|

시장보고서

상품코드

1848035

영국의 농업 기계 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)United Kingdom Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

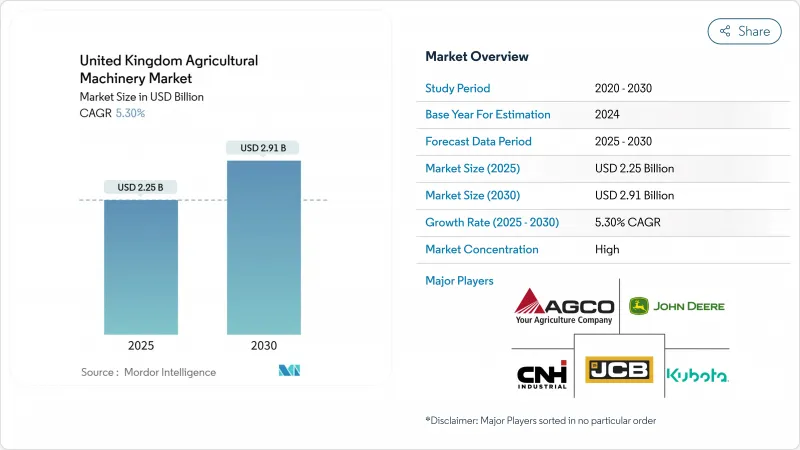

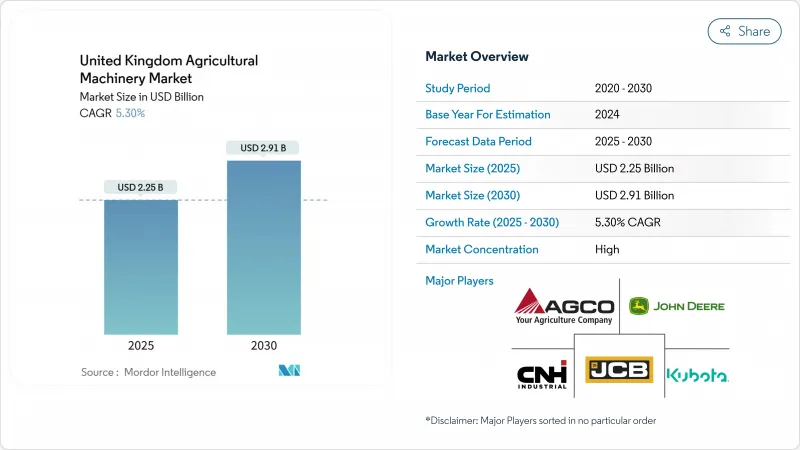

영국의 농업 기계 시장 규모는 2025년 22억 5,000만 달러로 평가되었고, 2030년 29억 1,000만 달러에 이를 것으로 예측되며, 예측기간 중 CAGR은 5.3%를 나타낼 전망입니다.

이러한 상승세는 브렉시트 이후 규제, 지속적인 노동력 부족, 가속화되는 농장 자동화 속에서도 해당 분야의 회복력을 입증합니다. 향후 5년간 농기계 구매는 생산성 향상 기계의 자본 비용을 직접 상쇄하는 5천만 파운드(6천3백만 달러) 규모의 보조금 프로그램인 '농기계 및 기술 기금'에 힘입어 증가할 전망입니다. 청정 전력 2030 실행계획 역시 수요에 영향을 미치는데, 이 계획은 농장이 2030년 국가 탄소중립 목표를 달성하는 데 도움이 되는 저배출 전기 및 수소 트랙터에 투자를 유도합니다. 한편, 스마트 기계 전략 2035의 지원을 받는 농업용 로봇 테스트베드 확장은 신속한 프로토타입 채택을 촉진하고 연구 클러스터 전반에 걸쳐 기술 파트너십을 유치하고 있습니다.

영국의 농업 기계 시장 동향 및 인사이트

노동력 부족으로 가속화되는 기계화

영국 농장의 40% 이상이 인력 부족을 보고하고 있으며, 이로 인해 수작업 노동을 대체할 수 있는 자율 및 반자율 기계에 대한 자본 지출이 증가하고 있습니다. 계절 근로자 비자는 2029년까지 4만 5,000개 직위로 확대되었지만, 정부는 동시에 이민 노동자에 대한 장기적인 의존도를 줄이기 위해 자동화에 5천만 파운드(6,300만 달러)를 투자하고 있습니다. 필드워크 로보틱스의 라즈베리 수확 시스템은 지속적인 운영과 인간에 필적하는 처리량이 어떻게 로봇 공학에 유리한 투자 수익률 계산을 변화시키는지 보여주는 사례다. 인건비가 상승함에 따라 사양 요구 사항은 제한된 감독으로 더 오랜 시간 작업할 수 있는 기계로 이동하며, 이는 영국 전역의 농업 기계 시장 전반에 걸쳐 수요를 강화하고 있습니다.

농업 기계에 대한 정부 보조금 제도 및 세금 감면

농업 기계 및 기술기금(Farming Equipment and Technology Fund)은 신청자 1명당 1,000-25,000파운드(1,250-3만1,250달러), 농업생산성 향상 프로그램(Improving Farm Productivity program)은 로봇공학과 정밀시스템에 최고 20만 5000파운드 각 보조 대상 품목은 5년 동안 계속 사용되어야 하므로 기계 공급업체는 예측 가능한 수요 사이클을 제공합니다. 보조금 채점 프레임워크는 이산화탄소 감축과 동물 복지 지표를 우선하여 센서가 풍부한 기구, 자율 유도, 저압축 솔루션으로 구매를 유도합니다. 이러한 인센티브는 영국의 농업 기계 시장, 특히 지금까지 고액 투자를 늦추어 온 중소규모의 농가에게 전반적인 설비 회전율을 직접 밀어 올립니다.

높은 초기 및 유지보수 비용

잉글랜드 및 웨일스 공인회계사 협회는 대규모 생산자들이 건전한 현금 흐름에도 불구하고 기계 구매를 지연하고 있다고 지적하며, 이는 단가 상승과 자금 조달 경직을 반영합니다. AGCO Corporation의 2025년 1분기 매출은 30% 감소했는데, 이는 비용에 민감한 구매자들이 자본 예산을 축소하고 있음을 시사합니다. 유지보수 부담은 현대식 콤바인과 트랙터가 전용 진단 소프트웨어, 클라우드 구독, 전문 기술자를 필요로 한다는 점에서 장벽을 가중시킵니다. 보조금 지원이 있더라도 많은 소규모 농장에서는 수명 주기 비용이 부담스러워 영국 농기계 시장 예상 확장 규모가 축소되고 있습니다.

부문 분석

2024년 영국의 농업 기계 시장에서 트랙터는 55.2%의 점유율을 차지했습니다. 부문 성장은 교체 주기와 마력 업그레이드에 여전히 의존하며, 자율 주행 및 텔레매틱스 통합이 기본 사양으로 자리잡고 있습니다. 트랙터 내에서는 100마력 미만 모델이 판매량을 주도하지만, 150마력 이상의 고출력 기계는 프리미엄 가격과 풀스택 기술로 인해 수익에서 불균형적으로 높은 비중을 차지합니다. 디어 앤 컴퍼니(Deere & Company)의 압도적 점유율은 통합 가이드 시스템, 연결성, 애프터서비스 네트워크의 중요성을 부각시키며, 이는 영국의 농업 기계 시장 전반의 총소유비용(TCO) 절감으로 이어집니다.

관개 기계는 2030년까지 연평균 8.2% 성장률(CAGR) 전망을 기록하며 모든 카테고리 중 가장 높은 성장세를 보일 것으로 예상됩니다. 이는 예측 불가능한 강우량과 강화되는 취수 허가 규제의 직접적인 대응책입니다. 토양 수분 센서와 결합된 피벗 시스템은 농장이 환경청의 물 관리 지침을 준수하도록 돕는 반면, 드립 기술은 고부가가치 원예 분야에서 점차 확산되고 있습니다. 정밀 관개는 유출수와 투입물 낭비를 줄여 재생 가능 목표를 지원하며, 기후 변동성이 영국 농업 기계 시장 규모 프레임워크 내에서 제품 다각화를 어떻게 주도하는지 보여줍니다. 수확기, 사료용 기계, 경운 기계 역시 꾸준한 수요를 보이지만, 농장 운영에서 물 관리의 중요성이 부각되면서 관개 기계에 비해 성장세가 뒤처지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 노동력 부족으로 가속화되는 기계화

- 농업 기계에 대한 정부 보조금 제도 및 세금 감면

- 정밀농업과 디지털화 수요

- 재생 농업 인센티브로 인한 저압축 기계 수요 증가

- 농업용 로봇 테스트베드 확대로 인한 프로토타입 도입 촉진

- 탄소중립 전기화 의무화 정책이 전기 트랙터 구매 촉진

- 시장 성장 억제요인

- 높은 초기 구입비 및 유지보수 비용

- 연결된 기계의 사이버 보안 및 데이터 프라이버시 위험

- 농촌 전력망 용량 한계로 인한 전기 기계 도입 지연

- 브렉시트 이후 인증 기준 차이 확대로 인한 규정 준수 비용 증가

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측

- 기계 유형별

- 트랙터

- 50마력 미만

- 50-100마력

- 100-150마력

- 150마력 초과

- 기기

- 쟁기

- 해로우

- 경운기 및 틸러

- 기타 기기(파종기, 롤러 등)

- 관개 기계

- 스프링클러 관개

- 점적 관개

- 기타 관개 기계(센터 피벗 시스템, 마이크로 스프링클러 등)

- 수확 기계

- 콤바인 수확기

- 사료 수확기

- 기타 수확기(감자 수확기, 비트 수확기 등)

- 건초 기계

- 잔디 깎기기계 및 컨디셔너

- 베일러

- 기타 건초 기계(레이크, 테더)

- 기타 기계류

- 트랙터

제6장 경쟁 구도

- 시장의 집중도

- 전략적 움직임

- 시장 점유율 분석

- 기업 프로파일

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Claas KGaA mbH

- JC Bamford Excavators Ltd.

- Kuhn Group(Bucher Industries AG)

- SDF Group SpA

- Bernard Krone Holding SE & Co. KG

- Horsch Maschinen GmbH

- Amazone-Werke H. Dreyer SE & Co. KG

- GRIMME Landmaschinenfabrik GmbH & Co. KG

- LEMKEN GmbH & Co. KG

- Vaderstad Group

제7장 시장 기회와 전망

HBR 25.11.10The United Kingdom agricultural machinery market size stands at USD 2.25 billion in 2025 and is projected to advance to USD 2.91 billion by 2030, delivering a steady 5.3% CAGR during the forecast period.

This upward trajectory underscores the sector's resilience amid post-Brexit regulation, persistent labor shortages, and accelerating on-farm automation. Over the next five years, equipment purchases will be buoyed by the Farming Equipment and Technology Fund, a GBP 50 million (USD 63 million) grant program that directly offsets capital costs for productivity-enhancing machinery. Demand is also influenced by the Clean Power 2030 Action Plan, which channels investment toward low-emission electric and hydrogen tractors that help farms meet the national net-zero target for 2030. Meanwhile, the Expansion of agri-robotics testbeds, supported by the Smart Machines Strategy 2035, is fostering rapid prototype adoption and attracting technology partnerships across research clusters.

United Kingdom Agricultural Machinery Market Trends and Insights

Shortage of labor accelerating mechanization

More than 40% of British farms report an insufficient workforce, a figure that has intensified capital outlays toward autonomous and semi-autonomous machinery capable of substituting manual labor. Seasonal-worker visas have been extended to 45,000 positions through 2029, yet government policy is simultaneously investing GBP 50 million (USD 63 million) in automation to reduce long-term reliance on migrant labor. Fieldwork Robotics' raspberry-picking system exemplifies how continuous operation and human-comparable throughput shift return-on-investment calculations in favor of robotics. As labor costs rise, specification requirements move toward equipment that can work longer hours with limited oversight, reinforcing demand across the United Kingdom agricultural machinery market.

Government grant schemes and tax relief on farm machinery

The Farming Equipment and Technology Fund awards between GBP 1,000 and GBP 25,000 (USD 1,250 to USD 31,250) per applicant, while the Improving Farm Productivity program finances up to GBP 500,000 (USD 625,000) for robotics and precision systems. Each funded item must remain in use for five years, providing equipment suppliers with predictable demand cycles. Grant scoring frameworks prioritize carbon reduction and animal welfare metrics, steering purchases toward sensor-rich implements, autonomous guidance, and low-compaction solutions. These incentives directly lift overall equipment turnover within the United Kingdom agricultural machinery market, especially for small and mid-sized farms that historically delayed high-ticket investments.

High upfront and maintenance costs

The Institute of Chartered Accountants in England and Wales notes that large producers are delaying equipment purchases despite healthy cash flows, reflecting rising unit prices and tighter financing. AGCO Corporation's Q1 2025 revenue fell 30%, a signal that cost-sensitive buyers are pruning capital budgets. Maintenance burdens compound the hurdle modern combines and tractors require proprietary diagnostic software, cloud subscriptions, and specialized technicians. Even with grant offsets, many small operations find lifecycle costs prohibitive, trimming projected expansion of the United Kingdom agricultural machinery market.

Other drivers and restraints analyzed in the detailed report include:

- Regenerative-farming incentives driving low-compaction equipment demand

- Net-Zero electrification mandates catalyzing electric tractor purchases

- Cybersecurity and data privacy risks in connected machinery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractors accounted for a 55.2% share of the United Kingdom agricultural machinery market in 2024. Segment expansion remains tethered to replacement cycles and horsepower upgrades, with autonomous and telematics integration becoming default specifications. Within tractors, models under 100 horsepower dominate volume, yet high-horsepower units above 150 horsepower capture disproportionate revenue due to their premium pricing and full-stack technology. Deere & Company's majority share highlights the importance of integrated guidance, connectivity, and after-sales networks that lower the total cost of ownership across the United Kingdom agricultural machinery market.

Irrigation equipment posted an 8.2% CAGR outlook through 2030, the strongest among all categories, and a direct response to unpredictable rainfall and tightening abstraction permits. Pivot systems coupled with soil-moisture sensors help farms align with the Environment Agency's water-management directives, while drip technology gains traction in high-value horticulture. Precision irrigation supports regenerative objectives by reducing runoff and input waste, underscoring how climate volatility drives product diversification within the United Kingdom agricultural machinery market size framework. Harvesters, forage machinery, and tillage implements also report steady demand, but their growth trails irrigation as water stewardship rises on farm agendas.

The United Kingdom Agricultural Machinery Market Report is Segmented by Machinery Type (Tractor, Equipment, Irrigation Machinery, Harvesting Machinery, Haying and Forage Machinery, and Other Machinery Types). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Claas KGaA mbH

- J.C. Bamford Excavators Ltd.

- Kuhn Group (Bucher Industries AG)

- SDF Group S.p.A.

- Bernard Krone Holding SE & Co. KG

- Horsch Maschinen GmbH

- Amazone-Werke H. Dreyer SE & Co. KG

- GRIMME Landmaschinenfabrik GmbH & Co. KG

- LEMKEN GmbH & Co. KG

- Vaderstad Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shortage of labor accelerating mechanization

- 4.2.2 Government grant schemes and tax relief on farm machinery

- 4.2.3 Demand for precision agriculture and digitalization

- 4.2.4 Regenerative-farming incentives driving low-compaction equipment demand

- 4.2.5 Expansion of agri-robotics testbeds boosting prototype uptake

- 4.2.6 Net-Zero electrification mandates catalyzing electric tractor purchases

- 4.3 Market Restraints

- 4.3.1 High upfront and maintenance costs

- 4.3.2 Cybersecurity and data privacy risks in connected machinery

- 4.3.3 Rural grid-capacity limits slowing electric-equipment adoption

- 4.3.4 Post-Brexit certification divergence escalating compliance costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Machinery Type

- 5.1.1 Tractor

- 5.1.1.1 Less than 50 HP

- 5.1.1.2 50 to 100 HP

- 5.1.1.3 100 to 150 HP

- 5.1.1.4 Above 150 HP

- 5.1.2 Equipment

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Equipment (Seed Drills, Rollers, etc.)

- 5.1.3 Irrigation Machinery

- 5.1.3.1 Sprinkler Irrigation

- 5.1.3.2 Drip Irrigation

- 5.1.3.3 Other Irrigation Machinery (Center Pivot Systems, Micro Sprinklers, etc.)

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting Machinery (Potato Harvesters, Beet Harvesters, etc.)

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers and Conditioners

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage Machinery (Rakes, Tedders)

- 5.1.6 Other Machinery Types

- 5.1.1 Tractor

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Claas KGaA mbH

- 6.4.6 J.C. Bamford Excavators Ltd.

- 6.4.7 Kuhn Group (Bucher Industries AG)

- 6.4.8 SDF Group S.p.A.

- 6.4.9 Bernard Krone Holding SE & Co. KG

- 6.4.10 Horsch Maschinen GmbH

- 6.4.11 Amazone-Werke H. Dreyer SE & Co. KG

- 6.4.12 GRIMME Landmaschinenfabrik GmbH & Co. KG

- 6.4.13 LEMKEN GmbH & Co. KG

- 6.4.14 Vaderstad Group