|

시장보고서

상품코드

1910569

필드 프로그래머블 게이트 어레이(FPGA) - 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Field Programmable Gate Array (FPGA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

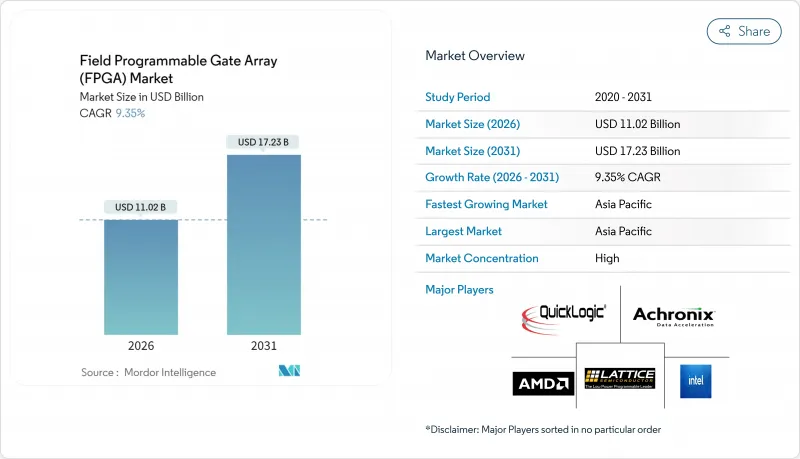

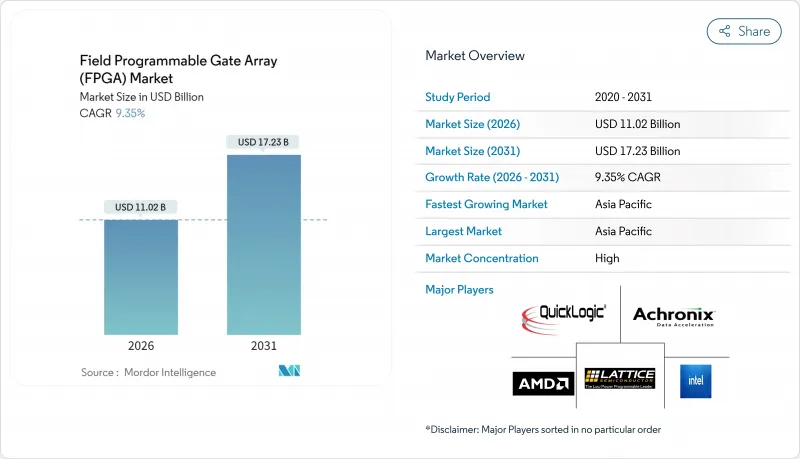

필드 프로그래머블 게이트 어레이(FPGA) 시장은 2025년 100억 8,000만 달러로 평가되었으며, 2026년 110억 2,000만 달러에서 2031년까지 172억 3,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)에 있어서 CAGR은 9.35%를 나타낼 것으로 전망되고 있습니다.

하이퍼스케일 데이터센터의 에지 AI 추론의 급속한 보급, 5G 오픈 무선 아키텍처로의 전환, 자동차 및 항공우주 일렉트로닉스기기 분야의 도입 후 재구성 가능성에 대한 수요 증가가 시장에 명확한 성장세를 가져왔습니다. 하이 엔드 디바이스가 수익의 기반을 유지하면서 설계 팀이 FPGA 기술을 비용 중심의 산업용, IoT, 민생 시스템에 전개함으로써 미드레인지 및 로우 엔드 제품이 급속히 성장했습니다. 아시아태평양은 전기자동차용 파워트레인과 신우주별자리 수요 증가를 통해 최대의 제조 거점 및 가장 빠른 성장 수요 센터로 대두했습니다. 인텔이 알테라를 분리 독립하기로 합의한 후 경쟁이 심화되고 공급업체의 역학이 재구성되었습니다. 한편, 수출규제는 중국에서 병행한 국내개발을 촉진했습니다. 300mm 파운드리 생산 능력의 박멸과 16nm 이하의 노드로의 고비용 마이그레이션도 벤더에게 고수익 용도 우선화와 TSMC 및 삼성과의 장기적인 웨이퍼 예약을 강요했습니다.

세계의 필드 프로그래머블 게이트 어레이(FPGA) 시장 동향 및 인사이트

하이퍼스케일 데이터센터의 에지 AI 추론 수요

하이퍼스케일 사업자는 대기 시간과 전력 예산이 순수한 처리량 요건을 초과하기 시작하면서 AI 추론을 가속화하기 위해 FPGA를 도입했습니다. AMD의 Versal AI Edge Gen 2 디바이스는 1세대 제품에 비해 최대 3배 높은 TOPS/와트 효율을 실현하여 운영 비용을 억제하면서 실시간 영상 분석을 가능하게 했습니다. Acronics는 대규모 언어 모델을 실행할 때 GPU 대체품에 비해 200%의 비용 및 전력 이점을 보고하고 메모리 제약 워크로드에서 FPGA의 효율성을 강조했습니다. 이 전환은 추론 처리가 데이터 소스에 근접한 분산 컴퓨팅 모델을 구현하여 대역폭 제약과 데이터 주권 위험을 완화했습니다. 주요 FPGA 제품군에 대한 온패키지 HBM 및 하드화 AI 엔진의 통합은 클라우드 에지 토폴로지의 지위를 강화했습니다. 그 결과, 필드 프로그래머블 게이트 어레이(FPGA) 시장은 하이퍼스케일 자본 지출 계획에서 지속적인 성장의 기둥을 발견했습니다.

5G ORAN 마이그레이션으로 무선 장치에 재프로그래밍 가능한 로직 필요

개방형 무선 액세스 네트워크를 통해 통신 사업자는 공급업체 독립적인 무선 장치를 채택해야 합니다. 이는 설비의 전반적인 업데이트가 아니라 소프트웨어 업그레이드를 통한 진화를 가능하게 합니다. 인텔의 Agilex 포트폴리오는 10nm SuperFin 기술을 채택하여 새로운 5G 릴리스에 적응하는 소프트웨어 정의 라디오를 구현하여 총 소유 비용을 줄였습니다. 래티스 세미컨덕터는 분산 네트워크를 위한 제로 트러스트 보안과 실시간암호화를 제공하는 레퍼런스 스택으로 이 하드웨어를 보완했습니다. AMD의 Zynq RFSoC DFE는 기존 장치에 비해 와트당 성능을 두 배로 늘리고 컴팩트하고 전력 제약이 있는 무선 헤드 내부에서 멀티밴드 작동을 가능하게 했습니다. 유연한 로직은 전개 사이클을 단축하고, 통신 사업자가 사설 5G, 고정 무선 액세스, mm파 서비스를 통합하는데 중요한 요소가 되었습니다. 이러한 유연성은 통신 인프라 전반에 걸친 필드 프로그래머블 게이트 어레이(FPGA) 시장에 새로운 대량 도입의 기회를 가져왔습니다.

고성능 FPGA의 중국용 수출 규제(미국·EU)

미국 산업안전보장국(BIS)의 신규규칙에 따라 2023년 말 중국용 선진 FPGA의 소비자용도 면제가 철폐되어 AI와 군용도에 적합한 디바이스 수출이 제한되었습니다. 이 변경으로 AMD-Xilinx와 Intel Altera는 많은 주문을 중단하거나 라이선스를 받았으며 단기 출하량이 감소했습니다. GOWIN 및 Pango와 같은 중국 공급업체가 공급 갭을 매립했지만 설계 도구, IP 및 고급 프로세스에 대한 액세스 장벽이 즉각적인 대체를 제한했습니다. 다국적 기업 고객은 중국에서 기밀성이 높은 생산을 이전하거나 비미국 장치를 지원하도록 시스템을 재설계하여 전 세계 공급망을 분리했습니다. 이로 인해 발생하는 불확실성은 새로운 무역 규범이 안정될 때까지 필드 프로그래머블 게이트 어레이(FPGA) 시장에 부담을 주었습니다.

부문 분석

2025년 하이엔드 디바이스는 필드 프로그래머블 게이트 어레이(FPGA) 시장 점유율의 65.80%를 차지했습니다. 이는 데이터센터 가속화와 5G 인프라의 핵심 역할을 반영합니다. 100만 로직 셀을 넘는 이러한 플랫폼은 고가격대이면서, GPU에서는 실현 불가능한 확정적인 레이턴시를 제공. 안전성이 매우 중요한 항공우주 분야와 핀테크 워크로드에 대한 수요를 유지했습니다. 중간 및 낮은 장치는 래티스와 같은 제조업체가 엣지 컴퓨팅 예산에 맞는 하드웨어 장착 AI 엔진이 장착된 비용 최적화 부품을 출하하여 2031년까지 연평균 복합 성장률(CAGR) 10.85%를 나타낼 전망입니다. 설계 툴은 보다 직관적으로 진화하여 하드웨어 전문 지식이 없는 임베디드 엔지니어에서도 구성 가능 로직을 채용할 수 있게 되었습니다.

AMD가 소비 전력 30% 삭감하고 비교할 수 없는 I/O 수를 자랑하는 Spartan UltraScale을 도입하여 상위에서 미드레인지 시장에 공세를 가함으로써 가치 제안은 진화했습니다. 동시에 모듈 공급업체는 사전 검증된 보드를 제공하여 핀아웃 계획 및 PCB 레이아웃을 추상화하여 설계 사이클을 단축했습니다. 이러한 변화에 의해 각 계층간의 가격차가 축소될 것으로 예상되지만, 새로운 AI나 네트워크 규격이 등장해, 최상위 노드의 실리콘만이 대응 가능한 경우, 하이엔드 디바이스가 필드 프로그래머블 게이트 어레이(FPGA) 시장 규모의 대부분을 차지해 계속할 전망입니다.

SRAM 기반 솔루션은 무제한 재프로그램 사이클과 깊은 소프트웨어 에코시스템을 통해 2025년 54.85%의 수익 점유율을 얻었으며 11.45%의 연평균 복합 성장률(CAGR) 전망을 보였습니다. 반면에 플래시 기반 변형은 즉각적인 시동이 필수적인 웨어러블 장비와 자동차 텔레매틱스 분야에서 인지도를 높여줍니다. 마이크로칩사의 RT PolarFire는 MIL-STD-883 클래스 B를 달성해, 동등한 SRAM 부품보다 50% 낮은 소비 전력으로 100 krad의 방사선 내성을 실현하고 있습니다. 안티 퓨즈 플랫폼은 방어 항공 전자 장비 분야에서 틈새 시장을 유지하고 있으며, 일회성 프로그래밍을 통해 변조 위험을 제거합니다.

소프트웨어의 이식성 향상으로 기존의 장벽이 축소되었기 때문에 설계자는 툴의 숙련도가 아니라 전력 소비와 보안에 따라 선택할 수 있게 되었습니다. 신흥 이기종 아키텍처는 SRAM 패브릭과 온다이 비휘발성 영역을 통합하여 두 가지 장점을 모두 제공합니다. SRAM 디바이스가 필드 프로그래머블 게이트 어레이(FPGA) 시장 수익을 계속 견인하는 반면, 플래시 및 안티퓨즈 제품은 저전력 및 가혹한 환경 용도에서 더 큰 점유율을 획득할 전망입니다.

필드 프로그래머블 게이트 어레이는 구성(하이 엔드 FPGA, 미드 레인지/로우 엔드 FPGA), 아키텍처(SRAM 기반 FPGA, 플래시 기반 FPGA 등), 기술 노드(90nm 이상, 20-90nm, 16nm 이하), 엔드 마켓(데이터센터·클라우드 컴퓨팅, 통신·5G 인프라, 자동차 등), 지역(북미, 유럽)

지역별 분석

아시아태평양은 2025년에 39.10%의 수익으로 필드 프로그래머블 게이트 어레이(FPGA) 시장을 견인해 2031년까지 연평균 복합 성장률(CAGR) 16.20%의 전망을 나타낼 전망입니다. 중국이 추진하는 반도체 자급자족정책은 전기자동차구동장치와 위성 페이로드 분야의 국내 이노베이터에 의해 현저해져 FPGA의 대규모 수요를 환기시켰습니다. 대만과 한국은 첨단 제조 기술을 제공하고 일본은 자동차 모듈과 공장 자동화 서브시스템을 전문으로 합니다. 래티스가 푸네에 연구개발센터를 개설함에 따라 인도의 설계서비스 부문은 진전되어 엔지니어링 인력 풀이 확대되었습니다.

북미는 데이터센터 인프라, 고신뢰성 항공우주, EDA 소프트웨어 분야에서 주도권을 유지했습니다. 하이퍼스케일러 기업은 AI 서비스 비용 관리를 위해 적응형 가속기에 거액의 자본 예산을 투입해, 이 지역의 강한 구매 점유율을 확보했습니다. 수출 라이선스 심사가 출하 패턴에 영향을 미친 반면, 필드 프로그래머블 게이트 어레이(FPGA) 시장을 지원하는 선진 패키징 기술과 OSAT(수탁 조립·테스트) 능력에 대한 국내 투자를 촉진했습니다.

유럽은 독일의 자동차 공급망과 북유럽 통신 장비 공급자에 의존했습니다. ISO 26262 규격이 자동차 용도를 촉진하는 반면, 에너지 전환 프로젝트는 저손실 전력 변환기에 대한 수요를 창출했습니다. EU Digital Decade 정책은 재구성을 중시하는 주권 엣지 컴퓨팅 플랫폼을 장려했습니다. 남미, 중동 및 아프리카는 현재 점유율이 작은 것, 5G 인프라와 산업 근대화에 있어서 성장 가능성이 예측 기간중의 공헌도 향상에 기여할 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이퍼스케일 데이터센터의 에지 AI 추론 수요

- 5G ORAN 이행에 수반하는 무선 기기에 있어서 재프로그램 가능 로직의 필요성

- ASIC/SoC의 미세화 사이클에서 신속한 프로토타이핑의 필요성(<=7 nm)

- 자동차 분야에서의 기능 안전 규격 준거(ISO 26262)

- 신우주별자리용 내방사선 설계

- 중국 EV 파워트레인 OEM 제조업체에 있어서 모터 제어용 eFPGA의 채용

- 시장 성장 억제요인

- 미국·EU에 의한 중국용 고성능 FPGA 수출 규제

- 300mm 파운더리 생산 능력 배분의 변동성

- 전용 ASIC에 비해 정적 소비 전력 증가

- 밸류체인 분석

- 규제 전망

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 동향이 FPGA 산업에 미치는 영향

제5장 시장 규모와 성장 예측

- 구성별

- 하이엔드 FPGA

- 미드레인지 및 로우 엔드 FPGA

- 아키텍처별

- SRAM 기반 FPGA

- 플래시 기반 FPGA

- 안티퓨즈 FPGA

- 기술 노드별

- 90nm 이상

- 20-90nm

- 16nm 이하

- 최종 시장별

- 데이터센터 및 클라우드 컴퓨팅

- 통신 및 5G 인프라

- 자동차(ADAS, 전동화)

- 산업 자동화 및 로봇공학

- 항공우주 및 방위(항공전자기기, 위성통신)

- 소비자용 전자기기 및 웨어러블 기기

- 테스트, 계측 및 의료기기

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 북유럽 국가(스웨덴, 노르웨이, 핀란드, 덴마크)

- 기타 유럽

- 아시아태평양

- 중국

- 대만

- 일본

- 한국

- 인도

- ASEAN

- 기타 아시아태평양

- 남미

- 멕시코

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Advanced Micro Devices Inc.(Xilinx)

- Intel Corporation

- Lattice Semiconductor Corp.

- Microchip Technology Inc.(Microsemi)

- Achronix Semiconductor Corp.

- QuickLogic Corporation

- Efinix Inc.

- GOWIN Semiconductor Corp.

- Flex Logix Technologies Inc.

- NanoXplore SAS

- Anlogic Infotech Co. Ltd.

- Pango Microsystems Inc.

- Shenzhen S2C Ltd.

- BittWare(Molex Company)

- Digilent Inc.

- AlphaData Parallel Systems Ltd.

- Colfax International

- Reflex Ces SAS

- Aldec Inc.

- Beijing Tsinghua Tongfang Co. Ltd.

제7장 시장 기회와 향후 전망

KTH 26.01.22The field programmable gate array market was valued at USD 10.08 billion in 2025 and estimated to grow from USD 11.02 billion in 2026 to reach USD 17.23 billion by 2031, at a CAGR of 9.35% during the forecast period (2026-2031).

Rapid adoption of edge-AI inference in hyperscale data centers, the migration to 5G open radio architectures, and the rising need for post-deployment reconfigurability in automotive and aerospace electronics gave the market clear momentum. High-end devices continued to anchor revenues, yet mid-range and low-end products climbed quickly as design teams pushed FPGA technology into cost-sensitive industrial, IoT, and consumer systems. Asia-Pacific emerged as both the largest manufacturing base and the fastest-growing demand center, benefiting from electric-vehicle powertrains and new-space constellations. Competitive intensity increased after Intel agreed to carve out Altera, reshaping supplier dynamics while export controls spurred parallel domestic development in China. Tighter 300 mm foundry capacity and the costly transition to <=16 nm nodes also forced vendors to prioritize high-margin applications and long-term wafer reservations with TSMC and Samsung.

Global Field Programmable Gate Array (FPGA) Market Trends and Insights

Edge-AI inference demand in hyperscale data centers

Hyperscale operators deployed FPGAs to accelerate AI inference once latency and power budgets began outweighing raw throughput requirements. AMD's Versal AI Edge Gen 2 devices delivered up to 3 X higher TOPS-per-watt than first-generation parts, enabling real-time vision analytics while containing operating expenses. Achronix reported 200 % cost and power advantages versus GPU alternatives when running large language models, underscoring FPGA efficiency in memory-bound workloads. This shift unlocked a distributed compute model where inference processing moved closer to data sources, easing bandwidth constraints and data-sovereignty risks. Integration of on-package HBM and hardened AI engines within leading FPGA families strengthened their position in cloud-edge topologies. Consequently, the field programmable gate array market found a durable growth pillar in hyperscale capital expenditure plans.

5G ORAN shift requiring re-programmable logic in radios

Open radio access network initiatives pushed carriers to adopt vendor-agnostic radio units that could evolve with software upgrades rather than forklift replacements. Intel's Agilex portfolio used 10 nm SuperFin technology to deliver software-defined radios that adapt to new 5G releases at a lower total cost of ownership. Lattice Semiconductor complemented that hardware with a reference stack providing zero-trust security and real-time encryption for disaggregated networks. AMD's Zynq RFSoC DFE doubled performance per watt versus prior devices, letting operators support multi-band operation inside compact, power-constrained radio heads. Flexible logic shortened rollout cycles, a critical factor as carriers blended private-5G, fixed-wireless access, and mmWave services. That flexibility secured a new volume opportunity for the field programmable gate array market across telecom infrastructure.

US-EU export controls on high-performance FPGAs to China

New Bureau of Industry and Security rules removed civilian exemptions for advanced FPGA shipments to China in late 2023, restricting devices suited for AI or military use. The shift forced AMD-Xilinx and Intel-Altera to halt or license-screen many orders, reducing near-term unit volumes. Chinese suppliers such as GOWIN and Pango sought to close the gap, yet hurdles in design tools, IP, and advanced process access limited immediate substitution. Multinational customers moved sensitive production away from China or redesigned systems to qualify non-US devices, fracturing previously global supply chains. The resulting uncertainty weighed on the field programmable gate array market until new trade norms stabilized.

Other drivers and restraints analyzed in the detailed report include:

- Rapid prototyping needs for ASIC/SoC shrink cycles (<=7 nm)

- Functional safety compliance in automotive (ISO 26262)

- Volatility in 300 mm foundry capacity allocation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-end devices held 65.80% of the field programmable gate array market share in 2025, reflecting their central role in data-center acceleration and 5G infrastructure. These platforms, often exceeding 1 million logic cells, carried premium ASPs yet delivered deterministic latency unavailable in GPUs, preserving their appeal for safety-critical aerospace and fintech workloads. Mid-range and low-end devices exhibited an 10.85% CAGR to 2031 as manufacturers like Lattice shipped cost-optimized parts with hardened AI engines that met edge-compute budgets. Design tools have grown more intuitive, letting embedded engineers adopt configurable logic without hardware backgrounds.

The value proposition evolved as AMD introduced Spartan UltraScale+ with 30% lower power and unrivaled I/O count, attacking the mid-range from above. Simultaneously, module vendors supplied pre-validated boards that abstracted pin-planning and PCB layout, trimming design cycles. These shifts are expected to compress the pricing gap between tiers, although high-end devices still command a majority of the field programmable gate array market size when new AI or networking standards emerge that only top-node silicon can satisfy.

SRAM-based solutions owned 54.85% revenue in 2025 and posted an 11.45% CAGR outlook thanks to unlimited reprogram cycles and a deep software ecosystem. Yet flash-based variants gained mindshare in wearables and automotive telematics, where instant-on behavior is vital. Microchip's RT PolarFire achieved MIL-STD-883 Class B, offering 50% lower power than equivalent SRAM parts while tolerating 100 krad radiation. Anti-fuse platforms sustained a niche in defense avionics where one-time programmability eliminates tampering risk.

Software portability is shrinking historical barriers, so designers can now choose based on power and security rather than tool familiarity. Emerging heterogeneous architectures integrate SRAM fabric with on-die non-volatile domains, providing the best-of-both options. While SRAM devices will continue leading the field programmable gate array market revenue, flash and anti-fuse offerings should carve larger shares in low-power and harsh-environment deployments.

Field Programmable Gate Array is Segmented by Configuration (High-End FPGA, and Mid-range/Low-end FPGA), Architecture (SRAM-Based FPGA, Flash-Based FPGA, and More), Technology Node (>=90 Nm, 20-90 Nm, and <=16 Nm), End Market (Data Centre and Cloud Computing, Telecommunications and 5G Infrastructure, Automotive, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific dominated the field programmable gate array market with 39.10% revenue in 2025 and showed a 16.20% CAGR outlook to 2031. China's push for semiconductor self-reliance, highlighted by domestic innovators in electric vehicle drives and satellite payloads, pulled in significant FPGA volumes. Taiwan and South Korea supplied advanced fabrication, while Japan specialized in automotive modules and factory automation subsystems. India's design-service sector advanced after Lattice opened an R&D center in Pune, broadening engineering talent pools.

North America maintained leadership in data-center infrastructure, high-reliability aerospace, and EDA software. Hyperscalers directed large capital budgets toward adaptive accelerators to manage AI service costs, ensuring the region's strong purchase share. Export-license reviews shaped shipment patterns but also prompted domestic investment in advanced packaging and OSAT capacity that supports the field programmable gate array market.

Europe leaned on Germany's automotive supply chain and Nordic telecom equipment providers. ISO 26262 compliance spurred in-vehicle usage, while energy-transition projects created demand for low-loss power converters. EU Digital Decade policies encouraged sovereign edge computing platforms that favor reconfigurability. Although South America and the Middle East, and Africa hold smaller slices today, growth potential in 5G infrastructure and industrial modernization should boost their contribution over the forecast period.

- Advanced Micro Devices Inc. (Xilinx)

- Intel Corporation

- Lattice Semiconductor Corp.

- Microchip Technology Inc. (Microsemi)

- Achronix Semiconductor Corp.

- QuickLogic Corporation

- Efinix Inc.

- GOWIN Semiconductor Corp.

- Flex Logix Technologies Inc.

- NanoXplore SAS

- Anlogic Infotech Co. Ltd.

- Pango Microsystems Inc.

- Shenzhen S2C Ltd.

- BittWare (Molex Company)

- Digilent Inc.

- AlphaData Parallel Systems Ltd.

- Colfax International

- Reflex Ces SAS

- Aldec Inc.

- Beijing Tsinghua Tongfang Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Edge-AI Inference Demand in Hyperscale Data Centres

- 4.2.2 5G ORAN Shift Requiring Re-programmable Logic in Radios

- 4.2.3 Rapid Prototyping Needs for ASIC/SoC Shrink Cycles (<=7 nm)

- 4.2.4 Functional Safety Compliance in Automotive (ISO 26262)

- 4.2.5 Radiation-Tolerant Designs for New-Space Constellations

- 4.2.6 Chinese EV Power-train OEMs Adopting eFPGAs for Motor Control

- 4.3 Market Restraints

- 4.3.1 US-EU Export Controls on High-performance FPGAs to China

- 4.3.2 Volatility in 300 mm Foundry Capacity Allocation

- 4.3.3 Higher Static Power Consumption vs. Dedicated ASIC

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Trends on the FPGA Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Configuration

- 5.1.1 High-end FPGA

- 5.1.2 Mid-range/Low-end FPGA

- 5.2 By Architecture

- 5.2.1 SRAM-based FPGA

- 5.2.2 Flash-based FPGA

- 5.2.3 Anti-fuse FPGA

- 5.3 By Technology Node

- 5.3.1 >=90 nm

- 5.3.2 20-90 nm

- 5.3.3 <=16 nm

- 5.4 By End Market

- 5.4.1 Data Centre and Cloud Computing

- 5.4.2 Telecommunications and 5G Infrastructure

- 5.4.3 Automotive (ADAS, Electrification)

- 5.4.4 Industrial Automation and Robotics

- 5.4.5 Aerospace and Defense (Avionics, SATCOM)

- 5.4.6 Consumer Electronics and Wearables

- 5.4.7 Test, Measurement and Medical Devices

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Nordics (Sweden, Norway, Finland, Denmark)

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Taiwan

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 India

- 5.5.3.6 ASEAN

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Mexico

- 5.5.4.2 Brazil

- 5.5.4.3 Argentina

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global and Market Overview, Core Segments, Financials, Strategy, Rank/Share, Products, Recent Moves)

- 6.4.1 Advanced Micro Devices Inc. (Xilinx)

- 6.4.2 Intel Corporation

- 6.4.3 Lattice Semiconductor Corp.

- 6.4.4 Microchip Technology Inc. (Microsemi)

- 6.4.5 Achronix Semiconductor Corp.

- 6.4.6 QuickLogic Corporation

- 6.4.7 Efinix Inc.

- 6.4.8 GOWIN Semiconductor Corp.

- 6.4.9 Flex Logix Technologies Inc.

- 6.4.10 NanoXplore SAS

- 6.4.11 Anlogic Infotech Co. Ltd.

- 6.4.12 Pango Microsystems Inc.

- 6.4.13 Shenzhen S2C Ltd.

- 6.4.14 BittWare (Molex Company)

- 6.4.15 Digilent Inc.

- 6.4.16 AlphaData Parallel Systems Ltd.

- 6.4.17 Colfax International

- 6.4.18 Reflex Ces SAS

- 6.4.19 Aldec Inc.

- 6.4.20 Beijing Tsinghua Tongfang Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment