|

시장보고서

상품코드

1636549

프랑스의 이차 전지 시장 전망: 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)France Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

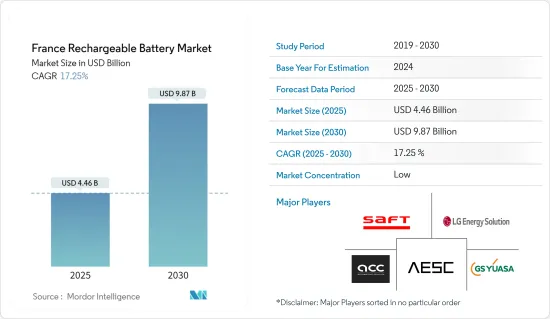

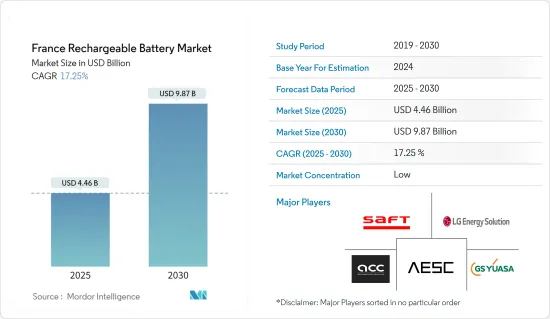

프랑스의 이차 전지 시장 규모는 2025년에 44억 6,000만 달러로 추정되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 17.25%로, 2030년에는 98억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 리튬 이온 전지 가격 하락, 전기차 보급 확대, 정부 지원에 의한 신재생에너지 부문 확대가 예측 기간 동안 프랑스의 이차 전지 시장을 주도할 것으로 예상됩니다.

- 한편, 원료의 수급 불균형이나 배터리 기술에 관한 안전성의 문제가, 예측기간 중 시장 성장의 방해가 될 가능성이 높습니다.

- 그럼에도 불구하고, 새로운 배터리 기술과 첨단 배터리 화학의 개발이 진행되고 있기 때문에 프랑스의 이차 전지 시장에 기회가 생길 가능성은 높습니다.

프랑스의 이차전지 시장 동향

크게 성장하는 자동차 배터리

- 프랑스에서는 자동차가 이차 전지 시장을 독점하고 있습니다. 이 나라에서 전기자동차(EV)가 보급됨에 따라 이차 전지, 특히 리튬 이온의 수요가 급증하고 있습니다.

- 또한 납 배터리는 자동차 시동, 조명, 점화(SLI) 액세서리에 전원을 공급합니다. 이 SLI 배터리는 엔진 시동에 필요한 중요한 초기 전력을 공급합니다. 딥 사이클 배터리보다 작고 가볍기 때문에 수요는 지속될 것으로 예측되어 프랑스의 이차 배터리 시장을 강화하고 있습니다.

- 국제자동차공업연합회(OICA) 데이터에 따르면 프랑스의 2023년 신차 판매량은 220만대를 넘어 2022년 192만대에서 14.67%, 2021년 214만대에서 3.12% 증가했습니다. 이러한 자동차 판매 증가는 자동차 용도에서 이차 전지의 채택을 더욱 촉진할 것으로 예상됩니다.

- 또한 프랑스 자동차 부문에서는 전기자동차(EV)의 채택이 현저하게 증가하고 있습니다. 국제에너지기구(IEA)의 보고에 의하면, 프랑스의 전기자동차(BEV)의 판매 대수는 2023년에 약 31만대에 달하였고, 2022년의 21만대로부터 47%의 대폭 증가되었습니다. 이 급속한 EV의 보급은 프랑스에서의 이차 전지 수요에 박차를 가하게 되었습니다.

- 2024년 5월 프랑스 정부는 중국과의 치열한 경쟁에도 불구하고 2030년까지 200만 대의 전기자동차 또는 하이브리드 자동차를 생산할 것을 자동차 제조업체에 과제로 제시했습니다. 새로운 중기협정의 일환으로 산업은 2027년까지 80만대의 전기자동차 판매를 목표로 하고 있으며, 이는 2022년 20만대에서 크게 급증했습니다. 또한 자동차 제조업체는 전기차(EV)의 연간 판매량을 2022년 16,500대에서 100,000대로 늘리는 것을 목표로 하고 있습니다.

- EV 생산과 구매를 더욱 강화하기 위해 프랑스 정부는 2024년 15억 유로(16억 달러)를 배정했습니다. 프랑스에서 판매되는 신차의 20% 가까이가 전기차이지만, 국산차는 불과 12%에 불과합니다. 또한 정부와 산업의 협의는 2030년까지 40만 곳의 충전 포인트를, 2027년까지 2만 5,000개 급속 충전 포인트를 주요 루트 및 주요 도시에 전략적으로 배치하는 것을 목표로 하고 있습니다. 이러한 구상은 향후 수년간 이차 전지, 특히 리튬 이온 유형 수요를 크게 밀어 올릴 계획입니다.

- 2023년 5월, Stellantis는 Total Energies, Merces-Benz와 공동으로 프랑스 빌리 벨크로 두브란에 Automotive Cells Company(ACC)의 배터리 기가 공장을 개설했습니다. 이것은 유럽에서 계획된 3개의 기가팩토리의 제1호가 됩니다. 13 기가와트시(GWh) 생산능력에서 시작하여 2030년까지 40GWh까지 확대하는 이 시설은 CO2 배출량을 최소화하면서 고성능 리튬이온 배터리를 생산하는 것을 목표로 하고 있습니다. 이 기가팩토리는 2030년까지 유럽에서 250GWh의 배터리 생산 능력을 달성하는 스텔란티스의 야심찬 목표를 부합하는 것입니다.

- 2024년 1월 대만의 전기자동차 배터리 제조업체인 ProLogium Technology Co.는 2027년 프랑스 신공장에서 양산을 시작하여 주식 공개를 목표로 계획을 발표했습니다. 2023년 초 프랑스 에마뉘엘 마크론 대통령은 프로로짐에 의한 던켈의 배터리 공장에 대한 52억 유로(56억 7,000만 달러)의 거액 투자를 강조하고, 유럽의 전기자동차 산업의 허브로서 프랑스의 지위를 더욱 견고하게 만들었습니다. 이러한 전략적 움직임은 프랑스가 이차 전지 부문에서 발전하려는 노력을 강조합니다.

- 이러한 신흥국 시장의 개발로 프랑스의 이차 전지 시장은 자동차 부문에서 급증할 것으로 전망되고 있습니다.

시장을 주도하는 신재생에너지 부문 채택 확대

- 프랑스에서는 재생 가능 에너지의 도입이 진행되고 있어 이차 전지 시장을 크게 주도하게 됩니다. 국제재생가능에너지기구(IRENA)의 보고에 따르면 프랑스의 재생가능에너지의 누적 용량은 2023년에 약 69.3GW에 달했고, 2022년부터 7% 증가했습니다. 프랑스가 태양에너지와 풍력에너지에 기여함에 따라 효율적인 배터리 에너지 저장 시스템(BESS)에 대한 수요가 급증하고 이러한 전원 공급 장치의 간헐적인 특성과 균형을 유지하는 데 중요한 역할을 합니다. 이 시나리오의 주역인 리튬 이온 배터리는 생산량이 많을 시에 잉여 에너지를 저장했다가 수요가 급증하거나 생산이 줄었을 때 이를 방출합니다.

- 2050년까지 온실가스 배출량의 80% 절감(1990년 대비)을 목표로 하는 프랑스의 야심적인 에너지 전환 프로젝트는 BESS 시장을 주도하게 됩니다. 또한 새로운 법률에 따라 2035년까지 원자력 에너지 소비를 75%에서 50%로 줄여야 합니다. 이 전환은 원자력의 출력 감소를 보완하고 재생 가능 에너지에 대한 정책적 지원을 강화하여 원전 생산량 감소를 보완할 것입니다. 이러한 움직임은 재생 에너지에대한 투자를 유치할 뿐 아니라, 첨단 배터리 에너지 저장 시스템의 시급한 필요성을 강조하여 최첨단 충전식 배터리에 대한 수요를 증폭시킵니다.

- 2023년 9월 Q ENERGY는 프랑스의 산 아볼드에 있는 에밀 유쉐 발전소에서 멜벳에너지 저장 프로젝트를 시작했습니다. 35MW, 44MWh의 용량을 가진이 시스템은 약 10,000명의 주민의 하루 전력 수요를 충족시킬 수 있습니다. 최첨단 배터리 컨테이너 24개를 갖춘 이 프로젝트는 신재생에너지 통합을 지원하고 보다 친환경 에너지 믹스에 기여하는 에너지 저장 부문의 성장을 상징합니다.

- 또한 여러 기업이 새로운 배터리 저장 프로젝트를 발표하고 있습니다. 2022년 12월 Tesla는 Electricite de France에 196MWh 배터리 시스템을 제공하여 태양광 발전소와 연결했습니다. 2022년 8월 BayWa re는 오토 산톤주 공동체로부터 40MWp의 태양광 발전소와 연간 출력 52GWh의 축전지를 갖춘 태양광 발전 및 배터리 저장 시설을 구축했습니다.

- 신재생에너지의 도입과 전지기술의 진보의 상호작용이 활기찬 시장 풍경을 만들어내고 있습니다. 기업은 효율적이고 내구성이 있고 비용 효율적인 배터리 솔루션을 고안하기 위해 연구 개발에 많은 투자를 하고 있습니다. 이러한 혁신에 대한 노력은 에너지 저장 문제를 극복하고 프랑스의 야심찬 재생 가능 에너지 목표를 달성하는 데 필수적입니다.

- 2024년 5월, Skeleton Technologies는 프랑스의 옥시타니 지역으로의 진출을 발표하고 5년간 6억 유로의 투자를 약속했습니다. 사업 확장의 시작으로 Skeleton은 툴루즈에서 차세대 배터리 기술 연구 개발을 시작합니다. 이어 옥시타니에 슈퍼 배터리제조 부문을 설립할 예정입니다. 고출력으로 급속 충전이 가능한 에너지 저장에 중점을 둔 Skeleton 제품은 EV에서 항공우주까지 다양한 부문에 대응하고 CO2 삭감과 에너지 절약에 중점을 두고 있습니다.

- 2024년 4월 Schneider Electric은 최신 배터리 에너지 저장 시스템(BESS)을 발표했습니다. 마이크로그리드 시스템에 통합된 BESS는 다양한 에너지원으로부터 에너지를 회수하고 향후 사용을 위해 저장합니다. 독특한 분산 에너지 자원(DER)으로서 BESS는 수요 충전 감소에서 재생 가능한 자기 소비에 이르기까지 광범위한 에너지 용도을 지원합니다.

- 종합하면 프랑스가 지속 가능한 저탄소 에너지의 미래를 향해 앞으로 나아가는 동안 재생 가능 에너지의 채택과 신뢰할 수있는 에너지 저장 수요의 상승 효과는 이차 전지 시장의 주요 촉매제가 될 것입니다.

프랑스의 이차 전지 산업 개요

프랑스의 2차 전지 시장은 반세분화되어 있습니다. 이 시장의 주요 기업(무순서)에는 Saft Groupe SAS, LG Energy Solution Ltd., AESC Group Ltd., Automotive Cells Company(ACC), GS Yuasa Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 성장 촉진요인

- 전기자동차의 보급 확대

- 재생 가능 에너지 부문의 채용 확대

- 리튬 이온 전지 비용 저하

- 억제요인

- 원료의 수급 미스매치

- 성장 촉진요인

- 공급망 분석

- PESTLE 분석

- 투자분석

제5장 시장 세분화

- 기술

- 납 배터리

- 리튬 이온

- 기타 기술(NiMh, Nicd 등)

- 용도

- 자동차용 전지

- 산업용 전지(동력용, 거치형(텔레콤, UPS, 에너지 저장 시스템(ESS) 등))

- 휴대용 배터리(가전 제품 등)

- 기타

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Saft Groupe SAS

- LG Energy Solution Ltd.

- AESC Group Ltd.

- Automotive Cells Company(ACC)

- GS Yuasa Corporation

- Exide Technologies

- Panasonic Corporation

- Duracell Inc.

- Schneider Electric SE

- Contemporary Amperex Technology Co., Limited

- EnerSys

- 기타 저명한 기업 일람(회사명, 본사 소재지, 관련 제품과 서비스, 연락처 등)

- 시장 랭킹, 공유 분석

제7장 시장 기회와 앞으로의 동향

- 새로운 배터리 기술과 선진 배터리 화학의 개발의 진전

The France Rechargeable Battery Market size is estimated at USD 4.46 billion in 2025, and is expected to reach USD 9.87 billion by 2030, at a CAGR of 17.25% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing renewable energy sector aided by government are expected to drive the France rechargeable battery market during the forecast period.

- On the other hand, the demand-supply mismatch of raw materials, and the safety issues related to battery technologies are likely to hinder the market's growth during the forecast period.

- Nevertheless, the growing progress in developing new battery technologies and advanced battery chemistries will likely create opportunities for the France rechargeable battery market.

France Rechargeable Battery Market Trends

Automotive Batteries Segment to Witness Significant Growth

- In France, automotive applications are poised to dominate the rechargeable batteries market. As electric vehicles (EVs) gain traction in the country, the demand for rechargeable batteries, particularly lithium-ion types, is set to surge.

- Moreover, lead-acid batteries power the starting, lighting, and ignition (SLI) accessories in vehicles. These SLI batteries provide the crucial initial power burst needed to start an engine. Being smaller and lighter than deep-cycle batteries, their demand is projected to persist, bolstering the French rechargeable battery market.

- Data from the International Organization of Motor Vehicle Manufacturers (OICA) reveals that France sold over 2.20 million new motor vehicles in 2023, marking a 14.67% jump from 2022's 1.92 million and a 3.12% rise from 2021's 2.14 million. This uptick in vehicle sales is expected to further drive the adoption of rechargeable batteries in automotive applications.

- Furthermore, the French automotive sector has witnessed a notable uptick in the adoption of electric vehicle (EV). The International Energy Agency (IEA) reported that battery electric vehicle (BEV) sales in France hit approximately 310,000 units in 2023, a robust 47% increase from 2022's 210,000 units. This rapid EV adoption is set to fuel the demand for rechargeable batteries in France.

- In May 2024, the French government challenged its carmakers to produce two million electric or hybrid vehicles by 2030, despite fierce competition from China. As part of a new medium-term agreement, the industry targets 800,000 electric vehicle sales by 2027, a significant jump from 200,000 in 2022. Furthermore, carmakers aim to boost annual sales of electric light utility vehicles to 100,000, up from 16,500 in 2022.

- To further bolster EV production and purchases, the French government allocated EUR 1.5 billion (USD 1.6 billion) in 2024. While nearly 20% of new cars sold in France are electric, only 12% are domestically produced. The government-industry agreement also envisions 400,000 charging points by 2030 and 25,000 quick charging points by 2027, strategically located along major routes and in major cities. These initiatives are poised to significantly boost the demand for rechargeable batteries, especially lithium-ion types, in the coming years.

- In May 2023, Stellantis, in collaboration with TotalEnergies and Mercedes-Benz, inaugurated the Automotive Cells Company's (ACC) battery gigafactory in Billy-Berclau Douvrin, France. This marks the first of three planned gigafactories in Europe. Starting with a production line capacity of 13 gigawatt-hours (GWh), set to expand to 40GWh by 2030, the facility aims to produce high-performance lithium-ion batteries with a minimal CO2 footprint. This gigafactory aligns with Stellantis' ambitious target of achieving a 250 GWh battery manufacturing capacity in Europe by 2030.

- In January 2024, ProLogium Technology Co., a Taiwanese electric vehicle battery manufacturer, announced plans to commence mass production at its new French factory in 2027, with aspirations for an initial public offering. Earlier in 2023, French President Emmanuel Macron highlighted ProLogium's significant EUR 5.2 billion (USD 5.67 billion) investment in a Dunkirk-based battery factory, further solidifying France's emerging status as a hub for Europe's electric car industry. These strategic moves underscore France's commitment to advancing in the rechargeable battery domain.

- Given these developments, the automotive segment is set for rapid expansion in France's rechargeable battery market.

Growing Adoption of Renewable Energy Sector To Drive the Market

- France's increasing embrace of renewable energy is set to significantly propel the rechargeable batteries market. The International Renewable Energy Agency (IRENA) reported that France's cumulative renewable energy capacity hit approximately 69.3 GW in 2023, marking a 7% rise from 2022. As France leans into solar and wind energy, the demand for efficient battery energy storage systems (BESS) surges, which is crucial for balancing the intermittent nature of these sources. Lithium-ion batteries, a key player in this scenario, store excess energy during peak production and release it when demand spikes or production wanes.

- France's ambitious energy transition projects, aiming for an 80% reduction in greenhouse gas emissions by 2050 (relative to 1990 levels), are set to drive the BESS market. Additionally, a new law mandates a reduction in nuclear energy consumption from 75% to 50% by 2035. This shift is poised to bolster renewable energy initiatives, compensating for the diminished nuclear output. Such moves not only attract investments in renewables but also underscore the urgent need for advanced battery energy storage systems, amplifying the demand for cutting-edge rechargeable batteries.

- In September 2023, Q ENERGY kicked off the "Merbette" energy storage project at the Emile Huchet power plant in Saint-Avold, France. With a capacity of 35 MW and 44 MWh, the system can meet the daily electricity needs of about 10,000 residents. Featuring 24 state-of-the-art battery containers, this project symbolizes the energy storage sector's growth, aiding in renewable energy integration and contributing to a greener energy mix.

- Moreover, several companies have unveiled new battery energy storage projects. In December 2022, Tesla provided a 196 MWh battery system to Electricite de France, linking it to a solar power plant. In August 2022, BayWa r.e. was selected by the Haute-Saintonge Community to establish a solar and battery storage facility, featuring a 40MWp PV park and an annual output of 52 GWh.

- The interplay between renewable energy adoption and battery technology advancements is creating a vibrant market landscape. Companies are heavily investing in R&D to devise efficient, durable, and cost-effective battery solutions. This commitment to innovation is vital for overcoming energy storage challenges and achieving France's ambitious renewable energy goals.

- In May 2024, Skeleton Technologies announced its expansion into France's Occitanie region, committing EUR 600 million over five years. Kicking off its expansion, Skeleton is initiating R&D in Toulouse for next-gen battery tech. Following this, they'll establish a manufacturing unit in Occitanie for their "SuperBattery." Focusing on high-power, fast-charging energy storage, Skeleton's products cater to diverse sectors, from EVs to aerospace, emphasizing CO2 reduction and energy conservation.

- In April 2024, Schneider Electric unveiled its latest Battery Energy Storage System (BESS). Integrated into microgrid systems, BESS captures and stores energy from various sources for future use. As a unique Distributed Energy Resource (DER), BESS supports a wide array of energy applications, from demand-charge reduction to renewable self-consumption.

- In summary, as France strides towards a sustainable, low-carbon energy future, the synergy between renewable energy adoption and the demand for reliable energy storage is poised to be a major catalyst for the rechargeable batteries market.

France Rechargeable Battery Industry Overview

The France rechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Saft Groupe SAS, LG Energy Solution Ltd., AESC Group Ltd., Automotive Cells Company (ACC), and GS Yuasa Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Growing Adoption of Renewable Energy Sector

- 4.5.1.3 Declining Lithium-ion Battery Cost

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Saft Groupe SAS

- 6.3.2 LG Energy Solution Ltd.

- 6.3.3 AESC Group Ltd.

- 6.3.4 Automotive Cells Company (ACC)

- 6.3.5 GS Yuasa Corporation

- 6.3.6 Exide Technologies

- 6.3.7 Panasonic Corporation

- 6.3.8 Duracell Inc.

- 6.3.9 Schneider Electric SE

- 6.3.10 Contemporary Amperex Technology Co., Limited.

- 6.3.11 EnerSys

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Progress in Developing New Battery Technologies and Advanced Battery Chemistries