|

시장보고서

상품코드

2070356

콜드체인 시장 : 유형별, 용도별, 온도 구분별, 기술별, 지역별 - 세계 예측(-2031년)Cold Chain Market By Type, Temperature Type (Chilled, Frozen, and Deep-frozen), Application (Food & Beverages, Pharmaceuticals), Technology (Blast Freezing, Vapor Compression, Programmable Logic Controller), and Region - Global Forecast to 2031 |

||||||

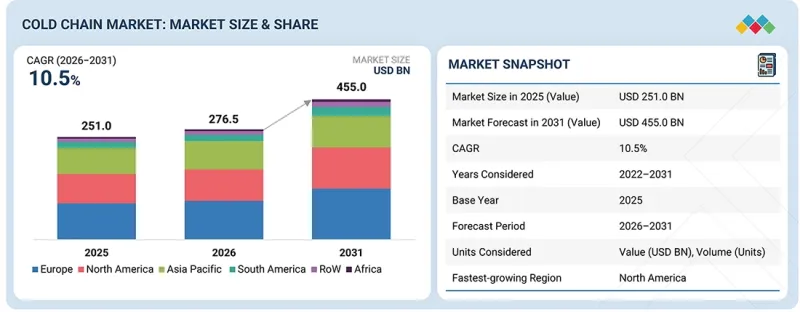

콜드체인 시장 규모는 2026년에 2,765억 달러로 추정되며, 2026년부터 2031년까지 CAGR 10.5%로 확대되어 2031년에는 4,550억 달러에 달할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(달러), 톤 |

| 부문 | 유형별, 용도별, 온도 구분별, 기술별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미 및 기타 지역 |

온도 관리 물류는 많은 산업 분야에서 그 중요성이 점점 더 커지고 있으며, 그 결과 시장은 눈부신 성장을 이루고 있습니다. 의료 업계에서는 의약품과 백신이 안전하고 유효한 상태를 유지하기 위해 적절한 온도 관리를 하는 것이 매우 중요합니다. 온도의 영향을 받기 쉬운 의약품의 수가 증가함에 따라, 적절한 콜드체인 체계의 구축이 요구되고 있습니다.

식품·음료 업계에서는 신선식품의 보존 및 유통기한 연장을 위해 콜드체인 프로세스가 필수적이며, 이를 통해 유제품, 육류, 수산물, 과일, 채소, 주스 및 기타 음료와 같은 신선식품의 손실을 최소화할 수 있습니다. 화학 업계에서도 수많은 화학제품과 원자재의 안전성과 유효성을 확보하기 위해 온도 관리가 필요하기 때문에 콜드체인이 요구되고 있습니다.

이 외에도 콜드체인 물류에는 다양한 용도가 있습니다. 온도가 적절히 조절된 환경도 필수적입니다. 극단적인 온도는 특정 전자기기의 기능에 악영향을 미칠 수 있습니다. 꽃이나 식물도 신선도를 유지하기 위해 온도가 관리되는 물류 시스템이 필요합니다. 그 결과, 다양한 산업 분야에서 제품의 품질과 안전성을 유지하기 위해 콜드체인이 필수 불가결한 요소가 되었습니다.

“용도별 카테고리 내의 의약품 부문은 예측 기간 동안 상당한 연평균 성장률(CAGR)을 기록할 것으로 추정됩니다.”

의약품, 바이오의약품, 백신, 특수 의약품 등 온도에 민감한 제품에 대한 수요가 증가함에 따라, 제약 업계에서 콜드체인 솔루션의 활용이 급증하고 있습니다. 제약 회사와 의료 기관은 유효성, 안전성 및 규정 준수를 유지하기 위해 운송 및 보관 중의 온도 관리가 필요하다는 점을 점점 더 인식하고 있습니다. 아주 미세한 온도 변동이라도 민감한 제품의 품질을 저해할 가능성이 있으므로, 더 많은 콜드체인 인프라가 요구되고 있습니다.

바이오의약품, 세포·유전자 치료, 인슐린 제제 및 개량형 백신의 도입 확대는 콜드체인 솔루션 수요 증가에 중요한 역할을 하고 있습니다. 또한, 전 세계적인 예방접종 캠페인의 확대, 의료비 증가, 그리고 전문 의약품에 대한 수요 증가가 수요를 견인하는 주요 요인으로 작용하고 있습니다. 또한, 정부 및 국제적으로 인정된 기준에 따른 의약품 운송 관련 규제 및 품질 요건의 도입이 진행되고 있는 점도 각 기관이 콜드체인 구축에 주력하도록 촉진하고 있습니다. IoT 기술을 활용한 온도 모니터링의 확대와 콜드체인의 가시성을 높이는 기타 기술의 도입으로 인해, 운송 과정에서 의약품이 분실될 위험이 줄어들고 있습니다. 또한, 세계 다른 지역의 제약 산업 발전 역시 콜드체인 서비스에 더 많은 기회를 제공하고 있습니다. 전반적으로 볼 때, 제약 업계는 앞으로도 시장의 주요 성장 동력 중 하나가 될 것입니다.

“온도 관리 부문 내 냉장 부문은 꾸준한 성장세를 유지할 것으로 예상됩니다.”

식품 업계, 의료 분야, 소매업 등 다양한 업계에서 상품 운송 및 보관 시 온도 관리에 대한 수요가 증가함에 따라, 콜드체인 시장에서 냉장 부문은 꾸준한 성장이 예상됩니다. 냉장 물류는 제품을 적절한 온도로 유지하는 데 도움이 되며, 운송 및 보관 중 품질 유지에 필수적입니다. 신선식품, 편의점 식품, 유제품, 고급 음료의 인기가 높아짐에 따라 냉장 물류 수요 확대에 중요한 역할을 하고 있습니다. 여기에는 부패로 인한 손실을 방지하기 위해 냉장 물류를 점점 더 많이 도입하고 있는 소매업체와 외식업계도 포함됩니다. 이와 동시에, 온도에 민감한 의약품의 운송 및 보관 필요성으로 인해 의료 분야에서의 냉장 물류 이용도 꾸준히 증가하고 있습니다. 급속한 도시화, 식생활의 변화, 슈퍼마켓 체인 및 대형마트 체인과 같은 선진적인 소매 채널의 확대, 나아가 온라인 식료품 판매 채널의 부상 등이 시장 내 수요를 뒷받침할 것으로 보입니다. 또한, 냉장 기술, 냉동 창고 용량 및 감시 시스템의 발전으로 인해 효율성이 향상될 전망입니다. 기업들이 제품의 안전성과 폐기물 감축에 더욱 주력하는 가운데, 냉장 식품 부문이 시장 성장에 크게 기여할 것으로 예상됩니다.

“북미는 콜드체인 시장에서 상당한 점유율을 차지할 것으로 추정됩니다.”

북미는 잘 갖춰진 물류 인프라, 제약 업계 주요 기업들의 입지, 그리고 해당 지역의 온도에 민감한 식품에 대한 수요 덕분에 콜드체인 분야에서 상당한 시장 점유율을 차지할 것으로 전망됩니다. 냉동식품 및 가공식품에 대한 수요 증가와 더불어, 유제품 및 육류 제품 등 신선식품에 대한 선호도가 높아지면서 북미의 효율적인 콜드체인 시스템에 대한 수요를 견인하고 있습니다. 또한, 해당 지역에 대형 제약사 및 생명공학 기업이 위치해 있어 백신이나 생물학적 제제 등 온도에 민감한 제품을 적절히 관리해야 할 필요성이 커지면서, 효율적인 콜드체인 시스템 도입이 활발히 진행되고 있습니다. 또한, 의약품 및 식품 안전에 관한 엄격한 규제도 콜드체인 기술에 대한 수요를 뒷받침하고 있습니다.

그러나 소비자들의 식료품 배달 서비스 이용 증가와 조직화된 소매업의 확장에 따라 냉장 창고 및 콜드체인 물류 서비스에 대한 수요가 높아지고 있습니다. 또한, IoT를 활용한 감시 시스템이나 자동 창고와 같은 최신 기술을 도입함으로써 공급망 관리를 개선하고 제품 손실을 줄이고 있습니다. 물류 인프라에 대한 투자 확대와 더불어, 제약 및 식품·음료 업계 등 다양한 분야에서 콜드체인 물류 서비스에 대한 수요가 증가함에 따라 북미가 세계 시장을 주도할 것으로 예상됩니다.

콜드체인 시장의 주요 기업으로는 Americold Logistics, Inc.(미국), Lineage, Inc.(미국), NICHIREI CORPORATION(일본), Burris Logistics(미국), A.P. Moller-Maersk(덴마크), United States Cold Storage(미국), Tippmann Group(미국), Coldman Logistics Pvt. Ltd.(인도), CONGEBEC(캐나다), CONESTOGA COLD STORAGE(캐나다), NewCold(네덜란드), Seafrigo Group(프랑스), Trenton Cold Storage(캐나다) 등이 있습니다.

그 밖의 주요 기업으로는 Blue Water Shipping(덴마크), Constellation Cold Logistics S.a R.L.(룩셈부르크), AntarctiCA Cold Storage(미국), APF Cold Storage & Logistics(미국), JS Davidson(영국), Coldrush Logistics(아일랜드), Canadian Dry Storage Ltd.(캐나다), Ruiyun Cold Chain(중국) 등이 포함됩니다.

조사 범위:

본 조사 보고서에서는 콜드체인 시장을 용도별, 온도대별, 기술별, 지역별로 분류하고 있습니다. 본 보고서의 조사 범위에는 콜드체인 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 제약요인, 과제, 기회 등)에 대한 상세한 정보가 포함되어 있습니다. 주요 업계 진출 기업에 대해 상세한 분석을 수행하여, 해당 기업의 사업 개요, 솔루션, 서비스, 주요 전략, 계약, 파트너십 및 합의 사항에 대한 인사이트를 제공합니다. 본 조사에는 콜드체인 시장과 관련된 제품 및 서비스의 출시, 합병 및 인수, 그리고 최근 동향이 포함되어 있습니다. 또한, 본 보고서에는 콜드체인 시장 생태계 내 신생 스타트업 기업들에 대한 경쟁 분석도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유:

본 보고서는 콜드체인 시장 전체 및 각 하위 부문의 매출액에 대한 가장 정확한 추정치를 제공함으로써, 시장 선도 기업 및 신규 진입 기업 여러분을 지원합니다. 또한, 이해관계자 여러분이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 나은 위치로 이끌며, 적절한 시장 진입 전략을 수립하는 데 필요한 추가적인 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자 여러분이 시장 동향을 파악할 수 있도록 지원하며, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 관한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다:

1. 유형, 운송 수단, 기술, 용도별 상세한 세분화 - 본 보고서는 콜드체인 시장에 대한 상세한 분석을 수행하며, 업계를 유형별, 온도대별, 용도별, 기술별, 지역별로 분류하여 콜드체인 시장에 대한 심층적인 분석을 제공합니다. 이러한 상세한 세분화를 통해 이해관계자들은 고성장 분야를 파악하고, 제품 개발을 최적화하며, 공급망 전반에 걸쳐 제품을 전략적으로 포지셔닝할 수 있게 됩니다.

2. 신흥 시장에 초점을 맞춘 지역별 인사이트 - 본 보고서는 국가 및 지역별 분석을 제공하며, 아시아태평양, 북미, 유럽, 남미 등 급성장 시장의 기회를 중점적으로 다루고 있습니다. 지역별 규제 체계, 주요 수요, 투자 동향을 심층적으로 분석함으로써, 사업 확대 및 현지화 전략을 추구하는 기업들에게 중요한 지침이 될 것입니다.

3. 경쟁사 정보 및 혁신 동향 - Americold Logistics, Inc.(미국), Lineage, Inc.(미국), NICHIREI CORPORATION(일본), Burris Logistics(미국), A.P. Moller-Maersk(덴마크), United States Cold Storage(미국), Tippmann Group(미국), Coldman Logistics Pvt. Ltd.(인도), CONGEBEC(캐나다), CONESTOGA COLD STORAGE(캐나다), NewCold(네덜란드), Seafrigo Group(프랑스), Trenton Cold Storage(캐나다) 등 주요 시장 참여 기업에 대해 상세히 분석하고 있습니다. 본 보고서에서는 신제품 출시, 합병·인수, 시설 확장, 연구 개발(R&D) 활동 등 최근 동향을 다루고 있어, 사용자가 경쟁사와의 비교 평가를 수행하고 새로운 혁신 동향을 파악하는 데 도움이 됩니다.

4. 데이터 기반 조사 기법에 따른 수요 예측 - 2031년까지의 시장 규모 및 성장 전망은 탑다운(top-down) 및 바텀업(bottom-up) 접근법을 결합하여 수립되었으며, 업계 전문가, 업계 단체 및 정부의 공식 데이터를 통해 검증되었습니다. 이러한 인사이트는 콜드체인 분야의 투자 계획 수립 및 시장 기회 평가를 위한 신뢰할 수 있는 지침이 됩니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 콜드체인 시장(유형별)

제10장 콜드체인 시장(용도별)

제11장 콜드체인 시장(온도 구분별)

제12장 콜드체인 시장(기술별)

제13장 온도 관리 수단

제14장 콜드체인 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 인접 시장 및 관련 시장

제19장 부록

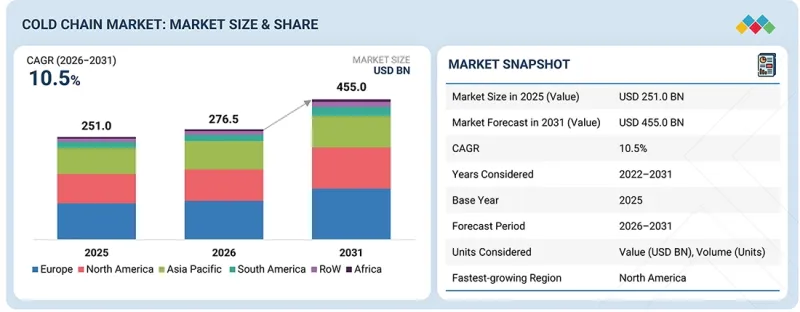

KSM 26.07.02The cold chain market is estimated at USD 276.5 billion in 2026 and is projected to reach USD 455.0 billion by 2031, at a CAGR of 10.5% from 2026 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD), Volume (Ton) |

| Segments | By Type, Temperature Type, Application, Technology (Qualitative), and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and RoW |

Temperature-controlled logistics are gaining more and more prominence in many industries; hence, the market is experiencing substantial growth. In the healthcare industry, it is critical that medications and vaccines undergo proper temperature control so that they remain safe and effective. With an increase in the number of drugs that are more vulnerable to temperature, there is a need for adequate cold chain capabilities.

In the food and beverages industry, the cold chain process is necessary in preserving fresh goods and increasing shelf life, thus ensuring minimal losses of perishable foods such as dairy products, meat, seafood, fruits, vegetables, juices, and other beverages. The chemical industry also needs cold chains since many chemicals and raw materials require temperature control for their safety and effectiveness.

Besides this, there are a number of other uses of cold chain logistics. Temperature-controlled environments are also vital. Extreme temperatures may harm the functioning of certain electronic devices. Flowers and plants, too, need temperature-controlled logistics to maintain their freshness. Consequently, cold chains have become necessary in order to maintain product quality and safety in many different industries.

"The pharmaceuticals segment within the Application category is estimated to witness a significant CAGR during the forecast period."

Cold chain solutions are experiencing an upsurge within the pharmaceutical sector due to increased requirements for temperature-sensitive products such as drugs, biologics, vaccines, and specialized pharmaceuticals. Pharmaceutical companies and healthcare institutions have increasingly recognized the need to control temperature during transportation and storage to maintain efficacy, safety, and compliance. Temperature variations, even by small degrees, can render the quality of sensitive products, hence necessitating more cold chain infrastructure.

The introduction of more biologics, cell/gene therapies, insulin products, and enhanced vaccines has played a critical role in boosting cold chain solutions. In addition, rising global immunization campaigns, higher healthcare expenditure, and increased demand for specialty drugs have been major factors fueling the demand. The increasing implementation of regulations and quality requirements concerning the transport of pharmaceuticals by governments and internationally accepted standards is also compelling organizations to focus on developing their cold chains. The increase in the application of temperature monitoring through IoT technology, as well as other technologies that provide greater visibility of the chain, has led to a decrease in the possibility of losing pharmaceutical products during the process. Moreover, the development of pharmaceutical industries in other parts of the world provides more opportunities for cold chain services. Overall, the pharma industry will be one of the major drivers in the market going forward.

"The chilled segment within the temperature category is estimated to maintain strong growth."

The chilled portion of the market is forecast to see consistent growth in the cold chain market as a result of the increasing demand for controlled temperatures when transporting and storing goods from various industries, such as the food industry, healthcare sector, and retailers. Chilled logistics help keep products at an acceptable moderate temperature, which is vital for preserving their quality during transport and storage. The rising popularity of fresh produce, convenience foods, dairy products, and premium beverages plays an important role in the growing demand for chilled logistics. This includes retailers and foodservice establishments that are increasingly incorporating chilled logistics to avoid losses due to spoilage. At the same time, the use of chilled logistics in the healthcare sector is steadily increasing due to the need to transport and store temperature-sensitive drugs. Fast-paced urbanization shifts in diet patterns, and the increasing presence of advanced retail channels like supermarket chains and hypermarket chains, along with the emergence of online grocery channels, will fuel demand within the market. In addition, developments in refrigeration technology, cold storage capabilities, and monitoring systems will improve efficiency. As companies focus more on product safety and waste reduction, it is anticipated that the chilled food sector will make significant contributions to market growth.

"North America is estimated to hold a significant share of the cold chain market."

North America is forecasted to hold a considerable market share within the cold chain sector owing to the logistics infrastructure in place, the presence of key players in the pharmaceutical industry, and the demand for temperature-sensitive food products in the region. The increase in demand for frozen and processed foods, coupled with an increased liking for fresh produce such as dairy and meat products, has been driving demand for efficient cold chain systems in North America. The presence of large pharma players and biotech firms in the region has also led to an increase in the adoption of efficient cold chain systems owing to the need for the proper management of temperature-sensitive products such as vaccines and biologics. Moreover, strict regulations with regard to pharmaceuticals and food safety have spurred demand for cold chain technologies.

However, the rise in the use of grocery delivery services by consumers as well as organized retailing, has increased the requirement for cold storage and cold chain logistics services. In addition to that, the implementation of modern technologies like IoT-enabled monitoring systems and automated warehouses ensures better supply chain management and reduced losses of products. Due to increased investments in logistics infrastructure, coupled with higher demand for cold chain logistics services in various sectors like pharmaceuticals and the food and beverage industry, North America is expected to lead the market globally.

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the cold chain market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) -10%

The key players in the cold chain market include Americold Logistics, Inc. (US), Lineage, Inc. (US), NICHIREI CORPORATION (Japan), Burris Logistics (US), A.P. Moller - Maersk (Denmark), United States Cold Storage (US), Tippmann Group (US), Coldman Logistics Pvt. Ltd. (India), CONGEBEC (Canada), CONESTOGA COLD STORAGE (Canada), NewCold (Netherlands), Seafrigo Group (France), and Trenton Cold Storage (Canada).

Other players include Blue Water Shipping (Denmark), Constellation Cold Logistics S.a R.L. (Luxembourg), AntarctiCA Cold Storage (US), APF Cold Storage & Logistics (US), JS Davidson (UK), Coldrush Logistics (Ireland), Canadian Dry Storage Ltd. (Canada), and Ruiyun Cold Chain (China).

Research Coverage:

This research report categorizes the cold chain market This research report categorizes the cold chain market based on application (food & beverages, pharmaceuticals, and other applications), type (cold chain storage and infrastructure, refrigerated transportation, and others), temperature type (chilled, frozen, and deep-frozen), technology (qualitative), and region (North America, Europe, Asia Pacific, South America, and Rest of the World) - Global forecast to 2031. The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the cold chain market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, and agreements. The study includes product & service launches, mergers & acquisitions, and recent developments associated with the cold chain market. This report also includes a competitive analysis of emerging startups in the cold chain market ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall cold chain and the subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

1. In-depth segmentation across type, transportation mode, technology, and application: This report offers an in-depth analysis of the cold chain market, categorizing the industry by type (Refrigerated Warehousing, Refrigerated Transportation, Cold Chain Monitoring & Tracking Solutions), temperature range (Chilled, Frozen, Deep-frozen/Cryogenic), application (Food & Beverages including dairy products, meat & seafood, fruits & vegetables, bakery & confectionery, processed foods; Pharmaceuticals including vaccines, biologics, blood products, and specialty drugs), technology (Blast Freezing, Vapor Compression Systems, Evaporative Cooling, IoT-enabled Monitoring, RFID & GPS Tracking, Automation & Robotics, PLC-based Systems), and transportation mode (Road, Rail, Air, Sea). This detailed segmentation enables stakeholders to pinpoint high-growth areas, optimize product development, and strategically position offerings along the supply chain.

2. Region-specific Insights with Focus on Emerging Markets: The report provides country- and region-specific analysis, emphasizing opportunities in rapidly growing markets such as Asia Pacific, North America, Europe, and South America. It explores regional regulatory frameworks, key demand drivers, and investment trends, serving as a critical guide for companies pursuing expansion or localization strategies.

3. Competitive Intelligence and Innovation Landscape: Leading market participants, including Americold Logistics, Inc. (US), Lineage, Inc. (US), NICHIREI CORPORATION (Japan), Burris Logistics (US), A.P. Moller - Maersk (Denmark), United States Cold Storage (US), Tippmann Group (US), Coldman Logistics Pvt. Ltd. (India), CONGEBEC (Canada), CONESTOGA COLD STORAGE (Canada), NewCold (Netherlands), Seafrigo Group (France), and Trenton Cold Storage (Canada) are profiled in detail. The report covers recent developments such as product launches, mergers & acquisitions, facility expansions, and R&D initiatives, helping users benchmark competitors and monitor emerging innovation trends.

4. Demand Forecasts Backed by Data-driven Methodologies: Market sizing and growth projections through 2031 are developed using a combination of top-down and bottom-up approaches, validated by industry experts, trade associations, and official government data. These insights provide reliable guidance for investment planning and market opportunity assessment in the cold chain sector.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 VOLUME UNITS CONSIDERED

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN COLD CHAIN MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN COLD CHAIN MARKET

- 3.2 ASIA PACIFIC: COLD CHAIN MARKET, BY APPLICATION AND COUNTRY

- 3.3 COLD CHAIN MARKET, BY TYPE

- 3.4 COLD CHAIN MARKET, BY APPLICATION

- 3.5 COLD CHAIN MARKET, BY TEMPERATURE TYPE

- 3.6 COLD CHAIN MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased demand for frozen perishable commodities

- 4.2.1.2 Rising international trade of perishable commodities

- 4.2.1.3 Growing need for temperature control to prevent food loss and potential health hazards

- 4.2.1.4 Technological innovations in refrigerated systems and equipment

- 4.2.2 RESTRAINTS

- 4.2.2.1 High energy costs and requirement for significant capital investments

- 4.2.2.2 Environmental concerns regarding greenhouse gas emissions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Intermodal transport to save fuel costs

- 4.2.3.2 Government support for cold chain infrastructure development

- 4.2.4 CHALLENGES

- 4.2.4.1 Maintaining integrity of perishable commodities during transportation

- 4.2.4.2 Rising fuel costs: Major concern for refrigerated transport providers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN COLD CHAIN MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.2.2 BARGAINING POWER OF SUPPLIERS

- 5.2.3 BARGAINING POWER OF BUYERS

- 5.2.4 THREAT OF SUBSTITUTES

- 5.2.5 THREAT OF NEW ENTRANTS

- 5.3 MACROECONOMIC INDICATORS

- 5.3.1 EXPANDING POPULATION AND URBANIZATION

- 5.3.2 RISING NUMBER OF DUAL-INCOME HOUSEHOLDS

- 5.3.3 INCREASING CONSUMPTION OF CONVENIENCE FOODS

- 5.3.4 RISING INVESTMENT IN COLD CHAIN AND FOOD LOGISTICS INFRASTRUCTURE

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.4.1 COLD CHAIN INFRASTRUCTURE & EQUIPMENT SUPPLIERS

- 5.4.2 COLD STORAGE & REFRIGERATION OPERATIONS

- 5.4.3 TRANSPORTATION & LOGISTICS

- 5.4.4 DISTRIBUTION & COMMERCIAL SUPPLY

- 5.4.5 MARKETING & SALES

- 5.4.6 END CONSUMERS

- 5.5 VALUE CHAIN ANALYSIS

- 5.5.1 SUPPLY PROCUREMENT

- 5.5.2 TRANSPORT

- 5.5.3 STORAGE

- 5.5.4 DISTRIBUTION

- 5.5.5 END-PRODUCT MANUFACTURERS

- 5.6 ECOSYSTEM ANALYSIS

- 5.6.1 DEMAND SIDE

- 5.6.2 SUPPLY SIDE

- 5.6.3 COLD STORAGE & REFRIGERATED LOGISTICS COMPANIES

- 5.6.4 ASSOCIATIONS & REGULATORY BODIES

- 5.6.5 STARTUPS

- 5.6.6 END USERS

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SERVICE PRICE TREND, BY VEHICLE TYPE

- 5.7.2 AVERAGE SERVICE PRICE TREND, BY REGION

- 5.8 TRADE ANALYSIS

- 5.8.1 TRADE ANALYSIS OF HS CODE 8418

- 5.8.1.1 Export trends of cold chain systems under HS Code 8418 (2021-2025)

- 5.8.1.2 Import trends of cold chain products under HS Code 8418 (2021-2025)

- 5.8.1 TRADE ANALYSIS OF HS CODE 8418

- 5.9 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.11 INVESTMENT AND FUNDING SCENARIO, 2021-2026

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 IMPLEMENTATION OF TELUS COLD CHAIN SOLUTIONS ON SUNDROP FARMS TO ENSURE FRESHNESS OF AGRICULTURAL PRODUCE

- 5.12.2 COLD CHAIN SOLUTION BY EMERSON USED FOR VACCINE STORAGE

- 5.12.3 UTILIZATION OF PANASONIC COLD CHAIN SOLUTIONS FOR IMPROVED FOOD SUPPLY CHAIN

- 5.13 IMPACT OF 2025 US TARIFF - COLD CHAIN MARKET

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRIES/REGIONS

- 5.13.4.1 North America (US, Canada, Mexico)

- 5.13.4.2 Europe

- 5.13.4.3 Asia Pacific

- 5.13.4.4 South America

- 5.13.4.5 Middle East & Africa

- 5.13.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 INTRODUCTION

- 6.2 KEY EMERGING TECHNOLOGIES

- 6.2.1 INTERNET OF THINGS

- 6.2.2 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 6.2.3 RADIO FREQUENCY IDENTIFICATION

- 6.3 COMPLEMENTARY TECHNOLOGIES

- 6.3.1 ADVANCED ANALYTICS AND DATA AGGREGATION

- 6.3.2 TELEMATICS

- 6.4 ADJACENT TECHNOLOGIES

- 6.4.1 TEMPERATURE & CONDITION MONITORING SYSTEMS

- 6.4.2 REFRIGERATION AIRFLOW & DISTRIBUTION SYSTEMS

- 6.5 TECHNOLOGY/PRODUCT ROADMAP

- 6.5.1 SHORT-TERM | DIGITALIZATION, TEMPERATURE CONTROL, & OPERATIONAL EFFICIENCY

- 6.5.2 MID-TERM | AUTOMATION, DIGITALIZATION, & SUSTAINABLE COLD CHAIN OPERATIONS

- 6.5.3 LONG-TERM | AUTONOMOUS COLD CHAINS & INTELLIGENT TEMPERATURE-CONTROLLED ECOSYSTEMS

- 6.6 PATENT ANALYSIS

- 6.7 FUTURE APPLICATIONS

- 6.7.1 AI-ENABLED TEMPERATURE MONITORING & PREDICTIVE OPERATIONS

- 6.7.2 AI-DRIVEN EFFICIENCY, VISIBILITY, & SUSTAINABILITY APPLICATIONS

- 6.7.3 COLD CHAIN MARKET IN FOOD, PHARMACEUTICAL, & E-COMMERCE APPLICATIONS

- 6.8 IMPACT OF GEN AI ON COLD CHAIN MARKET

- 6.8.1 INTRODUCTION

- 6.8.2 USE OF GEN AI IN COLD CHAIN MARKET

- 6.8.3 TOP USE CASES AND MARKET POTENTIAL

- 6.8.4 IMPACT ON COLD CHAIN MARKET

- 6.8.5 ADJACENT ECOSYSTEM WORKING ON GENERATIVE AI

- 6.8.6 BEST PRACTICES IN COLD CHAIN INDUSTRY

- 6.8.7 CASE STUDIES OF AI IMPLEMENTATION IN COLD CHAIN MARKET

- 6.8.8 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.8.9 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN COLD CHAIN MARKET

- 6.9 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 INTRODUCTION

- 7.2 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2.2 INDUSTRY STANDARDS

- 7.2.3 LABELING REQUIREMENTS AND CLAIMS

- 7.2.4 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 7.2.4.1 Enhanced end-to-end traceability and digital monitoring requirements

- 7.2.4.2 Stricter pharmaceutical cold chain and biologics distribution requirements

- 7.2.4.3 Increased focus on sustainable refrigeration and refrigerant transition

- 7.2.4.4 Expanded food safety, transportation, and temperature-control compliance requirements

- 7.2.4.5 Greater adoption of smart packaging and automated compliance technologies

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 ENERGY-EFFICIENT COLD STORAGE AND REFRIGERATION INFRASTRUCTURE

- 7.3.2 LOW-GWP REFRIGERANTS AND SUSTAINABLE COOLING TRANSITION

- 7.3.3 SUSTAINABLE TRANSPORTATION AND LOGISTICS OPTIMIZATION

- 7.3.4 FOOD WASTE REDUCTION AND SUPPLY CHAIN EFFICIENCY

- 7.3.5 SUSTAINABLE PACKAGING, DIGITALIZATION, AND MONITORING SYSTEMS

- 7.4 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.5 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS END USERS

- 8.6 MARKET PROFITABILITY

9 COLD CHAIN MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 COLD CHAIN STORAGE & INFRASTRUCTURE

- 9.2.1 EXPANDING COLD STORAGE CAPACITY AND FOOD SUPPLY CHAIN MODERNIZATION DRIVING SEGMENT GROWTH

- 9.3 REFRIGERATED TRANSPORTATION

- 9.3.1 REFRIGERATED ROAD TRANSPORTATION

- 9.3.1.1 Refrigerated LCVs

- 9.3.1.1.1 Rapid growth of last-mile cold delivery services driving adoption of refrigerated light commercial vehicles

- 9.3.1.2 Refrigerated MHCVs

- 9.3.1.2.1 Increasing intercity movement of perishable products driving demand for refrigerated medium & heavy commercial vehicles

- 9.3.1.3 Refrigerated HCVs

- 9.3.1.3.1 Expanding long-haul cold chain networks driving demand for refrigerated heavy commercial vehicles

- 9.3.1.1 Refrigerated LCVs

- 9.3.2 REFRIGERATED SEA TRANSPORTATION

- 9.3.2.1 Expanding global trade of perishable commodities driving demand for refrigerated sea transportation

- 9.3.3 REFRIGERATED RAIL TRANSPORTATION

- 9.3.3.1 Sustainable long-distance freight movement supporting adoption of refrigerated rail transportation

- 9.3.4 REFRIGERATED AIR TRANSPORTATION

- 9.3.4.1 Rising demand for high-value and time-critical shipments driving adoption of refrigerated air transportation

- 9.3.1 REFRIGERATED ROAD TRANSPORTATION

- 9.4 OTHER TYPES

10 COLD CHAIN MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 FOOD & BEVERAGES

- 10.2.1 DAIRY & FROZEN DESSERTS

- 10.2.1.1 Expanding dairy consumption and frozen food demand accelerating requirements for temperature-controlled logistics

- 10.2.2 FISH, MEAT, & SEAFOOD

- 10.2.2.1 Growing global protein consumption and seafood trade driving demand for advanced cold chain networks

- 10.2.3 FRUITS & VEGETABLES

- 10.2.3.1 Increasing fresh produce trade and food loss reduction initiatives supporting cold chain expansion

- 10.2.4 BAKERY & CONFECTIONERY

- 10.2.4.1 Growing demand for frozen bakery products and premium confectionery driving refrigerated logistics requirements

- 10.2.5 OTHERS

- 10.2.1 DAIRY & FROZEN DESSERTS

- 10.3 PHARMACEUTICALS

- 10.3.1 EXPANDING BIOLOGICS, VACCINES, AND SPECIALTY THERAPIES DRIVING GROWTH OF PHARMACEUTICAL COLD CHAINS

- 10.4 OTHER APPLICATIONS

11 COLD CHAIN MARKET, BY TEMPERATURE TYPE

- 11.1 INTRODUCTION

- 11.2 CHILLED

- 11.2.1 INCREASING CONSUMPTION OF PROCESSED FOODS DRIVING SEGMENT GROWTH

- 11.3 FROZEN

- 11.3.1 GROWING FROZEN FOOD CONSUMPTION AND GLOBAL PROTEIN TRADE ACCELERATING DEMAND FOR FROZEN COLD CHAIN INFRASTRUCTURE

- 11.4 DEEP FROZEN

- 11.4.1 EXPANDING BIOLOGICS, PREMIUM SEAFOOD EXPORTS, AND ULTRA-LOW TEMPERATURE LOGISTICS DRIVING DEMAND FOR DEEP-FROZEN COLD CHAINS

12 COLD CHAIN MARKET, BY TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 BLAST FREEZING

- 12.2.1 RISING DEMAND FOR HIGH-QUALITY FROZEN FOODS DRIVING ADOPTION OF BLAST FREEZING TECHNOLOGY

- 12.3 VAPOR COMPRESSION

- 12.3.1 WIDESPREAD DEPLOYMENT OF MECHANICAL REFRIGERATION SYSTEMS DRIVING DEMAND FOR VAPOR COMPRESSION TECHNOLOGY

- 12.4 PROGRAMMABLE LOGIC CONTROLLERS

- 12.4.1 INCREASING AUTOMATION AND REAL-TIME MONITORING REQUIREMENTS DRIVING PLC ADOPTION ACROSS COLD CHAINS

- 12.5 EVAPORATIVE COOLING

- 12.5.1 ENERGY-EFFICIENT AND SUSTAINABLE COOLING REQUIREMENTS SUPPORTING ADOPTION OF EVAPORATIVE COOLING TECHNOLOGIES

- 12.6 CRYOGENIC COOLING SYSTEMS

- 12.6.1 EXPANDING BIOLOGICS, VACCINE DISTRIBUTION, AND HIGH-VALUE FOOD EXPORTS DRIVING DEMAND FOR CRYOGENIC COOLING SYSTEMS

- 12.7 OTHER TECHNOLOGIES

13 MEANS OF TEMPERATURE CONTROL

- 13.1 INTRODUCTION

- 13.2 CONVENTIONAL REFRIGERATION

- 13.2.1 EXPANDING COLD STORAGE AND REFRIGERATED TRANSPORTATION INFRASTRUCTURE SUPPORTING DEMAND FOR CONVENTIONAL REFRIGERATION SYSTEMS

- 13.3 MECHANICAL REFRIGERATION

- 13.3.1 MECHANICAL REFRIGERATION DOMINATES GLOBAL COLD CHAIN OPERATIONS DUE TO RELIABILITY AND SCALABILITY

- 13.4 PACKAGING MATERIALS

- 13.4.1 DRY ICE

- 13.4.1.1 Increasing shipments of frozen foods, vaccines, and biologics to drive market

- 13.4.2 WET ICE

- 13.4.2.1 Rising focus on affordable means of cold storage to drive market

- 13.4.3 GEL PACKS

- 13.4.3.1 Enhanced compatibility with transportation systems to drive market

- 13.4.4 EUTECTIC PLATES

- 13.4.4.1 Increasing adoption in temperature-sensitive goods transportation to drive demand

- 13.4.5 LIQUID NITROGEN

- 13.4.5.1 Growing biologics and advanced therapy distribution to drive demand for liquid nitrogen cooling

- 13.4.6 INSULATED BLANKETS

- 13.4.6.1 Increasing need for cost-effective thermal protection during transit to support insulated blanket adoption

- 13.4.7 EXPANDED POLYSTYRENE

- 13.4.7.1 Strong demand for insulated shipping containers to drive demand for expanded polystyrene packaging

- 13.4.1 DRY ICE

14 COLD CHAIN MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Rising frozen food consumption and expansion of automated cold storage facilities to drive market

- 14.2.2 CANADA

- 14.2.2.1 Growing agri-food exports and increasing need for refrigerated transportation infrastructure to drive market

- 14.2.3 MEXICO

- 14.2.3.1 Rising investments in refrigerated warehouses and transportation facilities to drive market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Growing food processing activities and pharmaceutical logistics demand to drive market

- 14.3.2 FRANCE

- 14.3.2.1 Growing agri-food production and pharmaceutical exports to drive market

- 14.3.3 UK

- 14.3.3.1 Rising food trade volumes and investments in automated cold storage infrastructure to drive market

- 14.3.4 ITALY

- 14.3.4.1 Growing agri-food exports and pharmaceutical manufacturing activities to drive market

- 14.3.5 SPAIN

- 14.3.5.1 Growing fresh produce exports and pharmaceutical manufacturing activities to drive market

- 14.3.6 NETHERLANDS

- 14.3.6.1 Growing demand for temperature-controlled logistics to drive market

- 14.3.7 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Increasing government investments in cold chain infrastructure and digital logistics systems to drive market

- 14.4.2 JAPAN

- 14.4.2.1 Growing convenience food distribution and agri-food exports to drive market

- 14.4.3 INDIA

- 14.4.3.1 Government-led expansion of cold chain infrastructure and growth in processed food industries to drive market

- 14.4.4 AUSTRALIA & NEW ZEALAND

- 14.4.4.1 Growing agri-food exports and investments in supply chain resilience to drive market

- 14.4.5 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 SOUTH AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Expanding meat exports and rising processed food consumption to drive market

- 14.5.2 REST OF SOUTH AMERICA

- 14.5.1 BRAZIL

- 14.6 REST OF THE WORLD

- 14.6.1 AFRICA

- 14.6.1.1 Expanding agricultural trade and food security initiatives to drive market

- 14.6.1.2 South Africa

- 14.6.1.3 Egypt

- 14.6.1.4 Rest of Africa

- 14.6.2 MIDDLE EAST

- 14.6.2.1 Rising food import dependence and food security investments to drive market

- 14.6.2.2 UAE

- 14.6.2.3 Saudi Arabia

- 14.6.2.4 Rest of Middle East

- 14.6.1 AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 15.3 REVENUE ANALYSIS, 2023-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 BRAND/SERVICE COMPARISON

- 15.5.1 AMERICOLD LOGISTICS, INC. (US)

- 15.5.2 LINEAGE, INC. (US)

- 15.5.3 NICHIREI CORPORATION (JAPAN)

- 15.5.4 A.P. MOLLER - MAERSK (DENMARK)

- 15.5.5 C.H. ROBINSON (US)

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS 2025

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Type footprint

- 15.6.5.4 Application footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 SERVICE LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 AMERICOLD LOGISTICS, INC.

- 16.1.1.1 Business overview

- 16.1.1.2 Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Deals

- 16.1.1.3.2 Expansions

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 LINEAGE, INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Service launches

- 16.1.2.3.2 Deals

- 16.1.2.3.3 Expansions

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 NICHIREI CORPORATION

- 16.1.3.1 Business overview

- 16.1.3.2 Services offered

- 16.1.3.3 Recent developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 A.P. MOLLER - MAERSK

- 16.1.4.1 Business overview

- 16.1.4.2 Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.3.2 Expansions

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 C.H. ROBINSON

- 16.1.5.1 Business overview

- 16.1.5.2 Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Service launches

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 BURRIS LOGISTICS

- 16.1.6.1 Business overview

- 16.1.6.2 Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Deals

- 16.1.6.4 MnM view

- 16.1.7 KUEHNE+NAGEL

- 16.1.7.1 Business overview

- 16.1.7.2 Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Expansions

- 16.1.7.4 MnM view

- 16.1.8 UNITED STATES COLD STORAGE

- 16.1.8.1 Business overview

- 16.1.8.2 Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Expansions

- 16.1.8.4 MnM view

- 16.1.9 TIPPMANN GROUP

- 16.1.9.1 Business overview

- 16.1.9.2 Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Deals

- 16.1.9.3.2 Expansions

- 16.1.9.4 MnM view

- 16.1.10 COLDMAN LOGISTICS PVT. LTD.

- 16.1.10.1 Business overview

- 16.1.10.2 Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Expansions

- 16.1.10.4 MnM view

- 16.1.11 NEWCOLD

- 16.1.11.1 Business overview

- 16.1.11.2 Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Deals

- 16.1.11.3.2 Expansions

- 16.1.11.4 MnM view

- 16.1.12 SEAFRIGO GROUP

- 16.1.12.1 Business overview

- 16.1.12.2 Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.12.3.2 Expansions

- 16.1.12.4 MnM view

- 16.1.13 BLUE WATER SHIPPING

- 16.1.13.1 Business overview

- 16.1.13.2 Services offered

- 16.1.13.3 Recent developments

- 16.1.13.4 MnM view

- 16.1.14 CONSTELLATION COLD LOGISTICS S.A R.L.

- 16.1.14.1 Business overview

- 16.1.14.2 Services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Deals

- 16.1.14.3.2 Expansions

- 16.1.14.4 MnM view

- 16.1.15 CONGEBEC INC.

- 16.1.15.1 Business overview

- 16.1.15.2 Services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Deals

- 16.1.15.3.2 Expansions

- 16.1.15.4 MnM view

- 16.1.1 AMERICOLD LOGISTICS, INC.

- 16.2 STARTUPS/SME

- 16.2.1 CONESTOGA COLD STORAGE

- 16.2.1.1 Business overview

- 16.2.1.2 Services offered

- 16.2.1.3 Recent developments

- 16.2.1.4 MnM view

- 16.2.2 TRENTON COLD STORAGE

- 16.2.2.1 Business overview

- 16.2.2.2 Services offered

- 16.2.2.3 Recent developments

- 16.2.2.4 MnM view

- 16.2.3 RLS LOGISTICS

- 16.2.3.1 Business overview

- 16.2.3.2 Services offered

- 16.2.3.3 Recent developments

- 16.2.3.4 MnM view

- 16.2.4 ANTARRTICA COLD STORAGE

- 16.2.4.1 Business overview

- 16.2.4.2 Services offered

- 16.2.4.3 Recent developments

- 16.2.4.4 MnM view

- 16.2.5 APF COLD STORAGE & LOGISTICS

- 16.2.5.1 Business overview

- 16.2.5.2 Services offered

- 16.2.5.3 Recent developments

- 16.2.5.4 MnM view

- 16.2.6 JS DAVIDSON

- 16.2.7 AGILE COLD STORAGE, LLC

- 16.2.8 FRIOZEM

- 16.2.9 CANADIAN DRY STORAGE LTD.

- 16.2.10 RUIYUN COLD CHAIN

- 16.2.1 CONESTOGA COLD STORAGE

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Breakdown of primary profiles

- 17.1.2.3 Key insights from industry experts

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.2.3 SUPPLY-SIDE

- 17.2.4 DEMAND-SIDE

- 17.3 DATA TRIANGULATION

- 17.4 RESEARCH ASSUMPTIONS

- 17.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

18 ADJACENT & RELATED MARKETS

- 18.1 INTRODUCTION

- 18.2 LIMITATIONS

- 18.3 REFRIGERATED TRANSPORT MARKET

- 18.3.1 MARKET DEFINITION

- 18.3.2 MARKET OVERVIEW

- 18.3.3 REFRIGERATED TRANSPORT MARKET, BY TEMPERATURE

- 18.3.3.1 Introduction

- 18.3.4 REFRIGERATED TRANSPORT MARKET, BY REGION

- 18.3.4.1 Introduction

- 18.4 REFRIGERATED WAREHOUSING MARKET

- 18.4.1 MARKET DEFINITION

- 18.4.2 MARKET OVERVIEW

- 18.4.3 REFRIGERATED WAREHOUSING MARKET, BY TECHNOLOGY

- 18.4.3.1 Introduction

- 18.4.4 REFRIGERATED WAREHOUSING MARKET, BY REGION

- 18.4.4.1 Introduction

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS