|

시장보고서

상품코드

1850357

인적 자본 관리 소프트웨어 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Human Capital Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

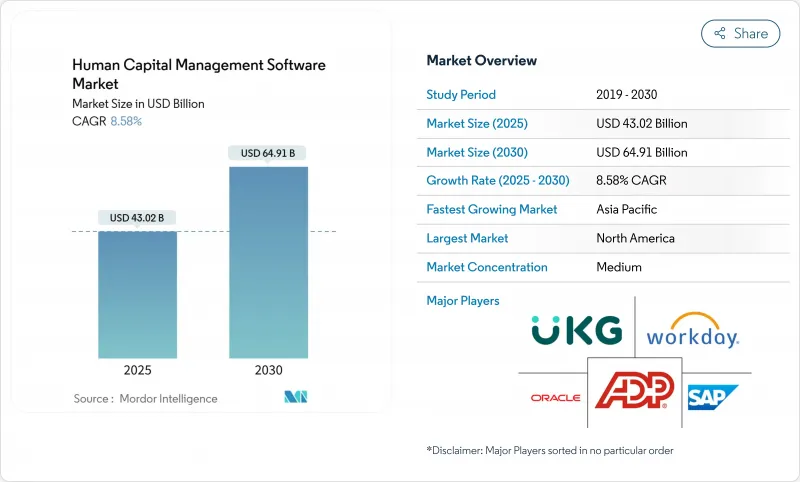

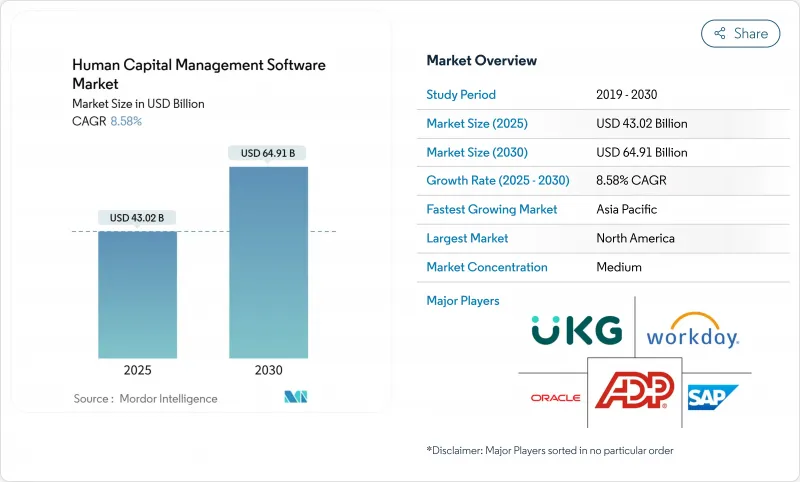

인적 자본 관리 소프트웨어 시장 규모는 2025년에 430억 2,000만 달러, 2030년에는 649억 1,000만 달러에 이르고, CAGR 8.6%를 나타낼 것으로 예측됩니다.

클라우드 마이그레이션, 임베디드 인공지능 및 지속적인 세계 컴플라이언스 자동화는 RFP 설계부터 계약 갱신에 이르기까지 구매 사이클의 모든 단계를 재구성하는 구조적인 힘이 되었습니다. 이사회는 현재 통합 클라우드 네이티브 HR 스위트를 급여 평등 조정, 세금 변경, 개인 정보 보호 의무를 자동화하는 동시에 생산성과 정착률을 높이는 실시간 노동력 분석을 제공하는 필수적인 위험 완화 도구로 간주하고 있습니다. 중소기업에서는 구독 기반의 도입으로 기존 On-Premise형 인사 시스템과 관련된 자본 비용이나 IT 부서의 인원이 필요 없기 때문에 도입이 가속화되고 있습니다. 보편적인 데이터 모델, 모바일 우선 워크 플로우 및 투명성이 높은 AI 파이프라인을 제공할 수있는 공급업체는 불균형 한 점유율을 얻고 있지만 레거시 아키텍처에 묶인 후 출발 업체는 업데이트를 잃고 있습니다. 북미의 확대 사건의 3분의 1 이상은 머신러닝 주도 목표 설정, 이직 리스크 스코어링, 스킬 매칭을 기본 권리로 번들어 AI가 더 이상 옵션을 추가하는 것이 아니라 기본적인 요구 사항임을 보여줍니다.

세계의 인적 자본 관리 소프트웨어 시장 동향과 인사이트

클라우드 네이티브 HCM 플랫폼으로 이동

클라우드로의 전환은 하드웨어 혁신에서 이사회 수준의 의무화로 진행되고 있습니다. 인사 부문 리더의 90% 이상이 클라우드 분석 및 자동 업데이트 컴플라이언스 엔진을 활용하기 위한 예산을 확보하거나 늘릴 계획입니다. 실시간 세액표 푸시 및 관할 지역별 급여 평등 규칙은 단일 코드 행으로 제공되므로 분기별 패치 백로그를 없앨 수 있습니다. 그러나 이러한 기능을 이용할 준비가 완전히 갖추어져 있다고 응답한 고용주는 불과 22%에 불과하고, 구현 파트너와 전문 서비스 팀이 수익화에 약기되고 있는 실행 갭이 남아 있습니다. 중견 기업의 구매자는 데이터센터를 유지하지 않고 엔터프라이즈급 애널리틱스를 얻을 수 있기 때문에 새로운 로고 수를 지배하고 있지만 대기업은 현재 컨테이너화된 마이크로서비스를 채택하면서 이전 맞춤 로직을 유지하는 단계적 마이그레이션 RFP를 발행하고 있습니다. 인적 자본 관리 소프트웨어 시장에서 모든 공급업체는 멀티테넌트 규모, 소블린 클라우드 옵션, 다운타임 없이 업그레이드를 제공함으로써 긴 보안 문제를 제거하는 것을 로드맵의 중심에 두고 있습니다.

통합인력과 급여계산 스위트가 인기를 끌

탤런트 엔진과 페이롤 엔진을 단독으로 사용하면 비용이 많이 드는 데이터 조합이 발생하여 분석의 정확성이 저하됩니다. 현재 85%의 고용주가 최소 2개의 유료 HR 제품을 라이선스 계약하고 있으며, 상거래 조건이 허용하는 한 통합을 진행하고 있습니다. 아시아태평양에서 급성장하는 기업은 1세대 디지털화 시 통합 제품군을 도입하고, 기술적 부채를 회피하며, 구미 도입 곡선을 뛰어넘고 있습니다. 컨버전스는 또한 더 풍부한 인사이트를 끌어냅니다. 급여 데이터는 실시간 예산 제약을 표면화하고, 인재 모듈은 기술 격차를 밝히고, 학습 결과에 연결된 알고리즘을 통해 보상 제안을 가능하게 합니다. 임금, 기술, 자격, 업적을 다루는 통합 오브젝트 모델에 투자하는 공급업체는 인수한 코드 기반을 연결하는 동업자를 능가하고 있으며, 이러한 경향은 인적 자본 관리 소프트웨어 시장의 갱신 가격에도 나타났습니다.

사이버 보안 및 데이터 프라이버시 우려

GDPR(EU 개인정보보호규정), CCPA, CPRA, 브라질의 LGPD는 데이터 보유, 거주 및 직원 동의에 엄격한 제약을 부과합니다. 인사 데이터베이스에는 은행의 상세 정보, 사회 보장 번호, 실적 메모 등이 포함되어 있으며 자격 증명 공격의 모습의 표적이 되고 있습니다. 따라서 구매자는 ISO 27001 인증, 제로 트러스트 네트워크 설계 및 지속적인 침입 테스트를 최우선 선정 기준으로 삼고 있습니다. 새로운 장애물은 애널리틱스의 성능을 유지하면서 개인 식별 정보를 전송 및 저장하는 동안 모두 암호화한다는 것을 증명하는 것입니다. 공급업체는 인메모리 토크나이제이션 및 속성 기반 액세스 제어를 통해 지원되지만 이러한 향상은 롤아웃 일정을 장기화하고 총 소유 비용을 증가시켜 인적 자본 관리 소프트웨어 시장의 성장을 억제합니다.

부문 분석

급여 계산은 여전히 HR 기술의 핵심이며 인적 자본 관리 소프트웨어 시장에서 2024년 매출의 38.0%를 차지했습니다. 그 중요성은 직원에게 정확하고 기한 내에 급여를 지불하는 법적 요건으로 인해 발생하며 아웃소싱 지연은 허용되지 않습니다. 그러나 학습과 개발은 2030년까지 CAGR 9.5%를 나타낼 전망입니다. 스킬 부족으로 고민하는 경영 간부는 채용 비용의 상승과 결원 기간의 장기화를 피하기 위해 사내 인력의 스킬 업을 선호하고 있습니다. 학습 카탈로그, 자격 추적 및 지도 워크플로우를 급여 계산과 동일한 플랫폼에 통합하여 폐쇄 피드백 루프를 실현합니다. AI는 미세 자격 취득과 임금 상승을 연관시킬 수 있으며, 참여도를 높이는 동시에 임금 평등 보고를 만족시킬 수 있습니다.

급여계산이나 학습뿐만 아니라, 인재 관리나 워크포스 매니지먼트의 큐브에 대한 수요도 견조하게 추이하고 있어, 스케줄링이나 잔업의 승인, 보수의 증액에 도움이 되는 통일된 퍼포먼스 데이터를 요구하는 고용주가 그 원동력이 되고 있습니다. 핵심 인사 관리는 테이블 스테이크스 모듈로 유지되지만, 부가가치가 높은 애널리틱스와 번들되지 않는 한 공급업체 선택에 영향을 미치지 않습니다. 진화하는 인적 자본 관리 소프트웨어 시장에서 제공업체는 코스 마켓플레이스, 기술 온톨로지, 내부 기그마켓 모듈을 통합하여 컴플라이언스 의무에서 전략적 생산성 엔진으로 학습을 강화하고 있습니다. 고객이 성과 지향 용도으로 예산을 전환하기 때문에 재구성에 실패한 공급자는 월렛 점유율이 저하됩니다.

On-Premise는 2024년 기준에서도 매출의 68.4%를 차지했지만, 이는 10년 전 ERP의 의사결정의 유산입니다. 공공 부문과 규제가 엄격한 고객 중 상당수는 데이터 주권 조항과 통합 얽힘으로 인해 마이그레이션에 저항합니다. 그러나 클라우드 도입은 CAGR 10.1%로 증가하고 있으며, 인적 자본 관리 소프트웨어 시장을 구독 퍼스트 시대로 밀어 올리고 있습니다. 구매자는 다운타임 없이 분기별 기능 추가 및 보안 패치를 받으면서 설비 투자를 고정 자산세로 전환할 수 있다는 점을 높이 평가합니다. 계약에는 1시간 이하의 컴플라이언스 푸시 및 실시간 분석 샌드박스가 포함되며 정적 On-Premise 스택으로는 얻을 수 없는 이점이 있습니다.

개인정보나 급여 계산은 프라이빗 클라우드나 소블린 클라우드에서 실시하고, 프론트엔드의 분석은 하이퍼스케일러의 인스턴스로 실시하는 하이브리드인 패턴도 나오고 있습니다. 컨테이너화된 서비스와 Infrastructure-as-Code 블루프린트를 제공하는 공급업체는 마이그레이션 불안을 완화하기 위해 도입 예산을 획득했습니다. 궁극적으로는 인공지능의 기능속도가 보수적인 섹터조차도 On-Premise의 보유를 재평가할 수밖에 없는 변곡점이 생겨, 인적 자본 관리 소프트웨어 시장은 클라우드 우위로 더욱 기울어질 것으로 보입니다.

인적 자본 관리 소프트웨어 시장 보고서는 솔루션별(급여 관리, 탤런트 관리, 워크포스 관리 등), 배포별(On-Premise, 클라우드), 조직 규모별(대기업, 중소기업), 업계별(IT 및 통신, BFSI 등), 지역별로 분류되어 있습니다.

지역 분석

북미는 인적 자본 관리 소프트웨어 시장에서 2024년 매출의 43.1%를 차지했습니다. 오랫동안 SaaS에 대한 친숙함, 강력한 벤처 자금 및 구현 파트너 생태계가 업그레이드 사이클에 박차를 가하고 있습니다. 임금평등에 관한 법규제가 보고모듈의 채용을 가속. 캘리포니아 주에서만 성별과 인종 범주에 걸친 임금의 중앙값 공개가 의무화되어 실시간 분석의 인센티브가 되고 있습니다. 벤더는 AI에 의한 설명의 용이성과 워크플로우의 확장성으로 차별화를 도모하고 있습니다. 환승 비용은 여전히 높지만 소비자 급 모바일 UX와 투명성이 높은 가격 설정을 약속하는 신규 진출기업은 급속히 직원 수를 확대하는 벤처 기업들 사이에서 발판을 발견하고 있습니다.

독일, 프랑스, 북유럽은 각각 독자적인 노동 협의회 워크플로우를 부과합니다. GDPR(EU 개인정보보호규정)은 엄격한 데이터 주권 심사를 추진하고 많은 구매자는 국경 내 데이터센터를 요청합니다. 기밀성이 높은 인사 파일은 로컬에 위치하고 머신러닝 워크로드는 EU 인증 공용 클라우드에서 실행됩니다. 지속가능성 증명과 책임있는 AI에 대한 헌신은 점점 더 조달에 영향을 미치고 있습니다. 공급업체는 입찰 점수를 통과하기 위해 에너지 효율적인 데이터센터와 편견 완화 프레임워크를 강조합니다.

아시아태평양은 CAGR 9.6%로 가장 빠르게 성장하고 있습니다. 인도에서 인도네시아까지 정부가 중소기업의 디지털화를 조성하고 1세대 급여계산과 근태 관리 구매를 촉진하고 있습니다. 모바일 퍼스트의 기능이 주류로, 현장 기반의 직원에 대응. 각 지역공급자는 법정 신고서, 전자 지갑에 의한 출납, 현지 언어로 채팅 봇 지원을 통합함으로써 성공을 거두고 있지만, 고급 분석을 위해 세계 스위트와 제휴하는 경우가 많습니다. 다국적 기업은 중국, 일본, 동남아시아에서 통일된 프로세스를 요구하고 있으며, 벤더는 언어 팩과 국내 세무 컨텐츠의 확충을 진행하고 있습니다. 인적 자본 관리 소프트웨어 시장에서 이 지역은 2층 구조를 보여줍니다. 규제의 뉘앙스를 소유하는 로컬 챔피언과 AI가 풍부한 애널리틱스를 공급하는 세계 선도적입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 클라우드 네이티브 HCM 플랫폼으로의 전환

- 통합된 인재·급여 계산 스위트가 보급

- 전략적인사를 위한 인재 분석과 AI

- 세계 급여 계산과 세무에 관한 컴플라이언스 의무

- 임금평등법이 보수 도구를 촉진

- 데스크레스 워커나 기그 워커용 모바일 퍼스트 HCM

- 시장 성장 억제요인

- 사이버 보안 및 데이터 프라이버시에 대한 우려

- 레거시 전환의 비용과 복잡성

- 복잡한 스위트의 최종 사용자에 의한 낮은 채용률

- AI 바이어스 소송 리스크가 전개를 제한

- 밸류체인 분석

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 솔루션별

- 급여 관리

- 인재 관리

- 인력 관리

- 핵심 인사 행정

- 학습 및 개발

- 배포별

- On-Premise

- 클라우드

- 조직 규모별

- 대기업

- 중소기업

- 업계별

- IT 및 통신

- BFSI

- 제조업

- 헬스케어

- 소매업 및 전자상거래

- 정부 및 공공 부문

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임과 전개

- 시장 점유율 분석

- 기업 프로파일

- SAP SE

- Oracle Corporation

- Workday Inc.

- ADP LLC

- Ceridian HCM Holding Inc.

- UKG(Ultimate Kronos Group)

- Infor

- Cornerstone OnDemand Inc.

- IBM Corporation

- Ramco Systems

- BambooHR LLC

- Zoho Corporation(Zoho People)

- Namely Inc.

- Gusto Inc.

- Paycom Software Inc.

- Sage Group plc

- Epicor Software Corporation

- SumTotal Systems LLC

- PeopleFluent Inc.

- Meta4(Cegid)

- Talentia Software

- OrangeHRM Inc.

- Rippling

- Deel Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.10The human capital management software market size is valued at USD 43.02 billion in 2025 and is projected to reach USD 64.91 billion by 2030, expanding at an 8.6% CAGR.

Cloud migration, embedded artificial intelligence, and always-on global compliance automation are the structural forces reshaping every stage of the purchase cycle, from RFP design to contract renewal. Boards now view integrated, cloud-native HR suites as essential risk-mitigation tools that automate pay-equity adjustments, tax changes, and privacy obligations, while simultaneously delivering real-time workforce analytics that lift productivity and retention. Small and medium enterprises are accelerating adoption because subscription-based deployments eliminate the capital costs and IT headcount traditionally associated with on-premise HRIS, creating a two-speed environment inside the human capital management software market where SME agility meets large-enterprise complexity. Vendors that can deliver universal data models, mobile-first workflows, and transparent AI pipelines are capturing a disproportionate share, whereas laggards tethered to legacy architectures are losing renewals. Over one-third of North American expansion deals already bundle machine-learning-driven goal-setting, attrition risk scoring, and skills matching as default entitlements, signaling that AI is no longer an optional add-on but a baseline requirement.

Global Human Capital Management Software Market Trends and Insights

Shift to Cloud-Native HCM Platforms

Cloud migration has progressed from hardware refresh to board-level mandate. Over 90% of HR leaders plan to protect or increase budgets specifically to unlock cloud analytics and auto-updated compliance engines. Real-time tax table pushes and jurisdiction-specific pay-equity rules arrive inside a single code line, eliminating quarterly patch backlogs. Yet only 22% of employers report full readiness to harness those capabilities, leaving an execution gap that implementation partners and professional-services teams are keen to monetize. Mid-market buyers dominate new-logo counts because they gain enterprise-class analytics without maintaining data centers, but large enterprises are now issuing phased migration RFPs that preserve prior custom logic while adopting containerized microservices. Within the human capital management software market, every provider's roadmap now centers on delivering multi-tenant scale, sovereign-cloud options, and zero-downtime upgrades to neutralize lingering security objections.

Integrated Talent and Payroll Suites Gain Traction

Stand-alone talent or payroll engines create costly data reconciliations that impede analytics accuracy. Eighty-five percent of employers currently license at least two paid HR products and are consolidating wherever commercial terms allow. In Asia-Pacific, fast-growing organizations deploy unified suites during first-generation digitization, avoiding technical debt and leapfrogging Western adoption curves. Convergence also unlocks richer insights: payroll data surfaces real-time budget constraints, while talent modules expose skills gaps, enabling algorithmic compensation recommendations linked to learning achievements. Vendors that invest in a unified object model-covering wages, skills, credentials, and performance-outperform peers still stitching together acquired codebases, a dynamic increasingly visible in renewal pricing inside the human capital management software market.

Cyber-Security and Data-Privacy Concerns

GDPR, CCPA, CPRA, and Brazil's LGPD impose strict constraints on data retention, residency, and employee consent. HR databases contain bank details, social-security numbers, and performance notes-prime targets for credential-stuffing attacks. Buyers, therefore, elevate ISO 27001 certification, zero-trust network designs, and continuous penetration testing to top selection criteria. The new hurdle is proving encryption of personally identifiable information both in transit and at rest while maintaining analytics performance. Vendors are responding with in-memory tokenization and attribute-based access controls, but those enhancements lengthen rollout timelines and raise total cost of ownership, tempering growth inside the human capital management software market.

Other drivers and restraints analyzed in the detailed report include:

- Workforce Analytics and AI for Strategic HR

- Compliance Mandates for Global Payroll and Taxation

- Legacy Migration Cost and Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Payroll remains the backbone of HR technology, accounting for 38.0% of 2024 revenue in the human capital management software market. Its criticality stems from legal requirements to pay employees accurately and on time, leaving little room for outsourcing delays. However, Learning and Development is advancing at a 9.5% CAGR toward 2030. Executives battling skill shortages prefer upskilling internal talent to avoid escalating recruiting costs and protracted vacancy periods. Incorporating learning catalogues, credential tracking, and mentorship workflows into the same platform that runs payroll unlocks a closed feedback loop: AI can correlate micro-credential completion with wage progression, boosting engagement while satisfying pay-equity reporting.

Beyond payroll and learning, demand for talent-management and workforce-management cubes remains steady, driven by employers seeking unified performance data that informs scheduling, overtime approval, and compensation bumps. Core HR Administration persists as a table-stakes module but rarely influences vendor selection unless bundled with value-add analytics. In the evolving human capital management software market, providers are embedding course marketplaces, skills ontologies, and internal gig-market modules to elevate learning from a compliance obligation to a strategic productivity engine. Those failing to retool will see wallet share erode as clients shift budget toward outcome-oriented applications.

On-premise still controls 68.4% of revenue in 2024, a legacy of decade-old ERP decisions. Many public-sector and highly regulated customers resist migration because of data-sovereignty clauses and integration tangles. Yet cloud implementations are climbing at a 10.1% CAGR, propelling the human capital management software market into a subscription-first era. Buyers appreciate converting capex to opex while gaining quarterly feature drops and security patches without downtime. Contracts now bundle sub-hour compliance pushes and real-time analytics sandboxes, benefits unattainable in static on-premise stacks.

A hybrid pattern is emerging: personal information and payroll calculations often remain on private or sovereign clouds, whereas front-end analytics run on hyperscaler instances for elasticity. Vendors offering containerized services and infrastructure-as-code blueprints capture implementation budgets because they reduce migration anxiety. Eventually, an inflection point will arise where artificial-intelligence feature velocity compels even conservative sectors to re-evaluate on-premise holdings, further tipping the human capital management software market toward cloud dominance.

The Human Capital Management Software Market Report is Segmented by Solution (Payroll Management, Talent Management, Workforce Management, and More), Deployment (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (IT and Telecom, BFSI, and More), and Geography.

Geography Analysis

North America controls 43.1% of 2024 revenue inside the human capital management software market. Longstanding SaaS familiarity, strong venture funding, and dense implementation-partner ecosystems fuel upgrade cycles. Pay-equity legislation accelerates reporting module adoption; California alone mandates median-pay disclosure across gender and race categories, incentivizing real-time analytics. Vendors differentiate on AI explainability and workflow extensibility because functionality parity exists across payroll, benefits, and learning. Switching costs remain high, yet new entrants that promise consumer-grade mobile UX and transparent pricing still find footholds among venture-backed firms scaling headcount rapidly.

Europe presents a mosaic of labor codes; Germany, France, and the Nordics each impose unique works-council consultation workflows. GDPR drives strict data-sovereignty reviews; many buyers demand data centers within national borders. Hybrid deployments lead: sensitive HR files stay local, while machine-learning workloads run on EU-accredited public clouds. Sustainability credentials and responsible-AI commitments increasingly influence procurement; vendors highlight energy-efficient data centers and bias-mitigation frameworks to pass tender scoring.

Asia-Pacific is the fastest-growing region at 9.6% CAGR. Governments from India to Indonesia subsidize SME digitization, driving first-generation payroll and attendance purchases. Mobile-first features dominate, catering to field-based workforces. Regional providers thrive by integrating statutory returns, e-wallet disbursements, and chatbot support in local languages, yet often partner with global suites for advanced analytics. Multinational corporations seek unified processes across China, Japan, and Southeast Asia, pushing vendors to expand language packs and in-country tax content. Within the human capital management software market, this region showcases a two-tier structure: local champions owning regulatory nuance and global giants supplying AI-rich analytics.

- SAP SE

- Oracle Corporation

- Workday Inc.

- ADP LLC

- Ceridian HCM Holding Inc.

- UKG (Ultimate Kronos Group)

- Infor

- Cornerstone OnDemand Inc.

- IBM Corporation

- Ramco Systems

- BambooHR LLC

- Zoho Corporation (Zoho People)

- Namely Inc.

- Gusto Inc.

- Paycom Software Inc.

- Sage Group plc

- Epicor Software Corporation

- SumTotal Systems LLC

- PeopleFluent Inc.

- Meta4 (Cegid)

- Talentia Software

- OrangeHRM Inc.

- Rippling

- Deel Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to cloud-native HCM platforms

- 4.2.2 Integrated talent and payroll suites gain traction

- 4.2.3 Workforce analytics and AI for strategic HR

- 4.2.4 Compliance mandates for global payroll and taxation

- 4.2.5 Pay-equity legislation spurs compensation tools

- 4.2.6 Mobile-first HCM for deskless and gig workforce

- 4.3 Market Restraints

- 4.3.1 Cyber-security and data-privacy concerns

- 4.3.2 Legacy migration cost and complexity

- 4.3.3 Low end-user adoption of complex suites

- 4.3.4 AI bias litigation risk restricts roll-outs

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Payroll Management

- 5.1.2 Talent Management

- 5.1.3 Workforce Management

- 5.1.4 Core HR Administration

- 5.1.5 Learning and Development

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Manufacturing

- 5.4.4 Healthcare

- 5.4.5 Retail and E-Commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN

- 5.5.3.6 Australia and New Zealand

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Workday Inc.

- 6.4.4 ADP LLC

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 UKG (Ultimate Kronos Group)

- 6.4.7 Infor

- 6.4.8 Cornerstone OnDemand Inc.

- 6.4.9 IBM Corporation

- 6.4.10 Ramco Systems

- 6.4.11 BambooHR LLC

- 6.4.12 Zoho Corporation (Zoho People)

- 6.4.13 Namely Inc.

- 6.4.14 Gusto Inc.

- 6.4.15 Paycom Software Inc.

- 6.4.16 Sage Group plc

- 6.4.17 Epicor Software Corporation

- 6.4.18 SumTotal Systems LLC

- 6.4.19 PeopleFluent Inc.

- 6.4.20 Meta4 (Cegid)

- 6.4.21 Talentia Software

- 6.4.22 OrangeHRM Inc.

- 6.4.23 Rippling

- 6.4.24 Deel Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment