|

시장보고서

상품코드

2073387

콜드체인 물류 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

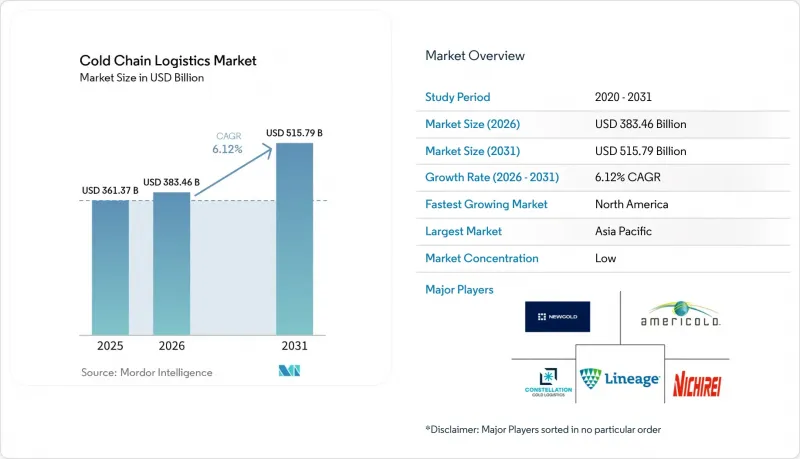

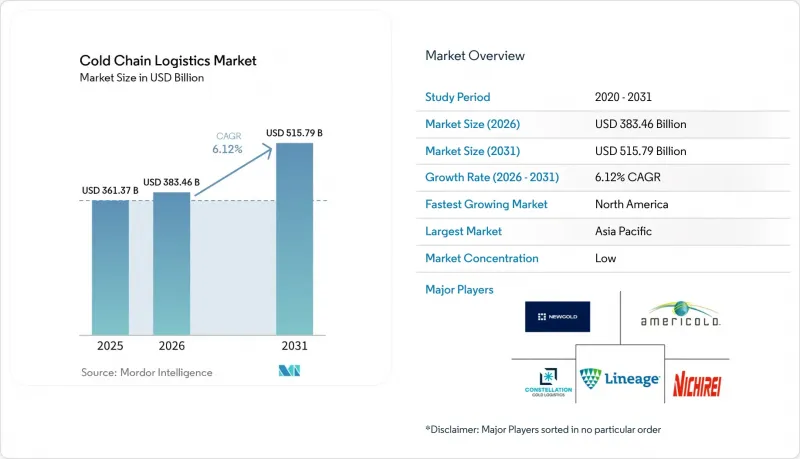

Mordor Intelligence에 의하면, 콜드체인 물류 시장 규모는 2025년 3,613억 7,000만 달러로 평가되었습니다. 2026년에는 3,834억 6,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 6.12%로 성장을 지속하여, 2031년에는 5,157억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서에서는 업계를 서비스별(냉장 보관, 냉장 운송, 부가가치 서비스), 온도 유형별(칠드(0-5°C), 냉동(-18-0°C) 등), 용도별(과일 및 채소, 육류·가금류, 어류·수산물 등), 그리고 지역별(북미, 남미, 아시아태평양 등)로 분류하고 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 콜드체인 물류 시장 동향 및 인사이트

초저온에서 유통되어야 하는 mRNA 백신 수요가 급증하고 있습니다.

mRNA 백신은 기존의 냉동 온도 범위를 훨씬 밑도는 -70°C에서 -80°C 사이에서 보관해야 합니다. 현재 각 제조업체는 전용 초저온 냉동고, 안구건조증스 보급 스테이션 및 이중화 전원 시스템을 운영하는 물류 업체와 제휴하고 있습니다. DHL은 2030년까지 헬스케어 물류에 20억 달러를 배정했으며, 이 중 8억 6,000만 달러는 북미 시장에 할당되었습니다. 백신의 품질 저하는 여전히 중대한 비용 요인으로 작용하고 있습니다. 전 세계 백신 투여량의 50% 가까이가 온도 기준 미준수로 인해 폐기되고 있으며, 이는 제약 회사들에게 연간 350억 달러의 손실을 초래하고 있습니다. 이러한 폐기물을 줄여야 할 필요성 때문에 콜드체인 물류 시장의 초저온 부문에 대한 투자가 가속화되고 있습니다. 현재 초저온 프로젝트는 높은 수익률을 창출하고 있으며, 이로 인해 사모펀드가 전용으로 설계된 냉동 창고 단지로 몰리고 있습니다. 이러한 요인들이 복합적으로 작용하여 시장의 장기 연평균 성장률(CAGR)을 1.2% 끌어올리고 있습니다.

퀵 커머스형 식료품 플랫폼의 급속한 확장이 라스트 마일 물류를 혁신하고 있습니다.

15분에서 30분 이내에 식료품을 배달하겠다는 약속이 인구 밀도가 높은 아시아 전역의 도시에서 마이크로 풀필먼트 센터 건설 붐을 일으키고 있습니다. 사업자는 농산물, 유제품, 육류, 아이스크림이 서로 오염되지 않고 완벽한 상태로 출하될 수 있도록 다온도대 보관실을 설치하고 있습니다. 온라인 식료품 판매 채널은 2025년까지 미국 식료품 총 매출의 5분의 1을 차지했습니다. 인도, 인도네시아, 한국에서도 스마트폰 보급률 상승에 힘입어 비슷한 보급 추세를 보이고 있습니다. 온라인 식료품 시장의 보급률이 1포인트 상승할 때마다, 온도 조절이 가능한 밴이나 이륜차에 대한 수요가 증가하면서 콜드체인 물류 시장이 확대되고 있습니다. 기존 소매업체들은 엄격한 온도 범위 내에서 정해진 시간을 엄수하는 배송을 보장하는 전문 제3자 기업에, 지역 밀착형 배송 업무를 위탁함으로써 이에 대응하고 있습니다.

사하라 이남 아프리카에서는 만성적인 전력 공급 불안정으로 인해 운영 비용이 상승하고 있습니다.

나이지리아, 케냐, 가나의 냉장 창고에서는 연간 500시간을 넘는 정전이 발생하고 있습니다. 사업자는 백업 전원으로 디젤 발전기를 가동하고 있으며, 그 결과 에너지 비용이 운영비의 60%를 차지하게 되었습니다. 반면, 선진국 시장에서는 그 비율이 35%에 그치고 있습니다. 태양광 발전과 화석 연료를 병행하는 하이브리드형 마이크로그리드는 연료 소비를 줄여주지만, 소규모 소유주에게는 여전히 초기 투자 비용이 너무 높습니다. 전력 공급의 불안정성은 온도 관리 규정을 준수하는 데 지장을 주며, 수출업체는 목적지 항구에서 화물 수취 거부를 당할 위험에 처할 수 있습니다. 재생에너지를 활용한 솔루션이 확대되지 않는 한, 물류 사업자들은 운송 능력 확대를 제한할 가능성이 있으며, 그 결과 해당 지역의 콜드체인 물류 시장 성장이 둔화될 우려가 있습니다.

부문별 분석

2025년 기준으로 냉장 창고는 콜드체인 물류 시장 점유율의 52.37%를 차지했으나, 냉장 운송은 연평균 성장률(CAGR) 6.88%라는 더 빠른 속도로 성장하고 있습니다. 이러한 성장은 신속하고 신선한 배송을 원하는 소비자들의 기대와 전 세계 조달 경로의 다양화를 반영하고 있습니다. 국경을 넘는 전자상거래공급망이 길어지고, 소비자에게 수산물을 직접 배송하는 사례가 증가함에 따라, 엄격한 온도 범위를 유지해야 하는 운송 거리가 확대되고 있습니다. 다중 경유 경로 설정 소프트웨어를 활용함으로써, 운송업체는 냉장 트럭의 가동률을 극대화하고, 단열 트레일러의 높은 자본 비용을 상쇄할 수 있습니다. 트레일러용 냉장 유닛에 리튬 이온 배터리 시스템을 도입함으로써 연료 소비량을 줄이고, 캘리포니아주와 유럽연합(EU)의 엄격한 배기가스 규제를 준수하고 있습니다.

부가가치 서비스는 콜드체인 물류 시장에서 수익성이 높은 틈새 분야로 부상하고 있습니다. 라벨 재부착, 역물류, 계절에 따른 포장 등의 업무에는 숙련된 인력과 신속한 업무 흐름이 필요하며, 이러한 업무는 기본적인 보관 업무보다 팔레트당 수익을 높여줍니다. 현재 제약 기업 고객들은 품질 감사를 효율화하기 위해 주문 키트화, 임상시험용 반품 처리, 온도 이탈 보고를 원스톱으로 제공해 주기를 기대하고 있습니다. 식품 브랜드들은 소매업체의 사양에 부합하기 위해 향기 유지 포장 및 최종 공정에서의 품질 검사를 요구하고 있습니다. 이러한 통합 서비스에 대한 수요가 증가함에 따라, 기존 창고 운영 업체들은 콜드체인 물류 시장에서의 점유율을 유지하고 가격 경쟁에만 치우치는 것을 피하기 위해, 운송과 부가가치 서비스를 결합한 패키지형 서비스로 사업을 확대되고 있습니다.

지역별 분석

북미는 2025년 매출의 33.62%를 차지하며, 50억 입방피트의 냉장 공간을 운영했으며, 그중 5분의 4 이상이 미국에 위치했습니다. 규모의 경제 덕분에 팔레트 밀도를 2배로 높이는 고층 크레인이나 셔틀 시스템 등 적극적인 자동화 도입이 가능해졌습니다. 그러나 운전기사 부족과 항만 혼잡이 종단 간 신뢰성에 부담을 주고 있습니다. FSMA 204 규정에 따라 IoT 텔레매틱스의 도입이 가속화되고 있으며, 규정 준수를 위한 투자가 서비스 품질 향상으로 이어져 콜드체인 물류 시장을 뒷받침하고 있습니다.

아시아태평양에서는 소득 증가에 따라 1인당 단백질 및 고급 냉동 디저트 소비량이 증가하고 있으며, 연평균 성장률(CAGR)은 8.05%로 가장 높은 수준을 기록하고 있습니다. 중국에서 조리 식품의 인기가 높아지면서 2급 도시의 지역 물류 허브에 대한 수요가 증가하고 있지만, 한편 인도에서는 냉장 창고의 소유 구조가 분산되어 있는 것이 여전히 병목 현상으로 작용하고 있습니다. FAO(유엔 식량농업기구)의 추산에 따르면, 콜드체인 인프라를 개선함으로써 아시아의 수확 후 손실을 최대 40%까지 줄일 수 있을 것으로 보입니다. 베트남, 인도네시아, 태국 정부는 외국인 직접 투자를 유치하기 위해 암모니아·CO2 플랜트에 대한 세제 우대 조치를 시행하고 있습니다. 이러한 정책으로 인해 아시아태평양은 콜드체인 물류 시장 점유율을 놓고 벌어지는 경쟁의 주요 전장이 되고 있습니다.

유럽에서는 엄격한 환경 기준을 충족하기 위한 노력을 기울이는 한편, 완만하지만 꾸준한 성장세를 보이고 있습니다. EU의 F가스 규제는 천연 냉매로의 전환을 촉진하고 있으며, 설비 투자 부담이 있음에도 불구하고 암모니아·CO₂ 캐스케이드 시스템의 도입을 뒷받침하고 있습니다. 사업자들은 단열재 개보수, LED 조명 도입, 가변속 압축기 도입 등을 통해 에너지 효율 인증을 취득하고, 전력회사로부터 리베이트를 받고 있습니다. OEM과의 제휴를 통해 플러그 앤 플레이 방식의 플랜트룸 도입이 가속화되면서 가동 중단 시간이 줄어들고 있습니다. 유럽의 운송량 중 의약품 운송이 상당한 비중을 차지하고 있으며, 콜드체인 물류 시장 전체에서 이 지역이 프리미엄 서비스 시장으로서의 입지를 공고히 하고 있습니다.

중동 및 아프리카는 절대적인 규모로는 여전히 작지만, 전력 공급이 불안정한 지역에서 태양광 발전을 이용한 냉장 창고가 활용되면서 두 자릿수 성장률을 기록하고 있습니다. UNIDO(유엔산업개발기구)의 조사에 따르면, 2020년 이후 아프리카의 콜드체인에 대한 투자는 25% 증가했습니다. 케냐와 남아프리카공화국에서는 태양광 발전 설비 설치 비용의 최대 30%를 지원하는 인센티브 제도가 도입되어 민간 부문의 관심을 불러일으키고 있습니다. 그러나 디젤에 대한 의존도가 여전히 높기 때문에 운영 비용은 여전히 높은 수준을 유지하고 있습니다. 라틴아메리카에서는 브라질이 이 지역의 성장을 주도하고 있습니다. 해당국의 창고협회에 따르면, 2020년 이후 보관 용량은 15% 증가했습니다. 소고기 수출업체들은 아시아의 품질 검사 기준을 충족하기 위해 부두와 직접 연결된 냉동 복합 시설을 요구하고 있으며, 이로 인해 콜드체인 물류 시장에서 브라질의 전략적 역할이 더욱 강화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the cold chain logistics market size is expected to grow from USD 361.37 billion in 2025 to USD 383.46 billion in 2026 and is forecast to reach USD 515.79 billion by 2031 at 6.12% CAGR over 2026-2031.

This report Segments the Industry Into by Service (Refrigerated Storage, Refrigerated Transportation and Value-Added Services), by Temperature Type (Chilled (0-5 °C), Frozen (-18-0 °C) and More), by Application (Fruits & Vegetables, Meat & Poultry, Fish & Seafood and More), and by Geography (North America, South America, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Cold Chain Logistics Market Trends and Insights

Surging demand for mRNA vaccines requiring ultra-low temperature distribution

mRNA vaccines must be stored between -70 °C and -80 °C, which is far below conventional frozen ranges. Manufacturers now partner with logistics providers that operate specialized ultra-low freezers, dry-ice replenishment stations, and redundant power systems. DHL earmarked USD 2 billion for healthcare logistics through 2030, with USD 860 million reserved for North America. Vaccine spoilage remains a critical cost driver; nearly 50% of global doses still go to waste because of thermal excursions, representing an annual USD 35 billion loss to drug makers. The need to mitigate this waste is accelerating investment in the deep-frozen segment of the cold chain logistics market. Ultra-low projects now command premium yields, which is drawing private equity into purpose-built freezer farms. Collectively, these forces add a 1.2 percentage-point uplift to the market's long-term CAGR.

Rapid expansion of quick-commerce grocery platforms transforming last-mile logistics

Fifteen-to-thirty-minute grocery delivery promises have triggered a wave of micro-fulfilment centre construction across densely populated Asian cities. Operators install multi-temperature chambers so that produce, dairy, meat, and ice cream depart in perfect condition without cross-contamination. The e-grocery channel is poised to account for one-fifth of all United States grocery revenue by 2025. Similar adoption curves are visible in India, Indonesia, and South Korea, aided by rising smartphone penetration. Every incremental point of e-grocery penetration raises demand for temperature-controlled vans and two-wheelers, which expands the cold chain logistics market. Legacy retailers are responding by outsourcing hyper-local distribution to third-party specialists that guarantee on-time delivery within strict temperature bands.

Chronic electricity instability inflating operational costs in Sub-Saharan Africa

Cold stores in Nigeria, Kenya, and Ghana face grid outages that exceed 500 hours per year. Operators run diesel generators for backup power, pushing energy costs to 60% of operating expenses versus 35% in developed markets. Solar-hybrid microgrids cut fuel consumption, yet upfront investments remain prohibitive for small owners. Unstable electricity hampers adherence to temperature protocols, exposing exporters to rejection at destination ports. Unless renewable solutions scale, logistics providers may limit capacity expansions, slowing the cold chain logistics market in the region.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical outsourcing drives GDP-compliant 3PL adoption

- IoT-enabled telematics under FSMA 204 elevate real-time monitoring investments

- Acute shortage of CDL-certified reefer drivers constraining United States capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated storage accounted for 52.37% of the cold chain logistics market share in 2025, yet refrigerated transportation is climbing faster at a 6.88% CAGR. The uptick mirrors consumer expectations for fast, fresh delivery and the diversification of global sourcing lanes. Longer cross-border e-commerce chains and direct-to-consumer seafood deliveries expand lane-kilometres that must stay within tight temperature ranges. Multi-stop routing software allows carriers to maximise the the utilisation of reefer trucks, offsetting the high capital cost of insulated trailers. Investments in lithium-ion battery systems for trailer refrigeration units lower fuel burn, aligning with strict emissions standards in California and the European Union.

Value-added services are emerging as a margin-rich niche inside the cold chain logistics market. Activities such as relabeling, reverse logistics, and seasonal packaging require skilled labour and high-velocity workflows that produce higher revenue per pallet than basic storage. Pharmaceutical shippers now expect order kitting, clinical return handling, and excursion reporting under one roof to streamline quality audits. Food brands request aroma-guard packaging and end-of-line quality inspection to match retailer specifications. Demand for integrated services entices traditional warehouse operators to expand into transport-plus-value-added bundles to protect share and avoid price-only competition in the cold chain logistics market.

Complete Report Scope:

- By Service Type

- Refrigerated Storage

- Public Warehousing

- Private Warehousing

- Refrigerated Transportation

- Road

- Rail

- Sea

- Air

- Value-Added Services

- Refrigerated Storage

- By Temperature Type

- Chilled (0-5 °C)

- Frozen (-18-0 °C)

- Ambient

- Deep-Frozen / Ultra-Low (more than -20 °C)

- By Application

- Fruits & Vegetables

- Meat & Poultry

- Fish & Seafood

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Ready-to-Eat Meals

- Pharmaceuticals & Biologics

- Vaccines & Clinical Trial Materials

- Chemicals & Specialty Materials

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Geography Analysis

North America generated 33.62% of 2025 revenue and operates 5 billion ft3 of refrigerated space, more than four-fifths of which sits in the United States. Scale advantages permit aggressive automation roll-outs, such as high-bay cranes and shuttle systems that double pallet density. Yet driver scarcity and port congestion pressure end-to-end reliability. The FSMA 204 rule accelerates adoption of IoT telematics, turning compliance spending into service-quality upgrades that sustain the cold chain logistics market.

Asia-Pacific registers the highest 8.05% CAGR as rising incomes increase per-capita consumption of protein and premium frozen desserts. China's ready-to-cook meal boom fuels demand for regional distribution hubs in tier-2 cities, while India's fragmented cold room ownership remains a bottleneck. FAO estimates that improving cold chain infrastructure could cut Asia's post-harvest losses by up to 40%. Governments in Vietnam, Indonesia, and Thailand offer tax breaks on ammonia-CO2 plants to lure foreign direct investment. These policies make Asia-Pacific the pivotal battleground for market share in the cold chain logistics market.

Europe exhibits slow-but-steady growth while executing stringent environmental upgrades. The EU F-Gas Regulation encourages a shift to natural refrigerants, driving installation of ammonia-CO2 cascade systems despite capital burdens. Operators retrofit insulation, LED lighting, and variable-speed compressors to earn energy-efficiency certificates that unlock utility rebates. Partnerships with OEMs accelerate deployment of plug-and-play plant rooms, limiting downtime. Pharmaceutical shipments form a sizable share of European volumes, reinforcing the region's status as a premium service market within the wider cold chain logistics market.

Middle East and Africa remain small in absolute terms but record double-digit gains where solar-powered cold stores mitigate unreliable grids. UNIDO tracks a 25% jump in African cold chain investments since 2020. Incentive schemes in Kenya and South Africa reimburse up to 30% of photovoltaic installation costs, spurring private-sector interest. However, diesel reliance persists, keeping operating costs elevated. In Latin America, Brazil leads regional expansion. Its national warehousing association notes a 15% capacity jump since 2020. Beef exporters demand near-dock freezer complexes to meet Asian quality checks, reinforcing Brazil's strategic role in the cold chain logistics market.

- Lineage Logistics

- Americold Logistics

- NewCold Advanced Cold Logistics

- Nichirei Logistics Group Inc.

- Constellation Cold Logistics

- United States Cold Storage, Inc

- Frigolanda Cold Logistics Group

- Emergent Cold Latin America

- Snowman Logistics Ltd.

- Conestoga Cold Storage

- Interstate Cold Storage, Inc.

- SuperFrio Logistica Frigorificada

- Vertical Cold Storage

- Magnavale Ltd

- Swire Cold Storage

- Arcadia Cold Storage & Logistics

- Congebec Inc.

- Burris Logistics

- Agile Cold Storage LLC

- Groupe Conhexa*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for mRNA Vaccines Requiring Ultra-Low Temperature Distribution in North America & Europe

- 4.2.2 Rapid Expansion of Quick-Commerce Grocery Platforms in Asia Increasing Same-Day Refrigerated Last-Mile Needs

- 4.2.3 Government Incentives for Solar-Powered Cold Warehouses in Middle East & Africa to Curb Post-Harvest Food Losses

- 4.2.4 China's "Ready-to-Cook" Meal Boom Propelling Cold Storage Leasing in Tier-2 Cities

- 4.2.5 Pharmaceutical Outsourcing Shifts Driving GDP-Compliant 3PL Adoption in Europe

- 4.2.6 IoT-Enabled Telematics Mandates by US FDA's FSMA 204 Rule Elevating Real-Time Temperature-Monitoring Investments

- 4.3 Market Restraints

- 4.3.1 Chronic Electricity Instability Inflating Operational Costs of Sub-Saharan African Cold Stores

- 4.3.2 Acute Shortage of CDL-Certified Reefer Drivers in the United States Constraining Transport Capacity

- 4.3.3 High Capital Costs of Ammonia/CO2 Cascade Retrofits for EU F-Gas Regulation Compliance

- 4.3.4 Fragmented Ownership of Small-Scale Cold Rooms in India Hindering Network Optimization

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.1.1 Public Warehousing

- 5.1.1.2 Private Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.1.1 Refrigerated Storage

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (more than -20 °C)

- 5.3 By Application

- 5.3.1 Fruits & Vegetables

- 5.3.2 Meat & Poultry

- 5.3.3 Fish & Seafood

- 5.3.4 Dairy & Frozen Desserts

- 5.3.5 Bakery & Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals & Biologics

- 5.3.8 Vaccines & Clinical Trial Materials

- 5.3.9 Chemicals & Specialty Materials

- 5.3.10 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East And Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.4.1 Lineage Logistics

- 6.4.2 Americold Logistics

- 6.4.3 NewCold Advanced Cold Logistics

- 6.4.4 Nichirei Logistics Group Inc.

- 6.4.5 Constellation Cold Logistics

- 6.4.6 United States Cold Storage, Inc

- 6.4.7 Frigolanda Cold Logistics Group

- 6.4.8 Emergent Cold Latin America

- 6.4.9 Snowman Logistics Ltd.

- 6.4.10 Conestoga Cold Storage

- 6.4.11 Interstate Cold Storage, Inc.

- 6.4.12 SuperFrio Logistica Frigorificada

- 6.4.13 Vertical Cold Storage

- 6.4.14 Magnavale Ltd

- 6.4.15 Swire Cold Storage

- 6.4.16 Arcadia Cold Storage & Logistics

- 6.4.17 Congebec Inc.

- 6.4.18 Burris Logistics

- 6.4.19 Agile Cold Storage LLC

- 6.4.20 Groupe Conhexa*