부상 위험을 줄여줍니다. 자동차 분야에서는 특히 아시아태평양의 자동차 생산량 증가와 법규에 따라 PVB 접합유리가 신차 앞유리, 측면 유리, 선루프에 표준으로 채택되고 있습니다. 또한 소비자의 취향에 따라 방음 유리, 태양광 제어 유리, 에너지 효율이 높은 솔루션에 대한 수요가 증가하고 있습니다.

건축 분야에서는 도시화와 인프라 개발로 인해 안전, 방음, 자외선 차단을 향상시키기 위해 상업용 건물과 주택에서 접합유리의 사용이 증가하고 있습니다. 또한 재생에너지 산업, 특히 태양전지 모듈에서 PVB는 태양전지를 습기 및 기계적 스트레스로부터 보호합니다. 또한 PVB 중간막의 바이오 옵션 및 재활용 컨텐츠와 같은 PVB의 지속적인 기술 혁신은 지속가능성 동향에 부합하며, 더 많은 사람들에게 어필하기 위해 지속적으로 인기를 얻고 있습니다. 이러한 용도와 세계 시장에서 요구되는 필수 제품은 일상 생활에서 PVB 수요의 안정적이고 지속적인 성장을 지원하고 있습니다.

폴리비닐부티랄(PVB) 시장은 자동차, 건축, 재생에너지 등 많은 주요 산업 및 민간부문에서 성공적으로 사용되고 있으며, 꾸준한 성장이 예상됩니다. 자동차 산업은 아시아태평양을 중심으로 생산량이 지속적으로 증가하고 있으며, 동시에 전 세계에서 안전유리 규제가 강화되고 있습니다. 자동차 생산량 증가에 따라 접합 안전유리에 대한 수요가 증가하고 있으며, PVB는 그 주요 부재 중 하나입니다. 건설 분야는 인도, 중국, 브라질 등의 급속한 도시화와 현대화, 유럽 각국의 에너지 효율 및 환경 기준 강화로 PVB 수요를 견인하고 있습니다. 재생에너지 발전 분야에서는 재생에너지를 생산하는 태양전지판의 태양전지를 보호하기 위해 PVB를 사용하는 경우가 많기 때문에 PVB 소비량 증가에 기여하고 있습니다. 다양한 재활용 공정과 과제가 있으므로 기업은 엄격한 규제와 원자재 가격 상승 속에서 경쟁력을 유지하기 위해 새로운 재활용 방법에 투자하고 PVB 생산을 보다 지속가능하게 만들기 위해 자원을 투입해야 합니다.

폴리비닐부티랄(PVB) 시장에서는 자동차, 건축 등 대부분의 주요 최종사용자 분야에서 성능, 비용, 규제 준수 측면에서 최적의 균형을 이루는 표준 필름 분야가 급성장할 것으로 예측됩니다. 일반적인 PVB 필름의 공칭 두께는 0.76mm로 접합 안전 유리의 업계 표준으로 간주됩니다. 크래레(Trosifol), 이스트만(Saflex) 등 업계 관계자들은 이 공칭 두께 범위에서 우수한 내충격성, 광학 투명성, 차음성, 자외선 차단 등 글레이징 용도에 필수적인 특성을 얻을 수 있다고 말합니다. 자동차 업계에서는 세계 충돌 테스트 기준을 충족하고(음향) 쾌적성 규제를 충족하기 위해 앞 유리와 창문에 표준 필름이 널리 사용되고 있습니다. 또한 전기자동차의 경우 차량내 소음을 줄이고 운전 경험을 향상시키기 위해 표준 두께의 방음 PVB의 사용이 증가하고 있음을 시사하고 있습니다. 건축 산업에서는 학교부터 오피스 타워에 이르기까지 모든 유형의 건축물의 외관과 창문에 PVB 필름이 사용되고 있으며, 빠른 접착, 자동화된 생산 라인, 에너지 효율 준수, 내충격성 등의 안전 기준이 요구되고 있습니다. 초박형 및 두꺼운 중간막과 달리 표준 막은 실용적인 중간 영역을 제공하고 더 많은 기능적 요구를 충족시키는 동시에 더 비용 효율적이고 확장 가능한 생산이 가능하므로 표준 막은 가장 빠르게 성장하는 하위 부문이 되었습니다.

중금속, 질산염, 기타 무기 오염물질 처리의 필요성으로 인해 무기 오염물질은 폴리비닐부티랄(EO) 시장에서 가장 빠르게 성장하고 있는 용도입니다. EO는 직접적인 전자 이동 또는 반응성 종의 생성에 의한 산화 또는 환원에 의해 무기물을 제거하며, 무기물 처리는 기존의 방법으로 제거 요구를 충족시킬 수 없는 경우에 매우 효과적입니다. 산업 관행의 변화와 규제 강화로 인해 EO는 주로 아시아태평양에서 최고의 처리 기술로 부상하고 있습니다. 이 지역에서는 광업, 화학, 전자 산업이 오염물질, 특히 중금속의 엄격한 배출 기준을 충족해야 하는데, 이는 중국의 산업 폐수 및 광업의 시범적인 노력과 인도의 폐수 배출 기준에 대한 폐수 배출 제로 요소를 가진 광업 사업에서 볼 수 있습니다. 북미에서는 질산염 오염에 대한 농업 규제가 변경되어 농업 폐수 및 지하수를 대상으로 하는 것으로 변경됨에 따라 효과적이고 효율적인 질산염 처리를 위해 이산화 납과 티타늄 전극을 사용한 EO 파일럿의 사용이 증가하고 있습니다. 유럽에서는 도시 폐수 처리 지침과 산업 폐수 중 무기 오염물질을 포함한 오염 방지를 위한 요구 사항으로 인해 화학 공장에서의 EO 적용에 대한 관심이 높아지고 있습니다. 또한 아프리카, 남미, 라틴아메리카 국가들의 광산 활동의 성장도 세계은행의 지원을 받아 중금속이 함유된 산성 광산 폐수를 처리할 수 있는 EO 처리에 대한 수요를 촉진하고 있습니다.

수지 유형별로 분류된 폴리비닐부티랄(PVB) 시장의 주요 소재는 고분자량 PVB 수지이며, 예상 수지 성장률로 볼 때 가장 빠르게 성장하고 있습니다. 고분자량 PVB 수지 부문의 성공적인 비즈니스는 고급 성능 특성으로 인해 운송, 건축, 건설 및 전자 산업에서 사용하기에 추가적인 장벽을 제공합니다. 저분자량 및 중분자량 PVB 수지에 비해 고분자량 수지는 기계적 강도, 탄성, 접착력, 열 안정성이 우수합니다. 이러한 고유한 특성은 접합 안전유리에 사용될 때 필수적이며, 중간막의 강도와 내구성에 대한 요구가 높아지고, 주거 및 상업 분야에서 여러 단체가 정한 안전, 위생, 환경 및 제품 책임에 대한 기준이 점점 더 엄격해지는 추세에 따라 접합 안전유리에 사용되는 것이 필수적입니다.

기술 간행물을 포함한 업계 전반의 정보원에 따르면 고분자량 수지는 접합 안전 유리에 사용될 때 더 나은 방음 특성을 가지고 있으며, 박리에 강합니다. 이러한 추세는 전기자동차, 일류 설계사무소의 정교한 건축 설계로 이어지고 있습니다. 향후 안전유리 사양과 방음, 자외선 차단, 에너지 효율을 포함한 첨단 디자인의 다기능 글레이징의 개발 동향도 있습니다. 최근 수지 배합 기술의 혁신으로 제조업체는 가공성과 기존 접합유리 장비와의 호환성을 개선한 고분자량의 PVB를 생산할 수 있게 되었습니다. 건축, 자동차, 전자 산업에서 고성능, 장수명 소재에 대한 수요가 전 세계에서 증가하고 있으며, "고분자량" PVB 수지의 전망은 여전히 유망합니다.

세계의 폴리비닐부티랄 시장에 대해 조사했으며, 용도별, 최종 용도 산업별, 제품 유형별, 수지 유형별, 두께별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 생성형 AI의 영향

- 폴리비닐부티랄 시장에서 생성형 AI의 영향

제6장 업계 동향

- 서론

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 밸류체인 분석

- 가격 분석

- 투자 상황과 자금조달 시나리오

- 에코시스템 분석

- 기술 분석

- 특허 분석

- 무역 분석

- 2024-2025년의 주요 컨퍼런스와 이벤트

- 관세와 규제 상황

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 거시경제 전망

- 사례 연구

제7장 폴리비닐부티랄 시장(용도별)

- 서론

- 필름과 시트

- 페인트와 코팅

- 접착제

- 기타

제8장 폴리비닐부티랄 시장(최종 용도 산업별)

- 서론

- 자동차

- 건설

- 전기·전자

- 기타

제9장 폴리비닐부티랄 시장(제품 유형별)

- 서론

- 분말·과립

- 기타

제10장 폴리비닐부티랄 시장(수지 유형별)

- 서론

- 고분자량 등급 PVB 수지

- 중분자량 등급 PVB 수지

- 저분자량 등급 PVB 수지

- 개질 PVB 수지

제11장 폴리비닐부티랄 시장(두께별)

- 서론

- 초박막

- 스탠다드 필름

- 미드레인지 필름

- 두껍고 복합적인 중간층

제12장 폴리비닐부티랄 시장(지역별)

- 서론

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 이탈리아

- 프랑스

- 영국

- 스페인

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제13장 경쟁 구도

- 서론

- 주요 참여 기업의 전략/강점

- 시장 점유율 분석, 2024년

- 매출 분석

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 참여 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가와 재무 지표, 2024년

- 경쟁 시나리오

제14장 기업 개요

- 주요 참여 기업

- KURARAY CO., LTD.

- EASTMAN CHEMICAL COMPANY

- SEKISUI CHEMICAL CO., LTD.

- HUBERGROUP

- CHANG CHUN GROUP

- VIZAGCHEMICAL

- KINGBOARD(FOGANG) SPECIALITY RESINS LIMITED

- EVERLAM

- HUAKAI PLASTIC(CHONGQING) CO., LTD.

- TRIDEV GROUP

- 기타 기업

- QINGDAO JIAHUA PLASTICS CO., LTD

- SIVA CHEMICAL INDUSTRIES

- TANYUN JUNRONG(LIAONING) CHEMICAL RESEARCH INSTITUTE NEW MATERIALS INCUBATOR CO., LTD.

- SYNPOL PRODUCTS PVT LTD.

- UNIFORM SYNTHETICS PRIVATE LIMITED

- D.R. COATS INK & RESINS PVT. LTD

- HUZHOU XINFU NEW MATERIALS CO., LTD.

- QINGDAO HAOCHENG INDUSTRIAL COMPANY LIMITED

- ZHEJIANG PULIJIN PLASTIC CO., LTD.

- TIANTAI KANGLAI INDUSTRIAL CO., LTD

- PERSTORP

- ATAMAN KIMYA A.S.

- WEGO CHEMICAL GROUP

- JAINISH INDUSTRIES

- SINOEVER INTERNATIONAL CO., LTD.

제15장 부록

KSA 25.09.08The polyvinyl butyral market is projected to grow from USD 1.5 billion in 2025 to USD 1.9 billion by 2030, registering a CAGR of 5.0% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) and Kiloton |

| Segments | Resin Type, Product Type, Thickness, Application, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

The PVB industry is experiencing significant growth with many applications across major industries such as automotive, construction, and renewable energy. A key driver of this growth is the rising use of PVB in laminated safety glass, where PVB acts as an interlayer to hold glass together upon impact, enhancing safety and reducing injury risk. In the automotive sector, increased vehicle production-especially in the Asia Pacific region-and regulatory requirements mean PVB laminated glass is now standard in new vehicles for windshields, side windows, and sunroofs. Additionally, there is growing demand for acoustic and solar-control glazing and energy-efficient solutions, driven by consumer preferences.

In construction, urbanization and infrastructure development are boosting the use of laminated glass in both commercial and residential buildings to improve safety, noise insulation, and UV protection. The use of PVB in laminated glass is also an important factor in the renewable energy industry, especially in photovoltaic modules, where PVB protects solar cells from moisture and mechanical stress. Additionally, ongoing innovation of PVB, including bio-based options and recycled content for laminated PVB interlayers, aligns with sustainability trends and continues to grow in popularity to appeal to a broader demographic. These applications and essential products needed in the global market support steady and consistent growth in demand for PVB in our daily lives.

"Powder & granules segment to be fastest-growing product type segment of polyvinyl butyral market during forecast period"

The polyvinyl butyral (PVB) market is poised for steady growth due to its successful use in many major industrial and private sector applications across automotive, construction, and renewable energy. The automotive industry has continued to increase production, especially in the Asia Pacific region, while also becoming subject to stricter safety glass regulations worldwide. As vehicle manufacturing rises, the need for laminated safety glass will grow, with PVB being a key component. The construction sector also drives PVB demand due to rapid urbanization and modernization in countries like India, China, and Brazil, along with stricter energy efficiency and environmental standards in many European nations. The renewable energy sector contributes to increased PVB consumption since it is often used to protect photovoltaic cells in solar panels that generate renewable energy. Due to different recycling processes and challenges, companies must invest in new recycling methods and commit resources to making PVB production more sustainable to stay competitive amid strict regulations and rising raw material costs.

"Standard films to be fastest-growing segment of polyvinyl butyral market in terms of value"

The standard film segment is projected to witness fast growth in the polyvinyl butyral (PVB) market due to its optimal balance of performance, cost, and regulation compliance across most major end-user sectors, such as automotive and construction. Standard PVB films typically have a nominal thickness of 0.76 mm and are regarded as the industry standard for laminated safety glass. Industry sources like Kuraray (Trosifol) and Eastman (Saflex) have stated that this nominal thickness range provides good impact resistance, optical clarity, sound insulation, and UV protection-all essential characteristics for glazing applications. In the automotive industry, standard films are widely used in windshields and windows to ensure they pass global crash test standards and meet (acoustic) comfort regulations. They also suggest that the use of acoustic PVBs, within standard thicknesses, is increasing in electric vehicles to reduce cabin noise and enhance the driving experience. In the architecture industry, all types of buildings, from schools to office towers, utilize PVB films in facades and windows where quick adherence, automated production lines, energy efficiency compliance, and safety standards like impact resistance are required. Unlike ultra-thin or thick interlayers, standard films provide a practical middle ground, meeting more functional needs while enabling more cost-effective and scalable production; thus, standard films have become the fastest-growing sub-segment.

"Inorganic pollutants treatment to be fastest-growing in electrode material segment of polyvinyl butyral market in terms of value"

Inorganic pollutants are the fastest-growing application segment in the Polyvinyl butyral (EO) market due to the need to treat heavy metals, nitrates, and other inorganic contaminants. EO removes inorganics through oxidation or reduction by direct electron transfer or reactive species generation, and treatment of inorganics can be highly effective when traditional methods cannot meet removal needs. Due to changes in industrial practices and stricter regulations, EO is mainly emerging as the best treatment technology in the Asia-Pacific region, where industries in mining, chemicals, and electronics must meet stringent discharge standards for pollutants, especially heavy metals, as seen in pilots in China's industrial wastewater and mining industries, and in India, where mining operations have a zero-liquid discharge component to wastewater discharge standards. Changes in North America's agricultural regulations for nitrate contamination, which now target agricultural runoff and groundwater, have increased the use of EO pilots using lead dioxide or titanium electrodes for effective and efficient nitrate treatment. In Europe, the Urban Waste Water Treatment Directive and its requirements for pollution prevention, including inorganic contaminants in industrial discharges, have generated interest in EO applications in chemical plants. The growth of mining activities in countries across Africa, South America, and Latin America has also driven demand for EO treatment, as it can treat acidic mine drainage with heavy metals, with support from the World Bank.

"Higher molecular weight PVB resin to be fastest-growing resin type segment of polyvinyl butyral market in terms of value"

The leading materials in the polyvinyl butyral (PVB) market, classified by resin type, are the higher molecular weight PVB resins, which are the fastest-growing based on expected resin growth rates. The success of businesses in the higher molecular weight PVB resin segment is due to their advanced performance features, offering extra barriers for use in transportation, building, construction, and electronics industries. Compared to low or medium molecular weight PVB resins, higher molecular weight variants deliver superior mechanical strength, elasticity, adhesion, and thermal stability. These unique qualities are essential when used in laminated safety glass, as there are increased demands for interlayer strength and durability, along with a trend toward stricter safety, health, environmental, and product liability standards set by multiple organizations in the residential and commercial sectors.

Sources across the industry, including technical publications, indicate that higher molecular weight resin choices have better acoustic dampening characteristics when used in laminated safety glass and are more resistant to delamination. This is recommended for electric vehicles and as the trend continues among leading design firms for exquisite architectural design. There is even a developing trend toward multi-functional glazing that will have future specifications for safety glass and advanced designs that include sound insulation, ultraviolet shielding, and energy efficiency. Recent innovations in resin formulation technologies have enabled manufacturers to produce higher molecular weight PVBs with improved processability and compatibility with existing laminated glass equipment. With the increasing global demand for materials that deliver high performance and longer service life across the construction, automotive, and electronics industries, the outlook for "high molecular weight" PVB resin remains promising.

In-depth interviews were conducted with Chief Executive Officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the polyvinyl butyral market. Additionally, information was gathered from secondary research to determine and verify the market size of several segments.

- By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

- By Designation: Managers- 15%, Directors - 20%, and Others - 65%

- By Region: North America - 25%, Europe - 15%, Asia Pacific - 45%, Middle East & Africa - 10%, South America - 5%.

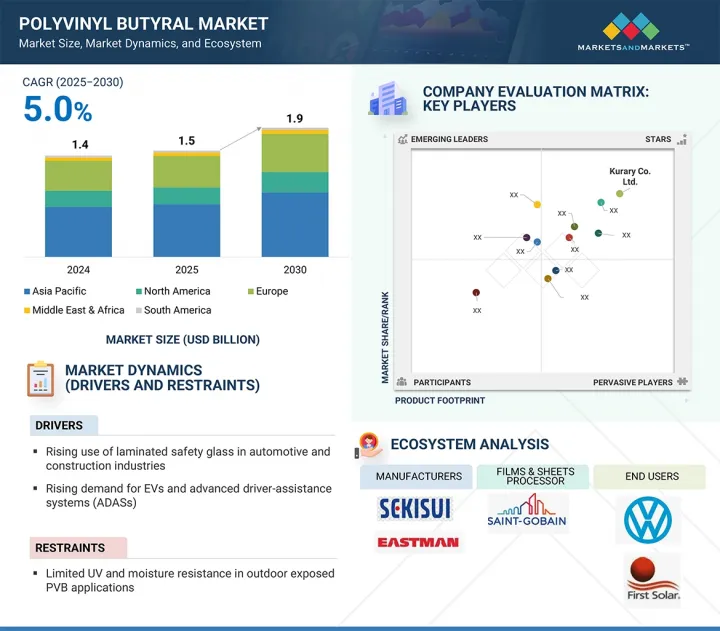

Key players in the polyvinyl butyral market include Sekisui Chemical Co. Ltd. (Japan), Kuraray Co. Ltd. (Japan), Eastman Chemical Company (US), Hubergroup (US), Chang Chun Group (China), Anhui WanWei Bisheng New Material Co., Ltd. (China), Kingboard Fogang Specialty Resin Co., Ltd (China), Qingdao Jinuo New Materials Co., Ltd. (China), Huakai Plastic Co. Ltd. (China), and Everlam (Belgium). The study provides an in-depth competitive analysis of these key players in the Polyvinyl Butyral market, including their company profiles, recent developments, and main market strategies.

Research Coverage

This report segments the market for polyvinyl butyral based on resin type, thickness, product type, end-use industry, application, and region, and provides estimates for the overall market value across different regions. A detailed analysis of key industry players is included to offer insights into their business overviews, products and services, key strategies, and expansions related to the polyvinyl butyral market.

Key benefits of buying this report

This research report focuses on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the polyvinyl butyral market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of drivers rising demand of EVs and advanced driver-assistant systems (ADAS) driving high-performance PVB adoption), restraints (Limited UV and moisture resistance in outdoor exposed PVB applications), opportunities (expanding recycled PVB (rPVB) adoption in industrial and infrastructure materials), and challenges (regulatory pressure on plasticizer formulations and VOC emission in PVB manufacturing).

- Market Penetration: Comprehensive information on the polyvinyl butyral market offered by top players.

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, partnerships, agreements, joint ventures, collaborations, announcements, awards, and expansions in the market.

- Market Development: Comprehensive information about lucrative emerging markets across regions.

- Market Capacity: Wherever possible, the production capacities of companies producing polyvinyl butyral are provided, along with upcoming capacities for the polyvinyl butyral market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the polyvinyl butyral market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key primary sources

- 2.1.2.3 Key participants in primary interviews

- 2.1.2.4 Breakdown of primary interviews

- 2.1.2.5 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 BASE NUMBER CALCULATION

- 2.2.1 SUPPLY-SIDE ANALYSIS

- 2.2.2 DEMAND-SIDE ANALYSIS

- 2.3 GROWTH FORECAST

- 2.3.1 SUPPLY SIDE

- 2.3.2 DEMAND SIDE

- 2.4 MARKET SIZE ESTIMATION

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- 2.6 FACTOR ANALYSIS

- 2.7 RESEARCH ASSUMPTIONS

- 2.8 GROWTH FORECAST

- 2.9 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POLYVINYL BUTYRAL MARKET

- 4.2 POLYVINYL BUTYRAL MARKET, BY PRODUCT TYPE

- 4.3 POLYVINYL BUTYRAL MARKET, BY RESIN TYPE

- 4.4 POLYVINYL BUTYRAL MARKET, BY THICKNESS

- 4.5 POLYVINYL BUTYRAL MARKET, BY APPLICATION

- 4.6 POLYVINYL BUTYRAL MARKET, BY END-USE INDUSTRY

- 4.7 POLYVINYL BUTYRAL MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Mandatory use of laminated safety glass in architectural and automotive applications

- 5.2.1.2 Rise in demand for EVs and advanced driver-assistance systems (ADAS)

- 5.2.1.3 Shift toward building-integrated photovoltaics (BIPV) using PVB-encapsulated laminated glass

- 5.2.1.4 Growth in acoustic and decorative glass installations in high-end construction

- 5.2.2 RESTRAINTS

- 5.2.2.1 Limited UV and moisture resistance in outdoor-exposed PVB applications

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expansion of recycled PVB (rPVB) adoption in industrial and infrastructure materials

- 5.2.3.2 Smart glass & dynamic glazing integration

- 5.2.4 CHALLENGES

- 5.2.4.1 Regulatory pressure on plasticizer formulations and VoC emissions in PVB manufacturing

- 5.2.1 DRIVERS

- 5.3 IMPACT OF GENERATIVE AI

- 5.3.1 INTRODUCTION

- 5.4 IMPACT OF GENERATIVE AI ON POLYVINYL BUTYRAL MARKET

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.3 VALUE CHAIN ANALYSIS

- 6.3.1 RAW MATERIAL SUPPLIERS

- 6.3.2 PVB RESIN PRODUCTION

- 6.3.3 FILM/CAST SHEET PROCESSING

- 6.3.4 END USERS

- 6.4 PRICING ANALYSIS

- 6.4.1 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2024

- 6.4.2 AVERAGE SELLING PRICE TREND, BY RESIN TYPE, 2021-2024

- 6.4.3 AVERAGE SELLING PRICE TREND AMONG POLYVINYL BUTYRAL KEY PLAYERS, BY RESIN TYPE, 2021-2024

- 6.5 INVESTMENT LANDSCAPE AND FUNDING SCENARIO

- 6.6 ECOSYSTEM ANALYSIS

- 6.7 TECHNOLOGY ANALYSIS

- 6.7.1 KEY TECHNOLOGIES

- 6.7.2 COMPLEMENTARY TECHNOLOGIES

- 6.7.3 ADJACENT TECHNOLOGIES

- 6.8 PATENT ANALYSIS

- 6.8.1 METHODOLOGY

- 6.8.2 PATENTS GRANTED WORLDWIDE, 2015-2024

- 6.8.3 PATENT PUBLICATION TRENDS

- 6.8.4 INSIGHTS

- 6.8.5 LEGAL STATUS OF PATENTS

- 6.8.6 JURISDICTION ANALYSIS

- 6.8.7 TOP APPLICANTS

- 6.8.8 LIST OF MAJOR PATENTS

- 6.9 TRADE ANALYSIS

- 6.9.1 IMPORT SCENARIO (HS CODE 392091)

- 6.9.2 EXPORT SCENARIO (HS CODE 392091)

- 6.10 KEY CONFERENCES AND EVENTS, 2024-2025

- 6.11 TARIFF AND REGULATORY LANDSCAPE

- 6.11.1 TARIFF AND REGULATIONS RELATED TO POLYVINYL BUTYRAL MARKET

- 6.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.11.3 REGULATIONS RELATED TO POLYVINYL BUTYRAL MARKET

- 6.12 PORTER'S FIVE FORCES ANALYSIS

- 6.12.1 THREAT OF NEW ENTRANTS

- 6.12.2 THREAT OF SUBSTITUTES

- 6.12.3 BARGAINING POWER OF SUPPLIERS

- 6.12.4 BARGAINING POWER OF BUYERS

- 6.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.13.2 BUYING CRITERIA

- 6.14 MACROECONOMIC OUTLOOK

- 6.14.1 GDP TRENDS AND FORECASTS, BY COUNTRY

- 6.15 CASE STUDY

- 6.15.1 ECO-FRIENDLY INNOVATION IN TEXTILE COATINGS: MODIFIED RECYCLED POLYVINYL BUTYRAL (RPVB) FOR TRADEMARK RIBBON APPLICATIONS

- 6.15.2 INVESTIGATING BUBBLE FORMATION MECHANISMS IN LAMINATED SAFETY GLASS (LSG)

- 6.15.3 BIOCOMPATIBLE COMPOSITES OF RECYCLED PVB AND HDPE: SAFETY EVALUATION FOR HUMAN CELL COMPATIBILITY

7 POLYVINYL BUTYRAL MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.2 FILMS & SHEETS

- 7.2.1 RISING GROWTH OF PVB IS SUPPORTED BY URBANIZATION AND INFRASTRUCTURE PROJECTS IN DEVELOPING COUNTRIES

- 7.3 PAINTS & COATINGS

- 7.3.1 INDIA'S SMART CITY PROJECTS UNDERSCORE POTENTIAL FOR PVB-BASED COATINGS IN PROTECTIVE APPLICATIONS

- 7.4 ADHESIVES

- 7.4.1 GROWING EMPHASIS ON LIGHTWEIGHT VEHICLES AND RENEWABLE ENERGY INFRASTRUCTURE TO DRIVE DEMAND

- 7.5 OTHER END-USE INDUSTRIES

- 7.5.1 WASH PRIMERS

- 7.5.1.1 Rising demand for advanced metal protection solutions to influence demand

- 7.5.2 CERAMIC BINDERS

- 7.5.2.1 Rising demand for high-performance ceramics across electronics, renewable energy, and industrial sectors to drive market

- 7.5.3 COMPOSITE FIBERS

- 7.5.3.1 Shift towards lightweight and high performance materials to drive demand for PVB materials

- 7.5.1 WASH PRIMERS

8 POLYVINYL BUTYRAL MARKET, BY END-USE INDUSTRY

- 8.1 INTRODUCTION

- 8.2 AUTOMOTIVE

- 8.2.1 RISING DEMAND FOR ADVANCED SAFETY GLASS IN EVS AND AUTONOMOUS VEHICLES

- 8.3 CONSTRUCTION

- 8.3.1 MANDATORY REGULATORY COMPLIANCE FOR GREEN BUILDING CODES AND ENERGY-EFFICIENT INFRASTRUCTURE

- 8.4 ELECTRICAL & ELECTRONICS

- 8.4.1 ADVANCING SHIFT TO SOLAR ENERGY AND CLEAN ELECTRONICS

- 8.5 OTHER END-USE INDUSTRIES

- 8.5.1 MILITARY & DEFENSE

- 8.5.1.1 Advancements in lightweight armor technology and composite glazing systems

- 8.5.2 RAIL & MASS TRANSIT

- 8.5.2.1 Expansion of metro networks, high-speed trains, and light rail systems

- 8.5.3 CONSUMER GOODS & WEARABLES

- 8.5.3.1 Lenses laminated with PVB in designer sunglasses improve visual clarity and extend product durability

- 8.5.4 CONSUMER ELECTRONICS

- 8.5.4.1 Demand for sustainable, durable, and visually appealing components

- 8.5.1 MILITARY & DEFENSE

9 POLYVINYL BUTYRAL MARKET, BY PRODUCT TYPE

- 9.1 INTRODUCTION

- 9.2 POWDER & GRANULES

- 9.2.1 VERSATILITY AND DIVERSE APPLICATIONS OF POWDER & GRANULATED PVB RESIN TO DRIVE DEMAND

- 9.3 OTHER PRODUCT TYPES

- 9.3.1 AQUEOUS DISPERSIONS

- 9.3.1.1 Increase in demand for green and sustainable coatings to drive market

- 9.3.2 RESIN SOLUTIONS

- 9.3.2.1 Resin solutions of PVB resin enable precision in electronics and optical applications

- 9.3.1 AQUEOUS DISPERSIONS

10 POLYVINYL BUTYRAL MARKET, BY RESIN TYPE

- 10.1 INTRODUCTION

- 10.2 HIGHER MOLECULAR WEIGHT GRADE PVB RESIN

- 10.2.1 UTMOST STRENGTH AND RESISTANCE AT BREAK

- 10.3 MEDIUM MOLECULAR WEIGHT GRADE PVB RESIN

- 10.3.1 SPECIALLY USED IN SAFETY GLAZING APPLICATIONS, WHICH OFFER LOW-COST SOLUTIONS

- 10.4 LOWER MOLECULAR WEIGHT GRADE PVB RESIN

- 10.4.1 VERSATILE USE OF LOW MOLECULAR WEIGHT GRADE PVB RESIN IN MULTIPLE APPLICATIONS

- 10.5 MODIFIED PVB RESIN

- 10.5.1 GROWING INTEREST IN VALUE-ADDED GLASS PRODUCTS IN RENEWABLE ENERGY SECTOR

11 POLYVINYL BUTYRAL MARKET, BY THICKNESS

- 11.1 INTRODUCTION

- 11.2 ULTRA-THIN FILMS

- 11.2.1 INCREASED USE IN DECORATIVE GLASS MARKET TO DRIVE DEMAND

- 11.3 STANDARD FILMS

- 11.3.1 RISING URBANIZATION, GROWING AUTOMOTIVE MANUFACTURING, AND STRENGTHENED REGULATORY ENFORCEMENT OF SAFETY STANDARDS TO DRIVE MARKET

- 11.4 MID-RANGE FILMS

- 11.4.1 ONGOING INNOVATION WITHIN MODERN GLAZING SYSTEMS TO INCREASE DEMAND

- 11.5 THICK & COMPOSITE INTERLAYERS

- 11.5.1 INCREASE IN DEMAND AT PREMIUM END OF PVB MARKET TO DRIVE GROWTH

12 POLYVINYL BUTYRAL MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Regulatory push for sustainability to drive polyvinyl butyral adoption

- 12.2.2 JAPAN

- 12.2.2.1 Harnessing technological advancements to propel polyvinyl butyral market growth

- 12.2.3 INDIA

- 12.2.3.1 Capitalizing on sustainability focus to boost polyvinyl butyral market growth

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Utilizing technological innovation in electronics market to accelerate polyvinyl butyral market growth

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Capitalizing on stringent regulatory frameworks to drive polyvinyl butyral market growth

- 12.3.2 CANADA

- 12.3.2.1 Sustainability focus to propel polyvinyl butyral market growth

- 12.3.3 MEXICO

- 12.3.3.1 Regulatory alignment to drive polyvinyl butyral market growth

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Leveraging sustainable plastic solutions to drive demand for polyvinyl butyral

- 12.4.2 ITALY

- 12.4.2.1 Sustainability commitment to boost polyvinyl butyral market growth

- 12.4.3 FRANCE

- 12.4.3.1 Growing demand for polyvinyl butyral packaging, textile, and automotive industries to propel market growth

- 12.4.4 UK

- 12.4.4.1 Growing focus on renewable energy and alignment with stringent European regulatory standards to drive polyvinyl butyral market

- 12.4.5 SPAIN

- 12.4.5.1 Favorable climate and adherence to stringent European regulations to drive demand of polyvinyl butyral

- 12.4.6 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 Sustainability initiative to drive polyvinyl butyral market growth

- 12.5.1.2 UAE

- 12.5.1.2.1 Strong incentives and policies supporting sustainability initiatives to drive market

- 12.5.1.3 Rest of GCC countries

- 12.5.1.1 Saudi Arabia

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Rapid expansion of utility-scale solar farms increases need for high-quality materials

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 SOUTH AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Growing housing initiative and infrastructure program to drive market for PVB

- 12.6.2 ARGENTINA

- 12.6.2.1 Growing wind and solar projects to drive market for PVB

- 12.6.3 REST OF SOUTH AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.3 MARKET SHARE ANALYSIS, 2024

- 13.4 REVENUE ANALYSIS

- 13.5 BRAND/PRODUCT COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.6.5.1 Company footprint

- 13.6.5.2 Product type footprint

- 13.6.5.3 Application footprint

- 13.6.5.4 End-use industry footprint

- 13.6.5.5 Region footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.7.5.1 Detailed list of key startups/SMEs

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS, 2024

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 DEALS

- 13.9.2 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 KURARAY CO., LTD.

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.3.4 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 EASTMAN CHEMICAL COMPANY

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths/Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 SEKISUI CHEMICAL CO., LTD.

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths/Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 HUBERGROUP

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.3.2 Deals

- 14.1.4.3.3 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths/Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 CHANG CHUN GROUP

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 MnM view

- 14.1.5.3.1 Right to win

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses and competitive threats

- 14.1.6 VIZAGCHEMICAL

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.7 KINGBOARD (FOGANG) SPECIALITY RESINS LIMITED

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.8 EVERLAM

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.9 HUAKAI PLASTIC (CHONGQING) CO., LTD.

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Deals

- 14.1.10 TRIDEV GROUP

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.1 KURARAY CO., LTD.

- 14.2 OTHER PLAYERS

- 14.2.1 QINGDAO JIAHUA PLASTICS CO., LTD

- 14.2.2 SIVA CHEMICAL INDUSTRIES

- 14.2.3 TANYUN JUNRONG (LIAONING) CHEMICAL RESEARCH INSTITUTE NEW MATERIALS INCUBATOR CO., LTD.

- 14.2.4 SYNPOL PRODUCTS PVT LTD.

- 14.2.5 UNIFORM SYNTHETICS PRIVATE LIMITED

- 14.2.6 D.R. COATS INK & RESINS PVT. LTD

- 14.2.7 HUZHOU XINFU NEW MATERIALS CO., LTD.

- 14.2.8 QINGDAO HAOCHENG INDUSTRIAL COMPANY LIMITED

- 14.2.9 ZHEJIANG PULIJIN PLASTIC CO., LTD.

- 14.2.10 TIANTAI KANGLAI INDUSTRIAL CO., LTD

- 14.2.11 PERSTORP

- 14.2.12 ATAMAN KIMYA A.S.

- 14.2.13 WEGO CHEMICAL GROUP

- 14.2.14 JAINISH INDUSTRIES

- 14.2.15 SINOEVER INTERNATIONAL CO., LTD.

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS