|

시장보고서

상품코드

2076886

애플리케이션 보안 시장 : 유형별, 적용 환경별, 전개 방식별, 조직 규모별, 업계별, 지역별 - 세계 예측(-2031년)Application Security Market By Component (Solutions (Security Testing Tools, Container Security, API Security, and Others), Services), Type (Web, Mobile), Deployment Mode (Cloud, On-premises), Organization Size, Vertical - Global Forecast to 2031 |

||||||

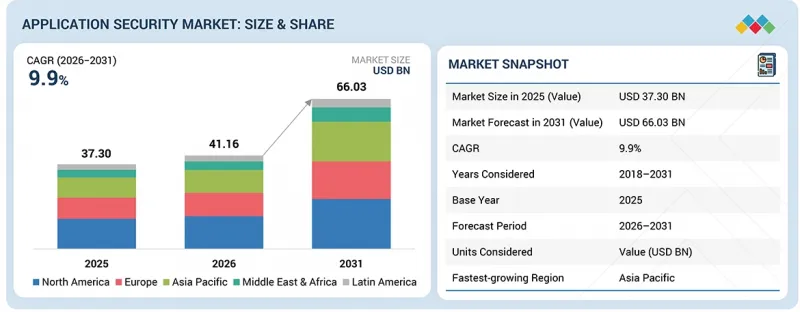

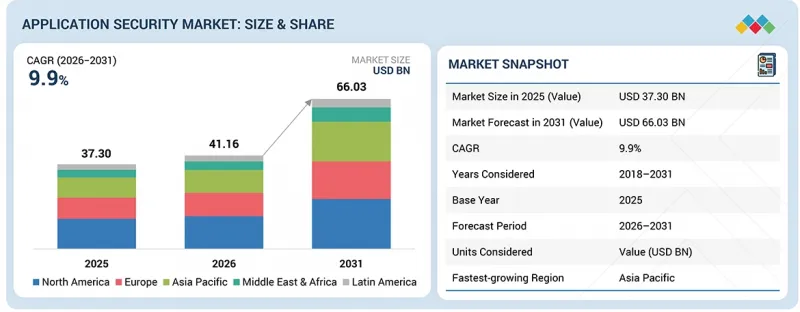

애플리케이션 보안 시장 규모는 예측 기간 동안 CAGR 9.9%로 확대되어 2026년 411억 6,000만 달러에서 2031년에는 660억 3,000만 달러에 달할 것으로 전망됩니다.

이 시장의 성장을 주도하고 있는 요인은, 현대 애플리케이션 개발에서 타사 및 오픈 소스 소프트웨어 구성요소에 대한 의존도가 높아지고 있다는 점입니다. 소프트웨어 공급망이 복잡해짐에 따라, 조직들은 외부 라이브러리의 취약점을 파악하고, 의존성을 악용한 공격을 방지하며, 소프트웨어의 무결성을 확보하기 위해 애플리케이션 보안 솔루션 도입을 점점 더 확대하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2018-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(10억 달러) |

| 부문 | 유형별, 적용 환경별, 전개 방식별, 조직 규모별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

또한, 주목을 받은 공급망 공격의 발생으로 인해 소프트웨어 구성 분석과 개발 라이프사이클 전반에 걸친 애플리케이션 구성요소의 지속적인 모니터링 필요성이 더욱 커지고 있습니다.

솔루션별로는 컨테이너 보안 부문이 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다.

조직이 클라우드 네이티브 개발을 지원하기 위해 컨테이너화된 애플리케이션과 마이크로서비스 아키텍처를 점점 더 많이 도입함에 따라, 컨테이너 보안 분야는 가장 빠른 성장을 이룰 것으로 예상됩니다. 컨테이너는 애플리케이션의 신속한 배포와 확장성을 실현하지만, 그와 동시에 컨테이너 이미지, 레지스트리, 오케스트레이션 플랫폼 및 실행 환경 전반에 새로운 보안 취약점을 초래합니다. 기업들이 쿠버네티스(Kubernetes)나 데브옵스(DevOps) 파이프라인 등의 기술을 도입함에 따라, 개발부터 배포, 실행에 이르는 컨테이너의 전체 수명 주기에 걸친 보안 확보가 매우 중요해지고 있습니다. 컨테이너 보안 솔루션은 컨테이너 이미지 내의 취약점을 탐지하고, 보안 정책을 적용하며, 실행 시 활동을 모니터링함으로써 악의적인 행위를 방지하는 데 도움이 됩니다. 또한, 멀티 클라우드 및 하이브리드 클라우드 환경의 활용이 확대됨에 따라, 동적인 컨테이너화 인프라 전반에 걸친 가시성, 위협 탐지 및 규정 준수를 제공하는 컨테이너 보안 도구에 대한 수요가 더욱 가속화되고 있습니다.

서비스별로는 2026년에 매니지드 서비스 부문이 시장을 주도할 것으로 추정됩니다.

조직들이 증가하는 사이버 위협과 숙련된 사이버 보안 전문가 부족 문제에 대처하기 위해 보안 운영을 외부에 위탁하는 경향이 강해지고 있는 만큼, 매니지드 서비스 부문이 애플리케이션 보안 시장을 독점할 것으로 추정됩니다. 관리형 서비스 제공업체는 지속적인 모니터링, 취약점 관리, 애플리케이션 보안 테스트, 사고 대응 서비스를 제공하므로, 조직은 사내 전문 지식에 막대한 투자를 하지 않고도 견고한 보안을 유지할 수 있습니다. 클라우드 네이티브 아키텍처, API, 모바일 플랫폼으로 인해 애플리케이션 환경이 점점 더 복잡해지는 가운데, 기업들은 일관된 보안 및 규정 준수를 보장하기 위해 관리형 서비스에 의존하고 있습니다. 또한, 매니지드 서비스는 조직이 위협에 대한 가시성을 높이고, 운영의 복잡성을 줄이며, 애플리케이션의 전체 수명 주기에 걸쳐 지속적인 보안을 확보하는 데 도움이 됩니다.

유형별로는 예측 기간 동안 웹 애플리케이션 보안 분야가 시장을 주도할 것으로 예상됩니다.

웹 애플리케이션 보안 부문이 애플리케이션 보안 시장을 주도할 것으로 예상되는 배경에는 디지털 서비스, E-Commerce, 온라인 뱅킹 및 기업 애플리케이션 분야에서 웹 기반 플랫폼이 널리 보급되고 있기 때문입니다. 조직이 고객 및 파트너와의 소통에서 웹 애플리케이션에 대한 의존도를 높일수록, 이러한 플랫폼은 SQL 인젝션, 크로스사이트 스크립팅, API 악용과 같은 사이버 공격의 주요 표적이 되고 있습니다. 웹 애플리케이션 보안 솔루션은 조직이 취약점을 파악하고, 의심스러운 활동을 모니터링하며, 기밀 데이터를 무단 접근으로부터 보호하는 데 도움이 됩니다. 또한, 클라우드 호스팅형 웹 애플리케이션의 도입 확대와 업계를 아우르는 디지털 전환(DX) 노력으로 인해, 고도화된 웹 애플리케이션 보안 도구와 지속적인 취약점 평가 솔루션에 대한 수요가 더욱 증가하고 있습니다.

주요 응답자의 구성

애플리케이션 보안 시장의 주요 공급업체로는 IBM(미국), HCL(인도), Cisco(미국), Synopsys(미국), Checkmark(미국), Veracode(미국), Capgemini(프랑스), Rapid7(미국), Onapsis(미국), GitLab(미국), CAST(프랑스), Qualys(미국), Contrast Security(미국), VMware(미국), OneSpan(미국), Trustwave(미국), Imperva(미국), F5 Networks(미국), Acunetix(몰타), NowSecure(미국), Pradeo Security Systems(프랑스), Lookout(미국), Data Theorem(미국), Zimperium(미국), Kryptowire(미국)입니다.

본 조사에서는 애플리케이션 보안 시장의 주요 기업에 대한 상세한 경쟁 분석, 각 기업 개요, 최근 동향 및 주요 시장 전략을 포괄적으로 다루고 있습니다.

조사 범위

본 보고서에서는 애플리케이션 보안 시장을 세분화하여 유형(웹 애플리케이션 보안 및 모바일 애플리케이션 보안), 적용 환경별(솔루션 및 서비스), 배포 방식(클라우드 및 온프레미스), 조직 규모(대기업 및 중소기업), 산업 분야(BFSI, 정부·공공 부문, 의료, 통신, 소매·E-Commerce, IT·ITeS, 교육, 기타 산업) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카)에 따라 시장을 세분화하고, 시장 규모를 예측하고 있습니다.

또한, 본 조사에서는 시장의 주요 업체에 대한 상세한 경쟁 분석, 각 기업 개요, 제품 및 사업 제공과 관련된 주요 관찰 사항, 최근 동향, 그리고 주요 시장 전략에 대해서도 다루고 있습니다.

본 보고서를 구매할 때의 주요 이점

본 보고서는 애플리케이션 보안 시장 전체 및 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써, 시장을 선도하는 기업과 신규 진입 기업을 지원합니다. 본 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 유리한 위치로 이끌며, 적절한 시장 진입 전략을 수립하는 데 필요한 귀중한 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악할 수 있도록 지원하며, 주요 시장 촉진요인, 제약요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(애플리케이션을 표적으로 한 침해 및 취약점의 급증), 제약요인(도입 비용 및 지속적인 운영 비용의 높음), 기회(모바일 및 API를 중심으로 한 보안 수요), 과제(위협 상황의 급격한 변화 및 제로데이 공격)에 대한 분석

- 제품 개발/혁신 : 애플리케이션 보안 시장의 향후 기술, 연구개발 활동, 신제품 및 서비스 출시에 관한 상세한 인사이트.

- 시장 동향 : 수익성이 높은 시장에 대한 종합적인 정보 - 본 보고서에서는 다양한 지역의 애플리케이션 보안 시장을 분석하고 있습니다.

- 시장의 다양화 : 애플리케이션 보안 시장의 신제품 및 서비스, 미개척 지역, 최근 동향, 그리고 투자에 관한 종합적인 정보.

- 경쟁사 분석 : IBM(미국), HCLTech(인도), Synopsys(미국), Microfocus(영국), Capgemini(프랑스), Onapsis(미국), Cloudflare(미국), F5 Networks(미국), Checkmarx(미국), Fortinet(미국), Checkpoint(이스라엘), Broadcom(미국), Palo Alto Networks(미국), Qualys(미국), Rapid7(미국) 등, 애플리케이션 보안 시장의 주요 기업들의 시장 점유율, 성장 전략, 서비스 제공 내용에 대해 상세히 평가하고 있습니다.

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 소비자 상황과 구매 행동

제9장 애플리케이션 보안 시장(유형별)

제10장 애플리케이션 보안 시장(적용 환경별)

제11장 애플리케이션 보안 시장(전개 방식별)

제12장 애플리케이션 보안 시장(조직 규모별)

제13장 애플리케이션 보안 시장(업계별)

제14장 애플리케이션 보안 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSMThe application security market is projected to grow from USD 41.16 billion in 2026 to USD 66.03 billion by 2031 at a CAGR of 9.9% during the forecast period. The market is driven by the growing dependence on third-party and open-source software components in modern application development. As software supply chains become more complex, organizations are increasingly adopting application security solutions to identify vulnerabilities in external libraries, prevent dependency-based attacks, and ensure software integrity.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2018-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | Type, Component, Deployment Mode, Organization Size, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Additionally, high-profile supply chain attacks have intensified the need for software composition analysis and continuous monitoring of application components throughout the development lifecycle.

By solution, the container security segment is expected to witness the highest CAGR during the forecast period.

Container security is expected to witness the fastest growth as organizations increasingly adopt containerized applications and microservices architectures to support cloud-native development. Containers facilitate faster application deployment and scalability; however, they also present new security vulnerabilities across container images, registries, orchestration platforms, and runtime environments. As enterprises adopt technologies such as Kubernetes and DevOps pipelines, ensuring security across the entire container lifecycle from development to deployment and runtime has become critical. Container security solutions help detect vulnerabilities in container images, enforce security policies, and monitor runtime activities to prevent malicious behavior. Additionally, the rising use of multi-cloud and hybrid cloud environments is further accelerating demand for container security tools that provide visibility, threat detection, and compliance across dynamic containerized infrastructures.

By service, the managed services segment is estimated to lead the market in 2026.

The managed services segment is estimated to dominate the application security market as organizations increasingly outsource security operations to address growing cyber threats and the shortage of skilled cybersecurity professionals. Managed service providers offer continuous monitoring, vulnerability management, application security testing, and incident response, enabling organizations to maintain strong security without investing heavily in in-house expertise. As application environments become more complex with cloud-native architectures, APIs, and mobile platforms, enterprises are relying on managed services to ensure consistent protection and compliance. Additionally, managed services help organizations improve threat visibility, reduce operational complexity, and ensure continuous security across the entire application lifecycle.

By type, the web application security segment is expected to lead the market during the forecast period.

The web application security segment is anticipated to lead the application security market due to the widespread use of web-based platforms for digital services, e-commerce, online banking, and enterprise applications. As organizations increasingly rely on web applications to interact with customers and partners, these platforms have become primary targets for cyberattacks such as SQL injection, cross-site scripting, and API exploitation. Web application security solutions help organizations identify vulnerabilities, monitor suspicious activities, and protect sensitive data from unauthorized access. Furthermore, the growing adoption of cloud-hosted web applications and digital transformation initiatives across industries is further driving the demand for advanced web application security tools and continuous vulnerability assessment solutions.

Breakdown of Primaries

The study draws insights from a range of industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-level - 40%, Managerial & Other Levels - 60%

- By Region: North America - 20%, Europe - 35%, Asia Pacific - 45%

Major vendors in the application security market include IBM (US), HCL (India), Cisco (US), Synopsys (US), Checkmark (US), Veracode (US), Capgemini (France), Rapid7 (US), Onapsis (US), Gitlab (US), CAST (France), Qualys (US), Contrast Security (US), VMware (US), OneSpan (US), Trustwave (US), Imperva (US), F5 Networks (US), Acunetix (Malta), NowSecure (US), Pradeo Security Systems (France), Lookout (US), Data Theorem (US), Zimperium (US), and Kryptowire (US).

The study includes an in-depth competitive analysis of the key players in the application security market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the application security market and forecasts its size based on type (web application security and mobile application security), component (solutions and services), deployment mode (cloud and on-premises), organization size (large enterprises and SMEs), vertical (BFSI, government and public sector, healthcare, telecommunication, retail & ecommerce, IT & ITeS, education, and other verticals), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall application security market and its subsegments. This report will help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of critical drivers (Surge in application targeted breaches and vulnerabilities), restraints (High implementation & ongoing operational costs), opportunities (Mobile and API centric security demand), and challenges (Rapid evolution of threat landscape & zero-day exploits)

- Product Development/Innovation: Detailed insights on upcoming technologies, research development activities, new products, and service launches in the application security market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the application security market across varied regions.

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the application security market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as IBM (US), HCLTech (India), Synopsys (US), Microfocus (UK), Capgemini (France), Onapsis (US), Cloudflare (US), F5 Networks (US), Checkmarx (US), Fortinet (US), Checkpoint (Israel), Broadcom (US), Palo Alto Networks (US), Qualys (US), and Rapid7 (US), among others, in the application security market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN APPLICATION SECURITY MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN APPLICATION SECURITY MARKET

- 3.2 APPLICATION SECURITY MARKET, BY APPLICATION ENVIRONMENT

- 3.3 APPLICATION SECURITY MARKET, BY TYPE

- 3.4 APPLICATION SECURITY MARKET, BY SECURITY TESTING TOOL

- 3.5 APPLICATION SECURITY MARKET, BY DEPLOYMENT MODE

- 3.6 APPLICATION SECURITY MARKET, BY ORGANIZATION SIZE

- 3.7 APPLICATION SECURITY MARKET, BY VERTICAL

- 3.8 APPLICATION SECURITY MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising frequency and sophistication of application-layer cyberattacks

- 4.2.1.2 Rapid adoption of AI-assisted software development and AI-generated code

- 4.2.1.3 Expansion of DevSecOps and shift-left security practices

- 4.2.1.4 Growing regulatory focus on secure software development and software supply chain security

- 4.2.2 RESTRAINTS

- 4.2.2.1 Complexity of securing modern distributed application architectures

- 4.2.2.2 Tool sprawl and fragmented application security ecosystems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emergence of Application Security Posture Management (ASPM) platforms

- 4.2.3.2 Growing demand for AI-powered vulnerability prioritization and automated remediation

- 4.2.3.3 Rising adoption of API security solutions

- 4.2.3.4 Increasing application security adoption among SMEs through SaaS-delivered platforms

- 4.2.4 CHALLENGES

- 4.2.4.1 Growing volume of vulnerabilities across applications, open-source components, APIs, containers, and cloud environments

- 4.2.4.2 Securing AI-generated code and AI-assisted development pipelines

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 CROSS-TIER STRATEGIC PATTERNS

- 4.5.2 STRATEGIC TRENDS

- 4.5.2.1 Adoption of DevSecOps and shift-left security

- 4.5.2.2 AI-driven application security and automated remediation

- 4.5.2.3 Growth of ASPM and software supply chain security

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ICT INDUSTRY

- 5.2.4 TRENDS IN GLOBAL CYBERSECURITY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 TECHNOLOGY & SECURITY COMPONENTS

- 5.3.2 APPLICATION SECURITY DESIGN & DEVELOPMENT

- 5.3.3 PLATFORM DEPLOYMENT & INTEGRATION

- 5.3.4 DISTRIBUTION, MANAGED SERVICES, CONSULTING & CHANNEL ECOSYSTEM

- 5.3.5 END-USER INDUSTRIES

- 5.4 ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY PLATFORM/SOLUTION, 2025

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY VENDOR, 2025

- 5.6 KEY CONFERENCES AND EVENTS IN 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 VERACODE ENHANCES APPLICATION SECURITY FOR BANCO GALICIA

- 5.9.2 CHECKMARX IMPROVES APPLICATION SECURITY FOR BEST BUY

- 5.9.3 CHECKMARX STRENGTHENS SECURE DEVELOPMENT AT CEBU PACIFIC

- 5.9.4 GITLAB IMPROVES SOFTWARE SECURITY FOR ZEBRA

- 5.9.5 CONTRAST SECURITY ENHANCES APPLICATION PROTECTION FOR BACKBASE

- 5.10 IMPACT OF 2025 US TARIFF - APPLICATION SECURITY MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON REGIONS

- 5.10.4.1 North America

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 AI and ML

- 6.1.1.2 DevSecOps

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Cloud security

- 6.1.2.2 Security Information and Event Management (SIEM)

- 6.1.2.3 Identity and Access Management (IAM)

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Blockchain

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY ROADMAP

- 6.2.1 SHORT-TERM (2026-2027) | FOUNDATION & EARLY PLATFORM EXPANSION

- 6.2.2 MID-TERM (2027-2030) | SCALING, AUTOMATION, & SOFTWARE SUPPLY CHAIN SECURITY

- 6.2.3 LONG-TERM (2030-2035+) | AUTONOMOUS, ADAPTIVE, & AI-DRIVEN APPLICATION SECURITY

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AUTONOMOUS AND AI-DRIVEN APPLICATION SECURITY PLATFORMS

- 6.4.2 APPLICATION SECURITY POSTURE MANAGEMENT (ASPM) AND PREDICTIVE RISK ANALYTICS

- 6.4.3 IDENTITY-CENTRIC AND ZERO TRUST APPLICATION SECURITY

- 6.4.4 UNIFIED SECURITY ACROSS CLOUD NATIVE, API, AND RUNTIME ENVIRONMENTS

- 6.4.5 SOFTWARE SUPPLY CHAIN SECURITY AND TRUSTED SOFTWARE ECOSYSTEMS

- 6.5 IMPACT OF AI/GEN AI ON APPLICATION SECURITY MARKET

- 6.5.1 BEST PRACTICES IN APPLICATION SECURITY MARKET

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN APPLICATION SECURITY MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN APPLICATION SECURITY MARKET

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.6.1 BLACK DUCK: SECURE SOFTWARE DEVELOPMENT FOR A GLOBAL TECHNOLOGY ENTERPRISE

- 6.6.2 CHECKMARX: AI-DRIVEN APPLICATION RISK MANAGEMENT FOR A GLOBAL ENTERPRISE

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CONSUMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KE STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.4.1 REVENUE POTENTIAL

- 8.4.2 COST DYNAMICS

- 8.4.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 APPLICATION SECURITY MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.1.1 TYPE: APPLICATION SECURITY MARKET DRIVERS

- 9.2 SECURITY TESTING TOOLS

- 9.2.1 COMPREHENSIVE SECURITY TESTING ENABLES SECURE SOFTWARE THROUGHOUT DEVELOPMENT LIFECYCLE

- 9.2.2 STATIC APPLICATION SECURITY TESTING (SAST)

- 9.2.3 DYNAMIC APPLICATION SECURITY TESTING (DAST)

- 9.2.4 INTERACTIVE APPLICATION SECURITY TESTING (IAST)

- 9.2.5 RUNTIME APPLICATION SELF-PROTECTION (RASP)

- 9.3 API SECURITY

- 9.3.1 API SECURITY PROTECTS MODERN DIGITAL SERVICES AND CONNECTED APPLICATIONS

- 9.4 SECURE DEVOPS (DEVSECOPS) ORCHESTRATION

- 9.4.1 DEVSECOPS ORCHESTRATION ENABLES CONTINUOUS SECURITY ACROSS SOFTWARE DELIVERY PIPELINES

10 APPLICATION SECURITY MARKET, BY APPLICATION ENVIRONMENT

- 10.1 INTRODUCTION

- 10.1.1 APPLICATION ENVIRONMENT: APPLICATION SECURITY MARKET DRIVERS

- 10.2 MOBILE APPLICATION SECURITY

- 10.2.1 INCREASING MOBILE APP USAGE TO FUEL DEMAND FOR THREAT MITIGATION, SOURCE CODE REVIEW, BEHAVIORAL ANALYSIS, AND VULNERABILITY PATTERN IDENTIFICATION

- 10.3 WEB APPLICATION SECURITY

- 10.3.1 SURGING RELIANCE ON WEB APPS COUPLED WITH ESCALATING CYBER THREATS TO DRIVE DEMAND FOR WEB APPLICATION SECURITY

11 APPLICATION SECURITY MARKET, BY DEPLOYMENT MODE

- 11.1 INTRODUCTION

- 11.1.1 DEPLOYMENT MODE: APPLICATION SECURITY MARKET DRIVERS

- 11.2 ON-PREMISES

- 11.2.1 PRIORITIZING COMPLETE AUTHORITY OVER SECURITY ENVIRONMENT WITH ON-PREMISES APPLICATION SECURITY

- 11.3 CLOUD

- 11.3.1 FASTER DEPLOYMENT AND ENHANCED PROTECTION WITH CLOUD SECURITY

- 11.4 HYBRID

- 11.4.1 ENABLES ORGANIZATIONS TO ACHIEVE CENTRALIZED VISIBILITY AND CONSISTENT POLICY ENFORCEMENT

12 APPLICATION SECURITY MARKET, BY ORGANIZATION SIZE

- 12.1 INTRODUCTION

- 12.1.1 ORGANIZATION SIZE: APPLICATION SECURITY MARKET DRIVERS

- 12.2 LARGE ENTERPRISES

- 12.2.1 RAPID ADOPTION OF CLOUD-BASED APPLICATIONS WITH INCREASE IN COSTS ASSOCIATED WITH DATA BREACHES

- 12.3 SMES

- 12.3.1 EVOLVING THREAT LANDSCAPE AND INCREASING RELIANCE ON APPLICATIONS BY SMES

13 APPLICATION SECURITY MARKET, BY VERTICAL

- 13.1 INTRODUCTION

- 13.1.1 VERTICAL: APPLICATION SECURITY MARKET DRIVERS

- 13.2 GOVERNMENT

- 13.2.1 GOVERNMENT SECTOR STRENGTHENS APPLICATION SECURITY FOR CRITICAL DIGITAL SERVICES

- 13.3 BANKING, FINANCIAL SERVICES, AND INSURANCE (BFSI)

- 13.3.1 BFSI PRIORITIZES SECURE APPLICATIONS FOR DIGITAL BANKING AND FINANCIAL SERVICES

- 13.4 IT & ITES

- 13.4.1 IT & ITES AMONG MATURE ADOPTERS OF APPLICATION SECURITY

- 13.5 HEALTHCARE & LIFE SCIENCES

- 13.5.1 HEALTHCARE PROTECTS DIGITAL HEALTH APPLICATIONS AND SENSITIVE PATIENT INFORMATION

- 13.6 AEROSPACE & DEFENSE

- 13.6.1 AEROSPACE & DEFENSE EMPHASIZES SECURE MISSION-CRITICAL SOFTWARE APPLICATIONS

- 13.7 RETAIL & E-COMMERCE

- 13.7.1 RETAIL SECURES CUSTOMER-FACING APPLICATIONS AND DIGITAL COMMERCE PLATFORMS

- 13.8 MANUFACTURING

- 13.8.1 MANUFACTURING SECURES CONNECTED APPLICATIONS SUPPORTING SMART FACTORY OPERATIONS

- 13.9 ENERGY & UTILITIES

- 13.9.1 ENERGY SECTOR PROTECTS CRITICAL OPERATIONAL AND ENTERPRISE APPLICATIONS

- 13.10 TELECOMMUNICATIONS

- 13.10.1 TELECOMMUNICATIONS EXPAND APPLICATION SECURITY ACROSS 5G AND DIGITAL SERVICES

- 13.11 MEDIA & ENTERTAINMENT

- 13.11.1 MEDIA COMPANIES SECURE DIGITAL CONTENT PLATFORMS AND STREAMING APPLICATIONS

- 13.12 TRANSPORTATION & LOGISTICS

- 13.12.1 TRANSPORTATION MODERNIZES SECURE APPLICATIONS FOR CONNECTED MOBILITY ECOSYSTEMS

- 13.13 EDUCATION

- 13.13.1 EDUCATION PROTECTS LEARNING PLATFORMS AND ACADEMIC DIGITAL INFRASTRUCTURE

- 13.14 OTHER VERTICALS

14 APPLICATION SECURITY MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 NORTH AMERICA: APPLICATION SECURITY MARKET DRIVERS

- 14.2.2 US

- 14.2.2.1 Increase in cyber threats and rapid adoption of cloud technology to drive market

- 14.2.3 CANADA

- 14.2.3.1 Digitization, increased awareness of cyber threats, and government support for cybersecurity initiatives to drive market

- 14.3 EUROPE

- 14.3.1 EUROPE: APPLICATION SECURITY MARKET DRIVERS

- 14.3.2 UK

- 14.3.2.1 Strengthening secure software development through regulatory compliance to drive market

- 14.3.3 GERMANY

- 14.3.3.1 Increased focus on application security across industrial and enterprise software to drive market

- 14.3.4 FRANCE

- 14.3.4.1 Growing focus on critical digital infrastructure protection to drive market

- 14.3.5 ITALY

- 14.3.5.1 Digital transformation and cyber resilience to drive market

- 14.3.6 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 ASIA PACIFIC: APPLICATION SECURITY MARKET DRIVERS

- 14.4.2 CHINA

- 14.4.2.1 National cybersecurity and software innovation to drive market

- 14.4.3 JAPAN

- 14.4.3.1 Increasing investment in secure software development to drive market

- 14.4.4 INDIA

- 14.4.4.1 Expanding digital economy and innovation to drive market

- 14.4.5 REST OF ASIA PACIFIC

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 MIDDLE EAST & AFRICA: APPLICATION SECURITY MARKET DRIVERS

- 14.5.2 GULF COOPERATION COUNCIL (GCC) COUNTRIES

- 14.5.2.1 KSA

- 14.5.2.1.1 Secure application development through Vision 2030 to drive market

- 14.5.2.2 UAE

- 14.5.2.2.1 Digital innovation, cloud adoption, and government-led smart city initiatives to drive market

- 14.5.2.3 Rest of GCC countries

- 14.5.2.1 KSA

- 14.5.3 SOUTH AFRICA

- 14.5.3.1 Enterprise digital transformation, cloud adoption, and increasing cybersecurity awareness to drive market

- 14.5.4 REST OF MIDDLE EAST & AFRICA

- 14.6 LATIN AMERICA

- 14.6.1 LATIN AMERICA: APPLICATION SECURITY MARKET DRIVERS

- 14.6.2 BRAZIL

- 14.6.2.1 Digital banking and enterprise modernization to drive market

- 14.6.3 MEXICO

- 14.6.3.1 Digital service modernization and expanding digital economy to drive market

- 14.6.4 REST OF LATIN AMERICA

15 COMPETITIVE LANDSCAPE

- 15.1 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2024-2026

- 15.2 REVENUE ANALYSIS, 2021-2025

- 15.3 MARKET SHARE ANALYSIS, 2025

- 15.4 BRAND COMPARISON

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Regional footprint

- 15.5.5.3 Application environment footprint

- 15.5.5.4 Type footprint

- 15.5.5.5 Vertical footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.6.5.1 Detailed list of key startups/SMEs

- 15.6.5.2 Competitive benchmarking of key startups/SMEs

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS, 2025

- 15.7.1 COMPANY VALUATION

- 15.7.2 FINANCIAL METRICS USING EV/EBIDTA, 2025

- 15.8 COMPETITIVE SCENARIO

- 15.8.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 15.8.2 DEALS

16 COMPANY PROFILE

- 16.1 KEY PLAYERS

- 16.1.1 PALO ALTO NETWORKS

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches/enhancements

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 AKAMAI

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches/enhancements

- 16.1.2.3.2 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 VMWARE (BROADCOM)

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches/enhancements

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 BLACK DUCK

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches/enhancements

- 16.1.4.3.2 Deals

- 16.1.4.3.3 Other developments

- 16.1.4.4 MnM View

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 IBM

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches/enhancements

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM View

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 SNYK

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches/enhancements

- 16.1.6.3.2 Deals

- 16.1.7 CHECKMARX

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches/enhancements

- 16.1.7.3.2 Deals

- 16.1.8 CISCO

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches/enhancements

- 16.1.8.3.2 Deals

- 16.1.9 IMPERVA (THALES)

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches/enhancements

- 16.1.10 QUALYS

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches/enhancements

- 16.1.11 CROWDSTRIKE

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches/enhancements

- 16.1.11.3.2 Deals

- 16.1.12 VERACODE

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches/enhancements

- 16.1.12.3.2 Deals

- 16.1.13 F5

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Product launches/enhancements

- 16.1.13.3.2 Deals

- 16.1.14 GITLAB

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches/enhancements

- 16.1.14.3.2 Deals

- 16.1.15 OPENTEXT

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Product launches/enhancements

- 16.1.16 INVICTI

- 16.1.16.1 Business overview

- 16.1.16.2 Products/Solutions/Services offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Product launches/enhancements

- 16.1.16.3.2 Deals

- 16.1.17 RAPID7

- 16.1.17.1 Business overview

- 16.1.17.2 Products/Solutions/Services offered

- 16.1.17.3 Recent developments

- 16.1.17.3.1 Product launches/enhancements

- 16.1.18 HCLSOFTWARE (HCLTECH)

- 16.1.18.1 Business overview

- 16.1.18.2 Products/Solutions/Services offered

- 16.1.18.3 Recent developments

- 16.1.18.3.1 Product launches/enhancements

- 16.1.18.3.2 Deals

- 16.1.1 PALO ALTO NETWORKS

- 16.2 OTHER KEY PLAYERS

- 16.2.1 CONTRAST SECURITY

- 16.2.2 MEND.IO

- 16.2.3 ONAPSIS

- 16.2.4 SEMGREP

- 16.2.5 ZIMPERIUM

- 16.2.6 HARNESS

- 16.2.7 SALT SECURITY

- 16.2.8 ARMORCODE

- 16.2.9 CAST SOFTWARE

- 16.2.10 WALLARM

- 16.2.11 CEQUENCE SECURITY

- 16.2.12 FLUID ATTACKS

- 16.2.13 CYCODE

- 16.2.14 APIIRO

- 16.2.15 NOWSECURE

- 16.2.16 PRADEO

- 16.2.17 BREACHLOCK

- 16.2.18 IMMUNIWEB

- 16.2.19 DATA THEOREM

- 16.2.20 QUOKKA (FORMERLY KRYPTOWIRE)

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Breakup of primary profiles

- 17.1.2.2 Key industry insights

- 17.2 DATA TRIANGULATION

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 TOP-DOWN APPROACH

- 17.3.2 BOTTOM-UP APPROACH

- 17.4 MARKET FORECAST

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS